16 billion market cap is just the beginning: The real dividend of tokenized stocks lies in on-chain infrastructure

- Core Thesis: The tokenized stock sector has growth potential, but current issuance is primarily through custodial wrapper models, making early investment opportunities difficult for retail investors to access. The true value lies in betting on the widespread adoption of native on-chain asset tokenization, not in directly trading tokenized stocks.

- Key Factors:

- Tokenized stocks carry multiple risks, including issuer custodial risk, insufficient liquidity, and smart contract risk. For example, the SPCX token on the xStocks platform dropped 40% due to lock-up issues.

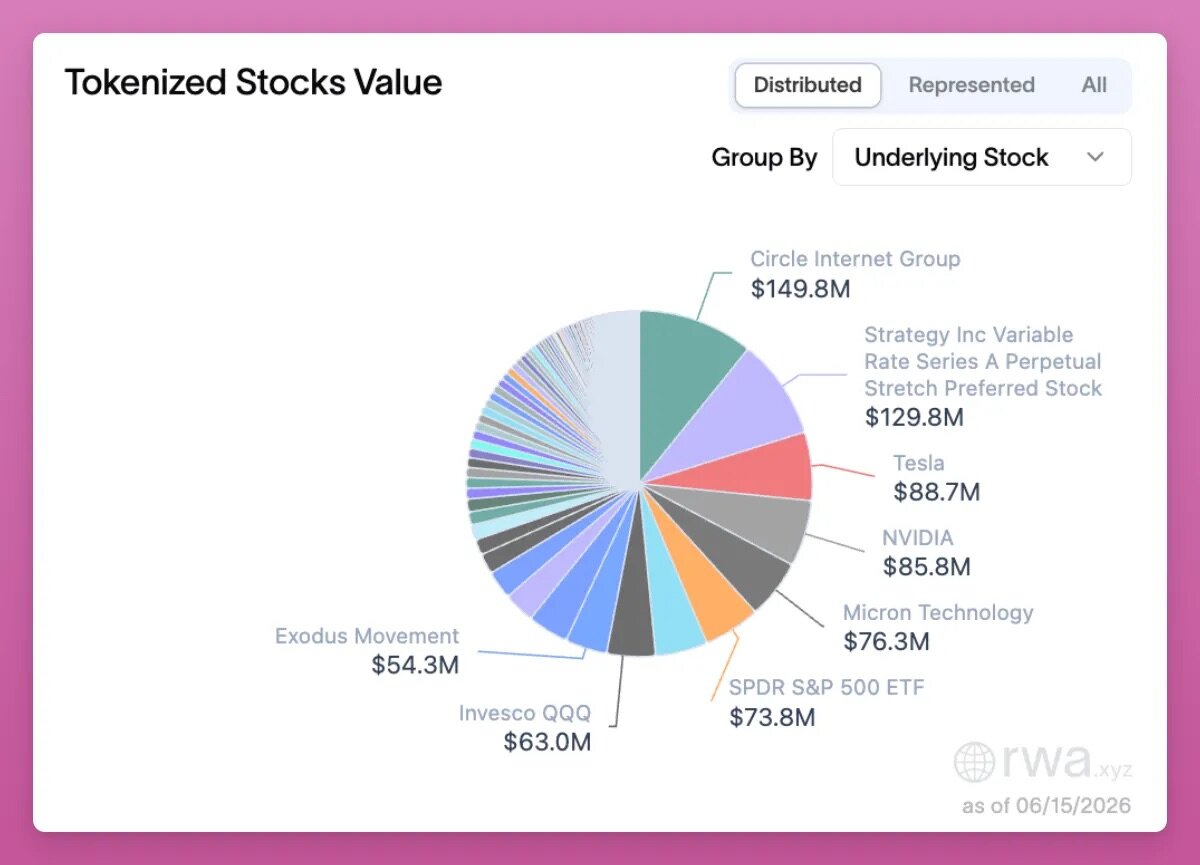

- The sector is extremely small, with a total circulating value of only $1.5 billion (lower than Uniswap's $1.9 billion). Most underlying assets are stocks of mature companies (e.g., Strategy stock valued at $129 million), not early-stage investment opportunities.

- Standard Chartered predicts that the value of on-chain tokenized assets will surpass $4 trillion by 2028. The growth of tokenized equities will drive revenue for platforms like Uniswap and give the crypto industry counter-cyclical characteristics.

- Backpack, through Superstate's Opening Bell, enables native on-chain equity issuance. Holders are entitled to dividends and voting rights, and its token BP can be exchanged for physical equity. BP has recently surged by 200%.

- Market leader xStocks holds a 60% share. Following its acquisition by Kraken, it launched a points program (xPoints), but the prospects for a token launch remain uncertain. Ondo's ONDO token serves only governance functions and faces nearly 50% token dilution.

- Trading opportunities include conducting delta-neutral hedging or participating in points farming on platforms like Backpack and Variational. However, caution is needed regarding the risk of platform shutdowns, such as with Ventuals.

Original Author: Ignas | DeFi Research

Original Translation: Saoirse, Foresight News

I believe there's only one way to make a fortune from tokenized stocks.

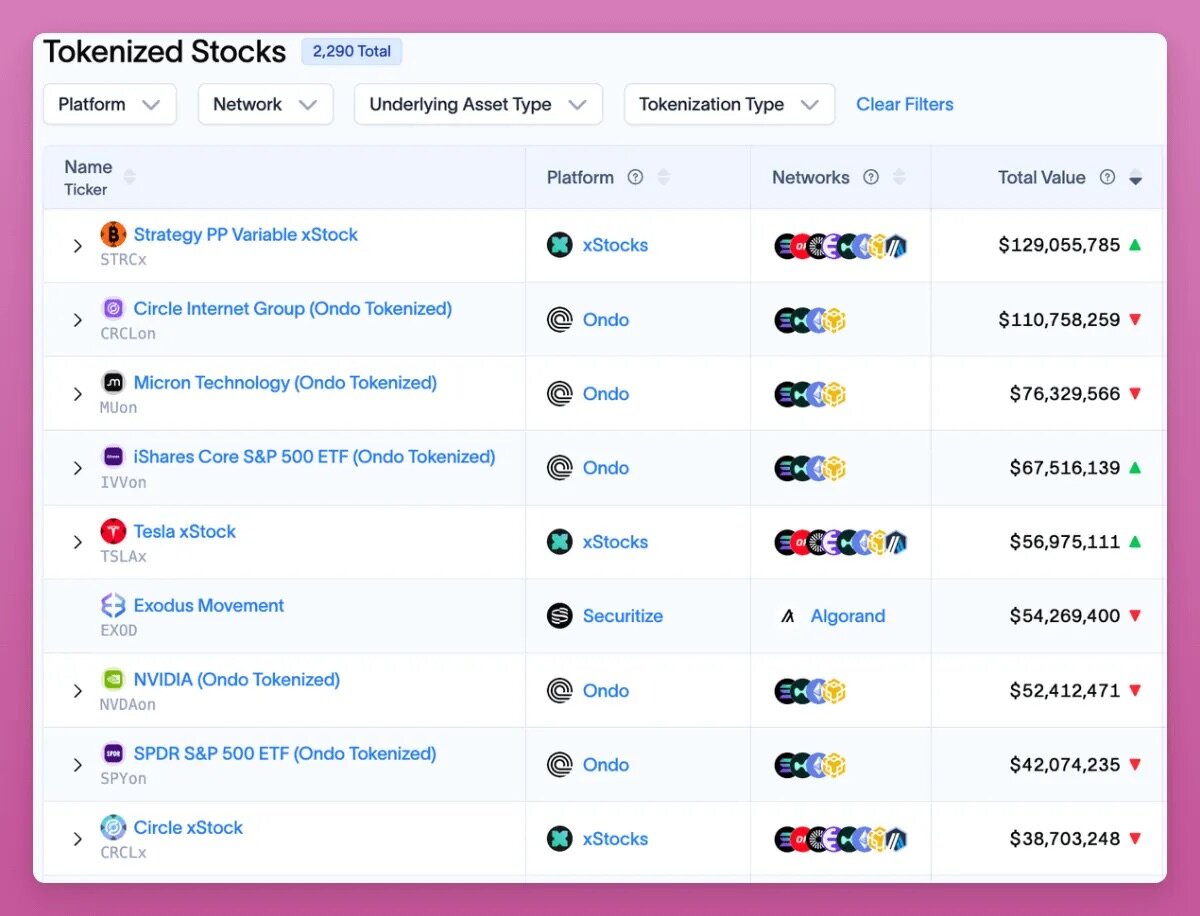

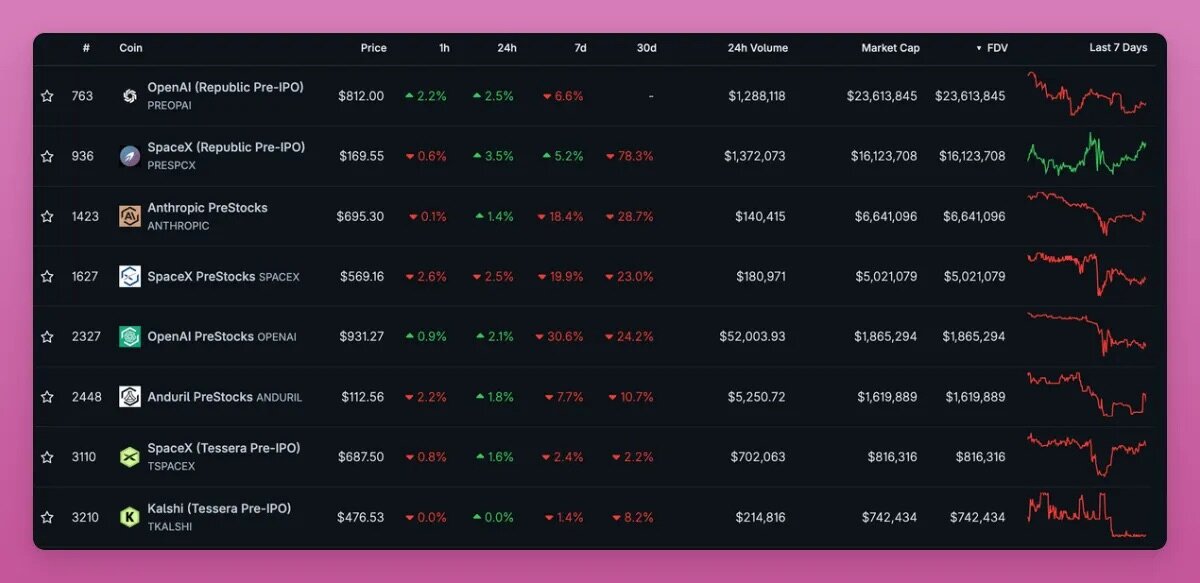

Of course, you can buy these tokens hoping for a tenfold surge, but aside from rare exceptions like Micron Technology (MU), the likelihood of such a windfall is minuscule. First, only about 2,290 stocks have been tokenized, with roughly 130 having a market cap exceeding $1 million. The vast majority of tokenized stocks have almost no liquidity on-chain.

According to RWA data site rwa.xyz, Strategy is one of the largest among these, with a total value of $129 million.

Most tokenized stocks today are from established, publicly listed companies. If you want to find undervalued, low-attention individual stocks, traditional brokers like Interactive Brokers actually offer more opportunities.

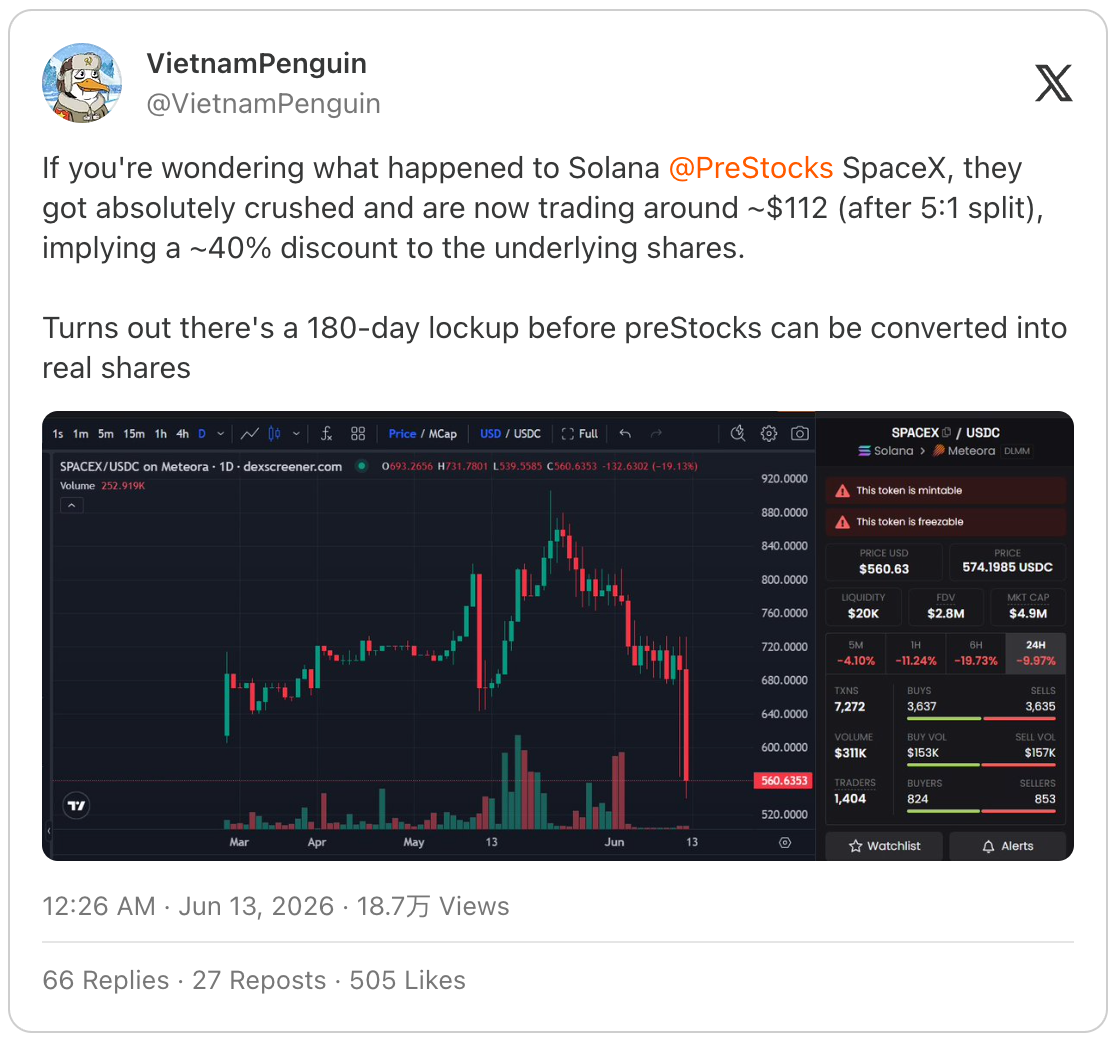

Secondly, holding tokenized stocks comes with many risks that don't exist with traditional brokerage holdings. For example, investors who bought SpaceX tokenized stock (SPCX) on the PreStocks platform found that these tokens had to be locked for 180 days before they could be exchanged for actual shares, a revelation that caused the token price to plummet by 40%.

Source: https://x.com/VietnamPenguin/status/2065470925252759680

Therefore, in addition to the inherent crypto industry risks of smart contract risk, self-custody asset risk (without enjoying the benefits of self-custody), and liquidity risk, investors must also bear the risks brought by the issuer and the asset custodian.

However, I'm not completely dismissing the tokenized stock track. It's one of the most promising sectors in crypto for growth: it can attract new users and retain existing users who might otherwise cash out their crypto to invest in traditional financial markets. Tokenized stocks bring on-chain transactions and fee revenue to the blockchain, and can attract venture capital, developers, and market attention to the industry.

Tokenized stocks themselves offer several opportunities: you can deposit them into decentralized exchange (DEX) liquidity pools to earn yields or use them as collateral for loans; you can also hold SPCX spot on-chain while shorting corresponding perpetual contracts to earn delta-neutral yields, along with collecting DEX platform points.

Speaking of hedging strategies, you can buy tokenized stock spot and short it on the Variational platform. The platform's native token, VAR, is arguably the best airdrop opportunity right now:

- 50% of the total token supply will be allocated to the community;

- The points activity ends on September 30th, leaving only about 3.5 months of the mining window;

- After the token launch, the team plans to use 30% of platform revenue for buybacks and burns;

- The platform is still in a closed beta testing phase.

Tokenized Stocks Are Not an Early-Stage Investment Track

But my biggest concern with tokenized stocks is this: this sector essentially makes crypto investors the exit liquidity for traditional financial assets.

In the past, the crypto industry produced many millionaires because we invested early in new tracks: Bitcoin, smart contract L1s, various project airdrops, NFTs, the Hyperliquid airdrop, and countless others. The tokenized listing process for SpaceX made this issue clear to me.

Its launch model is identical to the launch of a hyped-up Layer 2 token: a small circulating supply, a sky-high fully diluted valuation, and a price movement completely decoupled from the underlying business fundamentals. In the short term, traditional financial markets are currently in a phase where "high FDV is just hype," exactly like the crypto industry two years ago.

Undeniably, the prospects of rockets, artificial intelligence, and Starlink sound promising, but the company's valuation, equity unlock schedule, revenue data, and governance mechanisms are hardly optimistic.

The core value of tokenization lies in broadening asset distribution channels: any user with a Phantom, Metamask, or Rabby wallet can hold these tokens. Their volatility is lower than Bitcoin or altcoins, but they are not pegged to the dollar like stablecoins, offering a risk-return profile somewhere in between. For investors outside developed markets, or for users who don't want to or can't convert their crypto assets into traditional financial systems, tokenized stocks offer an attractive solution.

But this doesn't mean we've seized an early investment opportunity. The former allure of crypto was giving ordinary retail investors a chance to invest in revolutionary companies at their startup phase. An IPO project valued at a $2 trillion level can hardly be called an early-stage investment.

The future of the crypto industry with truly long-term growth potential is for companies to issue equity via on-chain tokenization from their inception. ICOs and fair launches were good attempts, but in the last bull cycle, the industry became increasingly extractive towards retail investors: private placement valuations were inflated, TGEs drove prices even higher, and the allocation of tokens to the general public was pitifully small. Cobie dissected this point very thoroughly in his blog post.

I am still investing through Cobie's Echo platform because it genuinely offers opportunities in early-stage projects: my investment in the MegaETH round has already increased 3.85 times, even though the market has been sluggish since the token launch.

Apptronic is a humanoid robot company. Despite its high valuation, I also participated in its Series B strategic financing. Traditional financial platforms do not offer such investment opportunities to ordinary retail investors.

By the way, besides Echo, I also think highly of the Legion platform, but it still needs to find high-quality investment targets with reasonable valuations, which is not an easy task.

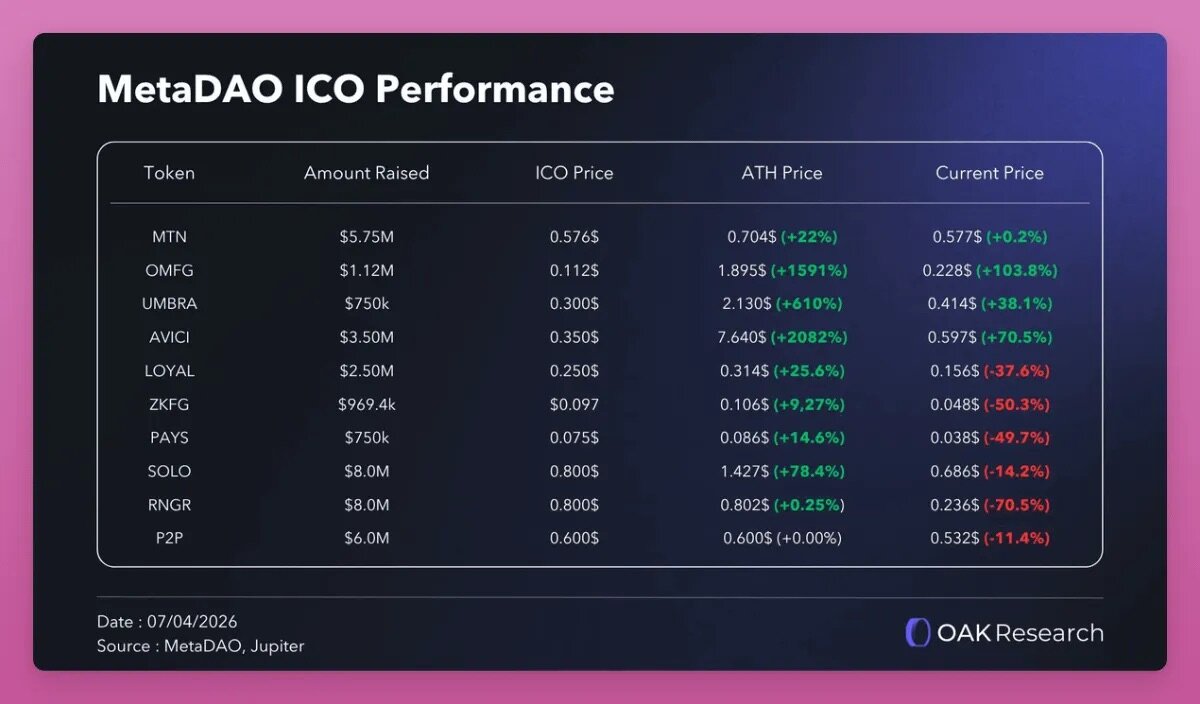

MetaDAO's model is excellent: the ownership tokens issued by the platform grant holders legal equity, use caps to monitor treasury spending, and unlock tokens based on company performance, perfectly solving the core problems exposed by the ICOs of yesteryear. For this reason, considering the current market environment, the various ICO projects launched on MetaDAO are performing relatively better overall.

Source: X Platform OAK Research

Beyond this, there is also the native on-chain issuance model, such as Superstate's Opening Bell product line. Its first target is Galaxy stock, where company equity is issued compliantly directly on-chain.

Imagine if large companies bypassed the traditional IPO process and instead issued equity directly on public chains like Ethereum or Solana, rather than just wrapping off-chain legal equity certificates with blockchain technology. At that point, blockchain's immutability and security would become core industry competitive advantages, and the value of the tokens we hold would increase accordingly.

MetaLeX is implementing this exact solution: creating fully programmable on-chain companies where corporate capital, equity, and vesting schedules are all managed on-chain.

Back to the point, major centralized exchanges like Binance, Coinbase, and Kraken are heavily moving into traditional finance by listing tokenized stocks, bonds, and ETFs. However, the xStocks platform couldn't deliver the underlying physical stocks, leading Binance, Bybit, and Bitget to all delist the SpaceX tokenized stock product, leaving over $1 billion in user orders unfulfilled. In contrast, trading orders on traditional brokers are much safer.

Stablecoins were initially only used for short-term asset storage while waiting to enter native crypto assets; now stablecoins have become the liquidity exit for absorbing funds from middle-aged and elderly investors in traditional finance.

Some might argue that pre-IPO tokenized stocks allow ordinary people to get in early on top-tier celebrities like OpenAI and Anthropic. Granted, by market cap, these two are the hottest primary market tokenized targets, but both companies are valued at nearly a trillion dollars.

This is hardly an early investment: Anthropic's latest Series H strategic financing round already valued it at $965 billion. Financing rounds: Series A, B, C, D, E, F, G, H (latest).

The Tokenized Equity Track is Still in Its Very Early Stages

Standard Chartered Bank has set a target price of $100 for the Uniswap token UNI, representing a potential 40x increase! The logic is as follows: The bank predicts that by 2030, the scale of tokenized assets circulating within decentralized finance will grow 37 times (currently only 3.5% of total assets, rising to 30% by 2030); by 2028, the total market cap of on-chain tokenized assets will exceed $4 trillion.

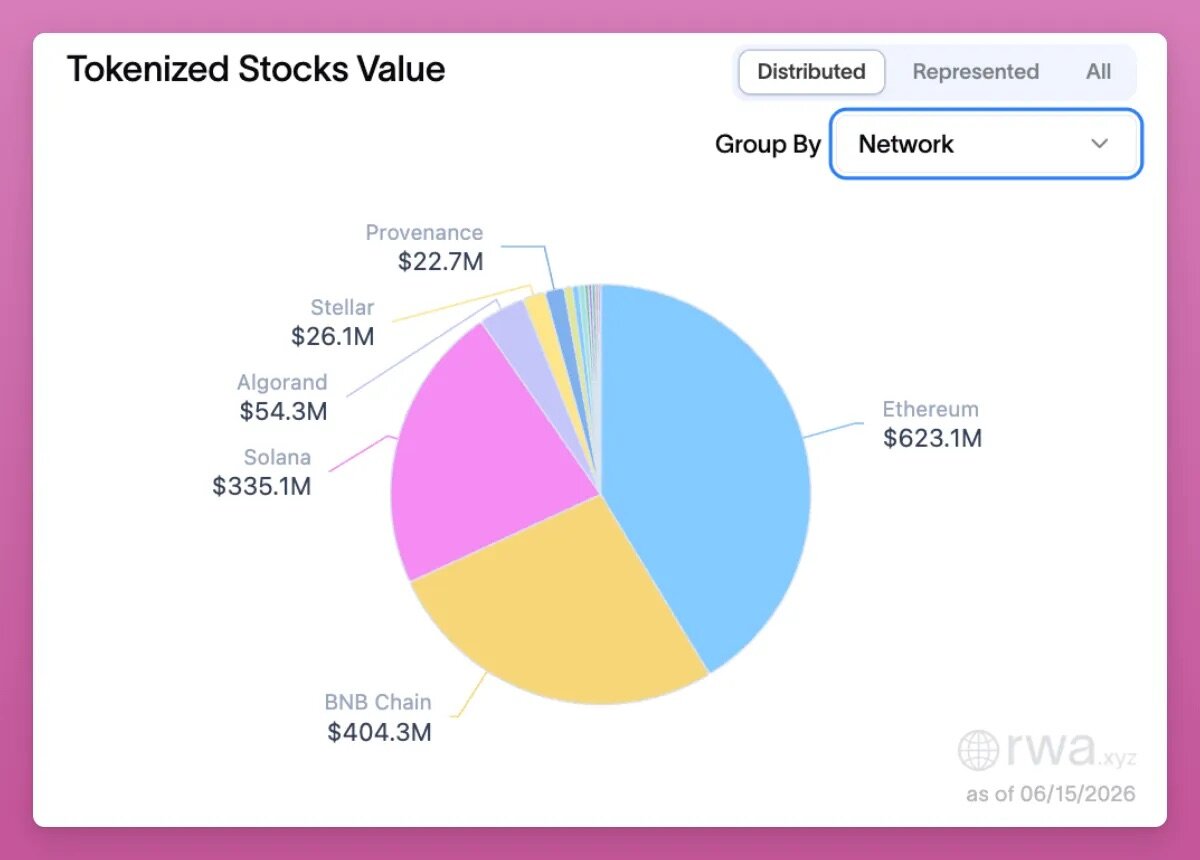

As of now, the total freely circulating value of tokenized equity across platforms is $1.5 billion (these assets can be transferred peer-to-peer between different wallets, independent of the issuing platform), mainly deployed on Ethereum, BNB Smart Chain, and Solana. But the overall size of this track is still minuscule: $1.5 billion is even lower than the $1.9 billion market cap of the Uniswap token UNI itself.

Standard Chartered is known for extremely optimistic price predictions (previously predicting Ethereum at $40,000 and Bitcoin at $500,000 by 2030), but the underlying logic for being bullish on UNI is sound: as the total value locked in tokenized equity rises, it will drive on-chain trading volume, increasing platform fees, which are now used to buy back and burn UNI tokens.

Uniswap is not the only beneficiary. Once the tokenized equity track explodes, the entire crypto industry chain will profit: lending protocols like Aave, Fluid, and Kamino, as well as decentralized exchanges like Pancakeswap and Jupiter on various public chains, will all get a piece of the pie.

The development of tokenized equity could make the crypto industry counter-cyclical: currently, when the prices of Bitcoin and Ethereum fall, decentralized lending experiences massive deleveraging, protocol revenues shrink, and platform tokens come under pressure simultaneously. Perpetual contract DEXs were among the first to benefit from tokenized stock dividends; spot exchanges will be the next wave of beneficiaries.

Following the release of Standard Chartered's report, the UNI token surged 13% in a single day, but there are more investment opportunities within the track. Over the past two weeks, Backpack's platform token, BP, has surged 200%.

As a centralized exchange, Backpack has struggled to find a core business that truly meets market demand, facing competition from established giants like Binance and battling with Hyperliquid's decentralized perpetual contract platform for users. The tokenized asset business seems to have finally found its core growth path.

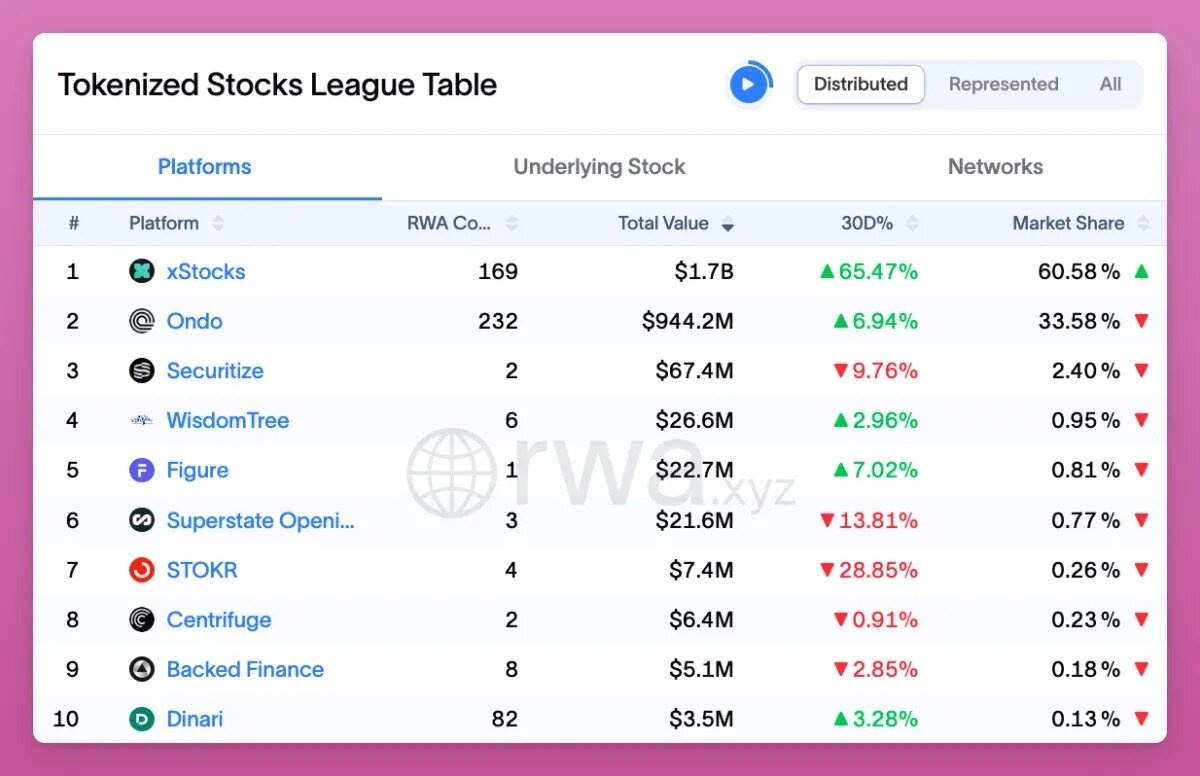

The vast majority of tokenized stocks on the market (xStocks, Ondo) follow a custodial wrapping model: the issuer holds the physical stock and mints a token that tracks the stock price. Users only gain price exposure and do not own the actual equity. Backpack, however, achieves native on-chain issuance through Superstate's Opening Bell product line: these tokens are SEC-registered equity, with rights identical to stocks listed on the NASDAQ. Holders are entitled to dividends and voting rights, and the platform holds a full set of compliance licenses (the Backpack founding team is from the former FTX Europe division).

This logic extends to the platform's native token, BP: by staking BP for one year, when the company goes public via IPO or is acquired, BP can be exchanged for actual company equity (with a 7-day redemption window each year).

There are also direct trading opportunities within the tokenized equity track: Ondo ranks second in the industry by total freely circulating value, and the platform has issued its native token, ONDO.

However, ONDO only has governance functions and almost no other value-capture capabilities. All platform revenue belongs to the company and is not distributed to token holders. While the market is discussing enabling a fee dividend mechanism, its implementation is still uncertain. Moreover, the token faces immense dilution pressure, with nearly 50% of the supply yet to be unlocked by 2029.

If market sentiment for tokenized equity heats up, there is an opportunity for short-term speculation on ONDO, but I would not hold it long-term.

The industry leader, xStocks, holds a 60% market share, with a total scale of approximately $1.7 billion. Backed Finance buys real stocks and ETFs, places them in 1:1 reserve with a custodian, and then mints tokens that track the price of the underlying assets. The products are deployed on Solana, Ethereum (with a small portion on Arbitrum Layer 2). Users can trade on the Kraken exchange 5 days a week, or trade 24/7 on-chain, covering about 60 assets. The number of assets is fewer than Ondo, but the liquidity is better.

Holding an xStock token does not mean holding the underlying physical stock; it is merely a claim against the issuer. In case the platform faces risk, investors are only unsecured creditors of a cross-jurisdictional wrapping service provider, a stark contrast to Backpack's model where holders have real equity.

Ironically, Kraken acquired Backed Finance just weeks after submitting its own IPO application last year, valuing itself at $20 billion. This also raises questions in the market about whether the platform will issue an independent token.

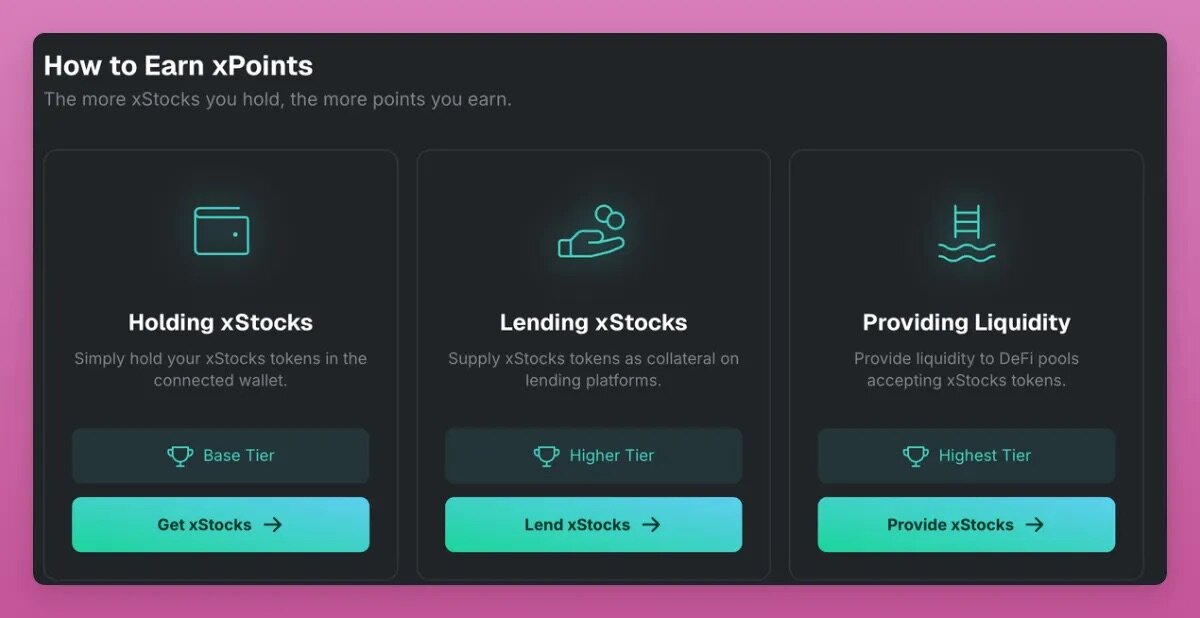

After the acquisition, xStocks launched the xPoints points activity in March. Points programs are often a precursor to a token launch, but the platform has not yet confirmed whether it will launch a token.

xPoints Activity Website

This is quite puzzling: since Kraken can sell its own equity through traditional channels, why would it need to issue a separate xStocks platform token?

A more plausible explanation for launching the points program is that Kraken has partnered with Nasdaq for tokenized stocks. The platform needs trading volume and liquidity to support the business scale, thereby boosting Kraken's overall performance metrics.

I don't want to be the exit liquidity for this sector again, but if you are willing to participate in points mining, the rules for acquiring points are as follows:

- Providing Liquidity: 7x points (highest tier, supporting Raydium, Orca, Byreal)

- Asset Lending: 5x points (on the Kamino platform)

- Simply Holding Tokens: 1x base points

- Trading on the Kraken centralized exchange does not earn points; only on-chain operations accrue points.

The third largest player in the industry is Securitize, and I don't plan to participate in its points mining. The company plans to go public via a SPAC merger with Cantor Equity Partners, with an overall valuation of approximately $1.25 billion. BlackRock led a $47 million funding round. The platform has no native token, so mining would yield no returns.

As mentioned above, there are several arbitrage strategies within this track: for example, when the perpetual contract funding rate is negative, you can short on Hyperliquid (while also mining trade.xyz points) or Variational while buying spot tokens; you can also compare funding rates across exchanges on the Ostium platform (which currently has no token).

If manually managing positions is too cumbersome, you can check out the Nado platform: it is an order book DEX supporting unified margin accounts for spot, margin, and perpetual contracts. The development team previously built Kraken and launched the INK product. The platform will support tokenized stock spot and perpetuals, enabling delta-neutral strategies. It's a low-attention opportunity worth participating in for points mining.

But be cautious: the primary market token platform Ventuals just announced its shutdown, informing users that all platform points have become worthless. Participating in token airdrop mining now requires more effort, and the certainty of returns has significantly decreased.

The Story is Far from Over

The term "crypto" now covers a vast area, including tracks like perpetuals, NFTs, prediction markets, and Meme coins; the RWA sector is also continuously expanding, with sub-tracks worthy of deep, individual analysis.

Stablecoins, money market funds, credit, private equity, and tokenized stocks are all different sub-sectors, each with vastly different risk and return logics