J.P. Morgan Mid-Year Outlook: AI Narrative Not Yet Peaking, Reduce Cash, Increase Physical Assets

- Core Viewpoint: J.P. Morgan believes the market is overly pessimistic in pricing the three major global risks (fragmentation, inflation, AI disruption), and the current volatility presents a window for entry. It recommends continuing to bet on the AI supercycle and US stocks, hedge inflation with physical assets, reduce cash holdings, and pay attention to opportunities in emerging markets.

- Key Elements:

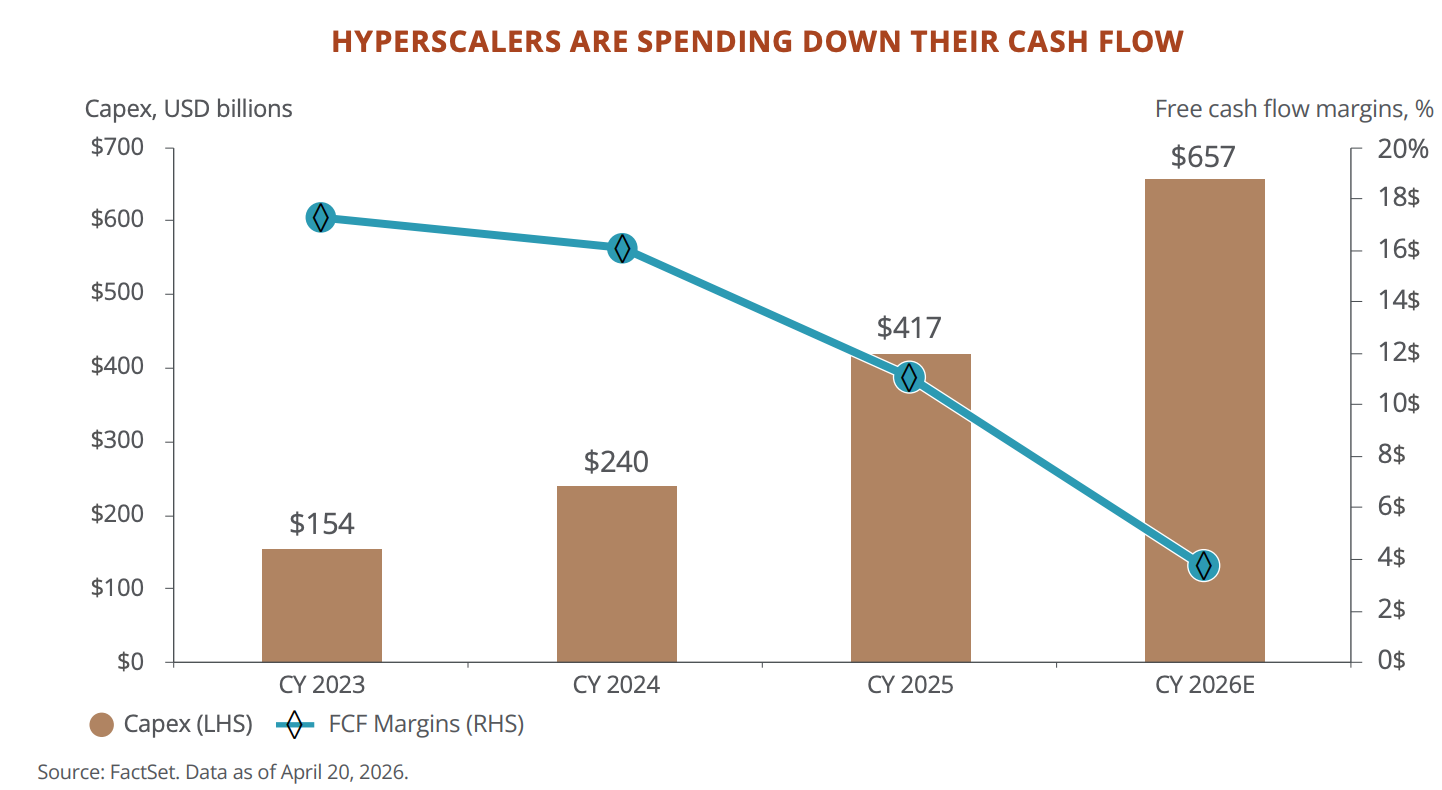

- AI Capex Unabated: The five major cloud giants' expected 2026 capital expenditure exceeds $650 billion, a further upward revision of $130 billion from last quarter. The market prices in "AI peaking," but data does not support it.

- Shift in Financial Profile of Tech Giants: The free cash flow of the five giants is expected to drop from $240 billion in 2024 to $73 billion in 2026, marking a transition from an asset-light to an asset-heavy, high-investment model.

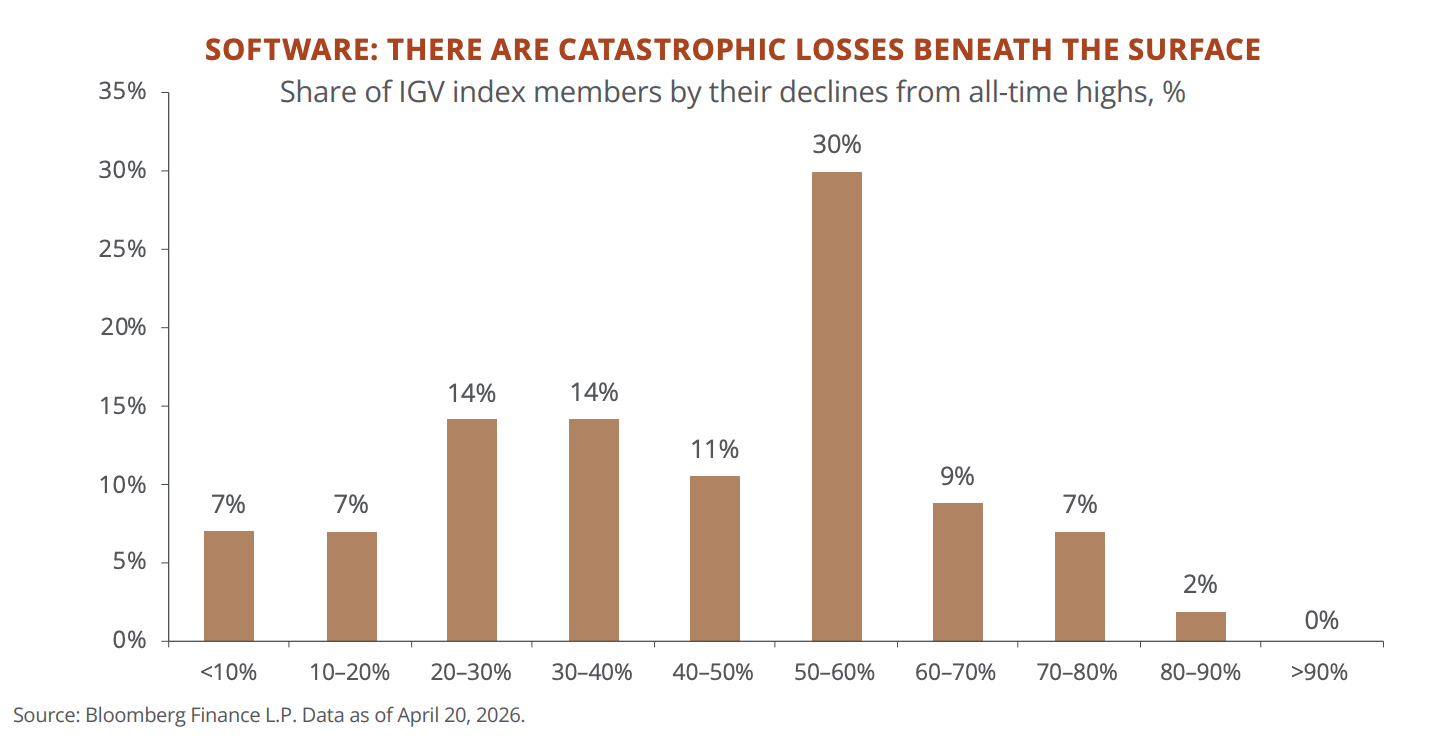

- Pressure on the SaaS Industry: Nearly half of the components in the software index have declined over 50% from their highs. The AI disruption impacts the subscription-based software business model, with approximately 21% of direct lending funds lent to software companies.

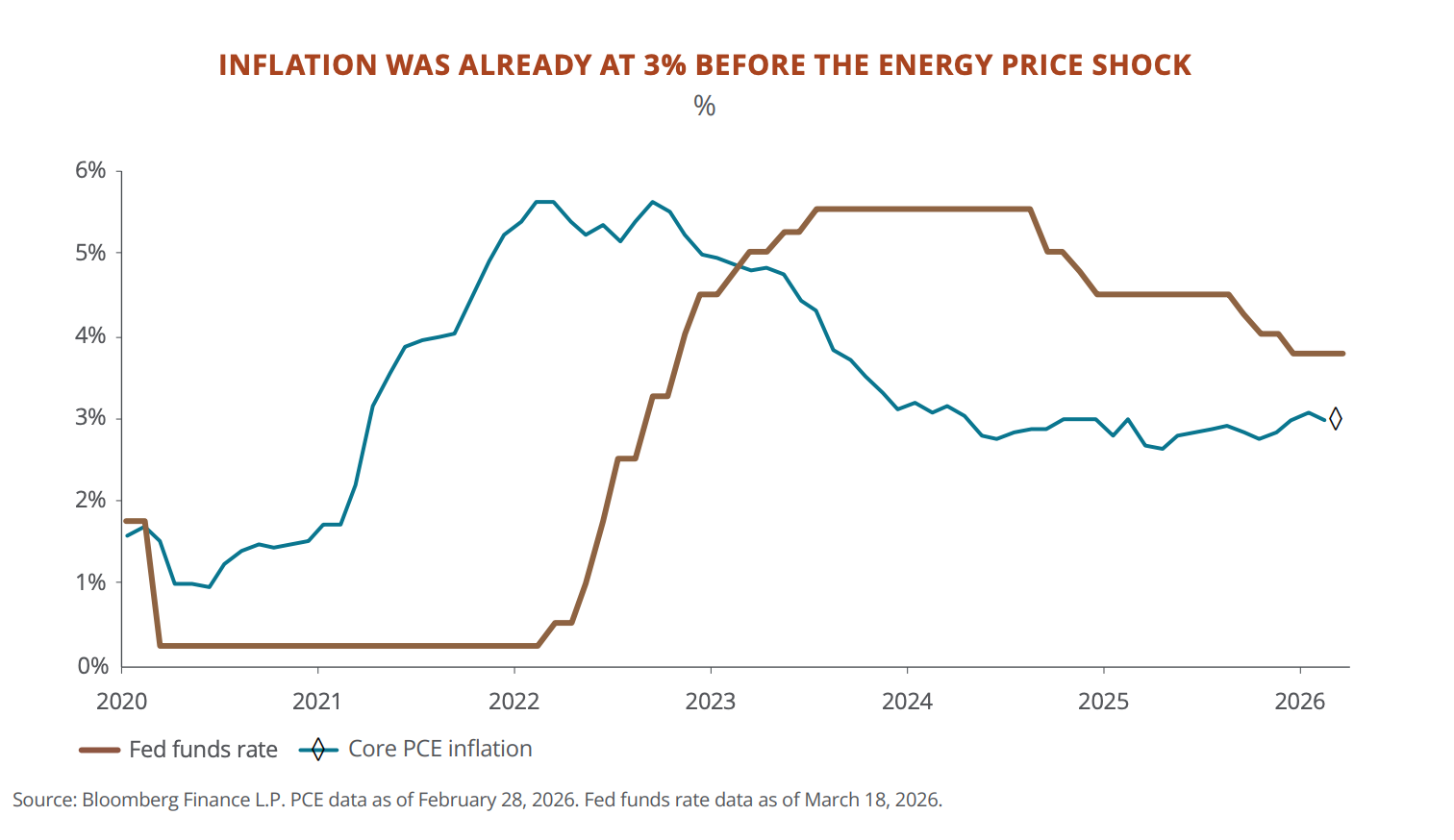

- Inflation Stickier Than Pre-Pandemic: Core PCE was already stuck at 3% before the energy shock. Cumulative price rises are 25%, while core fixed income has only yielded 6%, leading to real losses on cash and bonds.

- Historical Data Supports Buying on Dips: After a roughly 10% correction in US stocks, buying when the VIX breaks above 30 yields a 70%-83% probability of positive returns within 6 months, with an average return of 12.4%.

- Emerging Market Potential Emerges: EM corporate earnings growth expectations are 46%, with a P/E ratio of only 11.8x. The discount of Chinese stocks to Asia is at its deepest in 20 years, and a policy shift could trigger a structural revaluation.

Original Author: David

Overview:

J.P. Morgan Wealth Management released its 2026 mid-year outlook report on June 1st. Essentially, with the year half over, it advises their high-net-worth clients on investment strategies for the second half.

Against the backdrop of a Strait of Hormuz blockade driving up oil prices, resurgent inflation, and the AI narrative shifting from euphoria to skepticism, the report's overall tone is cautiously optimistic—but it emphasizes the need to adjust specific investment allocations.

J.P. Morgan believes the market has overly-pessimistically priced the three major global risks (fragmentation, inflation, AI disruption) and that the current volatility actually presents an entry window.

Overall assessment:

Continue betting on the AI super-cycle and US stocks, hedge against inflation with real assets and alternative strategies, reduce cash holdings, and focus on emerging markets.

If you hold US tech stocks or are considering increasing or reducing positions in the second half of the year, the framework and data in this report are worth a look. We have condensed and interpreted the original report, reordering the priorities based on investment relevance.

Six Key Conclusions:

① The AI super-cycle is not over; the market is overly pessimistic.

The five hyperscalers (Microsoft, Meta, Oracle, Google, Amazon) are expected to have combined capital expenditures exceeding $650 billion in 2026, an upward revision of $130 billion from the previous earnings season. AI-related investments contributed 25 basis points to US real GDP growth in 2025. Taiwan's GDP growth rate surpassed 7%, the fastest since 2010, driven primarily by semiconductor exports. JPM believes the market is pricing in "peak AI," but the data doesn't support this narrative.

② The financial profile of the Hyperscalers is changing.

Free cash flow is projected to decline from $240 billion in 2024 to $73 billion by the end of 2026. Microsoft's forward P/E ratio has dropped from the AI-era high of 35x to 22.5x. These companies are transitioning from "asset-light, high-return" to "asset-heavy, high-investment" models, and the market is still digesting this shift.

③ SaaS is experiencing a bloodbath beneath the surface.

Approximately half of the components in the S&P Software Index (IGV) have fallen over 50% from their all-time highs. JPM's tracked "AI Vulnerable" basket is down nearly 20% this year. In the private credit market, 21% of exposure is to software companies, which rises to 40% when including tech and business services. The disruption of SaaS business models by AI is already happening.

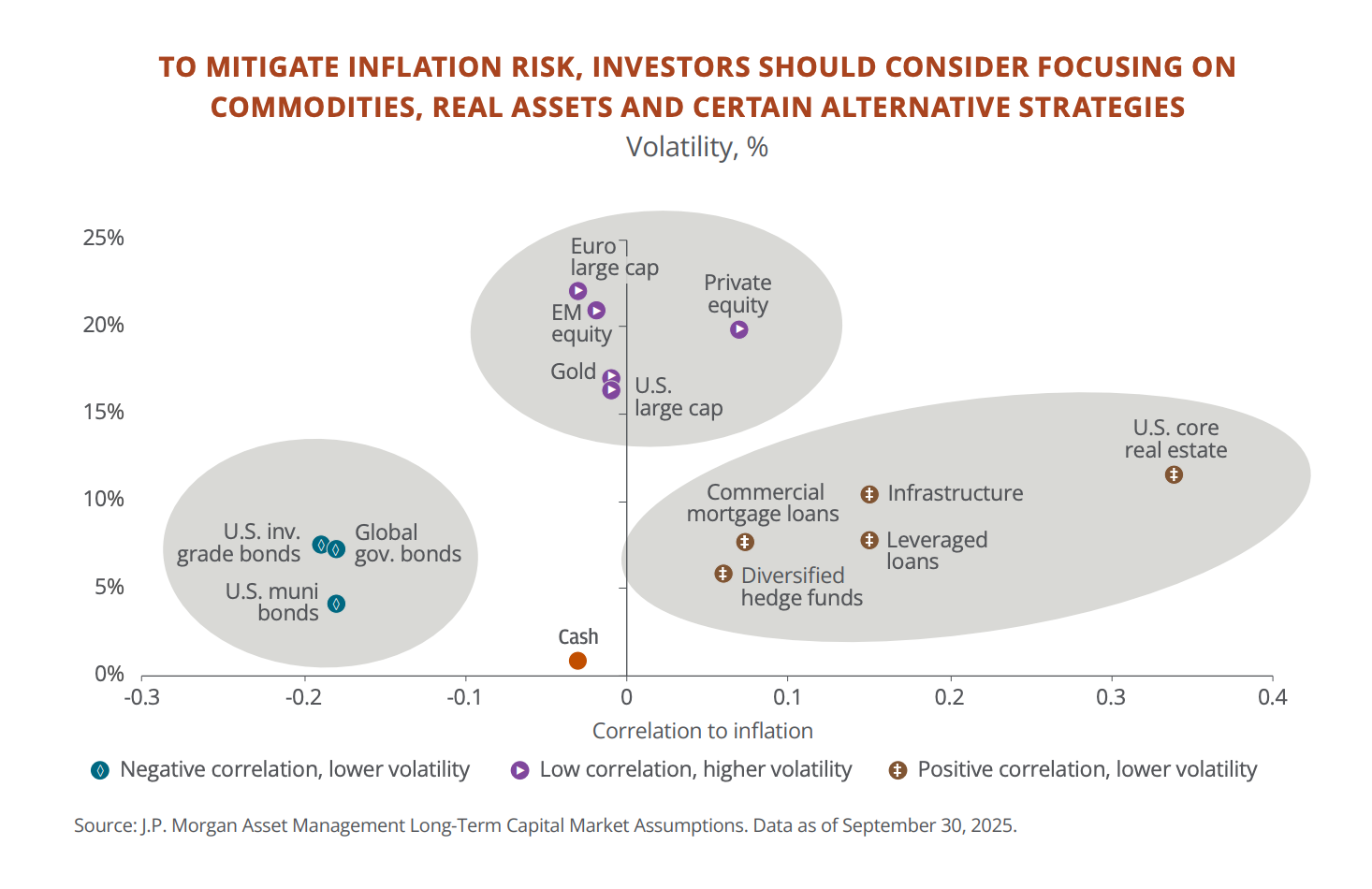

④ The inflation floor is higher than pre-pandemic; cash is slowly bleeding out.

US Core PCE was already sticky around 3% before the energy shock. Since the 2020s, consumer prices have risen a cumulative 25%, while core fixed income has only returned 6%. Nearly 20% of JPM's client assets are in cash and short-term bonds. The report's message is clear: you think you're hedging, but you're actually losing money.

⑤ The Strait of Hormuz blockade is the biggest oil supply shock since WWII, but JPM advises buying on the dip.

Oil prices nearly doubled, US stocks experienced a ~10% correction, and the S&P 500's P/E ratio briefly fell below 20x. JPM's historical data shows that buying after the VIX breaks above 30 yields a 70% to 83% probability of positive returns over six months, with an average return of 12.4%.

⑥ Emerging markets could be an opportunity for the second half.

EM corporate earnings are expected to grow by 46%, while the P/E ratio is only 11.8x. Taiwan and South Korea are critical nodes in the AI hardware supply chain. Latin America holds over 40% of the world's copper and nearly 60% of its lithium reserves. The valuation discount of Chinese stocks relative to the rest of Asia is at its deepest in 20 years, and JP's stance is "cautiously warming."

On AI: The Market Prices "Peaked," JP Morgan Says It's Too Early

JPM opens by stating that Wall Street's narrative on the AI super-cycle "has become too pessimistic."

Core data supporting this judgment:

The five cloud computing giants—Microsoft, Meta, Oracle, Google, and Amazon—are expected to have combined capital expenditures exceeding $650 billion in 2026. Cloud rental prices for GPUs (the core chips for training AI models) have risen 40% since last October, with supply still unable to keep up with demand. Nvidia's stock trades at a 40% discount to its average P/E ratio over the past decade. The market is pricing in "peak chip sales," but cloud business revenue is still accelerating.

At the same time, the financial characteristics of these five companies are changing. Free cash flow is projected to decline from $240 billion in 2024 to $73 billion by the end of 2026, and Microsoft's P/E ratio has dropped from the AI-era high of 35x to 22.5x. The asset-light model that attracted investors over the past decade is being rewritten by heavy capital investment. JPM believes the focus should now be on revenue growth rather than cash flow, but this also means that if demand slows, these investments could become a burden.

Other judgments on AI serve as localized risk warnings within the larger trend:

Traditional software companies are the first true victims of AI. About half of the components in the US software sector index have fallen over 50% from their highs, with a median operating profit margin of only 4%. The logic of the disruption is simple: SaaS charges per user, and AI reduces the number of users. This has already transmitted to the lending market, with about 21% of US direct lending money lent to software companies. Prices of publicly traded tech loan funds have fallen close to the lows of the last cycle. JPM's stress tests show potential losses up to 4% with leverage in extreme scenarios, but it doesn't currently pose a systemic risk.

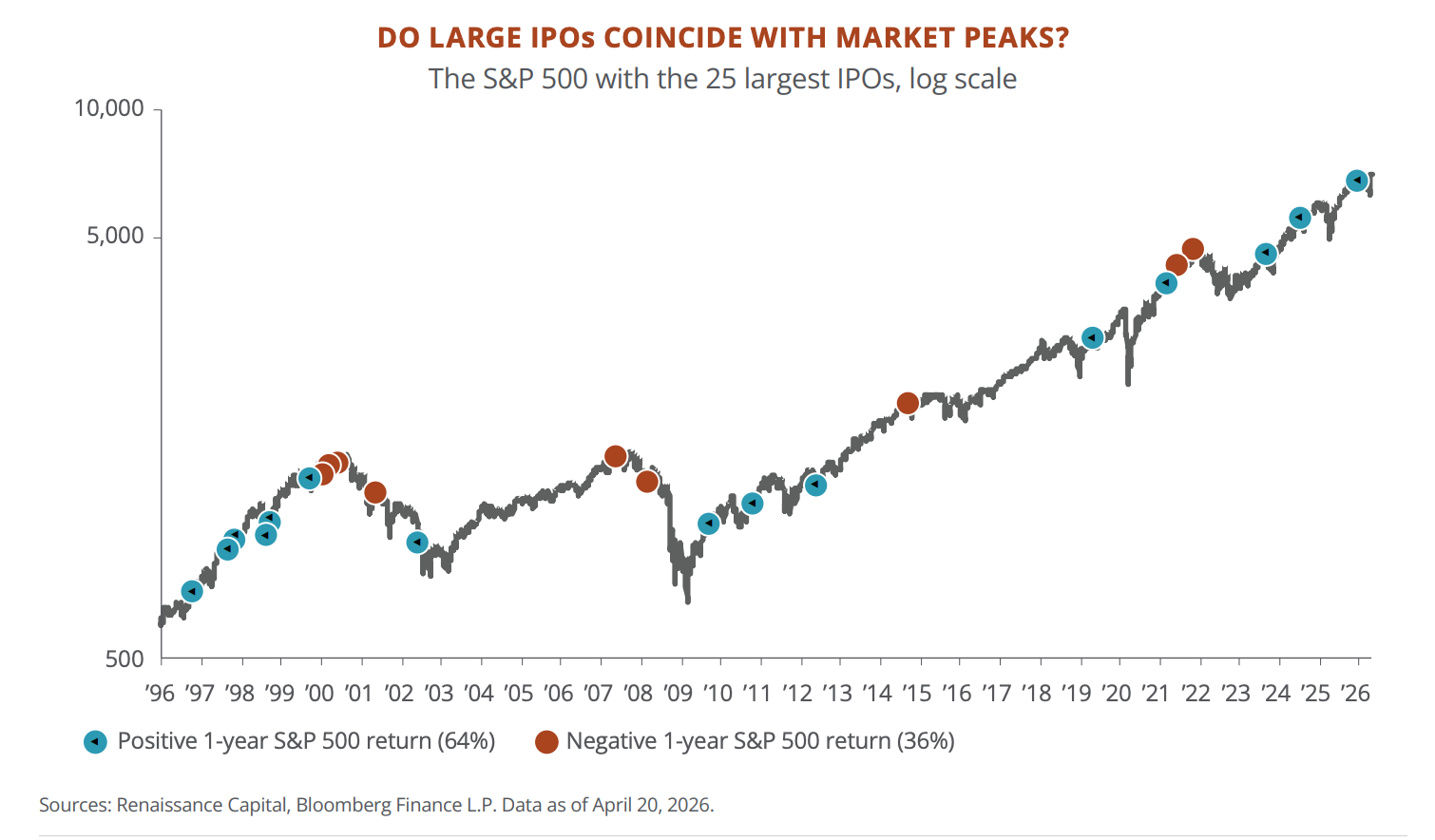

SpaceX, Anthropic, and OpenAI might go public this year in a cluster, historically a bad omen. Following the 25 largest IPOs in history, the median new stock underperformed the broader market by 30 percentage points in its first year, with 12 out of 18 falling in their first year. In years with mega-IPOs, the median annual return for the broader market was only 3%, far below the long-term average of 10%. JPM didn't say it's definitely a peak, but it explicitly treats the public listing reaction of SpaceX as a cycle thermometer.

On Inflation: Inflation Won't Return to 2%, Your Cash and Bonds are Losing You Money

The key point about inflation isn't the Strait of Hormuz driving up oil prices, but that US inflation hadn't returned to normal levels even before oil prices surged.

In January 2026, core PCE was 3.1% year-over-year, with particularly stubborn increases in local service categories like dining and personal care. Then oil prices doubled. The Fed's model shows that for every $10 increase per barrel of oil, inflation rises by about 0.3 percentage points. This time, oil rose by $40.

JPM believes a full-scale replay of the 1970s is unlikely. There is no wage-price spiral in the labor market, the quit rate is declining, housing inflation has dropped from 5% at the end of 2024 to just over 3%, and China's overcapacity is also depressing global goods prices. However, the inflation floor is significantly higher than pre-pandemic levels, likely hovering around 3%.

JPM's suggested response is to increase allocation to real assets.

Since 2020, US prices have risen a cumulative 25%, while bonds have only returned 6%, and cash even less. You might think your money is safe, but it's shrinking in value every year. Among JPM's own clients, nearly 20% of assets are still in cash and short-term bonds.

Therefore, its advice is to move some money into inflation-linked assets:

- Commodities, infrastructure, and real estate—things that rise with prices. It suggests allocating a combined total of about 5% of the portfolio to these.

- Gold alone is recommended at 3% to 6%.

- Additionally, hedge funds. When stocks and bonds both fell in 2022, macro strategy hedge funds returned 9%. However, JPM also admits that 94% of its private banking clients have never bought hedge funds, and 86% have never bought infrastructure-type products.

One sentence to summarize this section:

Inflation might not spiral out of control, but it won't return to 2% either. If your portfolio is still the traditional 60/40 stock-bond split with a pile of cash, JPM believes you are preparing for a world that no longer exists.

On Geopolitics: Chinese Stocks May Face a Structural Revaluation

This section covers the most diverse topics, from the Middle East conflict to US-China rivalry to Europe's struggles. We'll only pick out items directly relevant to investment decisions.

1. The Strait of Hormuz blockade was the biggest market shock in the first half of the year. Approximately 20 million barrels of oil pass through this chokepoint daily, accounting for one-fifth of global oil consumption. Following joint US-Israeli strikes on Iran, oil prices nearly doubled within a few days, and European natural gas prices surged nearly 100% in two days. QatarEnergy's CEO stated that 15% of LNG capacity could be offline for up to five years. Qatar also supplies about 30% of the world's helium, which is essential for chip manufacturing. South Korea has already warned of potential chip factory shutdowns.

JPM believes the conflict is moving towards de-escalation, but the physical damage and energy risk premiums won't disappear quickly.

Hence, their advice to investors is: Use the pullback to add to US stocks.

US stocks fell about 10% in the first half of the year, and the S&P 500's P/E ratio briefly dipped below 20x. Historically, buying after the VIX (fear index) breaks above 30 yields a 70% to 83% probability of positive returns over six months, with an average gain of 12.4%.

2. The US and China are building their own ecosystems, and the market may accelerate into two camps. The US is restricting chip exports to China, pressuring the Netherlands and Japan to jointly restrict semiconductor equipment sales. China is expanding exports to non-US markets, with Belt and Road Initiative investments hitting a record high in 2025—$53 billion invested in Brazil alone in one year. Total trade with Latin America has already surpassed that of the US. JPM's assessment is that future investment returns may increasingly depend on which camp your assets belong to, rather than just the company's own growth.

But fragmentation also creates opportunities, especially in emerging markets.

JPM lists several directions:

- Latin America holds over 40% of the world's copper and nearly 60% of its lithium, plus abundant nickel, rare earths, and agricultural resources. Foreign direct investment has doubled over the past twenty years. Central banks here are better at controlling inflation than those in developed countries, and the political landscape is shifting towards more pragmatic, business-friendly governments.

- Middle Eastern Gulf States are using oil revenues to build AI data centers. Saudi Arabia partnered with Blackstone on a $3 billion data center project, with costs 30% lower than in the US.

- East Asia (Taiwan, South Korea) holds key nodes in the AI hardware supply chain. If AI capital expenditures continue to accelerate, these economies' exports and pricing power will continue to strengthen.

- Chinese stocks trade at their deepest discount to the rest of Asia in 20 years. 80% of Chinese consumers are excited about AI products (compared to 38% in the US), and electricity costs are roughly half of those in the US. JPM's stance is "cautiously warming." If clearer pro-business signals emerge from policy, Chinese stocks could face a structural revaluation.

In comparison, Europe is the market towards which JPM is most conservative. Electricity prices are two to four times higher than in the US. R&D spending as a percentage of GDP is only 2.2% (US 3.6%, South Korea 5.2%), and venture capital is one-tenth the size of the US.

The energy shock also pressures the European Central Bank to potentially raise interest rates again. JPM only recommends buying defense and infrastructure-related assets in Europe, advising to avoid automotive and consumer sectors.

What JPM is Betting On, and Not Betting On

Condensing the 60-page report into one sentence: Volatility is an entry opportunity, but the posture for entry must change.

What You Should Bet On:

- AI infrastructure chains (chips, optical modules, power), emerging market stocks and bonds, real assets (commodities, infrastructure, gold), defense-related assets, China AI concepts (cautiously add positions).

What You Should Not Bet On:

- Cash, traditional subscription-based software companies, European automotive and consumer sectors, and investment models purely relying on a 60/40 stock-bond split to weather the second half of the year.

Link to original research report: