I generated a high-quality translation into Thai, ensuring strict adherence to HTML structure and terminology for blockchain and finance contexts. 一周千万,币圈套利者的美股新猎场

- ประเด็นหลัก: อุตสาหกรรมคริปโตกำลังนำกลยุทธ์การเก็งกำไรจากอัตราเงินทุน (funding rate) ของสัญญาถาวร (perpetual contract) มาประยุกต์ใช้กับตลาดหุ้นสหรัฐ โดยการทำธุรกรรมป้องกันความเสี่ยงแบบ "ถือครอง spot ยาว + ขาย futures สั้น" เพื่อรับอัตราเงินทุนที่สูง สร้างรายได้แบบ "เก็บค่าเช่า" ที่มั่นคง นี่คือผลประโยชน์ช่วงแรกเริ่มของการที่สินทรัพย์ดั้งเดิมถูกแทรกซึมโดยนวัตกรรมการเงินคริปโต

- ปัจจัยสำคัญ:

- สัญญาถาวรใช้กลไกอัตราเงินทุนเพื่อสร้างสมดุลระหว่างฝั่งซื้อและขาย เมื่อฝั่งซื้อ (Long) หนาแน่นจะต้องจ่ายค่าธรรมเนียมให้ฝั่งขาย (Short) อัตรานี้อาจสูงถึงหลายร้อยเปอร์เซ็นต์ต่อปี (เช่น หุ้น Samsung Electronics บน Binance สูงถึง 364%)

- นักลงทุนรายใหญ่คริปโต Cbb ใช้กลยุทธ์ป้องกันความเสี่ยงโดยซื้อหุ้นสหรัฐในตลาด Spot พร้อมกับทำ Short สัญญาถาวรบน Hyperliquid ซึ่งในช่วงหลายเดือนที่ผ่านมาสามารถทำกำไรจากอัตราเงินทุนได้ถึง 2.4 ล้านดอลลาร์สหรัฐ โดยไม่ขึ้นอยู่กับความผันผวนของราคาหุ้น

- สถาบันอย่าง Ethena วางแผนที่จะใช้กลยุทธ์เก็งกำไรแบบ Delta-Neutral กับสัญญาถาวรของหุ้นสหรัฐ โดยคาดว่าจะสามารถสร้างรายได้ที่มั่นคงจากอัตราเงินทุนได้ปีละ 40 ถึง 80 ล้านดอลลาร์สหรัฐ

- Binance รองรับการซื้อขาย Spot และสัญญาถาวรสำหรับหุ้นสหรัฐมากกว่า 7,000 ตัว ขณะที่ปริมาณสัญญาคงค้าง (Open Interest) บนแพลตฟอร์มแบบกระจายอำนาจอย่าง Hyperliquid เพิ่มขึ้นอย่างต่อเนื่อง ขยายฐานตลาด

- หน้าต่างโอกาสช่วงแรกเริ่มของกลยุทธ์เก็งกำไรนี้อาจแคบลงเมื่อเม็ดเงินไหลเข้ามามากขึ้น ซึ่งคล้ายกับกรณีที่อัตราเงินทุนของ Bitcoin ลดลงจาก 18% ต่อปีเหลือ 9% ต่อปี

Futures, options, and CFDs—these concepts sound highly technical.

In the past, many believed derivatives were the most complex instruments in traditional financial markets. However, these trading methods are becoming increasingly common in the crypto industry.

Recent hot discussions in the crypto community haven't only focused on US stock targets themselves, but also include topics like: "I've been having so much fun arbitraging on Hyperliquid lately, I don't even want to do research anymore," and "All I see is funding."

A few years ago, such conversations would have been about arbitrage opportunities in Bitcoin or Ethereum. But now, with US stocks being tokenized becoming a new trend, their targets have shifted to US stocks like Samsung, Nvidia, and GameStop.

Although trading US stocks these days almost seems like a no-brainer—toss money into popular sectors like chips, energy, or optics, and your account balance will likely go up. Someone you know has probably doubled their money by betting on just one or two stocks. But these savvy crypto professionals make money in a way that has absolutely nothing to do with whether those stocks go up or down.

A group of crypto natives are quietly building a new profit model using crypto market strategies on US stocks.

A Contract That Never Expires

This logic starts with one specific instrument: the perpetual contract. Perpetual contracts are the highest-volume "alternative futures" in the crypto market. They don't require settlement at expiry, no manual rollovers are needed, and they are specifically designed for betting on price direction and using leverage. You can open a $50 position with just $5, trade 24/7, and no one stops you if you want to place an order at 3 AM.

But perpetual contracts have come with an inherent problem since their inception: how can a contract that never expires maintain its price in line with the underlying real stock, without drifting off?

The crypto industry's solution for perpetual contracts is introducing a mechanism called the funding rate.

In simple terms, the funding rate is like a head tax—the side with more participants pays the side with fewer.

For example, let's say you are bullish on Nvidia. Instead of waiting for the US stock market to open, you open a 5x long position on a perpetual contract.

But the problem is, many others want to do the same thing. The long side becomes crowded, while there are very few shorts. To balance the two sides, the system mandates that the less crowded side gets paid, and the more crowded side pays. So as a long position holder, you automatically transfer a fee to those on the short side every few hours. The more people are long with you, the more you pay. These costs can be as punishing as paying a fine.

How expensive can this "fine" be? A few real numbers make it clear.

Binance is the world's largest cryptocurrency exchange by trading volume. The annualized funding rate for its Samsung Electronics perpetual long positions is 364%. This means if you go all-in long on Samsung and hold for a full year, this single "head tax" alone would eat up over three times your principal. Nokia's rate is 403% annualized, and BBX is 591%.

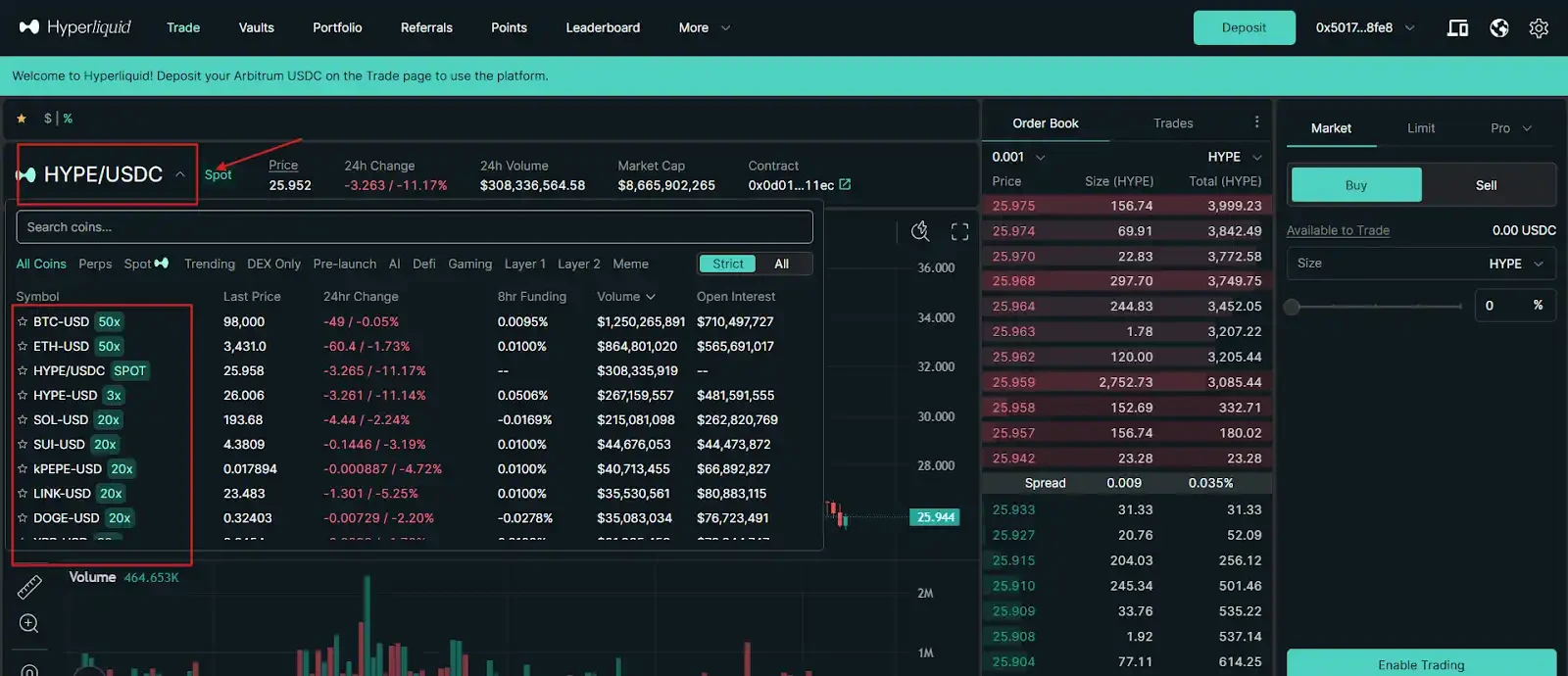

Another platform worth mentioning is Hyperliquid. It is currently the largest decentralized perpetual contract exchange by on-chain trading volume. It requires no account registration, no KYC, and anyone can connect their wallet directly and start trading. It's arguably the crypto product that has brought perpetual contracts closest to the experience of a centralized exchange.

Hyperliquid Trading Interface

On Hyperliquid, Dell's rate is 281%, GameStop (GME) is 227%, and even Zoom is at 287%—a video conferencing company, yet so many are rushing to leverage long positions on it.

An interesting aspect of this funding rate is that it serves as a clear signal of market sentiment between longs and shorts.

It shows how many people in the market are currently FOMO-ing. The stock being chased most aggressively, with the most crowded long positions, will have the highest funding rate. The reverse is also true. Eli Lilly, one of the largest pharmaceutical companies in the US, has negative funding rates on both Binance and Hyperliquid. On Binance, going long on Eli Lilly not only costs nothing but also earns you an annualized 65%. On Hyperliquid, you could earn 103%.

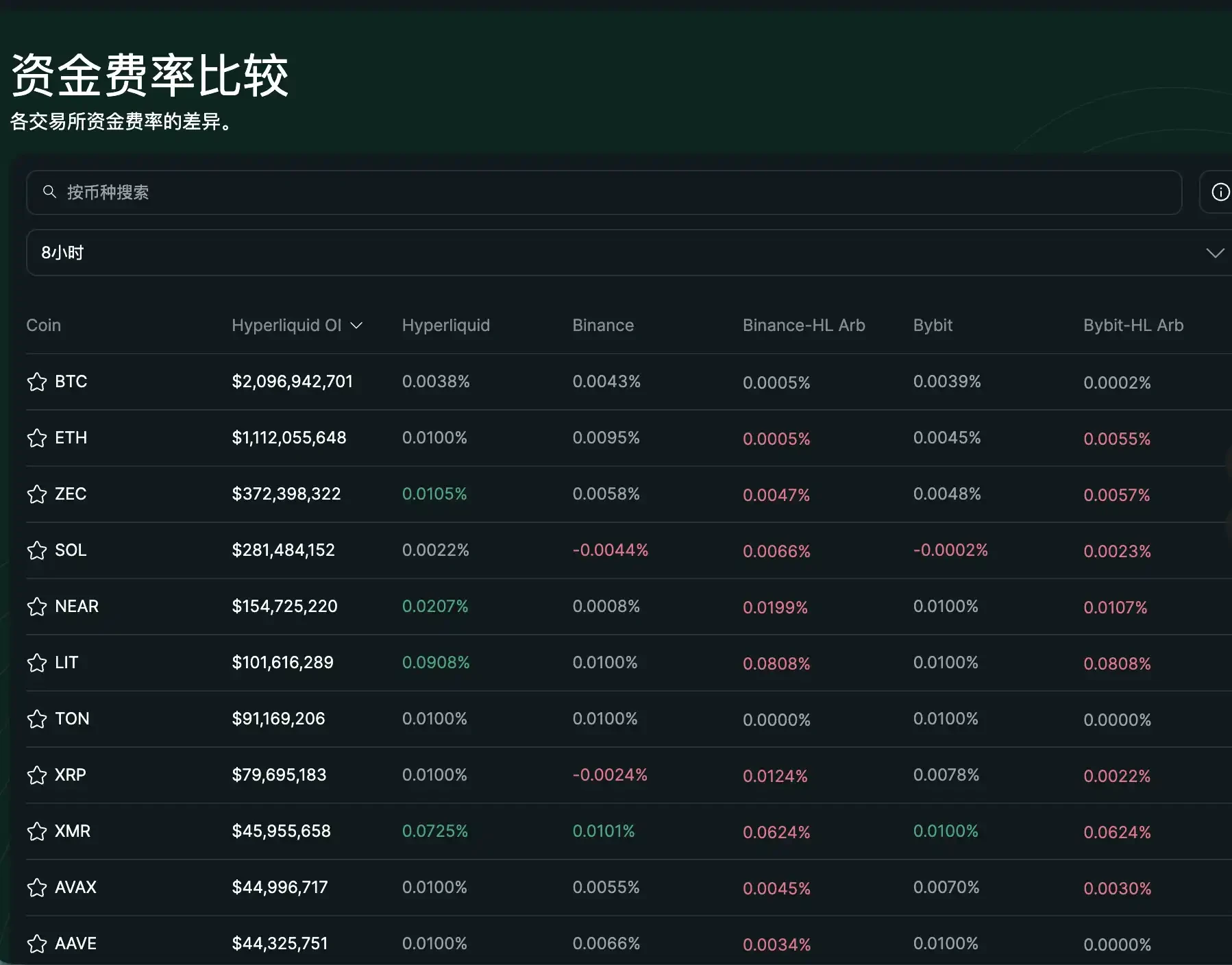

This indicates that too many people are shorting Eli Lilly, so the system has to effectively pay others to go long to maintain balance. The funding rate for the same stock can also differ across platforms. Apple's rate is 0 on Binance but an annualized -14% on Hyperliquid. This difference itself creates an arbitrage opportunity. These numbers don't lie; the more intense the rush into one side, the more lucrative it is for those on the opposite side.

These extreme funding rates are visible in real-time on platforms like Hyperliquid, also creating cross-exchange arbitrage opportunities (e.g., the rate difference between Binance and Hyperliquid)

A New Business After Tokenizing US Stocks

Cbb (X: @Cbb0fe) is a well-known large trader in the crypto space who made his initial fortune in the crypto market. He has been arbitraging token perpetual contracts for years. Early on, he publicly shared how he made $5 million running arbitrage bots on the Hyperliquid chain.

He is also one of the first to transplant this strategy onto US stocks.

Cbb's logic is simple: on one hand, he buys the actual stock in the traditional market; on the other, he opens an equal-sized short position on the perpetual contract. If the stock price goes up, profits from the spot position cover the losses on the contract. If the stock price drops, profits from the contract cover the losses on the spot.

This hedging mechanism makes him completely indifferent to price fluctuations. The only thing he cares about is that "head tax" in the middle. He recently stated that he has made $2.4 million purely from collecting funding rates. While everyone else is frantically trading US stocks to strike gold, he is selling shovels to the gold miners. Now that perpetual contracts on US stocks are emerging, he has directly applied his crypto-honed strategy to targets like Apple and Samsung.

Some might ask, why is this opportunity exclusive to the crypto space? Can't you do it in traditional finance? Traditional markets have similar concepts, like stock borrowing fees or overnight interest. Whether you are using margin to go long or borrowing shares to short, there is a cost. However, that fee goes into the broker's pocket. The mechanism is opaque; you can't see the overall long-short ratio in the market, and you certainly can't receive this fee as a counterparty. Brokers keep this business to themselves; ordinary market participants can only pay, never collect. Perpetual contracts have made this mechanism transparent. Anyone can see the real-time funding rate, and anyone can be the one collecting the fee. This is an invention of the crypto world now being applied to US stocks.

It's not just individuals like Cbb. Institutions have started to eye this lucrative opportunity.

Ethena, one of the largest stablecoin projects on the Ethereum ecosystem, is considering allocating a portion of its reserves into this strategy for hedging. They estimate this could generate an additional $40 million to $80 million in annual revenue.

Ethena captures funding rates through a delta-neutral hedging strategy (long spot + short perpetual), which has become a core mechanism for generating yield on its USDe stablecoin. This strategy is written into its protocol mechanism, representing a quantifiable "rent-collecting" type of income, rather than mere speculation.

For institutions, this is not gambling. It's a stable cash flow that can be programmed into asset allocation strategies. The nature of this income is more akin to collecting rent, where the "tenants" are those eager to use leverage to trade US stocks.

So the question remains: Will astronomical annualized rates like Samsung's 364% and BBX's 591% persist forever, or will they eventually be arbitraged away?

Let's look at Bitcoin for reference. In the early days, the annualized funding rate for Bitcoin perpetual contracts was consistently around 18%. After the Bitcoin spot ETF was listed and Wall Street arbitrage capital flowed in, the funding rate was compressed to 9% within a few months—cut in half.

It's highly probable that perpetual contracts for US stocks will follow a similar path. The current high rates exist because few participants are involved in this arbitrage and the order books are thin.

However, Binance has already listed spot trading for over 7,000 stocks, the NYSE is promoting 24/7 trading, and the US futures regulator, the CFTC, has begun signaling a willingness to create a compliant pathway for perpetual contracts. Both sides are moving towards the middle. Currently, the CFTC has opened a compliance path for Bitcoin perpetuals, and platforms like Coinbase are launching simulated perpetual products, while Hyperliquid's open interest (OI) for stock perpetuals continues to grow. Once arbitrage capital floods in, a compression path similar to Bitcoin's early drop from 18% to 9% is likely to repeat in the US stock perpetual market.

Therefore, the current phase is essentially an early-stage window of opportunity. Those who move first will capture the most significant share of the profits.