a16z and the Mega-Funds Are Eating the Seed Round: A Decade of Data from 20 Top VCs Dissected

- Core Thesis: Mega-funds managing over $10 billion in assets are structurally flooding into the seed stage, transacting 3.7-4.2 times more frequently than the market average. However, large-scale deployment dilutes investment quality. The survival strategy for Emerging Managers (EMs) lies in avoiding the hot sectors (like AI) where giants are focused, and building advantages through pricing discipline and domain expertise.

- Key Factors:

- In the AI era, the average annual early-stage deal count for mega-funds has increased from 10.6 in the SaaS era to 23.9. Notably, a16z averages 76.8 deals per year, and 16 out of 20 mega-funds have early-stage allocation ratios at all-time highs, indicating a strategic shift from cyclical speculation to a structural mission.

- The seed market is severely bifurcated: the median seed round with mega-fund participation is $6.2 million, which is 4.4 times the overall US market median of $1.4 million. Furthermore, the 90th percentile valuation has soared to $93.7 million, doubling in four years.

- The conversion rate from seed to Series B for mega-fund-backed companies is 3.7-4.2 times the market average. However, when deal volume surges, this conversion rate plummets (e.g., Sequoia's fell from 46% to 14%), revealing that "deal volume discipline equals portfolio quality."

- 42% of mega-fund early-stage activity is concentrated in two sectors: Enterprise AI & Automation and AI Infrastructure, where all 20 funds are active. In contrast, sectors like Climate, Logistics, and PropTech have only 8-13 active participants, facing significantly lower competitive pressure.

- The "Danger Index" shows that General Catalyst, a16z, Sequoia, and Accel pose the greatest threat to EMs, as they simultaneously feature high deal volumes, nearly 50% early-stage allocation, and median round sizes below $5.5 million—directly in the pricing sweet spot for EMs.

- AI companies sacrifice profit for growth (with gross margins as low as 25%). Mega-funds, with their deep pockets, can sustain long-term structural bets, but this creates a fundamental vulnerability for EMs managing funds in the $25-75 million range.

Original Author: Pavel Prata

Original Translation: Deep Tide TechFlow

Introduction: Mega-funds managing over $10 billion are flooding into seed rounds at an unprecedented pace. Murph Capital pulled data from Harmonic to analyze the early-stage investment behavior of 20 top mega-funds across three cycles: the SaaS era, the zero-interest rate era, and the AI era. The conclusion is not simple: mega-funds' seed-to-Series B conversion rate is indeed 3.7-4.2 times the market average, but this advantage is quickly diluted when they deploy at scale. For emerging managers, room to survive still exists, but they must choose their赛道 wisely.

A month ago, I posted a tweet asking a simple question: Are mega-funds really taking over seed rounds, or does it just feel that way? After 65,000 views and hundreds of DMs, it was clear this question hit a nerve.

Emerging Managers (EMs) wrote in saying they felt the pressure but couldn't quantify it; LPs questioned: if a16z and Sequoia are already in the game, does it still make sense to invest in seed funds? Even the GPs of mega-funds themselves wanted to know how aggressively their competitors were deploying in the early stages.

@pavelprata tweeted: Are mega-funds really taking over seed rounds? I decided to study the early-stage behavior of the world's largest VC funds ($10B+ AUM) to answer a simple question: Should EMs worry about their structural advantage?

A broad consensus quickly formed, which I largely agree with:

- Mega-funds have significantly increased their seed round allocations, roughly tripling over the past decade.

- The market is large and fragmented enough that their share remains relatively small, concentrated mainly in the top quartile.

- Their core motivation isn't immediate capital returns, but rather gaining early access to talent, acquiring high-signal-to-noise data, and minimizing the risk of missing the next generational opportunity.

But consensus is just the starting point. Behind the broad trends lies a more interesting and uneven picture that you simply can't see without the data.

So we pulled data from Harmonic, collected the performance of 20 mega-funds across three eras (SaaS, ZIRP, AI), and tried to honestly answer: What is really happening in the seed market? Where exactly are mega-funds going? What impact is this having on pricing? Do EMs have real reason to worry?

Intuition vs. Data

Let's start with the research framework.

We relied on public information, supplemented by real-time data from Harmonic (covering over 30 million companies and 190 million people). On the timeline, we analyzed the past decade, divided into three eras:

- SaaS Era (2015-2019): 5 years of a normal market cycle. Cloud, SaaS, marketplaces, and fintech were the dominant narratives. Interest rates were normal, and the market had discipline.

- ZIRP Era (2020-2022): 3 years of zero interest rate policy. Capital was almost free, with various investors flooding into early stages seeking yield. Tiger Global and SoftBank seemed to appear in every meaningful funding round. The seed market was severely overheated, but in a chaotic way lacking structural logic.

- AI Era (2023-2026): From the launch of ChatGPT to today. A massive technological shock that gave birth to a new class of companies for which super-sized seed rounds have become the norm.

Technically we focus on seed rounds, but in practice, we included Pre-Seed and Seed Extension. The reason is simple: the boundaries of these early stages are often blurred or shifting, making precise distinctions counterproductive.

Now, for the main event. Frankly, before starting the research, I had a strong intuition: mega-funds were appearing on the early-stage radar with increasing frequency. This intuition largely came from social media – the logos of a16z, General Catalyst, and Sequoia were showing up more and more frequently in seed round announcements, accompanied by high-profile media campaigns each time. The data confirmed this:

- In the first 6 months of 2026, a16z participated in approximately 48 seed round deals, leading 46% of them. This is a systematic seed strategy, not sporadic bets.

- The most striking aspect is check size: the median round led by a16z is $10.5 million, a figure more reminiscent of a classic Series A than a traditional seed round.

- Adding General Catalyst and Sequoia, these 3 giants completed 87 seed deals in just 5.5 months, averaging one early-stage investment every 1.5 business days.

@a16z tweeted: We are proud to lead the seed round for Westmag. One underappreciated advantage of investing in the entire hardware stack is getting firsthand exposure to the supply chain challenges plaguing the industrial base...

Meanwhile, the latest data from Carta shows that from a valuation perspective, seed round valuations are inflating rapidly. While some might argue this is the result of a few aggressive players, the math for most EMs still forces them to operate at or below the median to secure sufficient initial ownership and maintain a viable return path.

The logic for mega-funds is completely different. With accumulated AUM, brand premium, and superior deal flow, price discipline is no longer a real constraint. This gap is tearing the market into two distinct tiers, which we roughly call "Classic Seed" and "Super Seed":

- The 90th percentile seed round valuation soared to $93.7 million in Q1 2026, nearly doubling from four years ago.

- Over the past year, valuations above the median have risen by at least 53%.

- The bottom has barely moved: the 25th percentile crept from $18 million to $22.7 million.

@PeterJ_Walker tweeted: Top 5% seed round valuations now often exceed $175M, tripling in the past 12 months. Has a bit of that 2021 absurdity vibe to it (even coming from an AI believer).

But all of this remains circumstantial evidence, pointing to a general direction without providing a definitive answer to what is really happening in the early market and how systematic the presence of mega-funds truly is.

That's why we decided to dig deeper. We analyzed the individual dynamics of each fund across the three eras, deconstructed their behavioral patterns, and considered what this shift ultimately means for EMs.

Deconstructing the Deal Machine

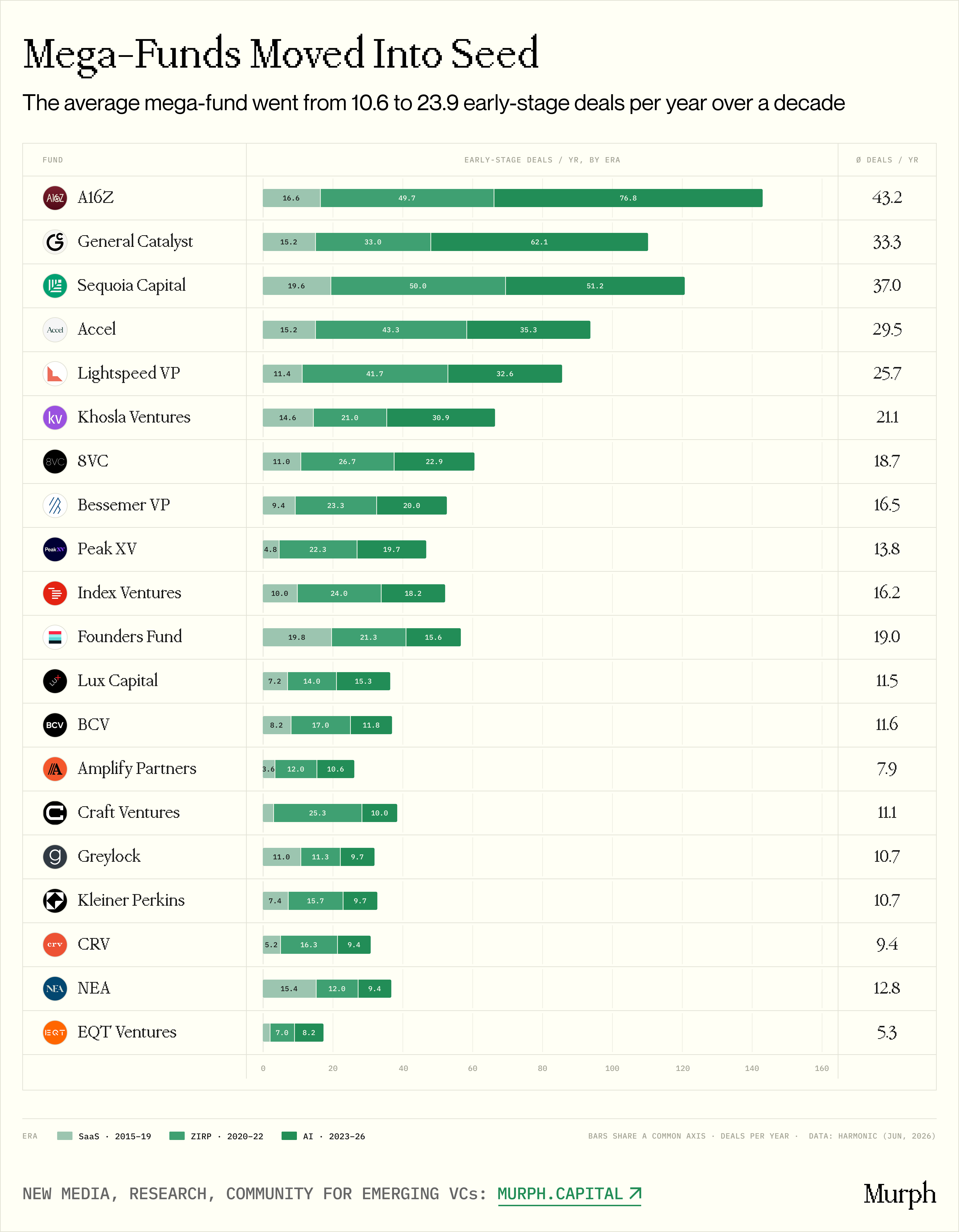

Caption: Comparison of early-stage deal counts for 20 mega-funds across three eras.

Looking at the averages, a typical mega-fund in the SaaS era completed 10.6 early-stage deals per year. By the AI era, this jumped to 23.9 deals, an average growth of 2.37x across the entire cohort.

The most interesting part is what happened after the ZIRP era ended. If this growth was purely a byproduct of free money, it should have reversed after interest rate hikes. However, among the 20 funds in our dataset, the average annual deal count in the AI era is nearly identical to the ZIRP era: 23.9 vs. 24.3. In fact, only 3 funds reduced their early-stage investment pace. This proves the shift is structural, although a few outliers pull the overall numbers up:

- a16z: 16.6 → 49.7 → 76.8 deals/year

- General Catalyst: 15.2 → 33.0 → 62.1 deals/year

- Khosla Ventures: 14.6 → 21.0 → 30.9 deals/year

Behind this, there are at least three fundamental driving factors:

AI-era companies are inherently more capital-intensive. GPU infrastructure, data pipelines, and research scientists earning $300,000-$500,000 annually create a completely different baseline cost structure. What $500,000 could accomplish in the SaaS era (two engineers plus AWS) now requires $2-5 million in the AI era. The expanding median check partly reflects genuine R&D spending, not just valuation inflation. Moreover, while the early-stage in the SaaS era was fundamentally exploratory (allowing founders to iterate, pivot, and spend years finding PMF), the first-mover advantage window in AI is much shorter. If your model works, you quickly pull ahead of the competition, and this window closes faster.

The battle for founders has shifted pricing power. In the early stages of a revolutionary technology cycle, high aptitude combined with top-tier talent is invaluable. The best AI founders can choose between a16z, Sequoia, and Lightspeed at the seed stage, building a cap table that helps them raise a larger next round in a shorter time. Often, pricing power has shifted from investors to founders: rounds become larger not because the company objectively needs more capital, but because founders can demand and get it.

The math of fund size is quite telling. The combined AUM of the top 5 funds in our cohort grew from approximately $34 billion to $249 billion, roughly 7x over ten years. Meanwhile, their seed deal count only grew by 2-4x. The expansion of AUM far outpaced seed activity, making seed checks an even smaller fraction of these funds' portfolios.

Take a16z: in 2015, it managed about $4 billion; now it manages $90 billion (including the latest $15 billion fundraise, the largest single VC fundraise in history). A $6 million seed check represents only 0.01% of $90 billion AUM. Mathematically, the fund has no incentive to haggle over every million in valuation. Conversely, in an increasingly concentrated market, the risk of missing a generational opportunity is catastrophic.

Therefore, we can say with high confidence: the influx of mega-funds into seed rounds in the AI era is not speculation from the cheap money era, but a strategic imperative. A massive influx of capital into mega-funds coincided with the emergence of new types of companies and talent worth competing for at the very earliest stages, and both factors jointly drove this shift.

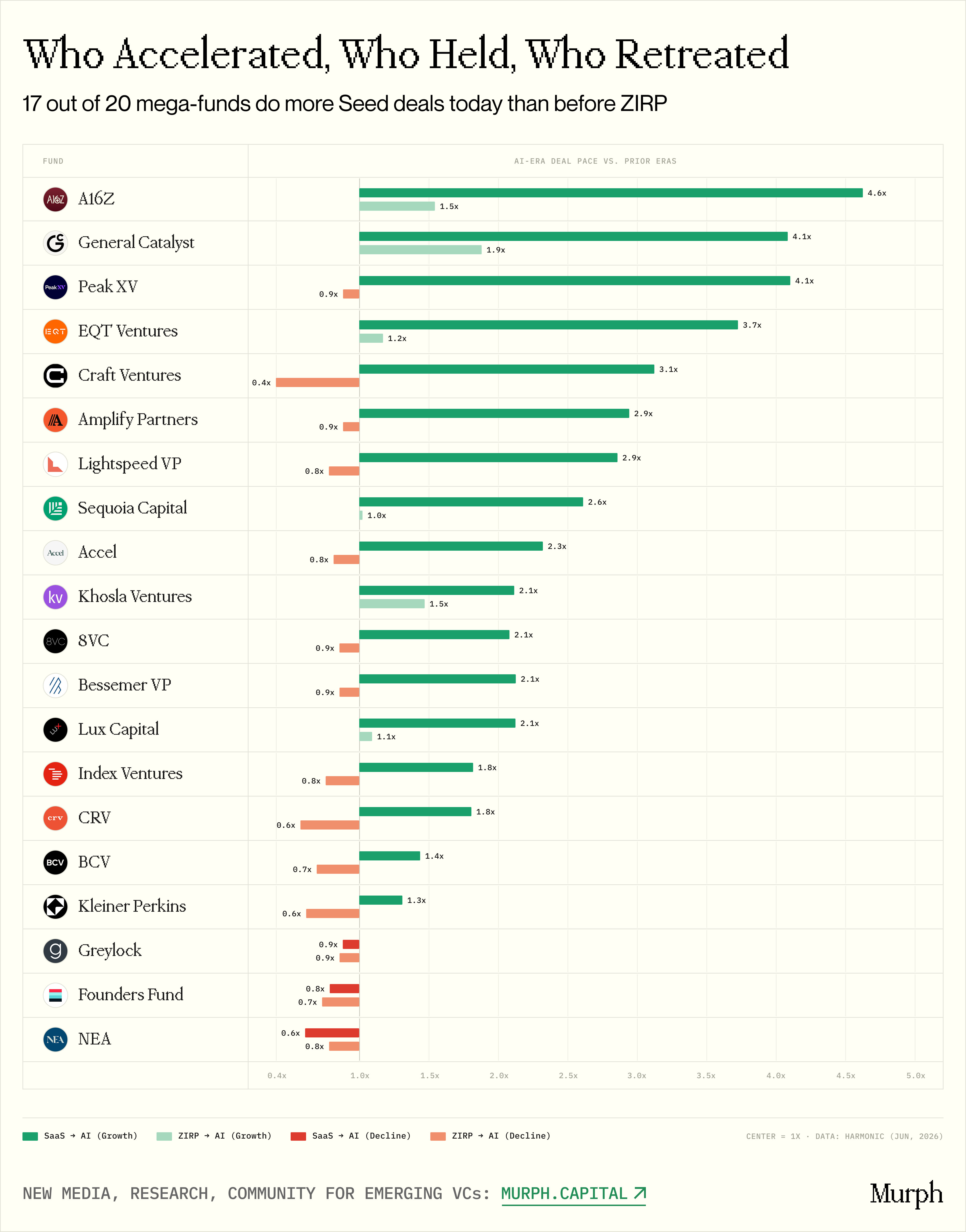

Group Analysis by Growth Rate

Caption: 20 funds grouped by growth trajectory.

During the ZIRP era, all 20 mega-funds in the dataset increased their early-stage deals, without exception. After the pandemic, the Fed cut rates to near zero, massive LP capital flowed into VC pockets, and total US VC fundraising in 2021 reached a staggering $169.5 billion.

Armed with massive dry powder, some mega-funds dipped down to the seed stage to test the waters; others proactively exited late-stage rounds (where valuations were extremely inflated at the time) and also moved down the ladder.

But by the AI era, with interest rates stabilizing above 5%, the market became highly differentiated. Macro divergence split funds into three behavioral paths:

Accelerators

Their deal volume in the AI era even exceeded the ZIRP period:

- a16z (75.3 deals/year)

- General Catalyst (61.5 deals/year)

- Khosla Ventures (31.5 deals/year)

These funds didn't just stay at the seed stage after cheap money vanished; they doubled down, aggressively expanding their presence.

Stabilizers

Deal volume in the AI era is slightly below the ZIRP peak, but still significantly higher than the SaaS era:

- Sequoia (19.6 → 49.3 → 50.6)

- Accel (15.2 → 43.3 → 34.7)

- Lightspeed (11.6 → 41.7 → 32.1)

The ZIRP surge has peaked and receded, but baseline activity has permanently elevated to 2-3 times historical levels. There's no going back.

Disciplined

Steady growth across all three eras:

- Bessemer (9.4 → 23.0 → 20.9)

- Lux (7.2 → 14.3 → 14.7)

- Index Ventures (10.0 → 23.3 → 17.6)

They avoided the ZIRP spike and the AI explosion, but the baseline has moved up permanently. From 10 deals per year in the SaaS era, they now stabilize at 15-21 deals.

The only exceptions are three funds: Founders Fund, NEA, and Greylock. They either decreased or held flat their early-stage activity from the SaaS era to the AI era.

Founders Fund is perhaps the institution that made a philosophical and active choice. Peter Thiel's contrarian framework, heavily influenced by Girard's mimetic theory, views crowded market consensus as a clear signal to look elsewhere for opportunities. So while the other 17 mega-funds rushed to the seed stage, Founders Fund went the other way, shifting towards large, concentrated late-stage bets, channeling capital into generational outliers like OpenAI, Databricks, and Anduril.

Greylock remains deeply committed to the tradition of being the "first check," but chooses to play a high-concentration game. It doesn't operate a high-volume deal machine but focuses on fewer, higher-conviction bets, sometimes even incubating companies directly within its own offices.

NEA's large multi-stage mandate makes its seed activity more difficult to analyze in isolation, and we won't speculate without hard data.

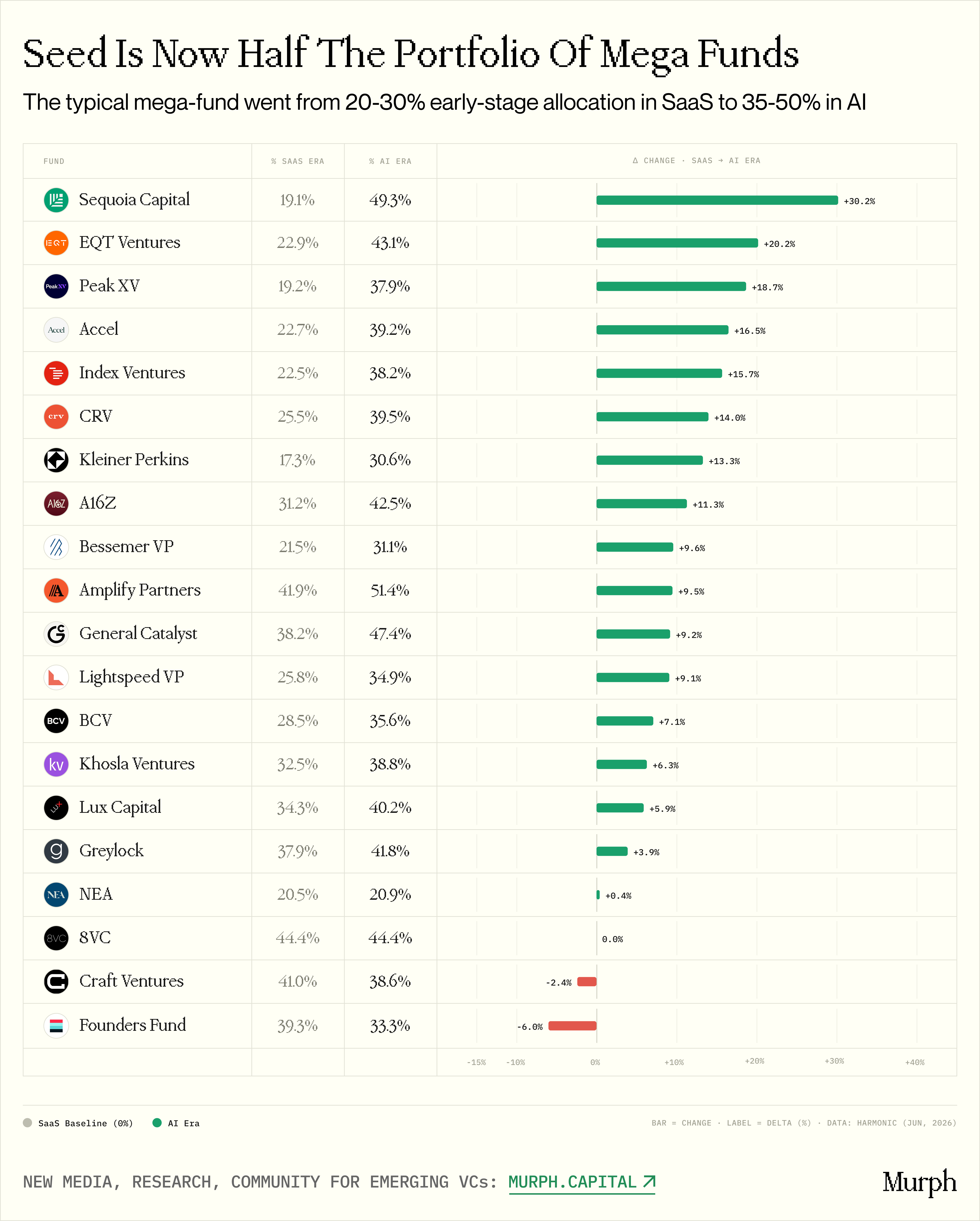

Core Allocation vs. Side Project

Caption: Change in the proportion of early-stage deals relative to total investments for each fund.