Saying goodbye to the Meme narrative, Solana staged a comeback with "US Stock DeFi"

- Core Insight: Solana has achieved an absolute leading position in the tokenized stock spot market, leveraging the efficient pricing mechanism of PropAMM and ecosystem composability, challenging the dominance of CEXs in this emerging track.

- Key Elements:

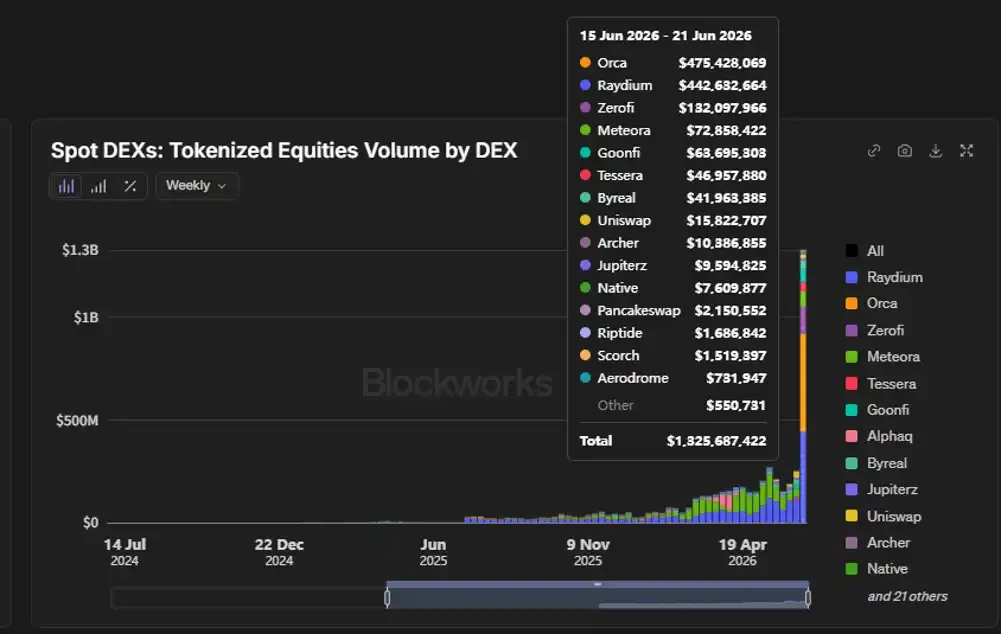

- Solana's tokenized stock trading volume last week reached $1.3 billion, far surpassing competing L1s such as Base (approx. $14.14 million) and BNB Chain (approx. $12.91 million).

- PropAMMs (e.g., Zerofi) contribute significant trading volume, employing an active pricing, closed-source, high-frequency quoting mechanism, achieving spot pricing efficiency close to that of mainstream CEXs.

- In the week following the SpaceX IPO, Solana set a single-week record of $1.04 billion, with $SPCX trading volume accounting for 91.7% of all tokenized SpaceX stock trading.

- In May this year, Solana's tokenized stock trading volume was approximately $870 million, ranking behind only Binance ($1.1B), Gate ($1.088B), and Bitget ($880M).

- On-chain DeFi protocols (e.g., Jupiter, Kamino) support tokenized stock lending and liquidity strategies, and the Nest protocol allows users to stake stocks to mint the stablecoin nUSD to earn yields.

There is no doubt that US stock trading has become a major new trend in the crypto space. When we talk about US stock trading in crypto, we often focus on it being "a competition between various CEXs and Hyperliquid."

Solana, a public chain widely viewed by players as centered around meme coins, has received relatively little attention in the US stock trading track. However, it has quietly entered this latest battle for the crypto market.

Solana Wins the Battle for the On-Chain Tokenized Stock Market

From Solana's official Twitter's recent activity, it's clear that a large number of its tweets are related to on-chain US stock trading. The night before last, Solana officially announced the launch of tokenized MU stock on Solana.

Clearly, as a public chain, Solana has also made US stock trading a recent key development focus. Looking at the data, they have done quite well, taking an absolute leading position in the competition for US stock trading among public chains.

One week after the SpaceX IPO, Solana recorded a single-week tokenized stock trading volume of $1.04 billion. The trading volume of $SPCX accounted for $439 million of that, representing 91.7% of all SpaceX tokenized stock trading volume.

In the past week (June 15-21), tokenized stock trading volume on Solana reached nearly $1.3 billion. Following behind were Base and BNB with approximately $14.1445 million and $12.9154 million respectively, while Ethereum mainnet saw only around $312,800.

Comparing various CEXs, Binance's tokenized stock trading volume in the past week was nearly $500 million, followed by Gate's nearly $220 million and Bybit's $107 million. In May's data, Solana also ranked behind only Binance (approx. $1.1 billion), Gate (approx. $1.088 billion), and Bitget (approx. $880 million) with a volume of about $870 million.

PropAMM has also made significant contributions to these achievements. Taking the past week's data as an example, the trading volume of PropAMMs like Zerofi, Goonfi, and Tessera ranked only behind Orca and Raydium.

These proprietary AMMs managed by professional market makers are 100% funded by the market makers' own capital. Unlike traditional simple x*y=k, open-source passive AMMs, these PropAMMs actively price themselves. They are closed-source, their liquidity is not publicly disclosed, they typically lack a front-end and are routed through aggregators, can update quotes multiple times every 50ms per block, and can also avoid MEV attacks.

In terms of spot asset price discovery efficiency, the gap between Solana and mainstream CEXs is already very small. Leveraging this spot efficiency advantage, the primary source of trading volume for various DEXs on Solana is now uniformly tokenized stocks.

"US Stock DeFi"

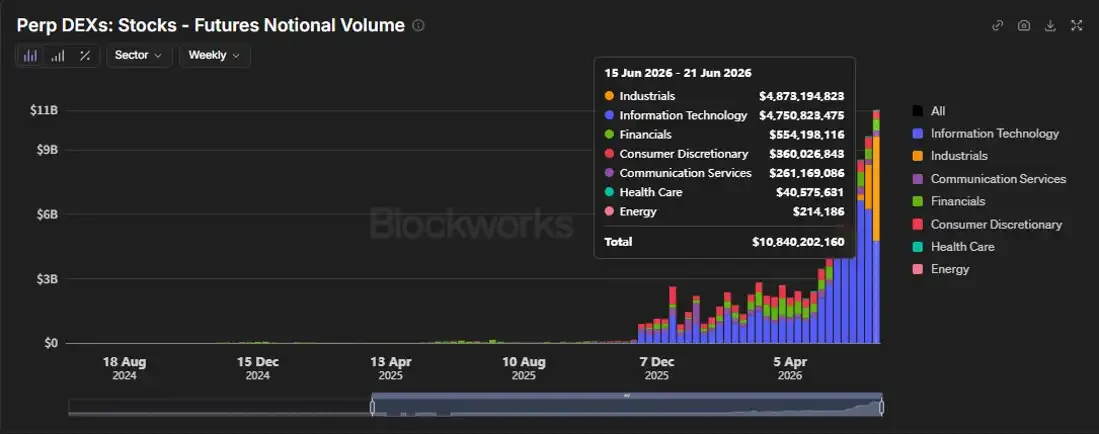

Although Solana's momentum in the tokenized stock spot market is strong, for US stock trading in the crypto space, perpetual contract trading volume still far exceeds that of spot. The stock trading volume of Perp DEXs in the past week was in the tens of billions of dollars:

Solana will likely ramp up efforts to catch up in this area as well. However, beyond trading, tokenized stock spots still have room for development. The composability of tokenized stock spots is a potential advantage for Solana.

Compared to simply trading stocks for profit, on-chain DeFi offers more diverse and flexible income channels for tokenized stock positions. On platforms like Jupiter, Raydium, and Kamino, users can use their held tokenized stocks for lending or providing liquidity. Users can execute portfolio strategies on their tokenized stocks, such as lending a portion while using another portion for liquidity provision.

Beyond these conventional DeFi strategies, some novel use cases have recently emerged on Solana. Nest allows users to mint the stablecoin nUSD using tokenized stocks or USDC.

nUSD can be staked to obtain snUSD and earn protocol-generated income (estimated 6% APY) and dividends.

After the protocol income is distributed, the remaining portion will be used to buy back and burn the governance token $NEST.

While looking forward to more new use cases, what is even more anticipated is Solana leveraging collaboration among projects within its ecosystem to promote stock DeFi-ification in a more prominent way (e.g., through more intuitive guidance in mobile apps) to on-chain players. Combined with cross-chain asset entry points like Sunrise, this could create network effects and achieve surprisingly differentiated competitive results in the tokenized stock derivatives market.