如何实现Crypto的基准利率?

- 核心观点:加密货币市场缺乏统一的基准利率,尽管存在多种利率候选(如永续资金费率、借贷利率),但没有任何单一指标能同时满足“宽口径、有期限结构、治理独立”的标准,导致整个金融体系缺乏可信的定价锚。

- 关键要素:

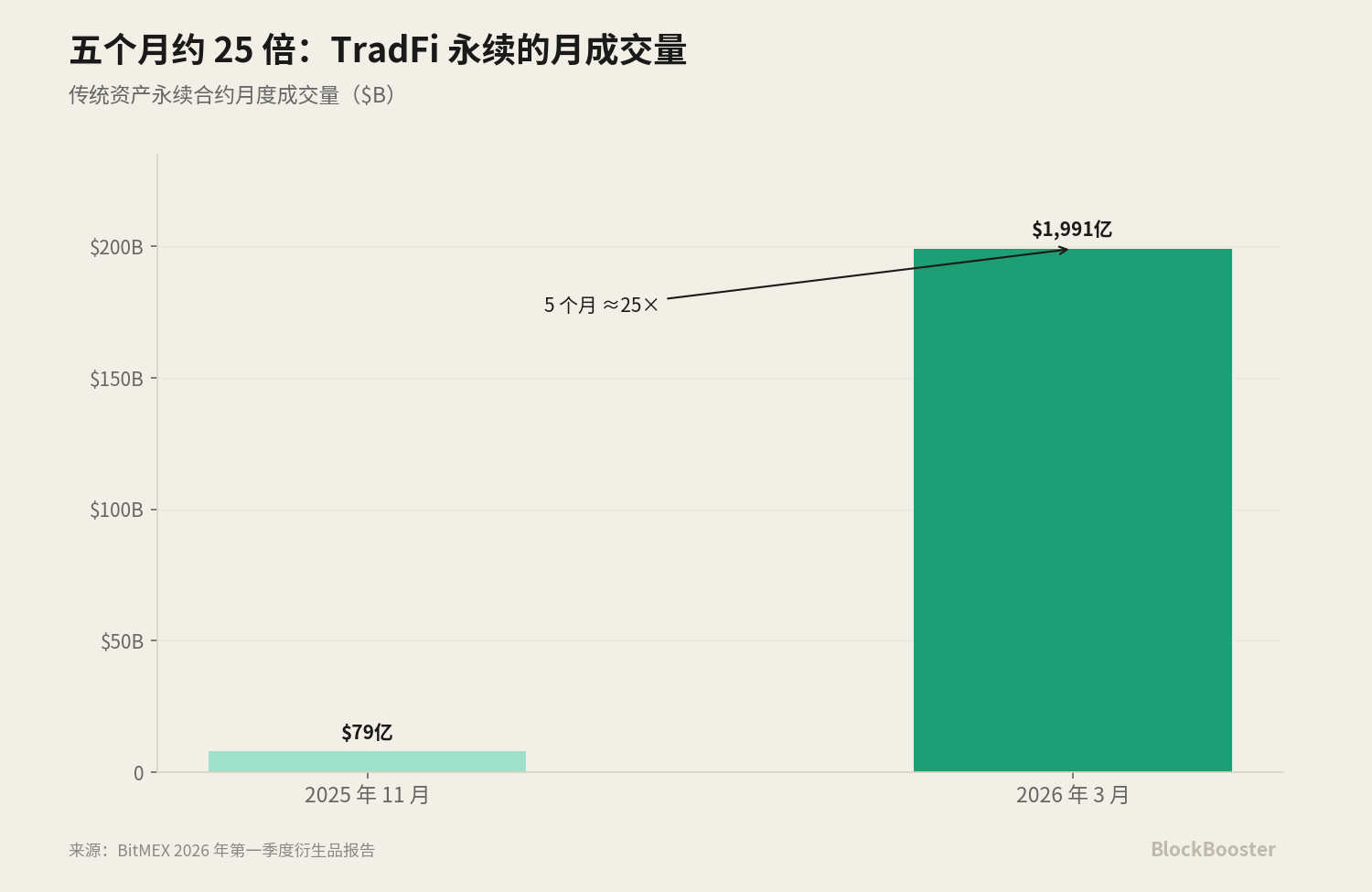

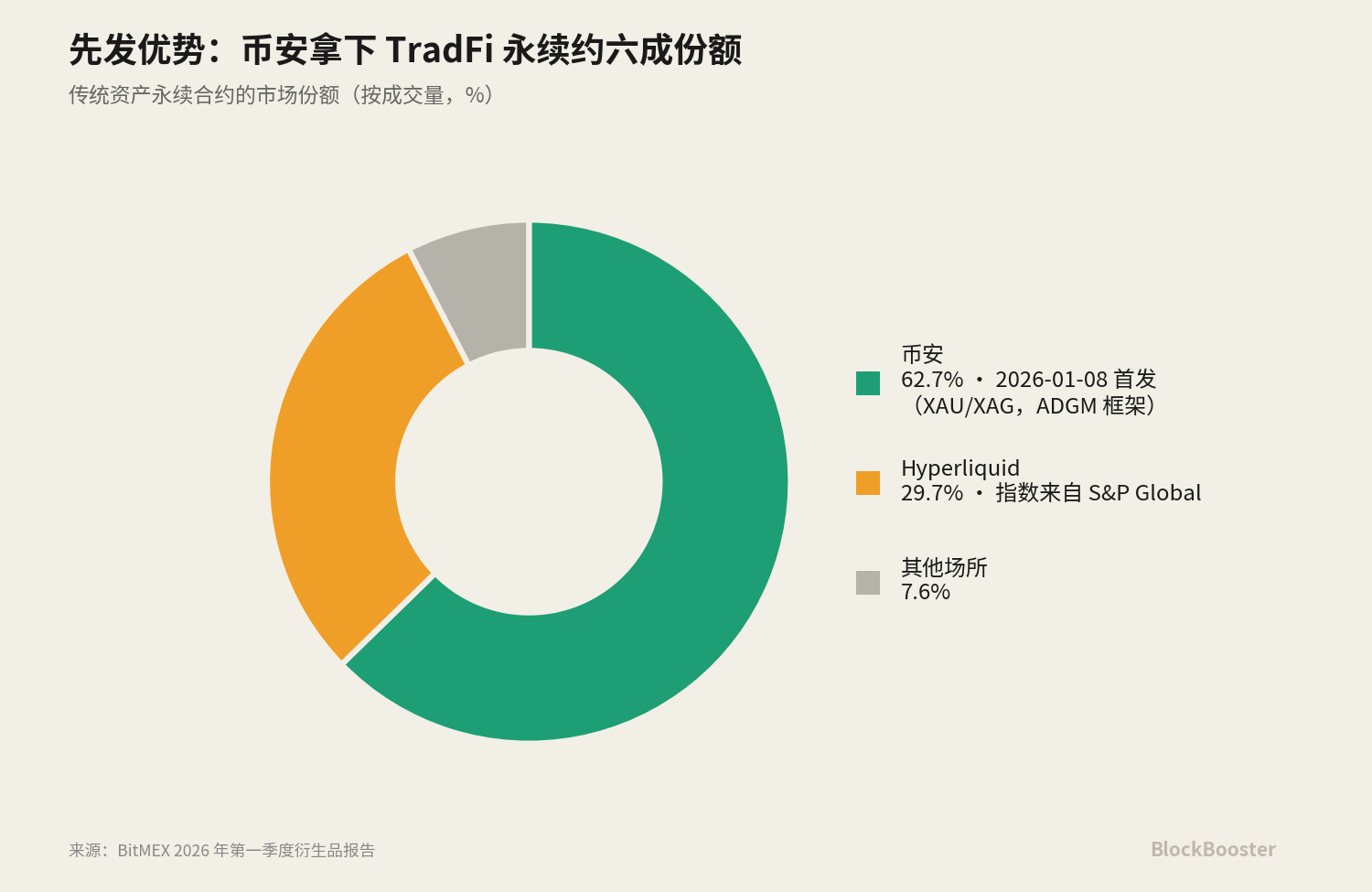

- 永续合约市场爆发式增长:BitMEX报告显示,“传统资产永续”赛道季度周成交量从5.26亿美元暴涨至307亿美元,增幅达5,756%。

- 合格基准需满足标准:基于真实交易、市场深广难以操纵、治理独立、具备期限结构,类似传统金融的SOFR(基于万亿级美债回购交易)。

- LIBOR因报价行操纵丑闻被废除,其替代品SOFR基于真实成交数据,由纽约联储管理,解决了利益冲突问题。

- Bitfinex的FRR(闪电回报率)基于真实期限融资交易,具备天然期限结构,但由单一交易所运营且与Tether同属母公司iFinex,存在集中度与利益冲突风险。

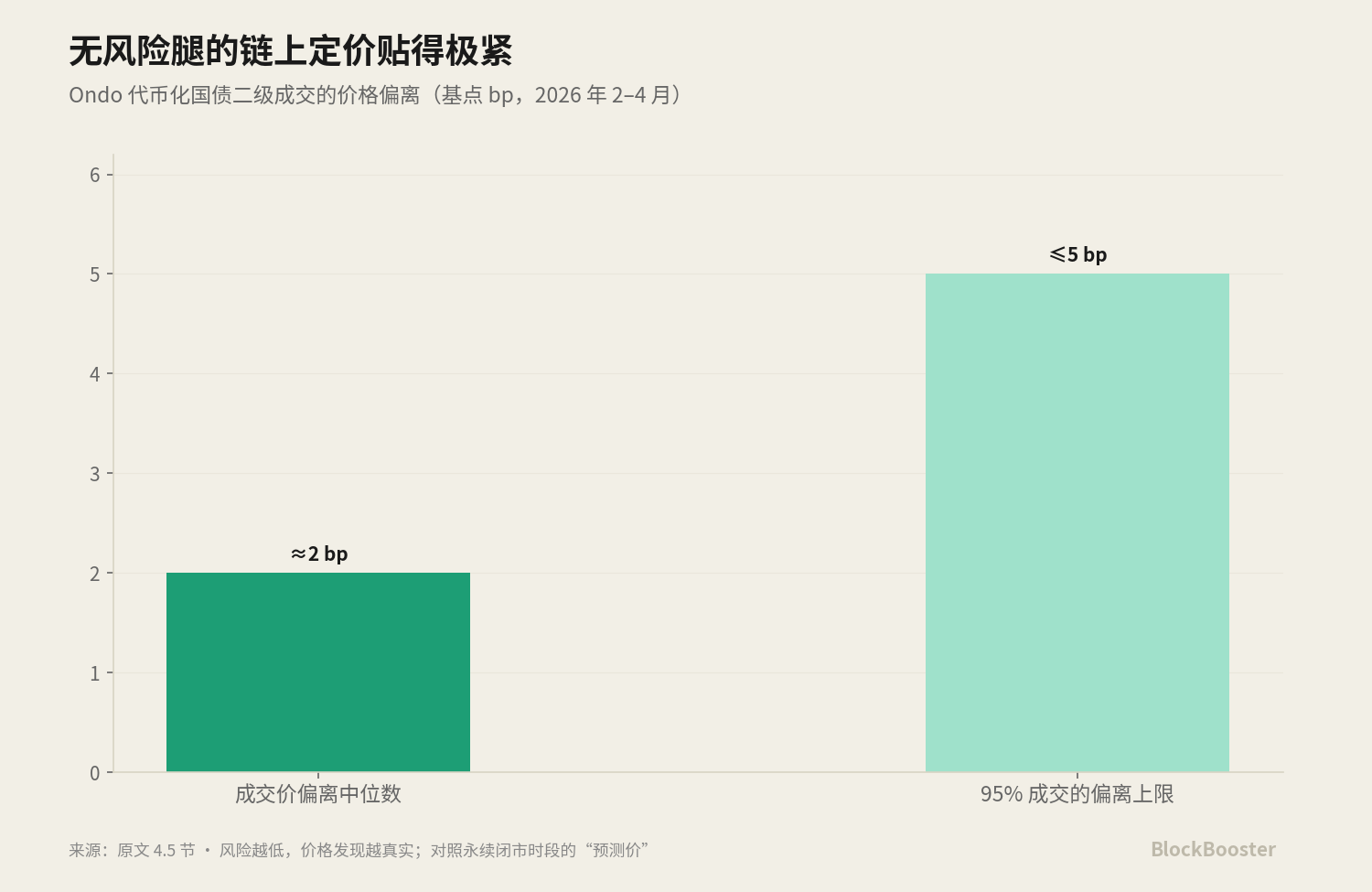

- 代币化国债收益(如BUIDL)紧贴美债收益率,是“加密无风险利率”候选,二级市场定价精准,偏差仅2-5个基点。

- 现有利率利差反映结构性风险:永续资金费率与国债收益的利差归因于杠杆波动率,Aave利率包含智能合约风险,Bitfinex FRR溢价体现交易所和稳定币对手方风险。

Original Author: @BlazingKevin_, Blockbooster Researcher

1. Crypto Has No "Benchmark Interest Rate"

Leverage and financing in the crypto world—trillions of dollars in leveraged positions, collateralized lending, yield products—operate without a unified benchmark yield curve.

According to BitMEX's Q1 2026 derivatives report, in the nascent sector of "traditional asset perpetuals" alone, the single-quarter weekly trading volume surged from approximately $525.8 million at the end of 2025 to $30.7 billion by mid-March 2026, a quarterly increase of roughly 5,756%; its monthly volume skyrocketed from $7.9 billion in November 2025 to $199.1 billion in March 2026, growing about 25 times in five months.

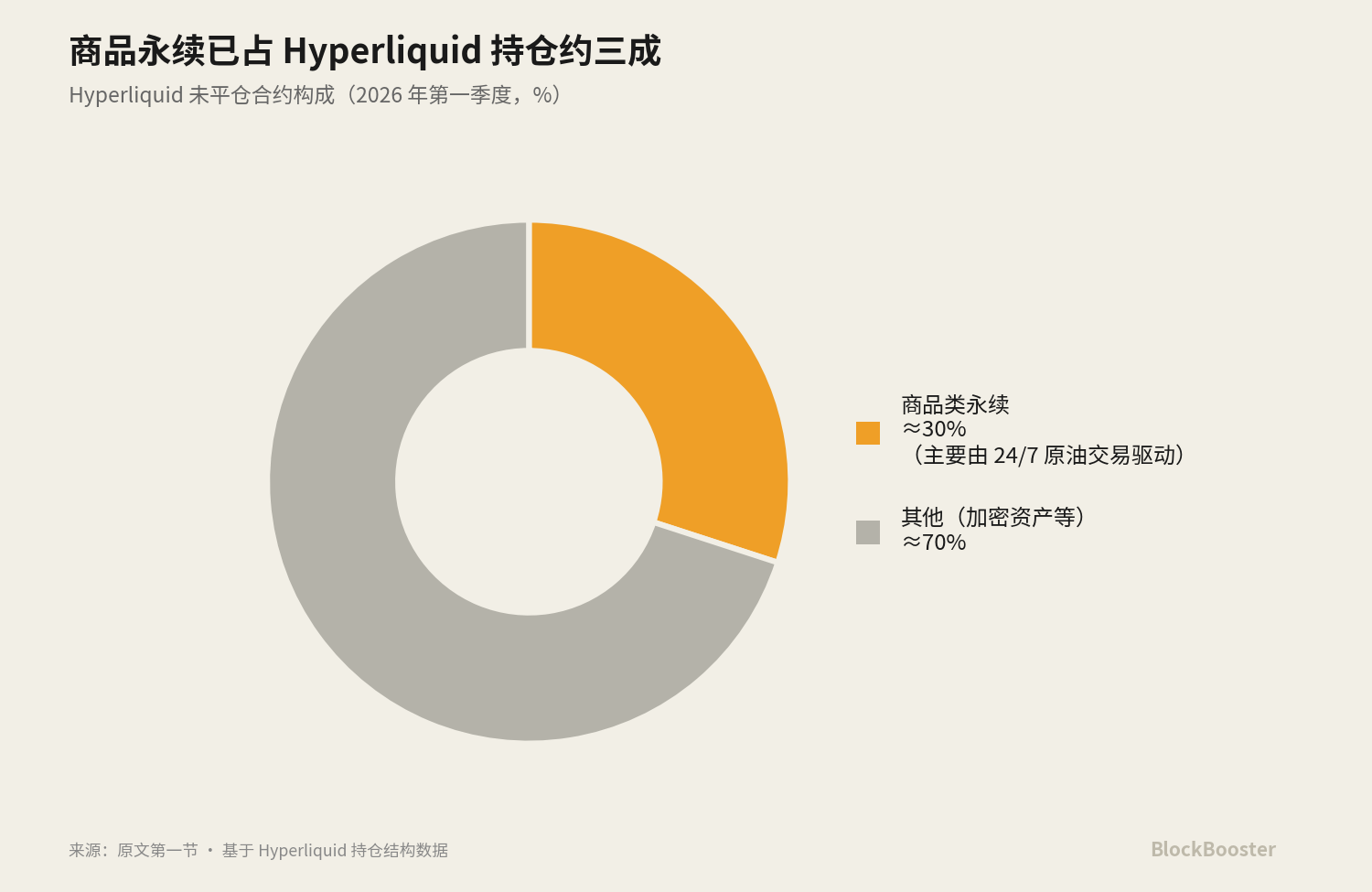

Based on DefiLlama's 30-day snapshot, Hyperliquid processed approximately $172.63 billion in perpetual trading volume, with open interest around $9.13 billion. In Q1 2026, commodity perpetuals accounted for about 30% of Hyperliquid's open interest, driven primarily by demand for 24/7 crude oil trading.

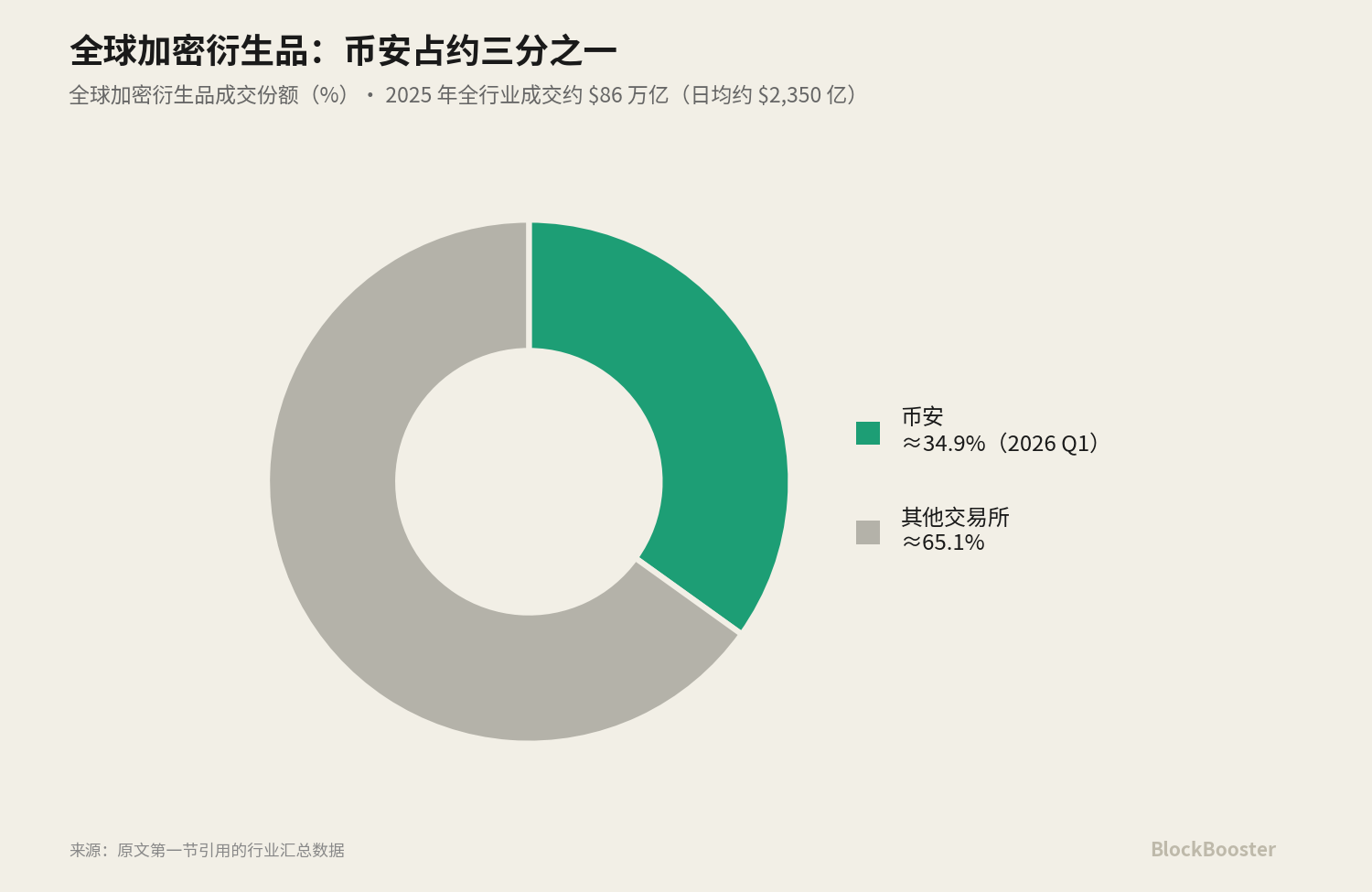

Regarding the "traditional asset perpetuals" track, Binance listed TradFi perpetual contracts on January 8, 2026, debuting with gold (XAUUSDT) and silver (XAGUSDT). Capitalizing on this first-mover advantage, Binance captured roughly 62.7% market share in TradFi perpetuals, with Hyperliquid following at 29.7%.

Hyperliquid's index data for these traditional asset perpetuals comes from a partnership with S&P Global, and this collaboration (linking crypto perpetuals directly to traditional indices) is drawing regulatory scrutiny from the US CFTC.

Meanwhile, the market cap of Ethena's USDe stood at approximately $4.5 billion to $5.9 billion in early June 2026.

These products each quote an "interest rate" or "yield"—perpetuals have funding rates, lending protocols have lending APRs, sUSDe has a staking yield, tokenized treasuries have coupons—but crypto still lacks its own SOFR. There is no widely accepted benchmark curve that can serve as an anchor for pricing. Each exchange and each protocol has become a micro financing market, quoting its own price, yet without a common, credible reference system among them.

2. What Qualifies as a Crypto "Benchmark Interest Rate"?

First, let's look at three different sets of interest rate comparisons:

- Set One: Benchmark Funding Rates vs. Product Yields vs. Derivatives Implied Rates. The APY of sUSDe is a product yield—the return to holders; the perpetual funding rate is a derivatives implied rate—the fee paid between longs and shorts to keep the perpetual price anchored to the spot price; a benchmark funding rate should be a public reference that countless other products can cite for pricing. Product yields and derivatives implied rates are not benchmarks—they are "downstream" of the benchmark, resulting from various premiums and structures layered on top of a baseline.

- Set Two: Overnight Rates vs. Term Rates. Perpetual funding rates settle every 1 or 8 hours, essentially an overnight rate—it only reflects the cost of capital from "now until the next settlement point," with no term structure. It cannot tell you the price difference between "borrowing for 30 days" and "borrowing for 90 days." Just as SOFR itself is an overnight rate, it relies on the futures market to construct a term structure, resulting in Term SOFR. An interest rate without a term structure cannot support any medium-to-long-term fixed-income market.

- Set Three: Real Lending Rates vs. Algorithmic/Implied Rates. Real bilateral lending transactions (e.g., Bitfinex's margin funding market, where real lenders and borrowers match) and algorithmic utilization pricing (e.g., Aave, where the interest rate is automatically calculated by a formula based on pool utilization) are two fundamentally different price generation mechanisms. The former is voted on by market participants with real money; the latter is a curve written into the code by protocol designers.

From these three distinctions, we can extract the criteria a "qualified benchmark" should meet:

Based on real transactions, underlying market is sufficiently broad and deep (difficult to manipulate by a single participant), governance independent (no conflict of interest between the administrator and the market being priced), and ideally possesses a term structure (to support medium-to-long-term pricing).

(SOFR's underlying is the real transaction volume of overnight repurchase agreements backed by U.S. Treasuries, with an average daily volume "often exceeding $1 trillion." This is the real transaction volume of overnight repos, entirely different from the notional volume of futures supporting Term SOFR.)

Applying SOFR's logic to crypto reveals structural isomorphism. The Bank for International Settlements, in its research, compares on-chain collateralized lending markets to "crypto-native money markets," whose operational mechanism is similar to traditional tri-party repo—over-collateralized, marked-to-market, and rolled overnight. Since on-chain lending is structurally a form of repo-style secured financing, evaluating crypto benchmarks using the design of SOFR (a benchmark built on real repo transactions) is a fitting isomorphic reference.

3. What Are the Characteristics of SOFR? Why Was LIBOR Discontinued?

LIBOR (London Interbank Offered Rate) was once the cornerstone of global finance. At its peak, approximately $300 trillion in financial contracts (including interest rate swaps, mortgages, student loans, corporate bonds, etc.) depended on LIBOR across five currency zones. However, LIBOR had a fatal design flaw: it was not based on real transactions but on daily "self-reported" borrowing cost estimates from a small panel of banks.

This flaw was fully exposed after the 2008 financial crisis. Regulatory investigations found that traders at several major global banks systematically manipulated LIBOR submissions to benefit their own derivative positions.

The manipulation scandal directly led to LIBOR's abolition.

Replacing it was SOFR (Secured Overnight Financing Rate). SOFR's design is almost a "reverse engineering" of every LIBOR flaw: it doesn't use self-reported estimates but is based on real transactions in the overnight repo market backed by U.S. Treasuries; it takes the volume-weighted median of transactions across three repo markets (tri-party repo, GCF Repo, and bilateral repo cleared through FICC's DVP service), offering a broad, deep, and hard-to-manipulate scope; it is administered by the New York Fed, adhering to IOSCO benchmark principles, ensuring no conflict of interest between the administrator and the priced market.

However, SOFR has an "inherent limitation": it's an overnight rate, lacking a term structure. The market needs not just "today's overnight cost" but also the "expected funding cost over the next three months" to price medium-to-long-term loans. Thus, CME launched CME Term SOFR—a set of forward-looking rates covering four tenors: 1-month, 3-month, 6-month, and 12-month.

It uses trading data from SOFR futures to infer the market's expectations for the future path of SOFR, thereby "constructing" a forward-looking term curve. (The representative notional volume of SOFR futures used to construct Term SOFR was approximately $2.3 trillion per day in Q4 2023.)

4. Some Candidate Interest Rates for Discussion

There are many candidates commonly considered as "interest rates" or "yields" in the market. Below, we dissect each one. During the meeting, we can discuss why some rates are clearly unsuitable as benchmarks and which ones have room to evolve.

A central theme running through all these dissections is "who has the power to decide": is it market weighting, algorithmic utilization, or governance setting?

4.1 Perpetual Funding Rate (Hyperliquid / Binance)

The perpetual funding rate is the implied price of leverage, driven by the basis between the spot and perpetual prices. It is essentially an overnight rate, lacking a term structure.

When the spot market for TradFi underlying assets is closed (e.g., stocks, precious metals over the weekend), exchanges cannot obtain a real spot price to calculate the funding rate. Binance's approach is to freeze the index price at the last spot price, switching to an EWMA mark price with a ±3% cap; Hyperliquid also switches to EWMA on weekends with volatility caps set per product. During closed market hours, the "anchor" for the perpetual price is actually a predicted value, not a real transaction price. When the market reopens and the real price gaps beyond this cap, it triggers limit-up/limit-down situations. Therefore, the price during closed market hours is a prediction, not a real anchor for arbitrage.

On May 29, 2026, the US CFTC approved KalshiEX's Bitcoin perpetual contract (BTCPERP)—the first truly perpetual regulated Bitcoin perpetual in the US. The CFTC simultaneously issued a policy statement on perpetual contracts, staff guidance on 24/7 trading and clearing, and a no-action position regarding Coinbase offering perpetuals through Deribit. The significance is that a regulated, centrally cleared perpetual means its funding rate and basis are generated in a compliant environment with clearing guarantees—this is a potential candidate for a future "crypto SOFR." This, combined with the aforementioned Hyperliquid-S&P Global index partnership under CFTC scrutiny, signals that "regulation is closing in on crypto benchmarks."

4.2 Bitfinex Margin Funding + FRR

This is crypto's native USD term funding market.

The mechanism works like this: Bitfinex operates a peer-to-peer margin funding market where lenders provide funds to margin traders to earn interest. The key design element is that loan terms range from 2 to 120 days (commonly 2, 7, or 30 days), and both the interest rate and term must be matched during order matching. This means Bitfinex's funding market naturally forms a real lending curve from the short to the long end: 30-day and 120-day money have different prices, determined by real supply and demand matching. It is one of the very few real lending markets in crypto that inherently possesses a term structure.

The FRR (Flash Return Rate) serves as the reference rate for this market: FRR is the average rate of all active fixed-rate funding offers, weighted by their size, updated hourly. Essentially, it is the "Bitfinex version of a benchmark reference rate"—an index reflecting the current average lending cost in the market. Lenders can choose to lend at FRR, allowing their rate to automatically track the market.

Bitfinex charges approximately 15% on lending earnings (18% for hidden orders), with a minimum order amount of $150. FRR is quoted as a daily rate, annualized from that daily rate: Bitfinex USD FRR is approximately 0.0136%/day, annualized to about 5.1%—in line with other candidates like tokenized treasuries, Aave, and SSR.

The critical issue is its volatility: USD lending rates historically fluctuate sharply within a range of roughly 3%–20% APR, highly correlated with leverage demand.

This daily rate curve unfolds across different tenors from 2 to 120 days, forming a native USD funding curve with a real term structure in crypto.

Bitfinex and Tether share the same parent company, iFinex, with overlapping management. This gives Bitfinex the most abundant USDT liquidity in the crypto world—a reason its funding market is so deep; however, it also concentrates counterparty risk and stablecoin issuer risk within the same complex. Borrowing from Bitfinex, using Bitfinex's matching, denominated in Tether, with the same parent company potentially backstopping in extreme scenarios—this is a highly self-contained structure.

Although Bitfinex's funding market is crypto's oldest and deepest native USD term funding market, its absolute size (the stock of funding offers and daily matching volume) is still significantly smaller compared to the trillions of dollars in trading volume seen in the aforementioned perpetuals market.

Comparing FRR to LIBOR and SOFR on the "based on real transactions" dimension, FRR is actually cleaner than LIBOR. FRR is calculated based on real, executed fixed-rate funding offers, weighted by size, reflecting real market behavior. However, FRR originates from a single exchange's order book (concentration), is operated by the same parent company iFinex that controls the largest stablecoin Tether (conflict of interest), and this operator also acts as the lender of last resort for positions in its own market (further concentration and conflict). Therefore, on the dimensions of concentration and conflict of interest, FRR hits the very issues that SOFR was designed to eradicate.

4.3 DeFi Lending Rates (Aave / Morpho)

This is the epitome of algorithmic utilization pricing: the interest rate is not determined by bilateral matching but is automatically calculated by a formula based on the pool's utilization rate—the higher the utilization, the higher the rate. It fluctuates in real-time with borrowing demand.

The USDC deposit rate on Aave's mainnet fluctuates between approximately 3.5%–6% depending on utilization; on Morpho, USDC vaults managed by curators yield approximately 5%–7% after curator fees.

4.4 MakerDAO / Sky Savings Rate (DAI's DSR / USDS's SSR)

This is a "quasi-policy rate" directly set by protocol governance. DAI's DSR (Dai Savings Rate) and USDS's SSR (Sky Savings Rate) are widely referenced, functionally similar to a policy rate set by a central bank—it is not determined by market matching or algorithmic utilization but by Sky's governance vote.

The governance-set DSR/SSR, market-weighted FRR, and algorithmic utilization of Aave represent three distinctly different interest rate generation mechanisms.

Governance setting vs. market weighting vs. algorithmic utilization—each mechanism has its own credibility issues and manipulation risks. A mature market's benchmark should ideally come from the least manipulable of these (market-weighted real transactions, with sufficient breadth and depth). In terms of current values, SSR was lowered by governance from 4.75% at the end of April 2026 to approximately 3.6%–3.75% by early June (the "governance-set" mechanism moving in tandem with the Fed's path); the circulating supply of USDS is approximately $11 billion.

4.5 Tokenized Treasury Yields (BUIDL / BENJI, etc.)

This is the ~4–5% "risk-free leg," a candidate eligible to be a "crypto risk-free benchmark." BlackRock's BUIDL, Franklin Templeton's BENJI, etc., bring the coupon yield of US Treasuries onto the chain. In terms of current values, major tokenized treasury tokens (BUIDL, USDY, USDM, USYC, etc.) were paying approximately 4.1%–4.7% APY in April 2026, closely tracking the 3-month US Treasury yield. Their yield can almost directly benchmark against the traditional risk-free rate.

The secondary market pricing for this "risk-free leg" of tokenized treasuries is extremely tight: taking Ondo's tokenized treasury as an example, between February and April 2026, the median deviation of its traded price was only about 2 basis points, with 95% of trades falling within 5 basis points. This indicates that when the underlying asset is sufficiently standard and risk-free, price discovery on-chain can be very precise; in contrast, the "price" of high-risk products like perpetuals during closed market hours is highly speculative—the lower the risk, the more real the price; the higher the risk, the more the pricing resembles guesswork.

4.6 Ethena sUSDe

This is a securitized product combining perpetual funding rates and collateral yield. Its APY is highly dependent on the funding rate levels of the perpetual market, making it essentially a repackaging of implied rates, not a benchmark itself.

Lining up these seven candidates: each measures something different (leverage sentiment,