UNI at $100 in Four Years: Will Standard Chartered’s Prediction Come True?

- Core Argument: Standard Chartered predicts a target price of $100 for the UNI token by 2030, with its core logic being that tokenized assets will drive demand for open DeFi liquidity. Uniswap is poised to handle a significant volume of transactions and earn fees. However, this prediction heavily depends on whether tokenized assets can truly break through institutional access barriers and achieve free circulation.

- Key Elements:

- Standard Chartered forecasts that the DeFi market will host over $2 trillion in tokenized assets by 2030, increasing from its current share of approximately 3.5% to 30%, providing a growth foundation for Uniswap.

- Although BlackRock’s BUIDL fund is integrated with Uniswap’s technology, it is only open to 108 qualified holders, demonstrating that strict access controls still exist for tokenized assets.

- As a liquidity infrastructure, Uniswap currently holds a total value locked of approximately $2.89 billion across multiple chains and generated over $50 million in fee revenue in the last 30 days, providing the scale to accommodate demand.

- The UNI token lacks a stable value capture mechanism. The distribution and burning of protocol fees depend on community governance and do not guarantee that holders will directly benefit from increased transaction volume.

- The Financial Stability Board points out issues in the tokenization industry such as closed access, insufficient interoperability, and fragmentation of trading platforms, which hinder assets from becoming universal liquidity instruments in DeFi.

Original Author: Liam Akiba Wright

Original Translation: Luffy, Foresight News

TL;DR:

- Standard Chartered reportedly published a Uniswap research report, setting a target price of $100 for the UNI token by 2030.

- The bank's core logic is that tokenized assets will generate demand for open DeFi liquidity, with Uniswap expected to capture significant trading volume and earn fees.

- However, most institutional-grade tokenization products adopt permissioned systems, and BlackRock's BUIDL product demonstrates that barriers to entry still exist in the DeFi space.

Standard Chartered's year-end 2030 target price of $100 for the UNI token suggests a value far exceeding current market levels for this governance token of the leading decentralized exchange.

The bank's thesis posits that future tokenized assets will require decentralized trading platforms to transform fragmented on-chain financial instruments into tradable liquidity.

Standard Chartered estimates that the global market for tokenized assets could reach $4 trillion by 2028, with the proportion of these assets flowing into DeFi markets rising from approximately 3.5% currently to 30% by 2030. Based on this projection, the asset volume hosted by the DeFi market could surpass $2 trillion by 2030.

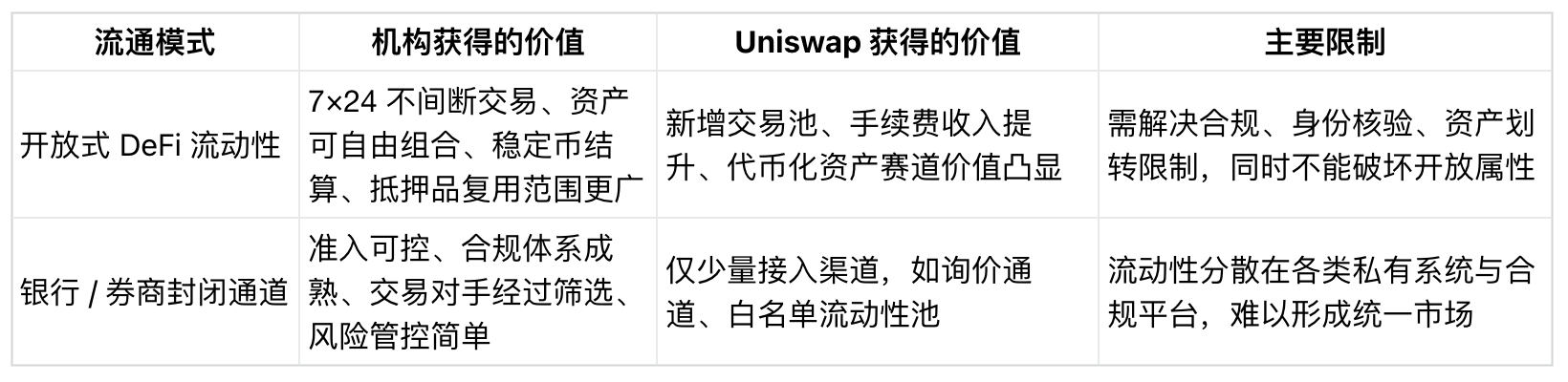

Banks, asset managers, transfer agents, and compliance platforms are all currently building in the asset tokenization space. However, if these assets require 24/7 trading, flexible collateralization, and the ability to combine across products—capabilities that individual proprietary systems may not fully provide—open decentralized protocols stand to capture the resulting liquidity benefits.

Against this backdrop, a core industry question emerges: Will on-chain assets like tokenized Treasuries, funds, stocks, and stablecoins become liquid instruments in open decentralized markets, or will they remain confined within closed systems featuring strict access controls and fully managed settlement and transfer processes?

Growth Prospects Depend on Open Liquidity

Standard Chartered's valuation target rests upon a series of assumptions: first, significant expansion of the tokenized asset market; second, a substantial portion of these assets moving beyond being mere compliant, on-chain wrappers for ownership registration to actively circulating within DeFi markets; and third, Uniswap capturing enough of the related trading volume to drive value for the UNI token. The core logic shifts the focus from asset issuance to liquidity trading.

Standard Chartered has previously identified asset tokenization as a major long-term opportunity. In 2024, a joint report with consulting firm Synpulse predicted the global Real World Asset (RWA) tokenization market could reach $30.1 trillion by 2034, with trade finance being a key application. The report also noted that tokenization would spawn new DeFi applications and business models.

A tokenization report from Citi (published June 2026) offered a similar view on market size but also highlighted potential headwinds: its baseline scenario projected $5.5 trillion in tokenized assets by 2030, with an optimistic scenario of $8.2 trillion. The report also suggested that a hybrid model might dominate, with institutions controlling the issuance, distribution, and settlement channels.

This divergence in potential paths directly determines Uniswap's growth potential. If the scale of tokenized assets continues to grow but value remains locked within bank platforms, transfer agent systems, brokerage networks, and compliant trading markets, the potential for open DeFi will be limited.

Conversely, if various tokenized financial instruments, stablecoins, and collateral assets require free cross-category trading, protocols like Uniswap will see their industry standing significantly enhanced.

Data from DeFiLlama confirms Uniswap's foundational capability to meet such demand. As of writing, the protocol's total value locked across multiple chains stands at approximately $2.89 billion, with fee revenues exceeding $50 million over the last 30 days.

While these figures only represent baseline operational scale, they illustrate Uniswap's role as liquidity infrastructure.

For institutions, there's a clear practical distinction. Issuing a tokenized fund is one process; building a venue where that token can freely trade against stablecoins, collateral, and other tokenized assets is a separate business undertaking.

The gap between these two determines whether automated market maker Uniswap becomes essential infrastructure or remains a peripheral supporting channel.

Thus, the choice of trading channel is as crucial as asset issuance. Liquidity determines whether tokenized products can form a tradable market, reusable collateral, and settleable assets; otherwise, they degenerate into static ownership certificates within compliant systems.

BlackRock BUIDL: Connected to DeFi, but with Access Gates

BlackRock's BUIDL Institutional Digital Liquidity Fund serves as a real-world case study of this inherent tension. In February, Uniswap Labs and compliance platform Securitize announced that the BlackRock USD Institutional Digital Liquidity Fund (BUIDL) was accessible via the UniswapX trading channel.

This integration utilizes a request-for-quote (RFQ) mechanism and is accessible only to whitelisted, pre-vetted eligible participants.

Previous CryptoSlate reporting on BUIDL highlighted the core contradiction: while BUIDL holders could use UniswapX to swap for USDC, trading permissions were subject to strict access thresholds.

The trading process leverages DeFi technology, yet asset circulation is limited exclusively to approved institutional participants.

BlackRock's initial BUIDL offering rules fully reflect this controlled model: the product was available only to qualified investors, required a minimum investment of $5 million, allowed transfers only to pre-approved parties, and was not listed for trading on any exchange.

RWA.xyz data shows that on June 16, BUIDL held approximately $2.37 billion in total assets managed by just 108 holders.

Considering the access rules, the current state of the tokenization industry becomes clear. Large-scale on-chain tokenized products can be created, but participation is highly concentrated and subject to full access control throughout.

Standard Chartered's own May 2026 investor presentation also used the BUIDL-Unipswap integration as a case study to argue that decentralized platforms can be used for asset distribution and trading.

Even though the full UNI valuation report has not been publicly released, this presentation clearly positions Uniswap as supporting infrastructure for institutional digital assets—a key underpinning for the $100 price target.

The BlackRock BUIDL model sits between the two extremes, utilizing Uniswap technology while retaining institutional access controls. This design creates a bridge to DeFi infrastructure without fully releasing tokenized assets into permissionless, open liquidity pools.

The liquidity solutions accepted by institutional assets are likely to initially adopt this compromise model: leveraging DeFi infrastructure for trading and settlement while enforcing stringent restrictions on user identity, asset transfers, and counterparties.

UNI Still Lacks a Value Capture Mechanism

Even if Uniswap facilitates more trading of real-world tokenized assets, UNI holders may not directly benefit, as the protocol still lacks a robust value capture mechanism.

A previously passed UNI tokenomics upgrade proposal on the Tally platform outlined plans for protocol fee distribution, UNI token burning, and positioning Uniswap as the default trading hub for tokenized assets.

This framework provides a path to realizing the valuation logic, but it is contingent on multiple factors: community governance decisions, fee parameter adjustments, institutional commercial partnerships, and genuine growth in trading volume.

Standard Chartered's $100 target price not only far exceeds current market prices but also surpasses UNI's all-time high from 2021. Achieving this target requires more than just asset issuance growth; it demands genuine, sustainable transaction flow, stable fee revenue, and a clear mechanism linking protocol development with token value.

The core tension in the institutional tokenization space is that while banks and asset managers require decentralized capabilities like on-chain settlement, 24/7 transfers, programmable collateral, and stablecoin payments, they simultaneously insist on KYC identity verification, asset transfer restrictions, designated counterparties, and control over secondary market distribution.

The Financial Stability Board's research report on tokenization reinforces this cautious approach. The report notes that the overall scale of tokenization remains small and identifies multiple issues including closed access, insufficient cross-platform interoperability, restricted settlement assets, and fragmented trading venues.

These frictions are the primary obstacles preventing tokenized assets from becoming universal, liquid instruments within DeFi.

If these industry barriers persist, Uniswap will remain a peripheral integration channel on the edge of institutional tokenization. If these pain points are progressively resolved, the protocol could become the core trading venue intersecting tokenized funds, stablecoins, and native crypto assets.

Ultimately, the validity of Standard Chartered's valuation forecast depends on where tokenized liquidity eventually flows. The $100 target represents significant upside potential, but the more critical signal is that a traditional Wall Street bank is acknowledging that a DeFi protocol has the potential to participate in the institutional tokenization wave.

The BlackRock BUIDL case has already demonstrated that asset managers can use DeFi technology while maintaining strict circulation controls. Citi's outlook for the tokenization industry also suggests Wall Street is likely to build hybrid systems, keeping issuance, distribution, and settlement firmly within institutional hands. The various industry pain points highlighted by the Financial Stability Board underscore that interoperability and settlement infrastructure remain core industry challenges.

Future market signals will come from more tokenized asset integration cases. If new assets exclusively use isolated, whitelisted RFQ channels, open DeFi will only capture a small fraction of the market. If cross-asset unified liquidity pools gradually emerge, and custom access controls decrease, Uniswap's position in the tokenization landscape will extend far beyond native cryptocurrency exchange.