Stock prices hit new highs, yet storage stocks remain undervalued

- Core Thesis: AI demand is transforming memory chips from cyclical commodities into "luxury goods" with pricing power and sustainable profitability. This has driven surging stock prices and profits for memory giants like Micron, but the market still applies outdated valuation frameworks. Consequently, their forward P/E ratios remain far below other segments of the AI supply chain, making valuations appear "cheap."

- Key Factors:

- Micron's FY2026 Q3 earnings surpassed expectations, with revenue of $41.46 billion and a gross margin guidance of 86%. The stock surged 13% in after-hours trading, pushing its market cap above $1.16 trillion, signaling that the memory pricing uptrend is far from over.

- Despite massive stock price gains over the past year (e.g., Micron up over 850%), forward P/E ratios for memory stocks remain at approximately 9-10x, significantly lower than Nvidia's 23x or the semiconductor industry median of 36x. Profit growth has outpaced stock price appreciation.

- HBM demand has broken the historical rule of DRAM costs halving every five years. Manufacturers are shifting capacity to high-margin HBM, creating a persistent structural supply constraint. DRAM prices have now risen for eight consecutive quarters.

- The supply-demand gap for NAND chips is even more rigid. Price collapses in 2022-2023 led manufacturers to halt capacity expansion for years, while enterprise SSD demand is exploding due to AI inference and HDD replacement. All production capacity for 2026 has already been sold out.

- The broader memory sector faces a dense earnings season ahead (TSMC, Samsung, SK Hynix, Western Digital, etc.). Micron's strong guidance sets the tone for the industry trend, with HBM4 and NAND becoming key focus areas.

Original Author: Jialiu

Today, Micron delivered a historic earnings report that significantly boosted confidence across the semiconductor sector.

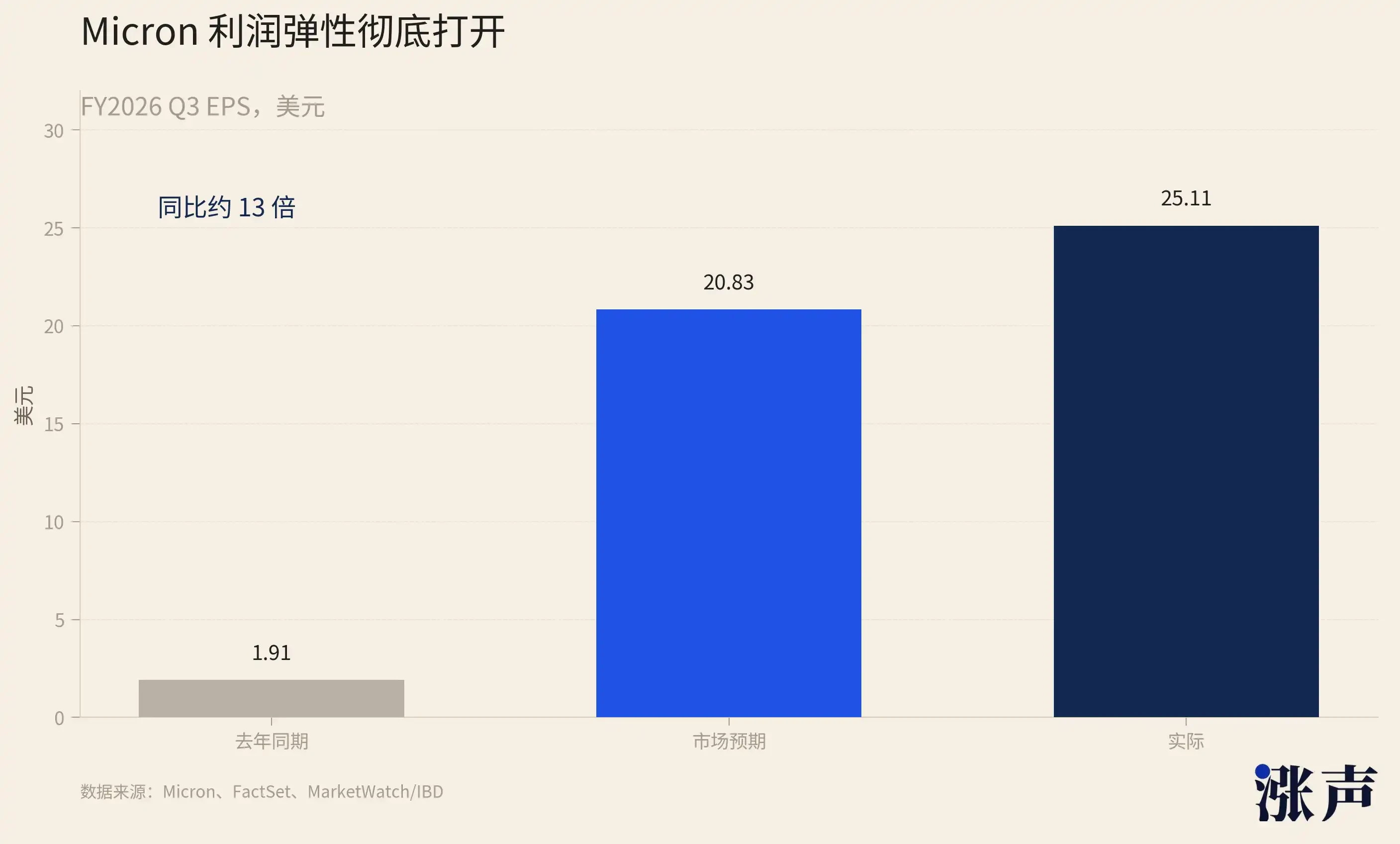

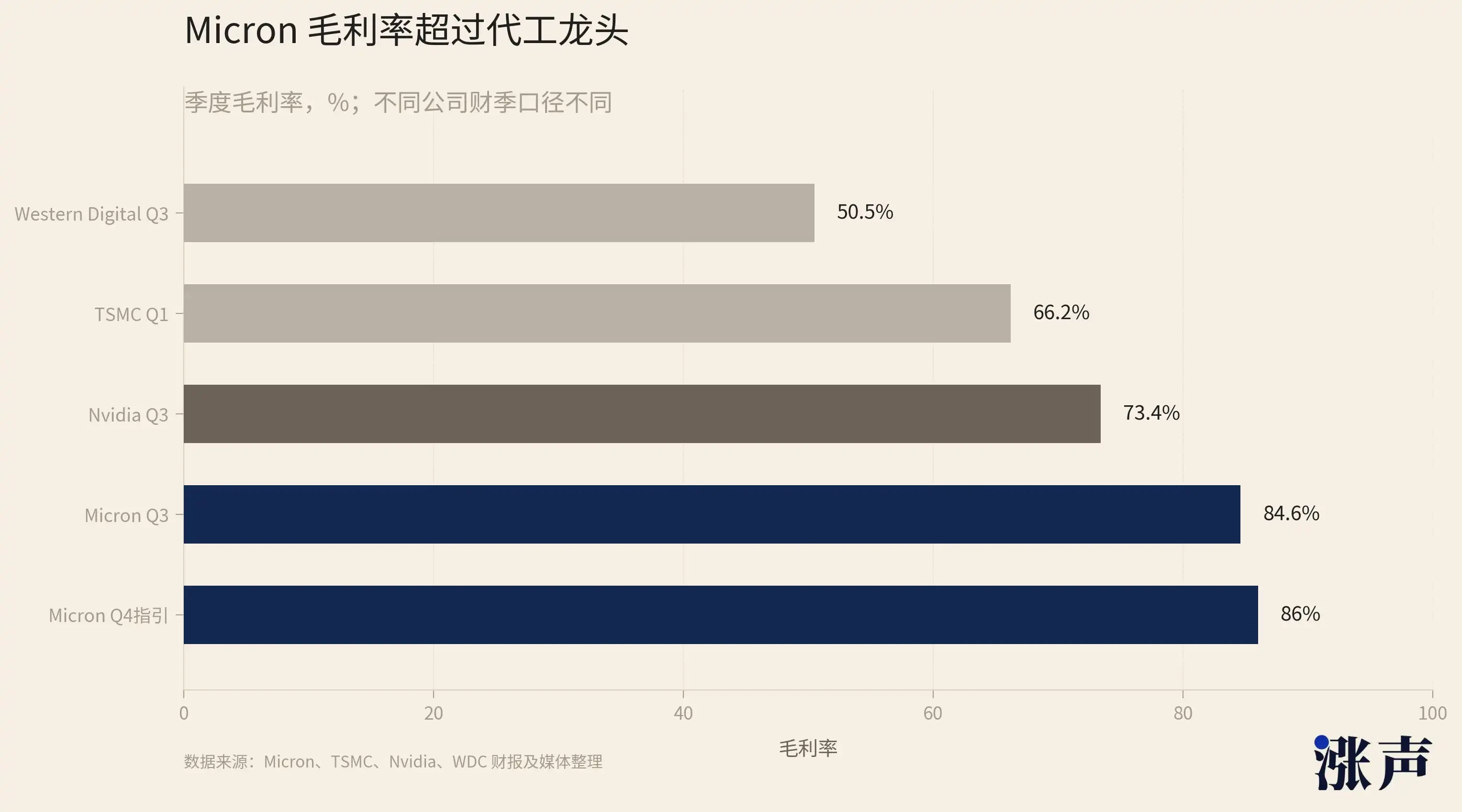

FY2026 Q3 revenue reached $41.46 billion, exceeding market expectations by nearly $6 billion. A memory company, long labeled a "low-margin commodity," posted a gross margin guidance typically seen in software companies. Its stock price surged 13% to 14% in after-hours trading, pushing its market cap to $1.16 trillion.

Micron's gains this year have already been remarkable. Closing at $1,211.38 on June 22, it has more than tripled year-to-date and soared over 850% in the past 12 months. It is the third best-performing stock in the S&P 500 for 2026, behind SanDisk and Western Digital, also memory companies. The entire sector is rising by this magnitude. SK Hynix is up over 800% in the past 52 weeks, and Samsung is up over 400%.

With such price increases, many people's first reaction is naturally "it's too expensive." However, in reality, a stock's price rising significantly doesn't necessarily mean its valuation is expensive. From many perspectives, memory is still a very "cheap" hot sector.

Stock Price Up 9x, Yet PE Stagnant

One of the most common metrics to judge whether a company's stock is expensive or cheap is the PE ratio, or price-to-earnings ratio.

Simply put, PE measures how much the market is willing to pay for every $1 of profit a company earns. A PE of 10x means investors are willing to pay $10 for $1 of annual profit. A high PE usually indicates the market believes in strong future growth; a low PE might mean the stock is cheap, or it could mean the market thinks the company's current profit is just a cyclical peak that will soon decline.

This is where the counterintuitive aspect of memory stocks lies: stock prices have risen a lot, but PE ratios remain very low.

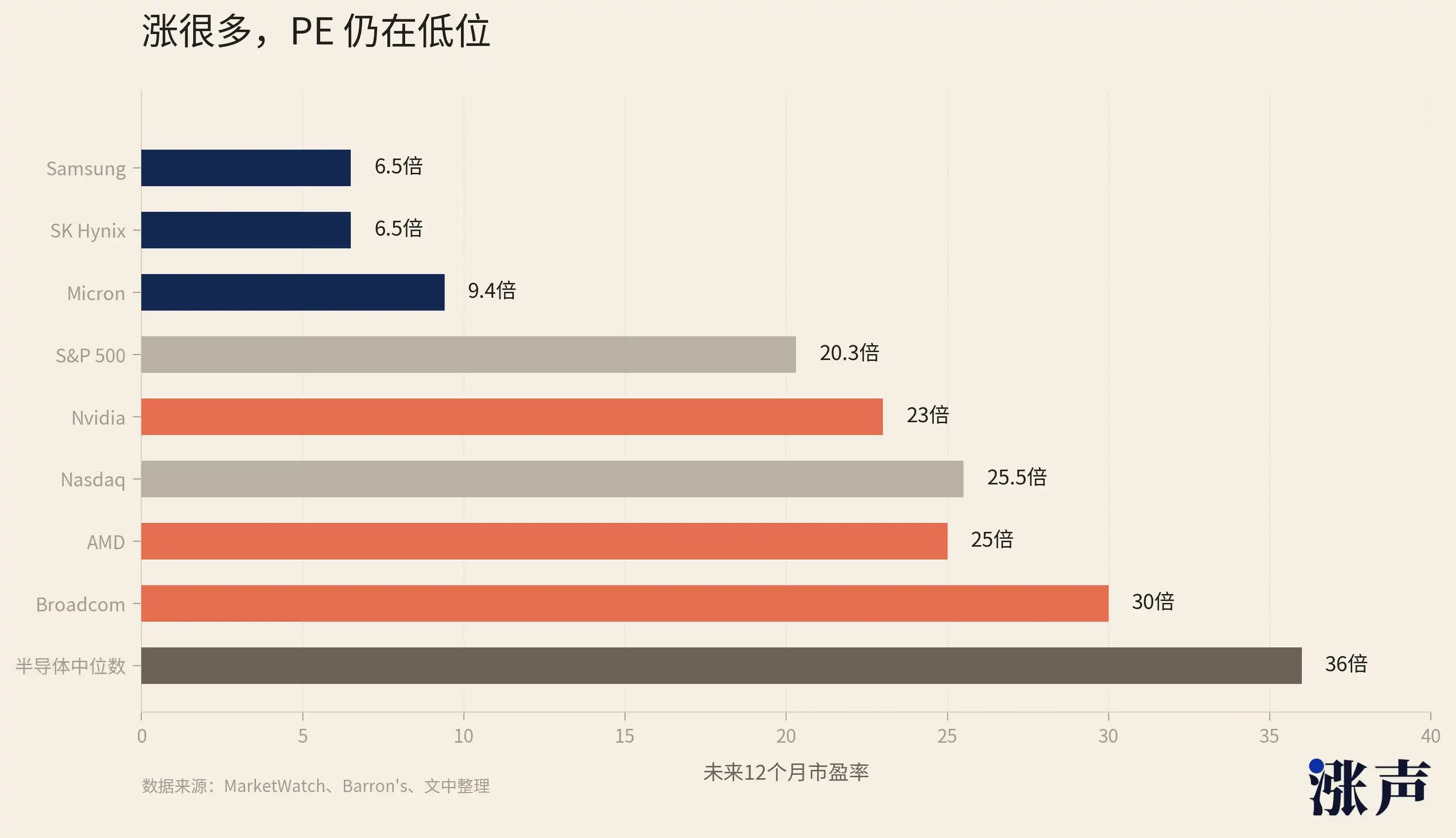

According to FactSet data, a MarketWatch report in mid-June provided a set of figures: Micron's forward 12-month PE was around 9x, while SK Hynix and Samsung were around 6.5x. Barron's estimated Micron's forward PE at about 9.74x, compared to the Nasdaq Composite Index at roughly 25.5x and the S&P 500 at about 20.3x. Data from GuruFocus on June 21 showed Micron's forward PE at 9.90x, SK Hynix at 5.92x (late May data), and Samsung at approximately 5.45x.

In other words, most data sources suggest that the forward PEs of the big three memory manufacturers are all in single digits or just above 10x.

Looking across the entire AI industry chain, these figures are almost the lowest tier.

Nvidia's forward PE is around 23x, Broadcom's is about 30x, AMD's is around 25x, TSMC's is about 20x, and the median PE for the semiconductor industry is around 36x. This means the valuation level of the big three memory manufacturers is roughly one-third of Nvidia's and one-quarter of the industry median.

But ironically, an increasing amount of money in the AI industry is being captured by the memory segment.

AI servers aren't just about GPUs. Every high-end AI accelerator card needs HBM, every inference server needs large-capacity DRAM. KV cache, model weights, local cache, and data throughput are all inseparable from SSDs. Without HBM, there are no GPU training clusters; without server DRAM, there are no inference clusters; without high-capacity NAND, the storage and caching costs for AI applications can't be reduced.

Memory is no longer a common accessory in the AI industry chain; it's a physical bottleneck that all AI capital expenditure must address. A figure from Micron's latest report illustrates this: single-quarter data center revenue was $25 billion, of which enterprise SSD revenue was $5 billion, accounting for 20% of data center revenue.

It's evident that this bottleneck is now even beginning to affect consumer electronics.

AI data centers have driven up the capacity and prices of HBM, DRAM, and NAND, eventually forcing even a powerful negotiator like Apple to face cost pressures and pass some of the price increases onto consumers. In the past, discussions about AI profitability first mentioned Nvidia; but it's becoming increasingly clear that a large portion of the AI bill is flowing to memory manufacturers.

Memory stock prices have risen a lot, but profits have risen even faster.

Micron just reported Q3 EPS of $25.11, compared to $1.91 in the same period last year, a tenfold increase in one year. SK Hynix's Q1 2026 operating profit was 37.61 trillion KRW, up 405% year-over-year. Samsung's semiconductor division saw Q1 operating profit increase more than eightfold year-over-year. Stock prices have multiplied several times, but profits have multiplied even more, preventing the PE ratio from being pushed higher.

AI money is genuinely flowing into the income statements of memory manufacturers.

Sector Releases Positive Catalysts, Micron Just the Starting Gun

Micron's earnings report is the starting gun for this round of memory earnings season.

Next, the memory sector enters a month of high information density: TSMC on July 16, Samsung on July 23, SK Hynix and Western Digital on July 29.

The impact of Micron's report has already set the tone for the subsequent companies. Its most crucial information isn't the single-quarter beat, but the Q4 guidance of $50 billion in revenue and 86% gross margin.

This guidance essentially tells the market that price increases haven't peaked; they are accelerating. The next four companies are essentially validating or disproving the same trend revealed by Micron's guidance, albeit in different markets and with different product mixes.

First, consider TSMC, reporting on July 16.

TSMC doesn't make memory, but it's the foundation of the entire AI chip supply chain. Nvidia's GPUs, Broadcom's custom accelerators, and AMD's data center chips all come from its fabs. The question TSMC answers is more fundamental: whether the capacity bottleneck for AI chips has been resolved. Q1 revenue was $35.9 billion, up 40.6% year-over-year, with a gross margin of 66.2%, and advanced process nodes accounted for 74% of wafer revenue. Q2 guidance is for revenue between $39 billion and $40.2 billion.

TSMC and memory have a multiplier relationship. Every additional advanced process wafer it sells leads to one more AI accelerator downstream, and every additional accelerator requires several HBM stacks. The HBM capacity per GPU for Nvidia's Vera Rubin platform is several times that of the previous generation. The more aggressively TSMC ships, the tighter memory capacity becomes.

July 23 is Samsung's earnings report.

Fifteen brokerages expect Samsung's Q2 operating profit to be around 88.3 trillion KRW, with operating margin flat or higher than Q1's 66%. A conglomerate making phones, panels, and home appliances has had its profit margins lifted to this level by its memory division alone.

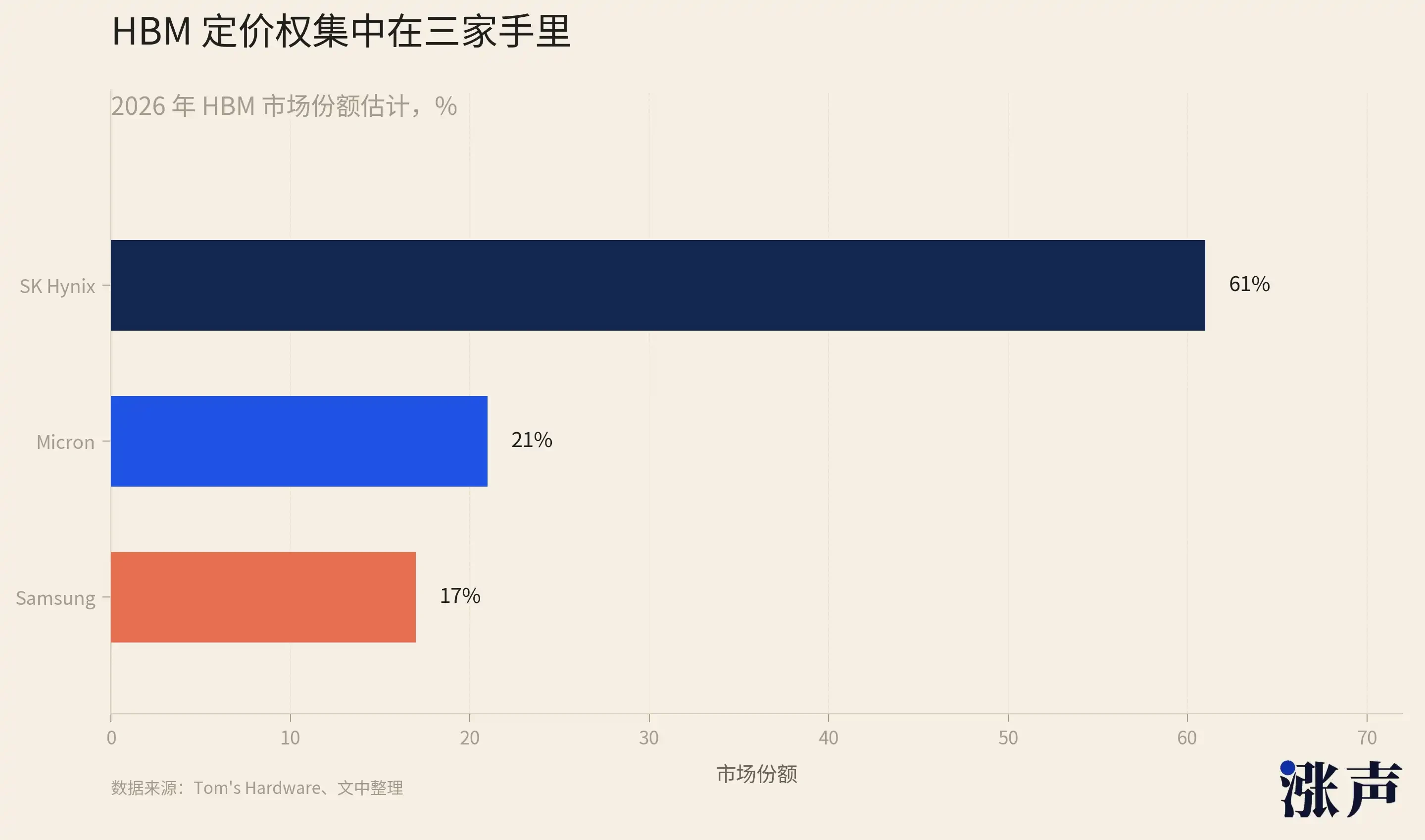

But the most important aspect of Samsung's report isn't the profit figure; it's HBM4. Samsung holds only about 17% of the HBM market, far behind SK Hynix's 62% and Micron's 21%. The generational shift to HBM4 is Samsung's only window to close the gap. In its Q1 conference call, it made a few specific statements: HBM sales in 2026 will grow more than three times year-over-year, and starting from Q3, HBM4 will account for over 50% of HBM sales. Micron just disclosed that its 36GB 12-Hi HBM4 has begun mass production and shipment. The competitive positioning among the three in HBM4 is the most important battle to watch in the second half of the year.

On July 29, SK Hynix and Western Digital report on the same day.

SK Hynix's Q1 was textbook: quarterly revenue of 52.6 trillion KRW, up 198% year-over-year, operating margin of 72%, and net profit margin of 77%. A hardware manufacturer achieving a 77% net profit margin is staggering, compared to Apple's roughly 25% and Nvidia's roughly 58%. Some brokerages predict Q2 operating margin could approach 80%. Micron has already led the way, achieving an operating margin of 81.2%, surpassing TSMC. As the top player in HBM share, SK Hynix is highly likely to deliver a Q2 report comparable to Micron's. The combined operating profit of Samsung and SK Hynix for Q2 is expected to exceed 150 trillion KRW. Together with Micron, the three giants are set to set a record for combined quarterly profit.

Western Digital reports Q4 on the same day. It has no DRAM or HBM, being pure NAND and SSD. It provides another dimension of AI storage demand: the KV cache for inference requires high-capacity SSDs. Q3 Cloud revenue grew 48% year-over-year, with a record gross margin of 50.5%. It's worth noting that Western Digital and its spun-off SanDisk are the two best-performing stocks in the S&P 500 for 2026, outperforming Micron. Growth in the NAND line is less explosive than DRAM, but the direction is completely aligned.

AI Transformed Memory from Commodity to Luxury

Stock prices hit new highs, yet PEs remain low. Earnings reports are more explosive than the last.

At this point, some may still doubt whether this is sustainable or just another cyclical frenzy destined to collapse.

Let's revisit the analysis of Jukan, a semiconductor analyst at Citrini Research.

As early as Q1 2024, when SK Hynix and Micron were still mired in post-pandemic DRAM inventory gluts and depressed stock prices, the Citrini team predicted they would outperform. Subsequently, these stocks rose several-fold to nearly 10x. They have been almost perfectly right throughout this memory cycle. A detail from early June shows his market influence: he reposted a SemiAnalysis report about adjustments to Nvidia's Rubin server memory configuration, which immediately created visible downward pressure on Micron and SK Hynix.

Jukan's core bullish argument for memory isn't a short-term judgment like "prices will rise," but rather the belief that AI has transformed memory from a commodity into a luxury good.

First, HBM has broken a sixty-year trend. From 1957 to 2020, the cost per Gb of DRAM decreased by roughly an order of magnitude every five years; prices were always falling. This was a fundamental law of the memory industry, upon which the competitive model and valuation framework of the entire sector were built. Jukan points out that AI-driven HBM demand has completely shattered this law. Manufacturers shift capacity towards HBM, which is more complex to produce and consumes more silicon area, squeezing traditional DRAM supply.

Currently, no manufacturer plans to convert HBM production lines back to traditional DRAM. The reason is simple: HBM profit margins are far higher than standard DRAM, and rational manufacturers won't swap high-margin lines for low-margin products. This has transformed supply tightness from a cyclical phenomenon into a structural one that will persist as long as AI demand continues.

Therefore, sustained price increases for HBM memory will be long-term.

Annual HBM volumes and prices are largely negotiated at the beginning of the year, providing manufacturers with strong earnings visibility. TrendForce data confirms this: traditional DRAM contract prices rose 90% to 95% quarter-over-quarter in Q1 2026, the largest single-quarter increase on record, with further increases expected in Q2. In a normal DRAM cycle, the price increase phase typically lasts 4 to 6 quarters before peaking. This current uptrend has lasted nearly 8 quarters without stopping. JPMorgan even predicts DRAM prices could rise for four consecutive years, something unprecedented in the industry's history.

So, it's almost fair to say memory has evolved from a commodity to a luxury good.

The biggest difference between luxury goods and commodities lies in pricing. Commodity prices are determined by marginal cost; anyone can expand production, profits are eventually competed away, hence a low valuation. Luxury goods prices are determined by scarcity and pricing power; supply is controlled, profits can be sustained at high levels, hence a premium valuation. The old rule "low PE equals peak" presupposes that earnings will revert to the long-term downward trend line. But if the trend line itself has turned, where reversion occurs becomes an open question.

Back to the initial paradox. Stock prices are at all-time highs, valuations are at historical lows. This anomaly exists because the market is still using the old framework for commodities to price an industry that has become a luxury. Micron just struck a heavy blow to this old framework with its 84.9% gross margin report and 86% gross margin guidance. If we can't go back, the current PE of 5 to 10 times is wrong.

Therefore, we believe that despite the price highs, memory stocks are still not expensive.

After HBM, Is NAND the Real Main Course?

In every major market cycle, halfway through, the market asks the same question: after the leader has run up, who will take the baton?

HBM and DRAM have been the absolute protagonists of this memory cycle, with the big three's surges largely attributed to them. NAND has consistently been viewed as a supporting actor.

But if you look closely at the supply-demand structure, you'll find a counterintuitive fact: the NAND segment, long treated as a side dish, might actually be the main course itself, with its shortage being, in some ways, even more severe than HBM's.

First, why is HBM so hot? HBM is standard equipment for AI accelerator cards, with high unit prices, thick margins, and high technical barriers. SK Hynix used it to achieve a 62% market share and 77% net profit margin. These are facts. But HBM has one characteristic: while supply is tight, the path to capacity expansion is clear. The big three are all pouring money into expanding HBM capacity; Samsung and Micron are chasing SK Hynix, climbing generation by generation (HBM4, HBM4E). Supply is increasing at a visible rate, just temporarily unable to keep up with demand.

However, NAND manufacturers haven't expanded capacity for years.

The 2022-2023 NAND price crash scared all players. Capital expenditure on NAND by Kioxia, Western Digital, Samsung, and SK Hynix was slashed to extremely low levels, and new production lines have been delayed, with the earliest expected completion not until 2027.

The big three prioritize wafer capacity and capital expenditure for HBM and high-end DRAM, leaving fewer resources for NAND. Micron even directly shut down its consumer-grade Crucial business, reallocating all its capacity to enterprise and GPU-grade storage.

NAND supply is missing, but demand is huge.

Large model inference requires massive KV cache and data throughput, which directly fuels explosive demand for enterprise SSDs (eSSDs). In Q1 2026, global eSSD revenue grew 86% quarter-over-quarter. Another reason is HDD shortages. Mechanical hard drive supply is also tight, forcing data centers to substitute high-capacity SSDs for HDDs, transferring a portion of HDD demand to NAND.

The CEO of Phison Electronics said, "Every NAND manufacturer tells us that all of 2026 is sold out." Kioxia also confirmed that its entire 2026 NAND capacity is fully booked. The price of a 1Tb TLC NAND chip rose from around $4.8 in July 2025 to around $10.7 by the end of 2025, more than doubling in a few months.

HBM is in shortage, but supply is increasing deterministically. NAND is in shortage, but supply has almost no growth. The HBM shortage has a remedy, just slow-acting; the NAND shortage has no remedy for now because no one is preparing one. From this perspective, the NAND supply-demand gap is more rigid than HBM's, and the price persistence could be stronger.

This is why the two best-performing stocks in the S&P 500 for 2026 are not the HBM leader SK Hynix or Micron, but pure-play NAND and SSD companies Western Digital and its spin-off SanDisk. The market has already voted with its feet, quietly moving NAND from the supporting cast to the leading role, though most people haven't noticed yet.

Of course, NAND also has its risks. It doesn't have the rigid demand binding of AI accelerator cards