Storage is still rising, but smart money is starting to position in this "flash memory chain"

- Core Viewpoint: AI computing power is constrained by expensive and scarce memory (DRAM). Giants like AMD, NVIDIA, and SanDisk are pushing to partially replace DRAM with cheaper flash memory (NAND). This "flash memory substitution" logic will create new incremental demand for the NAND industry chain, while segments whose valuations have not yet fully reflected this change (such as controller chips) offer higher cost-effectiveness.

- Key Factors:

- The surging demand for High Bandwidth Memory (HBM) in AI chips has led to tight DRAM capacity. Contract prices in Q1 2026 are expected to rise over 90% quarter-over-quarter, and HBM is projected to account for 25% of DRAM wafer output, resulting in a high "memory tax."

- AMD's acquisition of MEXT, NVIDIA's launch of CMX, and SanDisk and SK Hynix's HBF standard project—these three giants are exploring solutions to move AI data from DRAM to NAND flash memory to achieve cost reduction and efficiency gains.

- Within the NAND industry chain, original manufacturers and module makers (such as SanDisk and Longsys) have already been fully priced in based on the "price hike logic." In contrast, the controller chip segment (Silicon Motion, Phison, Lianyun) benefits from SSD shipment growth, but their valuations lag behind relatively.

- The top three independent SSD controller manufacturers globally are Silicon Motion (SIMO), Phison (8299.TW), and Lianyun Technology (688449). Among them, Lianyun has the largest valuation gap due to its high R&D expense ratio of 36%-38%, which compresses profits.

- HBF (High Bandwidth Flash) is expected to sample in the second half of 2026, with a projected market size of approximately $12 billion by 2030. This will drive demand for advanced packaging (JCET, Tongfu Microelectronics) and packaging materials (Huahai Chengke), but at this stage, it remains mostly expectation-based, with a mix of genuine and speculative concept stocks.

Original Author: David

Preface: SanDisk surged about 40 times in 16 months after its IPO. A-share Longsys saw its Q1 net profit soar 26 times year-on-year... Storage is the hottest track of 2026, without exception. However, since June, three industry giants – AMD, NVIDIA, and SanDisk – have almost simultaneously done the same thing:

Find ways to use less expensive memory (DRAM) and shift workloads to cheaper flash storage (NAND). Along this "flash replacement" undercurrent, leading stocks have already taken off, but the truly unpriced opportunities may lie hidden in their upstream and downstream sectors.

Understanding AI's Constraint: The "Memory Tax"

Just a few numbers suffice to show how fierce the current storage market rally has been.

SanDisk (SNDK), spun off from Western Digital in February 2025 at an IPO price of around $38, reached approximately $2000 by mid-June 2026 – a nearly 40-fold increase in 16 months, with a P/E ratio of about 69x. Not to mention Micron.

On the A-share side, Longsys reported a net profit of 3.862 billion RMB for Q1 2026, a year-on-year increase of 2644%. GigaDevice's Q1 net profit surged 522% year-on-year, hitting its historical high on June 17th. The previous consensus in the entire market seemed to be just one sentence:

AI is desperately short of storage, shortages will persist until 2028, just buy storage stocks and watch them rise with your eyes closed.

But while everyone revels in the "shortage," the most influential companies are quietly planting landmines in this narrative.

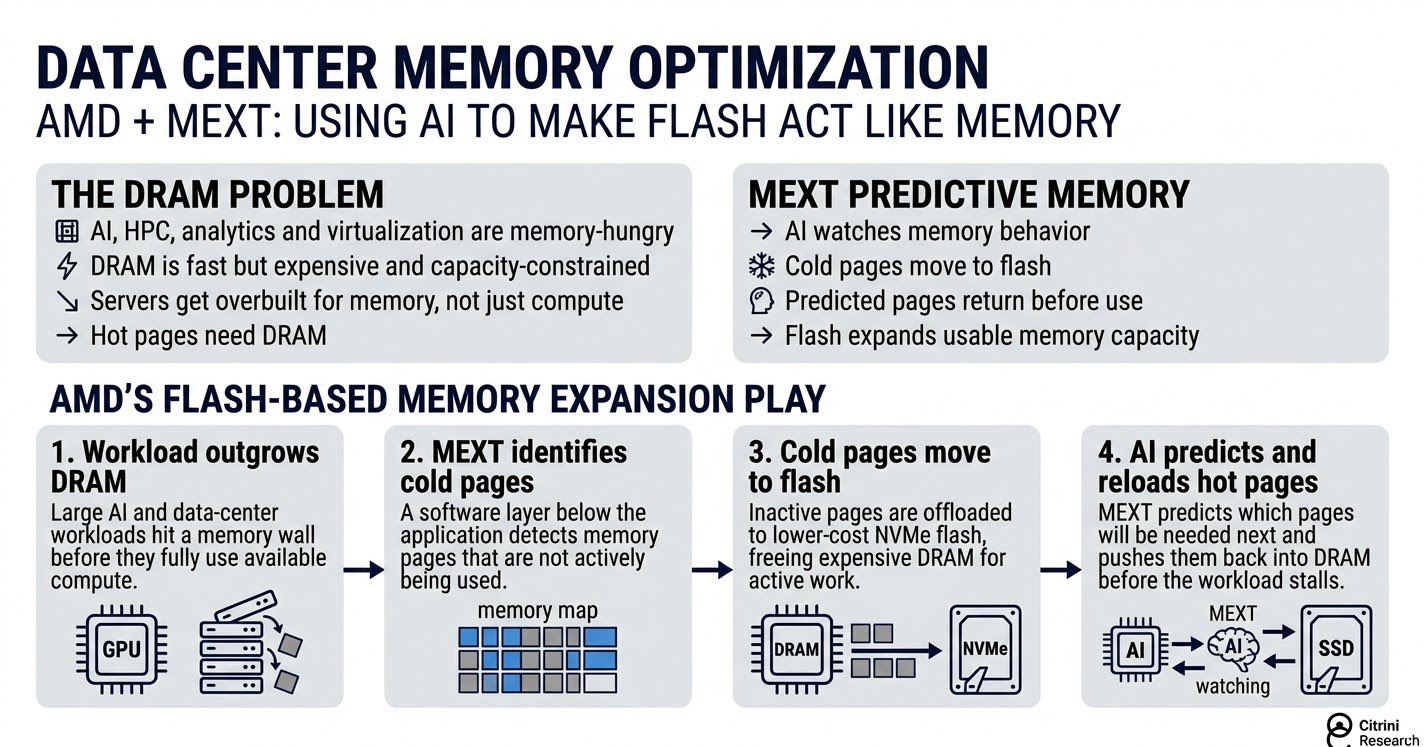

On June 15th, AMD announced the acquisition of a company called MEXT, whose core technology uses AI to make flash memory "pretend" to be memory.

Going further back, NVIDIA launched CMX at CES and GTC in early 2026, shifting the most memory-intensive data during AI runtime to the flash layer. Even earlier, in February, SanDisk and SK Hynix jointly initiated a new standard called HBF, aiming to fit flash memory into packaging previously reserved exclusively for high-end memory (HBM).

Looking at these three events together, the direction is completely aligned:

Create an intermediate memory layer for AI that is "cheaper than memory, faster than hard drives," reducing the need to pay the premium for expensive DRAM. Overseas thematic investment research firm Citrini Research even coined a term for this phenomenon: "The AI Tax."

To understand this term and follow it to find investment targets, you first need to distinguish between AI's two types of "memory."

One is memory, i.e., DRAM, and its highest-end form, HBM (High Bandwidth Memory, specifically attached to GPUs). It's fast, allowing the GPU to retrieve data instantly, but extremely expensive and has limited capacity.

The other is flash memory, i.e., NAND. This is what's inside your computer's solid-state drive (SSD). It's cheap and has large capacity but is slower. To use an imprecise but practical analogy: DRAM is like files spread out on your desk, immediately accessible. NAND is like inventory in a warehouse downstairs – cheap and plentiful, but retrieving it takes a trip.

The problem facing AI development over the past two years is clear: the "desk" (DRAM) isn't big enough, and it's outrageously expensive.

TrendForce data shows that DRAM contract prices rose over 90% quarter-on-quarter in Q1 2026. Citi predicts an average DRAM price increase of 88% for the full year 2026, and a 74% increase for NAND. The root cause of these price hikes is AI:

NVIDIA GPUs need to be fed data. HBM is both fast and expensive. Consequently, HBM has been consuming an increasing share of DRAM production capacity.

Data cited by Citrini shows HBM's share of total DRAM wafer output rising steadily from 2% in 2020 to roughly 21% in 2025, and an estimated 25% in 2026... This means a quarter of memory production capacity is taken up by HBM, leaving the rest tighter and more expensive.

This is the origin of the "Memory Tax."

For AI to run fast, it is forced to pay an increasingly high "tax" for expensive, scarce memory. When the tax becomes too heavy, naturally people look for tax avoidance. The only path is to shift some of the workload originally burdening DRAM onto cheaper NAND flash memory.

The three actions taken by AMD, NVIDIA, and SanDisk mentioned earlier are essentially different paths of "tax avoidance." But their shared effect is to add an intermediate memory layer for AI that is "cheaper than memory, faster than hard drives."

The investment significance lies precisely in this "shifting." Every workload shifted to flash memory means additional demand directed into the NAND supply chain. Leading storage stocks have already rallied once due to "shortage-induced price hikes." The "flash replacing DRAM" theme is the secondary layer of logic layered on top of the price hikes.

Its target isn't necessarily the already-skyrocketing leaders, but rather the links in this chain that haven't yet been priced for this logic. That's what's worth digging into.

Dissecting the Flash Memory Supply Chain: Foundries Feast, Controller Makers Sell the Tools

The flash memory business, from wafer to the drive in your hand, can be roughly divided into three layers. The further upstream you go, the more profitable and monopolistic it becomes.

- The very top is the NAND foundries, the ones who manufacture the wafers themselves:

Samsung, SK Hynix (after merging with Kioxia), Micron, and SanDisk (spun off from Western Digital). They control production capacity and profit the most during price up-cycles.

- The middle layer consists of module manufacturers, who buy wafer chips from foundries and package them into SSDs, memory modules for sale to end-users:

They don't manufacture wafers but profit from processing and branding. Their earnings elasticity can be even more dramatic than the foundries. When chip prices rise, their low-cost inventory instantly appreciates in value.

A-share companies like Longsys, Biwin Storage Technology, and Team Group belong to this layer. Longsys reported a Q1 2026 net profit of 3.862 billion RMB (up 2644% YoY), while Biwin saw 1567% growth in the same period.

However, elasticity is a double-edged sword. Once chip prices fall, inventory becomes a liability. Module manufacturers are the first to feel pressure in a downturn cycle.

- The third layer, often the most overlooked, is the controller chip:

Besides the flash memory chips, an SSD has a "brain" responsible for scheduling data input and output – this is the controller. It doesn't directly benefit from chip price increases, but as long as SSD shipments grow, demand for controllers grows.

Theoretically, this layer is the closest thing to a "pick-and-shovel seller" in this chain. The global top two independent controller makers are Taiwan's Silicon Motion (SIMO) and Phison (8299.TW). A-share Maxio Technology (688449) ranks third.

Currently, the foundries and module manufacturers among these three layers are fully priced for the market's "price hike logic." Their stock prices reflect the present reality of shortage-driven price increases.

"Flash replacing DRAM" is the secondary logic layered on top of the price hikes. It benefits not just price increases, but more importantly, the long-term amplification of SSD/flash memory shipment volumes.

The links that should benefit most from this logic are precisely the ones driven by shipment volume and haven't been swept up by price hike hype – such as the controller makers, and the new increments specifically spawned by HBF, which we'll discuss next.

Truly Unpriced: The Controller's "Value Gap" and HBF's "New Pie"

Links driven by shipment volume, yet not carried away by the price hike rally. Delving deeper, we find two areas.

First area: The valuation gap for controllers.

Maxio Technology (688449) is a case study. It's the world's third-largest independent SSD controller maker, behind Taiwan's Silicon Motion and Phison. Its PCIe 5.0 controller is one of the few capable of mass production in China.

However, as of April 2026, its market cap was still below its IPO day peak, its stock price lagging far behind A-share module makers like Longsys and Team Group... The reason is probably not complicated:

Controllers don't directly benefit from chip price hikes. During the half-year surge in chip prices, capital flocked en masse to module makers with the highest elasticity, leaving controllers behind.

But the author believes this is precisely the divergence point between the "price hike logic" and the "shipment volume logic." Chip price hikes benefit foundries and module makers holding inventory; controllers don't share in that. However, flash memory replacing DRAM leads to a long-term amplification of SSD shipments. Every additional SSD sold requires an additional controller.

If this thesis holds, the beneficiary is shipment volume, not price hikes. Controllers are a purer play on this theme.

There are three key players in this layer:

Silicon Motion SIMO (US ADR): The global #1 independent controller maker, holding over 30% global market share in consumer SSD controllers.

Phison 8299.TW (Taiwan stock): Global #2 independent controller maker. Kioxia's custom controllers come from them.

Maxio Technology 688449 (A-share): Global #3 independent controller maker. Technologically the most advanced among domestic Chinese controller companies, and also the one with the largest valuation gap.

However, risks must be stated clearly. Controllers are not a highly monopolistic segment. There are many domestic players, and price wars are ongoing. Public data shows Maxio's own R&D expense ratio is as high as 36%-38%, continuously compressing profits. The "global #3" market share does not equate to high profits.

Second area: The "new pie" fostered by HBF.

First, what is HBF?

HBM is fast, expensive, and consumes a quarter of DRAM production capacity. So, SanDisk and SK Hynix came up with a solution: stack NAND flash memory to create a replacement layer similar in form factor to HBM, but with 8 to 16 times the capacity and at a fraction of the cost. This is HBF (High Bandwidth Flash).

It doesn't steal HBM's job; rather, it acts as a "large-capacity warehouse" right next to HBM, specifically designed for AI inference data that 'can't fit in HBM but isn't worth relegating to cold storage.'

The process for making HBF involves TSV (Through Silicon Via – drilling holes in chips for vertical connections) to stack multiple layers of NAND and then bonding them for packaging – the same technology used for HBM. This process will drive demand for advanced packaging, assembly & testing, and specialized materials. Technically related targets include:

JCET Group 600584, Tongfu Microelectronics 002156 (A-shares): The twin giants of domestic OSAT (Outsourced Semiconductor Assembly and Test). The stacking and bonding processes used for HBF fall within their capability scope.

Wah Hing Choi Technology 688535 (A-share): The only domestic company capable of mass-producing GMC, the core packaging material for HBM. The technology is extendable to HBF due to common processes.

However, this area feels more like an unrealized expectation, and several points need attention.

First, HBF is not yet in mass production. SanDisk's timeline is sampling in the second half of 2026 and initial equipment shipments in early 2027. Currently, all "benefits" are anticipatory; not a single cent has entered financial reports.

Second, the total addressable market isn't as huge as one might think. According to forecasts cited by SK Hynix, the HBF market will reach approximately $12 billion by 2030, compared to HBM's ~$117 billion. HBF is less than a rounding error. It's a supplementary layer, not a disruptor.

Third, A-shares have already spawned numerous "HBF concept lists". Companies like E-Sheng Materials, PhiChem, ACM Research, and Quick Intelligent Equipment are frequently mentioned. Most of these companies are only "theoretically possibly related," without any actual HBF-related orders or disclosed process validation. This is typical concept speculation.

Their situation is entirely different from companies like JCET and Wah Hing Choi, whose "processes are genuinely linkable." They must be evaluated separately.

Therefore, these two areas can be seen as the present and future narratives under the same investment theme.

Controllers represent a "value gap" that is *shipping now* but whose valuation hasn't yet reflected the *replacement logic*. This is a tangible play. HBF's new increment is a "distant option" with a sexy story but payoff expected after 2027. This is a more conceptual play with significant hype-stock risks.

One Chart to Understand the Entire Market: Along the Supply Chain, Where Are the Targets and Are They Expensive?

Let's consolidate the segments discussed earlier into a map.

Based on real geographic distribution, this chain is concentrated in four markets: NAND foundries are in the US, Japan, and South Korea; controllers are on US ADRs and Taiwan stocks; modules, OSAT, and materials are almost entirely on A-shares. Hong Kong stocks have no pure flash memory plays, so none are forced in here.

When reading this chart, remember one coordinate:

The further upstream (foundries), the more monopolistic and beneficial the position, but also the most fully priced and expensive in valuation. Moving downstream (modules, controllers, OSAT, materials), elasticity and certainty vary; some haven't yet been priced for the "replacement logic."