美光财报前夜:韩美科技股巨震之际,如何才能守住存储牛市?

- 核心观点:美光科技即将发布的财报不仅是季度业绩检验,更是对AI存储牛市逻辑的一次压力测试。核心矛盾在于,市场预期已被推至极高水平,美光需证明供需缺口远未结束且能持续上调指引,否则可能引发股价剧烈波动并波及整个产业链。

- 关键要素:

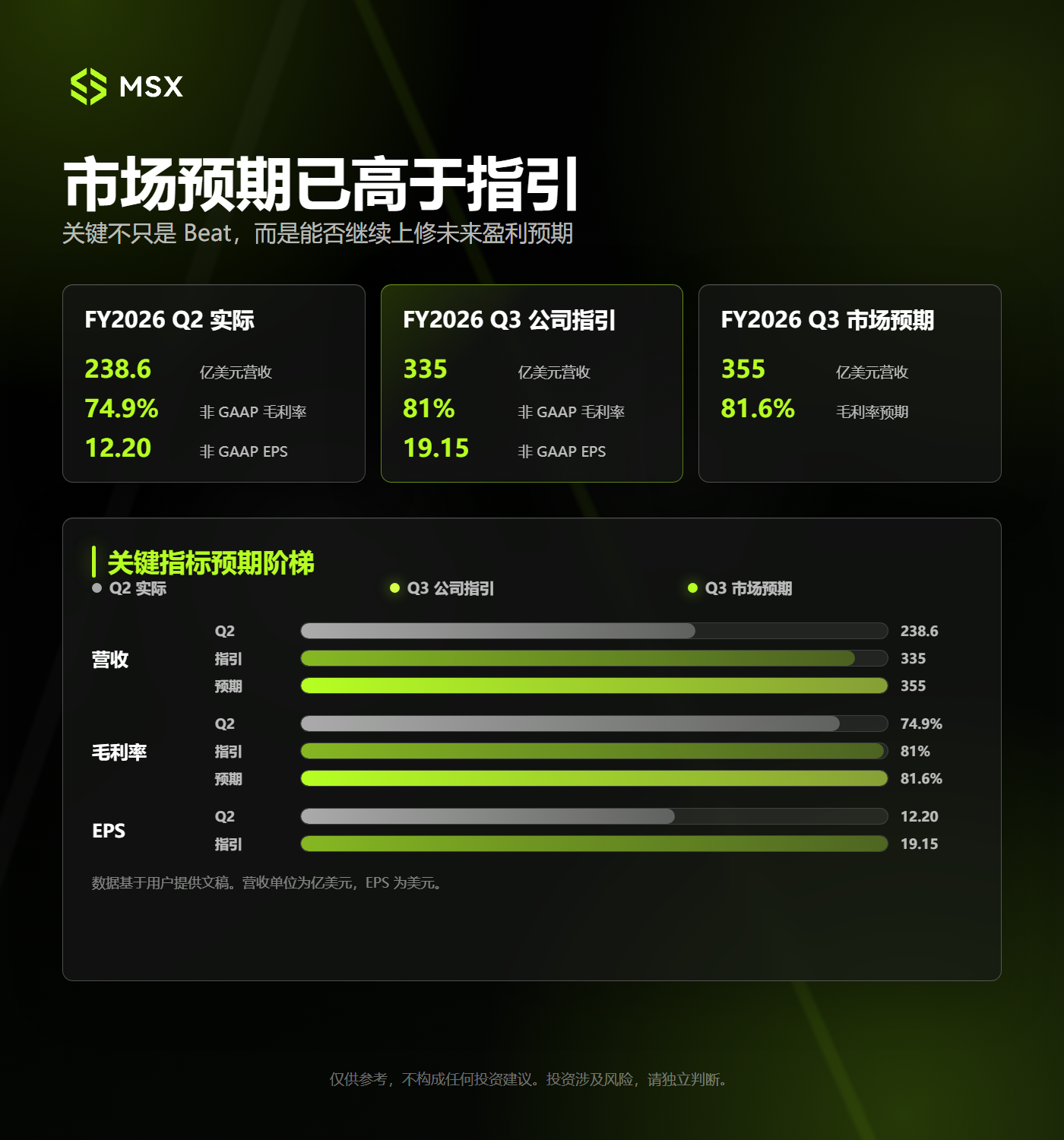

- 市场预期与公司指引存在巨大落差:市场对美光第三季度营收预期已达355亿美元,高于公司此前335亿美元的指引,要求业绩不仅超预期,还要超出已极乐观的市场一致预期。

- HBM供需持续性成焦点:美光需在电话会中明确HBM4良率进展、2027年订单锁定情况及与英伟达等客户的合作深度,以证明高景气是结构性增长而非短期产品周期。

- 超高毛利率(第三季度指引约81%)是否为常态:市场关注管理层对毛利率未来走向的描述,若展望保守,高估值逻辑或将松动,触发“Sell the News”行情。

- 供需缺口何时被产能填平:市场关注新增产能投放节奏,若供给释放快于AI需求增长,存储行业可能重回价格竞争,美光需证明需求增速仍快于供给。

- 期权隐含波动率高达13%:市场已押注财报后股价出现两位数涨跌,反映了当前资金对存储主线的高分歧与拥挤交易风险。

On June 23, global tech assets, from South Korean stocks to U.S. equities, experienced a sharp sentiment cooldown.

During the Asian session, the KOSPI index fell nearly 10% in a single day, with Samsung Electronics and SK Hynix both dropping over 12%, triggering a market-wide trading halt. The sell-off quickly spread to U.S. markets in the evening, with AI and memory assets, which had been the strongest performers over the past year, becoming the epicenter of the global tech stock correction.

What makes this market turmoil particularly intriguing is its timing, coinciding with Micron Technology's Q3 FY2026 earnings report due out after the close on June 24.

On one hand, global AI memory stocks are collectively retracing, with the market beginning to reassess high valuations and crowded trades. On the other hand, Micron is about to deliver a highly anticipated earnings report. The confluence of these factors means this earnings report holds significance far beyond a single company's quarterly results; it serves as a concentrated stress test for the entire memory investment theme.

After all, the core narratives driving the sustained rally in global memory stocks—soaring HBM demand, DRAM and NAND price increases, persistent supply tightness, and rapidly expanding gross margins—all require fresh validation of confidence. This makes the underlying question more direct: With stock prices and market expectations already pushed to elevated levels, can Micron once again deliver answers that exceed the imagination?

In other words, an "in-line earnings report" may no longer be sufficient. What the market truly awaits is whether Micron can once again raise its guidance and prove the supply-demand gap in AI memory is far from over.

1. Why Is This Micron Earnings Report So Important?

Looking at the previous quarter's data, Micron's fundamentals can hardly be described with a simple "beat expectations."

In Q2 FY2026, Micron's revenue reached $23.86 billion, nearly tripling year-over-year. Non-GAAP gross margin rose to 74.9%, and non-GAAP EPS hit $12.20, both setting company records.

More importantly, Micron's guidance for the third quarter was aggressive: revenue projected at $33.5 billion, non-GAAP gross margin around 81%, and non-GAAP EPS of $19.15.

However, the capital market's appetite has escalated even faster than the company's guidance. Current market consensus for Micron's Q3 revenue has already reached approximately $35.5 billion, exceeding the upper end of the company's guidance range. The gross margin consensus is around 81.6%, indicating the market has already priced in another earnings beat.

This creates the biggest contradiction for this earnings report: Micron's results must not only surpass the company's guidance but also exceed an already very optimistic market expectation.

Therefore, this earnings report requires looking beyond whether revenue and EPS "beat." It's crucial to observe if the market will continue to revise up earnings forecasts for coming quarters post-release. Simply put, if the earnings are just "normally good," it might not be enough. But if the results are strong enough to prompt further guidance upgrades, yesterday's decline might prove to be a premature shakeout.

After all, for a high-expectation stock that has already rallied significantly, the most dangerous scenario is often not poor performance, but decent performance that falls short of justifying an even higher valuation.

This is precisely the pricing environment Micron faces today.

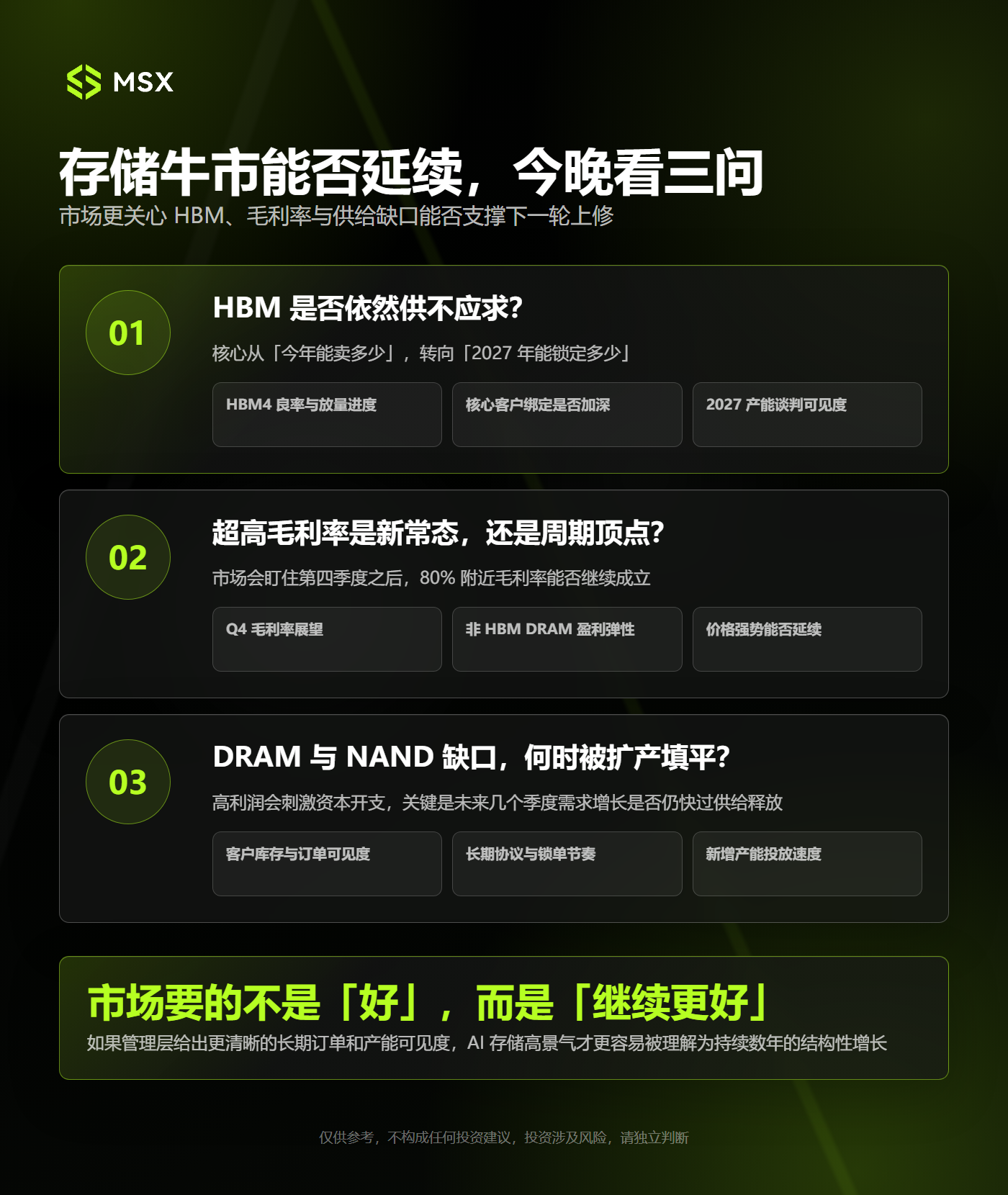

2. Three Key Questions to Determine if the Memory Bull Run Continues Tonight

1. Is HBM Supply Still Falling Short of Demand?

Micron's core growth narrative remains centered on HBM.

As is well known, AI servers require more than just GPUs. With the compute power,功耗, and data throughput of individual AI accelerators continuously increasing, HBM has evolved from a standard supporting component into a critical bottleneck determining the performance of the entire AI system.

Micron has already begun ramping up production and shipments of HBM4, targeting its use in NVIDIA's upcoming Vera Rubin platform. HBM capacity for 2026 is largely spoken for. Therefore, the market's focus is shifting from "how much can be sold this year" to "how much can be locked in for 2027."

During the earnings conference call, investors are likely to seek answers to several key questions:

Are HBM4 yields and volume ramp-up progressing as expected? Is the relationship with core customers deepening? How far along are capacity negotiations for 2027? Can subsequent products like HBM4E further close the gap with SK Hynix?

If Micron can provide clearer visibility on long-term orders and capacity, the market can more readily interpret the current HBM boom as a multi-year structural growth trend, rather than a product cycle nearing its peak.

Conversely, if management's commentary on 2027 demand and orders is vague, the market may begin to suspect that the tightest and most pricing-powerful phase of the HBM cycle has already been priced into the stock.

2. Is the Ultra-High Gross Margin a New Normal or a Cyclical Peak?

For Micron, profit elasticity stems not only from shipment volumes but also from pricing and gross margins.

Consider that last quarter, Micron's non-GAAP gross margin reached 74.9%, and Q3 guidance is around 81%. This means for every $100 in revenue, Micron expects to retain over $80 in gross profit.

Such high gross margins are uncommon in past memory cycles. This is driven by a combination of factors: an increasing proportion of high-value products like HBM, widespread DRAM and NAND price increases and supply constraints, and a product mix shifting steadily toward data center applications.

Notably, the driver of Micron's margin expansion isn't solely HBM. Micron management has previously indicated that some non-HBM DRAM products are also exhibiting very strong profitability, occasionally even surpassing HBM in certain periods. This suggests the current memory upcycle is no longer limited to a high-end niche but is beginning to diffuse across the broader DRAM market.

Therefore, the most important aspect of this earnings report isn't just whether gross margin hits 81%, but how management describes the trajectory for Q4 and beyond.

If Micron provides guidance for gross margins continuing above 80%, it signals that the supply-demand gap and price appreciation trends remain robust, potentially prompting the market to raise its earnings power estimates further. However, if gross margins merely meet guidance, or if management's language regarding future margins turns cautious, the stock could experience a 'Sell the News' event.

3. When Will Capacity Expansion Fill the DRAM and NAND Gaps?

Every memory bull market eventually confronts the same question: when will supply catch up with demand?

The reason this cycle has consistently exceeded market expectations is two-fold. First, AI data centers are driving rapid demand growth for HBM, server DRAM, and enterprise SSDs. Second, memory production capacity cannot be unleashed simultaneously in the short term.

HBM, in particular, consumes more wafer and advanced packaging resources. Manufacturers allocating capacity towards HBM inevitably compresses the supply of traditional DRAM to some extent, thereby pushing up prices across the product line.

Micron has previously stated that in the medium term, it can only satisfy approximately one-half to two-thirds of customer demand, and some new fab contributions won't yield meaningful output until later stages. This implies new capacity is unlikely to quickly bridge the supply-demand gap in the near term.

However, the market will also focus on the other side of the coin. Driven by high profits, Micron, Samsung, and SK Hynix are all increasing capital expenditures. If new capacity ramps faster than AI demand growth, the memory industry could still revert to its traditional cycle of price competition and inventory adjustments.

Thus, in this conference call, management's commentary on customer inventories, order visibility, long-term agreements, and the pace of new capacity deployment may be more critical than single-quarter shipment volumes. The focus will be on whether Micron can demonstrate that demand growth continues to outpace supply addition for at least the next few quarters.

3. 13% Implied Volatility from Options: What is the Market Betting On?

Beyond the fundamentals, the options market has already provided another answer.

Based on option prices around the close of June 22, the combined price of at-the-money Call and Put contracts expiring June 26 was approximately $159. Relative to Micron's stock price of around $1,211, the options market implied an earnings-related move of roughly 13%.

This means that if you buy options today, theoretically, Micron's stock needs to move more than about 13% post-earnings for you to outpace the premium cost. For investors holding the underlying stock, this figure also signals that a double-digit gap move post-earnings is not unexpected.

In other words, the options market is not pricing in a small move; it is pricing in a very violent reaction to the earnings report.

More importantly, the high implied volatility itself reflects the current market divergence: some capital believes AI memory remains in an early, supply-constrained growth phase, while other capital fears the stock price has already discounted too much future growth.

Analyzing potential scenarios post-earnings, MSX Research identifies three main possibilities:

Scenario 1: Earnings Beat, Guidance Raised

This is the most favorable outcome.

If Micron's revenue, EPS, and gross margin exceed current market expectations, coupled with strong Q4 guidance, continued emphasis on smooth HBM4 ramp-up, improved 2027 order visibility, and sustained DRAM/NAND pricing power, the logic for the memory bull market would be further validated.

In this case, Micron's rally could rejuvenate the entire memory supply chain, including SanDisk, Western Digital, Samsung, SK Hynix, and some semiconductor equipment and AI server-related stocks.

However, even with strong earnings, one must watch for profit-taking at elevated levels. As noted, the options market has already priced in significant volatility, meaning a surge after-hours does not guarantee a one-way upward move in the following trading session.

Scenario 2: Good Earnings, but No Better Guidance

This is perhaps the most caution-worthy scenario for this report.

Micron could very well deliver a record-breaking earnings report. However, if the numbers merely confirm prior guidance, or if Q4 gross margin and revenue outlook are not raised further, the market may still choose to sell.

This isn't because Micron's fundamentals have suddenly deteriorated, but because the market has already priced in a "beat." Ultimately, for stocks at high valuations and high levels of crowding, meeting expectations can sometimes equate to falling short of expectations.

The recent sharp volatility in the South Korean market reinforces this risk. On June 22, South Korean regulators publicly reflected on the rapid approval of single-stock leveraged ETFs for Samsung and SK Hynix. A day later, the KOSPI index plunged nearly 10%, with both memory giants dropping over 12%.

This pullback doesn't necessarily signal a long-term reversal in AI memory demand, but it serves as a stark reminder: when high valuations, leveraged capital, and crowded trades coalesce around a single theme, any slightly disappointing information can be rapidly amplified.

Therefore, the decline in Korean memory stocks acts like a stress test before Micron's earnings: If Micron is strong enough, it can restore market confidence. If Micron is merely "normally good," the Korean market's correction might be interpreted as a signal that the whole memory trade is beginning to cool.

Scenario 3: Gross Margin or Forward Guidance Misses Expectations

If Micron shows a clear miss against market expectations in areas like HBM4 progress, gross margins, product pricing, or Q4 guidance, the stock could face even greater pressure.

The reason is that Micron's current stock price bakes in at least three layers of expectations:

- Layer 1: Long-term memory demand from AI computing expansion.

- Layer 2: A price-up cycle driven by tight DRAM and NAND supply-demand dynamics.

- Layer 3: Micron's continued improvement in market share and profitability within the high-end HBM segment.

A crack in any one of these layers could lead the market to simultaneously lower future earnings forecasts and valuation multiples. In such a scenario, the impact wouldn't be limited to Micron but could spread across the entire memory and AI hardware complex.

Conclusion

Based on currently available information, Micron's long-term thesis appears intact.

AI servers continue to consume more HBM and DRAM. Data center SSD demand is growing steadily. The traditional NAND market is also recovering. New capacity cannot be added quickly in the short-term, and supply constraints continue to provide memory manufacturers with strong pricing power.

However, strong fundamentals do not mean the stock is without risk.

When revenue, margins, and stock price are continuously setting new records, the market's yardstick for measuring Micron changes accordingly: Previously, the company only needed to prove the industry was recovering. Now, it must demonstrate that this upcycle is not only sustainable but even stronger than what investors have already envisioned.

Therefore, the true suspense of this earnings report is not whether Micron can deliver another good set of results, but whether it can once again raise the market's expectations for the future.

In a nutshell, what Micron needs to prove is not merely that the memory bull market continues, but that the finish line of this bull run remains further away than where the market is currently pricing it.