美股两个月狂飙16%:历史只出现过4次,最近一次是1987崩盘前

- 核心观点:美股近两月16%的涨幅在非衰退背景下极为罕见,仅1987年“黑色星期一”前出现过类似情况。当前市场存在信用市场过度乐观、消费者压力信号累积及股债市背离加剧等多重风险,尾部风险异常突出。

- 关键要素:

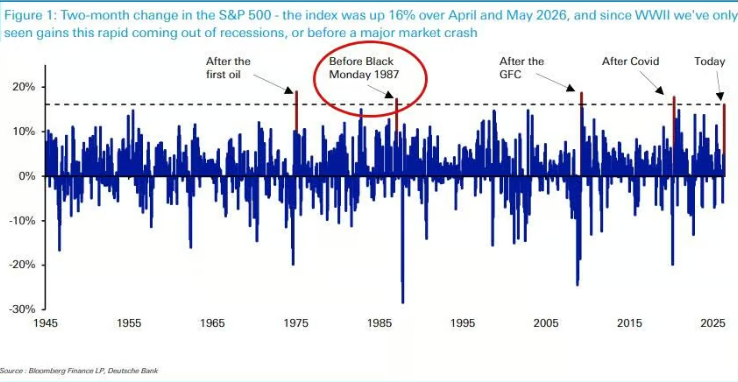

- 历史先例:标普500在4-5月累计上涨16%,二战以来仅4次,其中3次为衰退后复苏,唯一非衰退先例是1987年崩盘前。

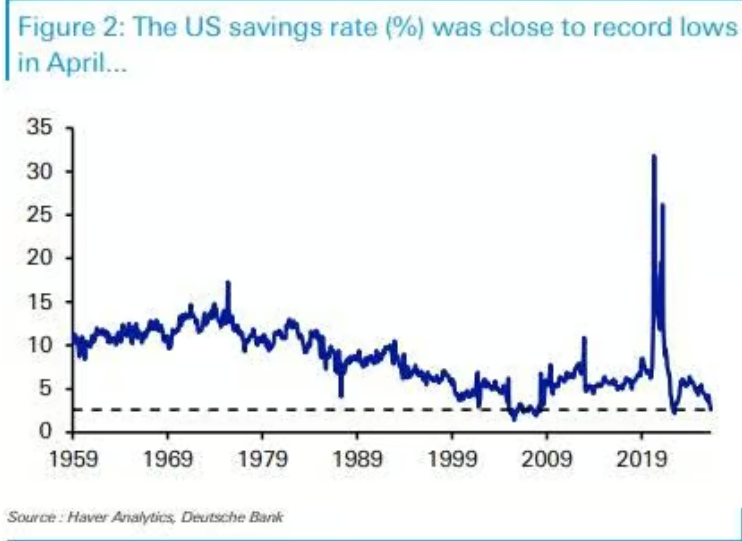

- 消费者信号:美国4月储蓄率降至2.6%,仅类似2022年及金融危机前夕;5月密歇根消费者信心指数创历史最低。

- 信用背离:美欧信用利差收窄至低于冲突前水平,但这与央行加息预期及历史规律(利差应走阔)形成反差。

- 债市压力:10年期美债收益率随油价波动独立承压,30年期美债收益率升至2007年以来最高,与股市高位形成背离。

- 油价支撑:霍尔木兹海峡封锁超预期,但布伦特原油价格保持平稳,这抑制了滞胀定价,是风险资产韧性的关键。

Original Author: Zhao Ying

Original Source: Wall Street CN

The strong rebound in U.S. stocks over the past two months is triggering a historical alarm. The S&P 500 index rose a cumulative 16% in April and May, a gain that has occurred only four times since World War II. Three of those instances happened during recovery phases after economic recessions, with the sole exception occurring in a non-recession context—just months before the "Black Monday" crash in October 1987.

Henry Allen, a macro strategist at Deutsche Bank, pointed out that the current rally is not occurring against a backdrop of recession recovery, making the historical comparison particularly stark. Meanwhile, credit spreads remain near historic lows, but pressure signals on the consumer side are building. Expectations for Federal Reserve rate hikes are rising, and the divergence between sovereign bond markets and the stock market continues to widen.

With multiple risk factors overlapping, tail risks in the market are becoming unusually concentrated. Henry Allen wrote in his report, "The tail risks in the current distribution are exceptionally prominent, both at the geopolitical level and at the market level."

A Rare Historical Precedent: Only One Instance Outside a Recession

The S&P 500's two-month gain of 16% in April and May has only four precedents since World War II.

Three of these occurred during strong post-recession rebounds: the recovery after the COVID-19 pandemic from April to May 2020, the rebound after the global financial crisis from March to April 2009, and the repair rally following the first oil crisis from January to February 1975.

The fourth instance was January to February 1987, just months before the "Black Monday" crash in October of that year—a day when the S&P 500 plunged 20% in a single session.

Henry Allen emphasized that while the current rally has fundamental support, including enthusiasm for artificial intelligence and robust economic data, "the pace itself has broken all recent precedents." In an economy that has not emerged from a recession, such a rapid rebound has historically ended poorly.

Additionally, the S&P 500 is on track to achieve double-digit gains for the fourth consecutive year—a feat not seen since the late 1990s.

Excessive Optimism in Credit Markets, Consumer Pressure Signals Ignored

The strength in the stock market has also extended to the credit market. Credit spreads in both the U.S. and Europe are currently tighter than before the outbreak of the U.S.-Iran conflict, reflecting a high tolerance for risk in the market.

However, warning signs at the consumer level are accumulating. The U.S. savings rate in April was just 2.6%, a level historically seen only during two periods: a single month in 2022 (when excess savings accumulated during the COVID-19 pandemic were being depleted) and on the eve of the global financial crisis. At the same time, the University of Michigan Consumer Sentiment Index hit its lowest level on record in May, dating back to 1952.

The monetary policy environment is also tightening. The European Central Bank is widely expected to raise rates this month, and bets on a Fed rate hike in 2026 are intensifying—supported by the U.S. PCE inflation rate, which stood at 3.8% year-over-year in April.

Henry Allen noted that historically, a hawkish Fed stance has often coincided with widening credit spreads, as seen in 2022, late 2018, and 2015-16. The current calm in the credit market stands in stark contrast to this historical pattern.

Bond Markets Under Pressure Alone, Divergence from Stocks Continues to Widen

While stock and credit markets have shown a high degree of immunity to geopolitical risks, sovereign bond markets have taken a distinctly different path.

Over the past month, the yield on the 10-year U.S. Treasury note has almost perfectly tracked oil price movements, becoming clearly decoupled from trends in other asset classes. In mid-May, sovereign bond yields hit multi-year highs: the 30-year U.S. Treasury yield rose to 5.18%, its highest since 2007; the 10-year German Bund yield rose to 3.19%, its highest since 2011.

At that time, stocks were just a stone's throw away from their all-time highs, while bond yields were at levels not seen in over a decade. This divergence has shown no signs of narrowing.

Henry Allen believes that bond markets price inflation and fiscal risks more directly, making them more sensitive to geopolitical shocks. The persistent divergence between stocks and bonds is, in itself, a manifestation of the current market's fragility.

Oil Prices Surprisingly Stable, A Key Pillar for Risk Assets

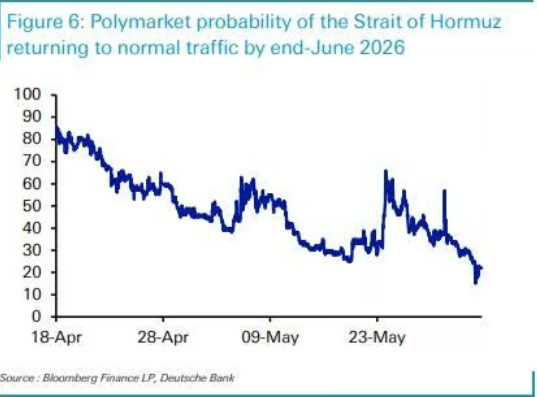

The blockade of the Strait of Hormuz has lasted far longer than initial market expectations, yet the oil price reaction has been surprisingly mild, partly explaining the resilience of risk assets.

When the U.S.-Iran conflict erupted on February 28, the White House initially estimated the operation would last 4 to 6 weeks. However, to date, the Strait of Hormuz remains blockaded. According to data from the prediction market Polymarket, the probability of normal navigation resuming by the end of June has plummeted from around 80% in mid-April to 22%.

Despite this, the oil futures curve has remained relatively stable. Just two weeks after the conflict erupted on March 13, the six-month Brent crude futures contract settled at $85.66 per barrel; by June 1, the contract was trading near $84.88, essentially unchanged.

Henry Allen pointed out that precisely because the oil futures curve has not shifted significantly higher, investors have not priced in severe stagflation risks, thus preventing a larger-scale sell-off in risk assets. However, he also warned that if the Strait of Hormuz remains blocked, it is uncertain whether this support can be maintained.