Institutions reaped 100x returns. Is Zhipu's stock price peaking?

- Key Point: Zhipu (02513.HK), as China's first AI stock, saw its share price surge 24.6 times post-IPO. This was driven by its government and enterprise on-premise deployment business, recognition of its GLM-5.2 model in the global tech community, and an extremely low free float (less than 4% at the initial listing stage). However, the upcoming lock-up expiration for cornerstone investors (July 8) and a high valuation (price-to-sales ratio exceeding 1,280x) constitute major risks.

- Key Elements:

- From its IPO to the intraday high on June 22, Zhipu's share price rose 24.6 times. Early investors (such as China Science & Merchants Venture Capital) achieved returns exceeding 100 times, while the book value per person on the employee shareholding platform reached hundreds of millions to billions of Hong Kong dollars.

- Core revenue comes from government and enterprise on-premise deployment. In 2025, this generated revenue of 534 million yuan (73.7% of total revenue), benefiting from government-driven procurement. However, the company remains unprofitable overall.

- The GLM-5.2 model received praise from executives like the CEO of Vercel within the English-speaking developer community, being regarded as an open-source model capable of replacing GPT/Claude. This triggered a global revaluation of Zhipu.

- The free float is extremely low: The IPO issuance accounted for only 9.65% of share capital, with cornerstone investors locking up nearly 70%. The tradable chips in the initial listing stage were less than 4% of total share capital, resulting in significant price elasticity.

- The unlock of cornerstone investor shares on July 8 will release approximately 25.68 million shares (5.76% of share capital), expanding the tradable pool by 2.5 times. This could alter the supply-demand dynamics and exert downward pressure on the stock price.

Original author: Jia Liu

The recent market hotspot is Zhipu (02513.HK), China's first AI stock.

If you had bought 1 million yuan worth of Zhipu in January this year, it would have been worth nearly 25 million yuan at its intraday peak on June 22, and still over 20 million yuan at the close. It is also one of the fastest companies in recent years on the Hong Kong stock market to go from a market cap of tens of billions at IPO to trillions of Hong Kong dollars.

Around this stock, three questions are repeatedly asked in the market: Who made this money? Why did it rise like this? Who will take over next?

This article is written to answer these questions.

Fastest Wealth Creation Wave in Hong Kong Stocks in Recent Years

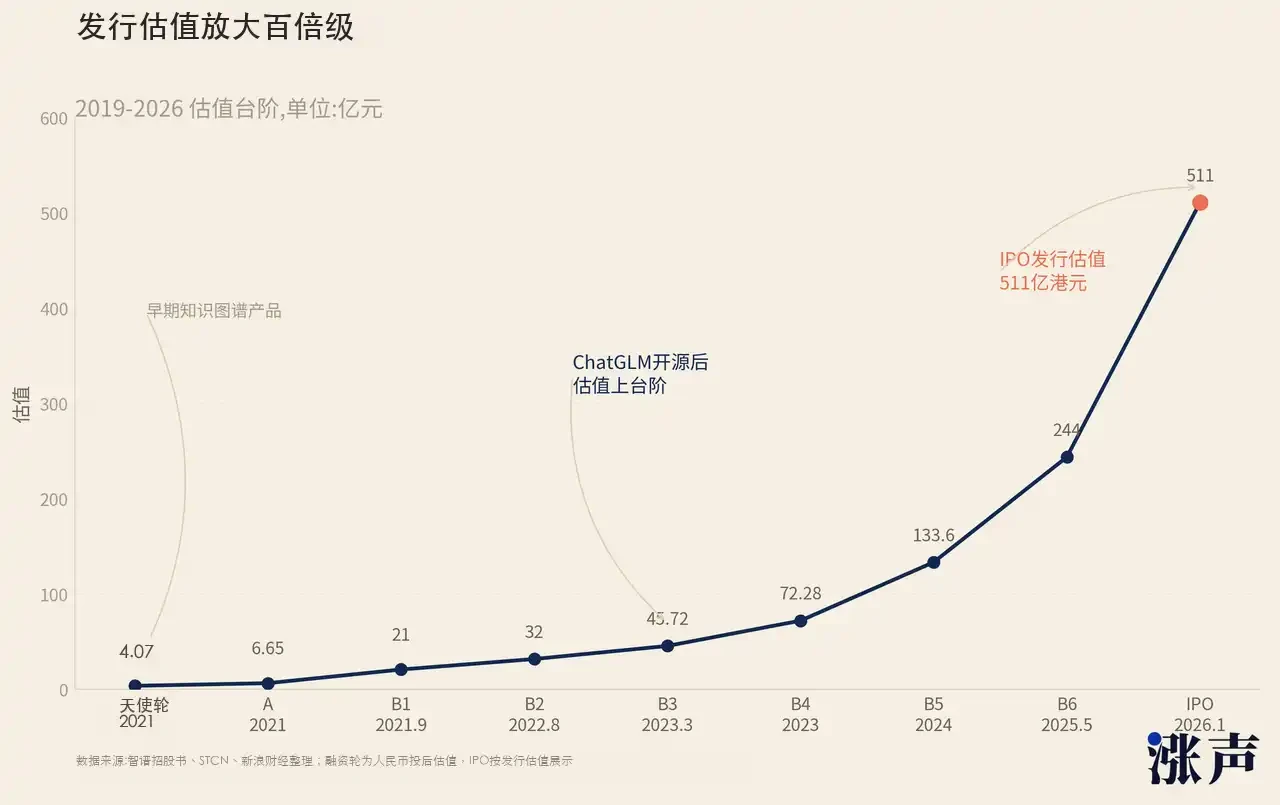

From angel round to IPO, Zhipu's valuation has increased by about 130 times. From IPO to the intraday high on June 22, Zhipu's stock price has risen another 24.6 times.

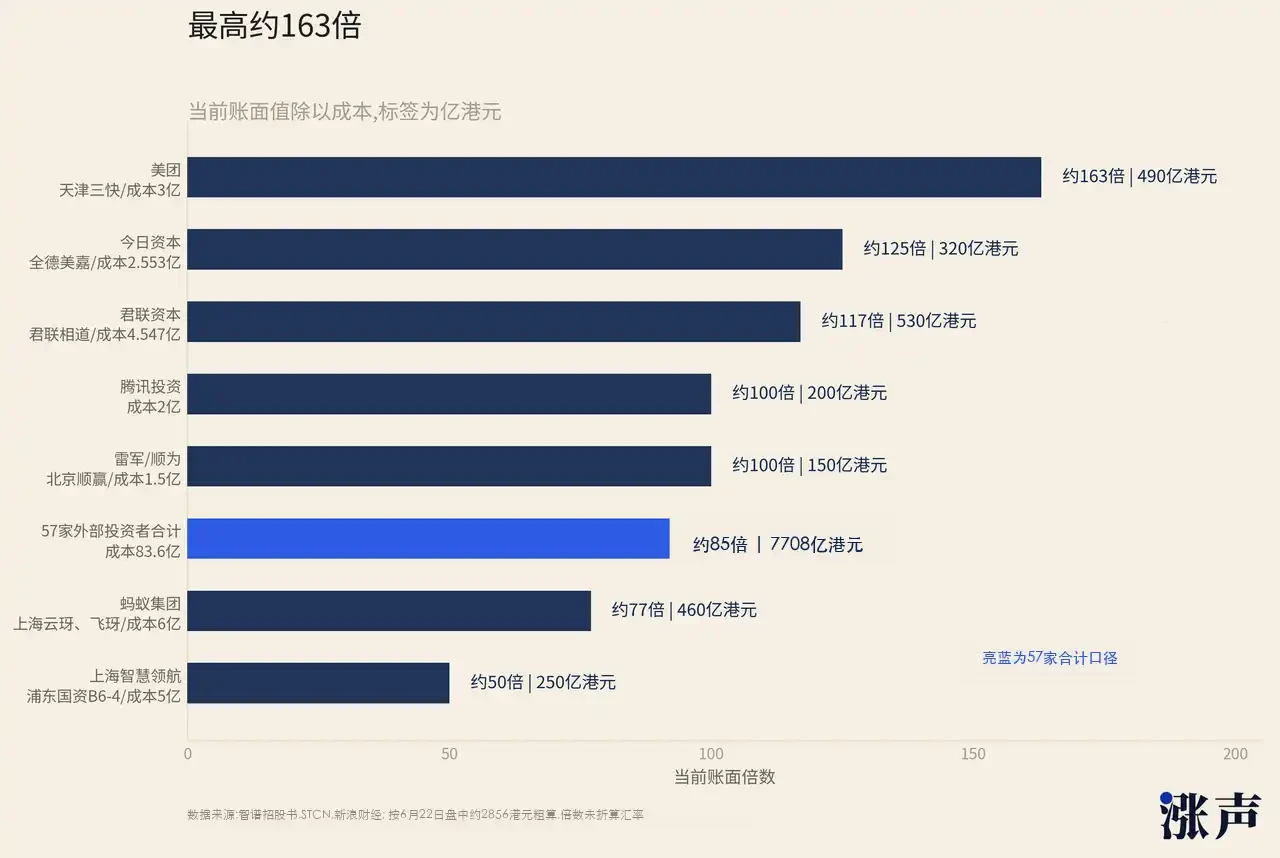

57 external investors invested a total of 8.36 billion yuan. At the intraday high on June 22, the total book value was about 770.8 billion Hong Kong dollars. The overall return was about 85 times. In the history of China's primary market, you can count on one hand the number of cases where a single project achieved an average return of 85 times for all investors.

According to the prospectus, Zhipu's financing is categorized as "three rounds, fourteen times." The returns for the earliest money are particularly astonishing.

China Innovation Xingye is the most extreme case in terms of return multiple. According to the prospectus, it invested about 20.37 million yuan in the angel round, corresponding to a post-investment valuation of about 407 million yuan. At that time, Zhipu was still a knowledge graph team spun off from Tsinghua's KEG lab; the concept of large models didn't even exist. Over 20 million yuan turned into tens of billions of Hong Kong dollars. This is one of the most extreme cases of single-investment return multiples in the history of China's AI primary market.

The same goes for Series A and Series B investors. Roughly calculated based on the intraday high on June 22 and market cap, funds entering in Series A have already multiplied by several hundred times, and Series B is close to a hundred times.

The numbers for the subsequent institutions are also staggering. Xu Xin's Capital Today invested 255.3 million yuan in November 2023, receiving 11.35 million shares. Based on the intraday high on June 22, the book value is roughly over 30 billion Hong Kong dollars, a return of over a hundred times. Capital Today manages about $3 billion. This means the book value of this single Zhipu investment has exceeded the size of her entire fund. Xu Xin previously invested in NetEase, JD.com, and BOSS Zhipin, but in terms of absolute amount, Zhipu is likely the most profitable investment of her career.

The Meituan example is also intuitive. According to available information, Meituan invested about 300 million yuan at the time, and now the book return is over 150 times. In other words, the paper profit from one industrial investment has exceeded 5% of Meituan's own market cap.

Lei Jun's Shunwei Capital invested 150 million yuan through Beijing Shunying. Based on the intraday high on June 22, the book value is roughly 14.8 billion Hong Kong dollars, a return of about 90 times. Shunwei manages nearly 50 billion yuan, and this Zhipu investment accounts for about a quarter of its total scale.

Junlian Capital made the largest absolute amount. It followed up 6 times, investing a total of 454.7 million yuan. Based on the intraday high on June 22, the book value is roughly 53.3 billion Hong Kong dollars, a return of about 107 times. Junlian manages over 90 billion yuan in total. The book value of this single Zhipu investment is close to half of its total management scale. An established PE that invested in iFLYTEK, CATL, and WuXi AppTec eventually achieved a historic single-project return with Zhipu.

Besides market-oriented institutions, Zhipu also has a high density of state-owned capital shareholders. State-owned capital from Beijing, Tianjin, Shanghai, Hangzhou, Zhuhai, Chengdu, and Daxing is all involved. Zhongguancun Science City, Zhuhai Huafa, Haihe Fuxin Youda Fund, AI Fund, Hangzhou Chengtou, Daxing Industrial Fund – these are all well-known local government investment platforms. The Social Security Fund Zhongguancun Independent Innovation Investment Fund also participated.

This capital inflow isn't just financial investment. After they come in, they drive procurement by the government systems of their respective cities and provinces. If a local state-owned capital invests in Zhipu, when the local government selects a large model supplier, Zhipu gains a natural advantage. This is a very clear characteristic of China's tech industry: the wealthiest buyer is the government. If a tech project can secure government investment and support, it's half successful. Zhongji Innolight and CXMT are precedents for this model: founders bring technology back from overseas, the government invests in factories and provides orders, and the company scales up quickly.

Employees are also big winners in this wealth creation round. Zhipu has a heavy employee stock ownership plan. Two employee stock ownership platforms together hold about 15% of the company. The 25 employees on the Zhideng platform had an average stock market value exceeding 100 million Hong Kong dollars per person at the time of the IPO. Based on the intraday high on June 22, this has become tens of billions of Hong Kong dollars per person. For the other platform, Huihuili, after removing the founder's equity, the rough calculation for over 400 employees based on the June 22 high is also in the hundreds of millions of yuan per person.

This density of wealth creation ranks among the very top in the history of Chinese tech company listings.

When Kuaishou went public in 2021, it also mass-produced "paper billionaires," but Kuaishou's IPO market cap was larger, its employee base was larger, and the wealth was distributed more evenly. Zhipu is a company with fewer than 900 people. Core stock options are concentrated in the hands of a very small number of early employees. After the IPO, combined with the maximum intraday gain of 24.6 times, the book numbers each person received became extremely exaggerated.

Why Did Zhipu Rise So Sharply? The Capital Game Behind the Narrative's Glory

This is a rare case of collective wealth creation: early VCs, local state-owned capital, internet giants, competitors, founding teams, and core employees – all were repriced by the public market on the same project. So why did it rise to this extent?

The first thing the market saw was that it did have a business capable of generating revenue.

Zhipu's most solid revenue doesn't come from C-end chat products or the developer community, but from localized deployment. Simply put, it means installing the entire GLM large model suite into the client's own servers and intranet, so data doesn't leave the local environment. The buyers are mainly government agencies, state-owned banks, energy groups, and smart city projects. For the full year of 2025, localized deployment revenue was 534 million yuan, a year-over-year increase of over 100%, accounting for 73.7% of total revenue, with a gross margin of 48.8%. For a large model company still incurring losses, this business at least proves it's not just a pure narrative.

The pricing for local deployment roughly falls into several tiers. District/county governments and small/mid-sized enterprises use a lightweight version, with an annual fee of around several hundred thousand yuan. Municipal governments and ordinary state-owned enterprises buy the standard general version, with a three-year package costing one or two million yuan. Provincial departments, top-tier banks, smart city projects, meteorological bureaus, and energy groups use the flagship version, with annual fees possibly reaching several million yuan, plus operation and maintenance upgrade fees. A single project isn't astronomically priced, but China has dozens of provincial-level administrative regions, hundreds of prefectural-level cities, thousands of districts and counties, plus vertical sectors like finance, energy, and transportation.

As long as government and enterprise AI budgets persist, Zhipu's revenue ceiling won't be too low.

The shareholder structure also endorses this business. Names like Zhongguancun Science City, Zhuhai Huafa, Hangzhou Chengtou, Chengdu High-tech Zone, and Pudong State-owned Capital don't just appear on the shareholder list because they want to make stock profits. After they invest, they often drive local demonstration projects, government system procurement, and industrial park cooperation. There's a long-standing similar path in China's tech industry: the government provides money, scenarios, and orders; the company takes the project and scales up quickly. In the past, chips, storage, and new energy vehicles have followed similar paths. Zhipu is just applying this logic to large models.

But if it were only government and enterprise deployment, Zhipu wouldn't have risen to where it is today. What truly ignited the second wave of sentiment was the rediscovery of GLM-5.2 in the English-speaking tech community.

In mid-June, Z.ai released GLM-5.2, focusing on coding and agents, supporting a 1 million token context, MIT open-source weights, and keeping API prices unchanged. It didn't immediately create a huge buzz on the Chinese internet, as domestic large model topics are often diverted by DeepSeek, Tongyi, and Hunyuan. However, the English-speaking developer community reacted very quickly.

Vercel CEO Guillermo Rauch said on X that GLM-5.2's coding ability "really impressed him, almost shocking." Matt Velloso, a former executive at Meta, Google DeepMind, and Microsoft, also called it the first open-source model to reach the threshold for daily use. Other developers switched their daily work to GLM-5.2 and found they no longer needed to switch back to GPT or Claude for many tasks.

This type of viral spread is very important for Zhipu. Chinese investors look at Zhipu and see a Tsinghua-affiliated company, state-owned capital, government/enterprise deployment, and a scarce AI target on the Hong Kong stock market. The English-speaking tech community sees GLM-5.2 and asks a different question: Can it replace part of Claude and GPT? Can it be deployed locally? Is it open-source? Is the cost low enough?

When overseas developers, AI infrastructure companies, and English-speaking investors start discussing Zhipu within this framework, it is no longer just a local Chinese government/enterprise AI story. It becomes a target that can be driven by the global revaluation logic of the model layer assets.

The market is no longer buying just the over 500 million yuan in localized deployment revenue from 2025. It's buying a possibility: if open-source models can truly approach closed-source models, if Chinese model companies can drive down inference costs, and if unlisted tech giants like OpenAI, Anthropic, and SpaceX continue to raise the valuation anchor for model layers and hard-tech assets, then Zhipu, as one of the few listed model companies that can be directly bought on the public market, will naturally command a premium.

Of course, there's a big question here. Whether developer enthusiasm can ultimately translate into API revenue, local deployment contracts, and high-margin cash flow has not yet been fully proven. But during a stock price rally, the market often trades on possibility first and asks about the profit statement later. GLM-5.2 gave Zhipu a new narrative entry point and a reason for overseas funds to buy.

There is an even more direct and important reason: the freely tradable shares are too few.

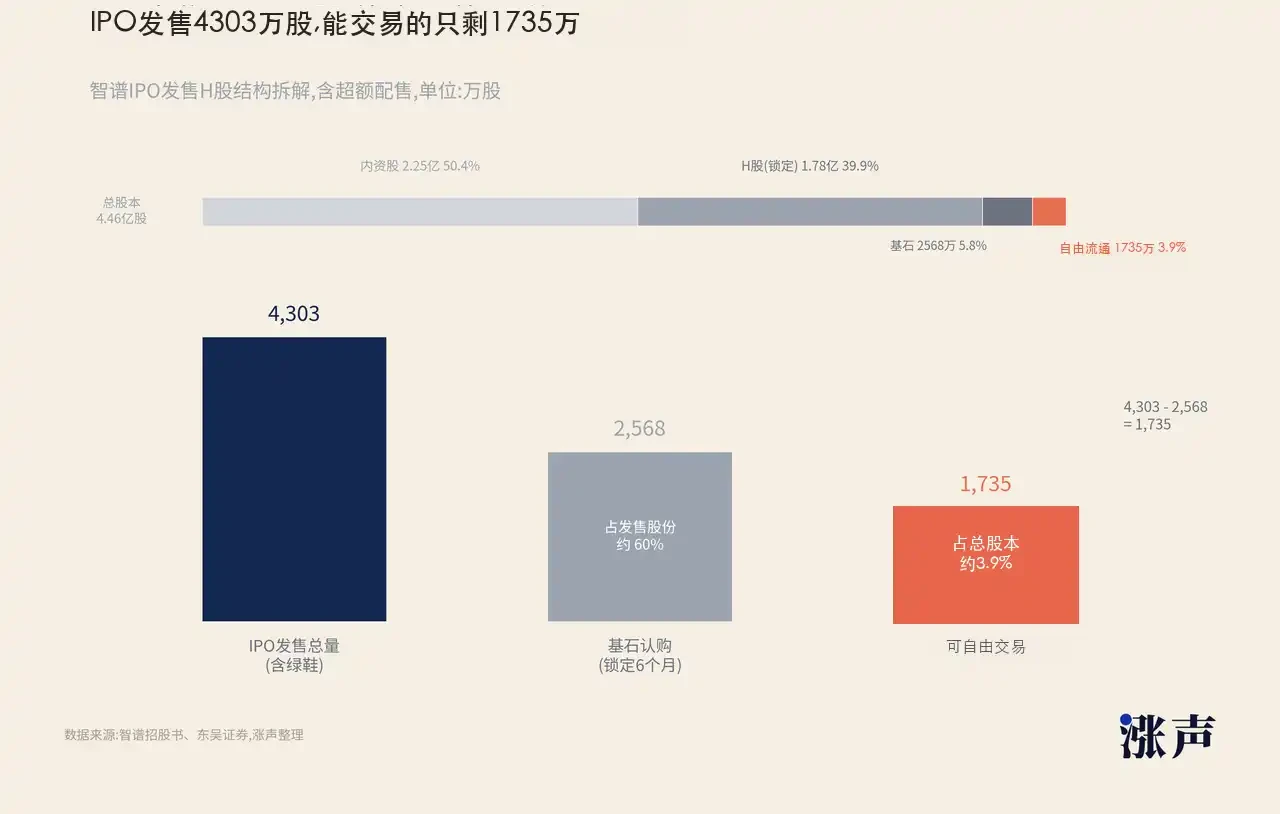

Many people see the IPO share figures in Dongwu Securities research reports and think Zhipu's tradable shares are 221.31 million, accounting for about 49.6% of the total share capital, which isn't low. But it's crucial to distinguish between "tradable shares" and "free float." Zhipu is a joint-stock company registered in Mainland China and listed in Hong Kong. The "tradable shares" in the research report likely refer to the H-share count listed. However, a significant portion of these H-shares are still locked up in the initial stage of listing and cannot be traded immediately. What truly determines stock price elasticity is how many shares are available for free buying and selling in the market each day.

Looking at the IPO structure, Zhipu's global offering was about 37.4195 million H-shares. Including the over-allotment option, the total issuance was about 43.03 million shares, accounting for about 9.65% of the total share capital. This is already less than one-tenth of the total equity. More critically, the majority of the IPO shares were taken by cornerstone investors. 11 cornerstone investors subscribed for a total of about 2.984 billion Hong Kong dollars, accounting for nearly 70% of the offered shares. Cornerstone investors usually have a 6-month lock-up period. For this batch of Zhipu, the corresponding unlock date is July 8, 2026.

In other words, out of the 43.03 million newly issued IPO shares, approximately 25.68 million are locked up by cornerstone investors. In the initial stage after listing, only about 17.35 million shares were truly freely tradeable, which is less than 4% of the total share capital. A company with a superficial market cap of over a trillion Hong Kong dollars, yet only less than 4% of its shares are floating in the market. As soon as buying pressure concentrates even slightly, the price is amplified significantly.

This is not unique to Zhipu. Low free float with high market cap has become very common in the capital markets in recent years.

The most typical example is SpaceX's listing a few days ago. Publicly tradable shares were less than 5%, but the company's IPO valuation was already close to $1.77 trillion. It closed up 19% on the first day, briefly rising near 30%. Everyone globally wants to buy SpaceX, but very few shares are actually available to buy.

CoreWeave, Circle, and Figma, these 2025 US stock IPOs, had similar operations. CoreWeave reduced its IPO size, resulting in limited initially tradeable shares, but later surged driven by the AI computing narrative and Nvidia's shareholding catalyst. Circle sold a relatively small number of shares compared to its total equity, and once the stablecoin regulation narrative took off, its price shot up several times soon after listing. When Figma went public, the total issuance and secondary sale accounted for less than one-tenth of its total equity, and its stock price multiplied several times on the first day.

Although the company perspectives differ, the market structure is very similar: grand narratives, large market cap expectations, small free floats.

Hong Kong stocks also have their version. When CATL's H-shares were listed, only a small portion of shares were traded in Hong Kong, but it represented a global battery giant already priced in the A-share market, leading to a first-day gain exceeding double digits. For Hong Kong capital, it wasn't just buying a new stock; it was buying a scarce core Chinese asset directly tradeable in a Hong Kong stock account. Zhipu follows a similar logic now, except the asset label has changed from power batteries to large models.

Will the Upcoming "Massive Unlock" Cause a Sell-off?

Government/enterprise business provides the revenue base, GLM-5.2 provides the global technology narrative, and low free float provides stock price elasticity. This has pushed Zhipu's stock price to where it is now.

But the sharper the rise, the more direct the subsequent questions become: Who will take over next?

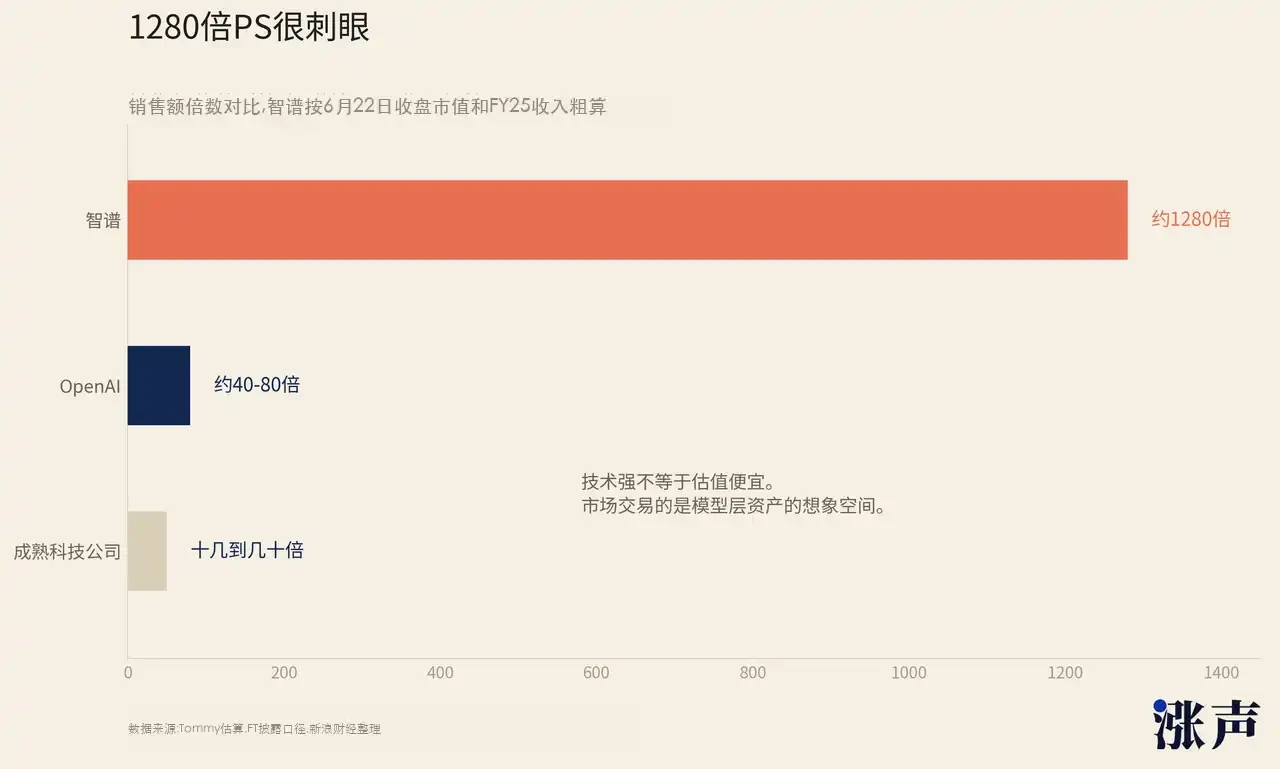

First, consider the valuation. Zhipu's closing market cap on June 22 was about $137 billion. Its full-year 2025 revenue was about $100 million, corresponding to a price-to-sales ratio of about 1280 times. This multiple has detached from any traditional valuation framework.

Nvidia, Tesla, Palantir – these companies, frequently discussed in the market for being "too expensive," were mostly trading at tens of times sales at their peak. OpenAI, based on FT's disclosed 2025 revenue of about $13 billion and a $730 billion valuation, trades at roughly 56 times sales. Zhipu is at 1280 times.

Applying OpenAI's multiple to Zhipu's revenue, Zhipu's "reasonable" market cap would be between $4 billion and $8 billion. Even using J