一年涨134%、市盈率75倍:市场为什么愿意为「零增长」的村田买单?

- 核心观点:村田制作所股价一年内上涨约134.9%,市盈率推高至约75倍,这并非基于当期平淡的业绩(利润近乎零增长),而是市场基于AI需求结构性扩张和公司独家定价权,对其未来利润爆发的预期下注。

- 关键要素:

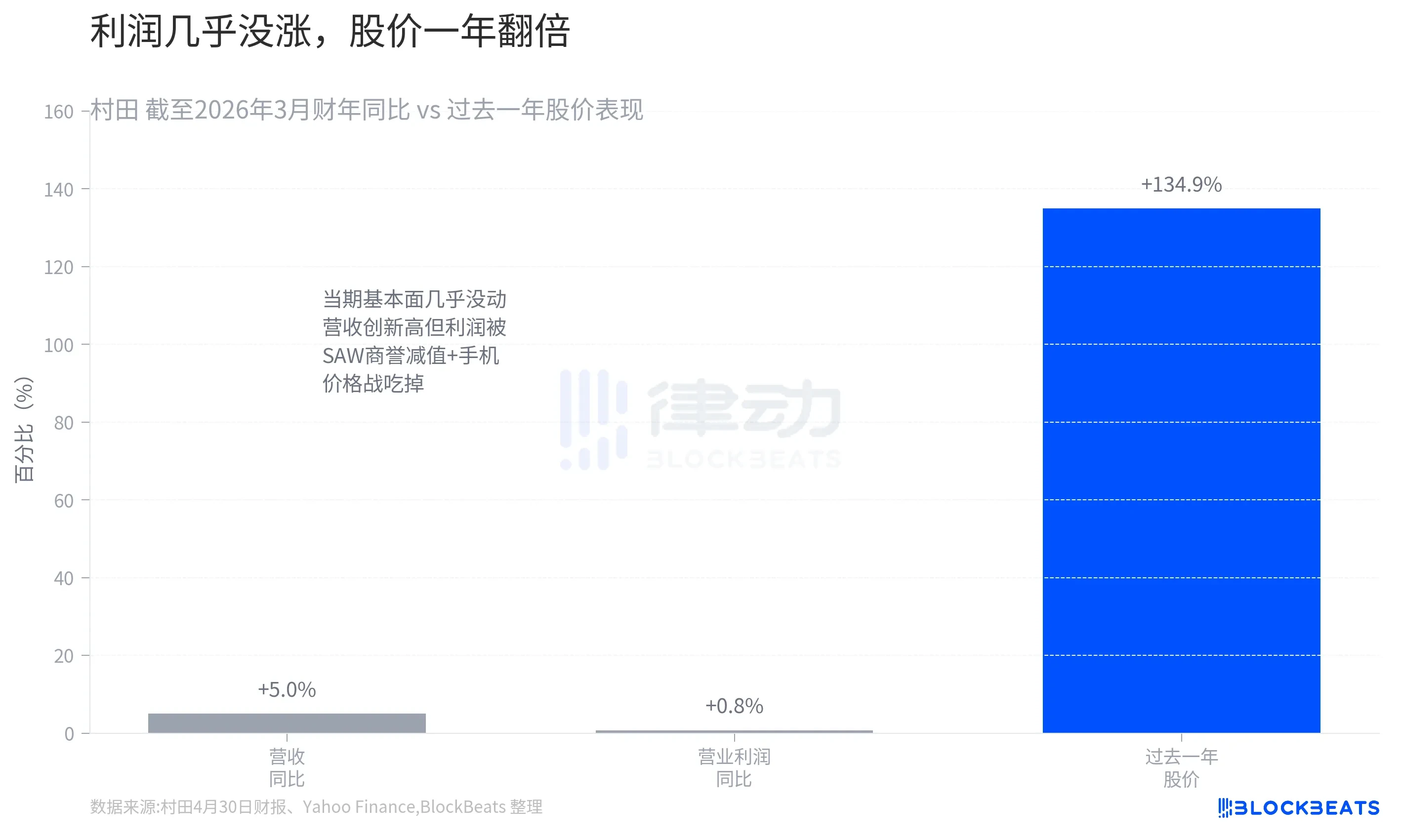

- 业绩与股价反差显著:村田2026财年营收创历史新高但仅增5%,营业利润几乎无增长,股价却在过去一年翻倍,表明市场在交易远期预期而非当期表现。

- 股价暴涨导火索:管理层在5月27日说明会上,将AI投资高峰预期延长至2030年,并透露客户“保量不保价”,需求约为产能两倍,直接引发次日股价大涨12%。

- 利润弹性来自指引柱:公司本财年(至2027年3月)营业利润指引为3800亿日元,同比大增34.8%,利润率修复至19.4%,市场交易的是这根尚未兑现的业绩柱子。

- AI营收占比将翻倍:AI/数据中心相关营收预计从约1700亿日元跳升至3250亿日元,占总营收比例从9%升至17%,成为近五分之一的支柱业务。

- 结构性定价权支撑高估值:AI营收增长并非简单提价,而是源于公司更高端MLCC产品结构升级,其份额超70%,这种“只有我能做所以贵”的可持续定价权被市场认可。

- 高位风险不容忽视:管理层也承认部分客户需求预测可能偏高,一旦AI投资放缓或指引不及预期,75倍的高估值将面临快速回落的风险。

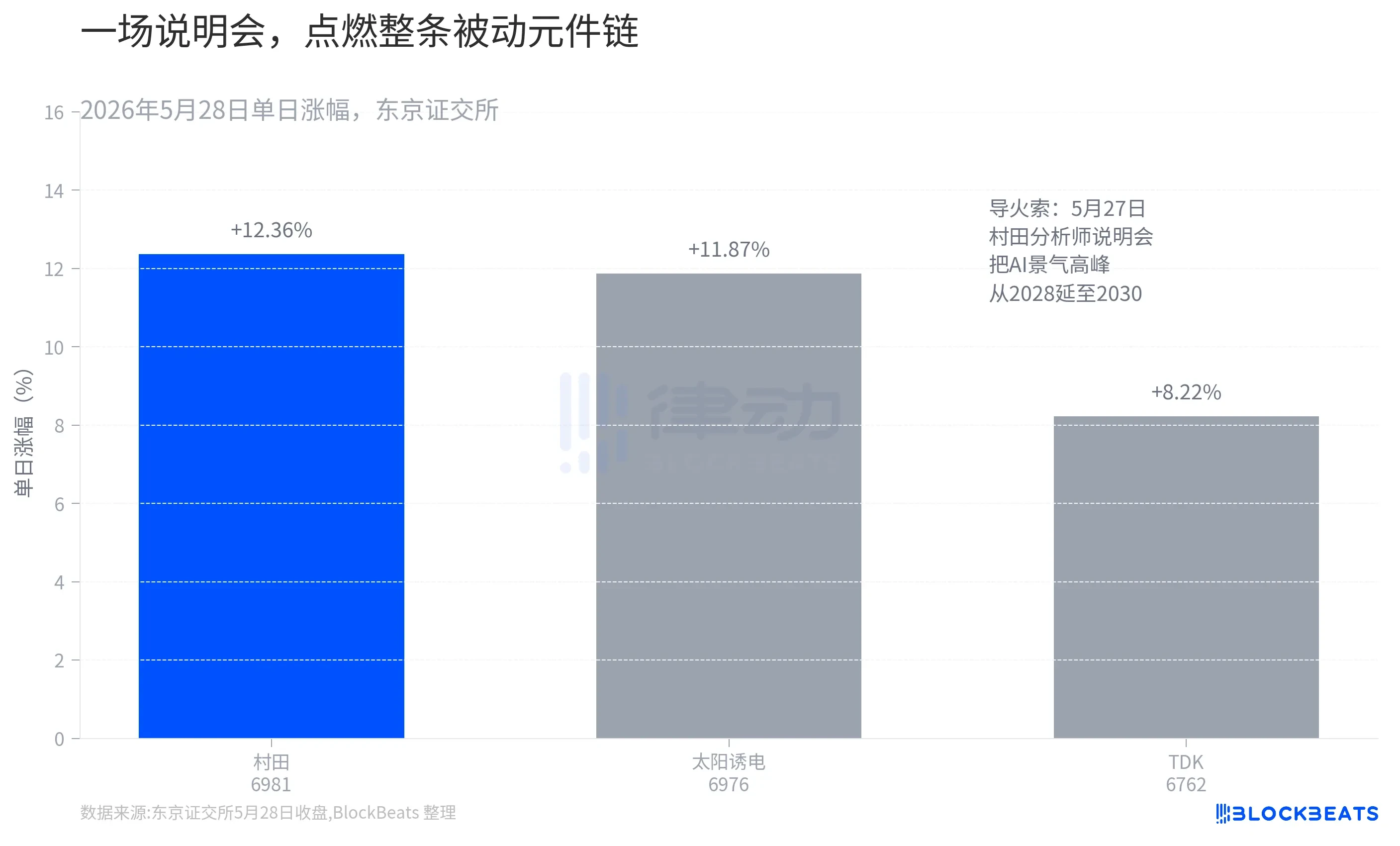

On May 28, Murata Manufacturing, the world's largest passive component manufacturer, surged 12.36% on the Tokyo Stock Exchange, hitting its daily limit at one point before closing at 8,787 yen, a record high on an adjusted basis. Two months ago, we analyzed an article about Murata raising prices for AI server MLCCs (multilayer ceramic capacitors) by 15-35%, discussing how these sub-millimeter capacitors are disrupting the AI computing supply chain. This time, what's worth analyzing isn't the capacitor, but the Murata stock itself.

Because if you look at Murata's just-released financial report, you'll find a contrast: the performance is actually quite mediocre, yet the stock price has already doubled in a year.

According to Murata's financial report on April 30, for the fiscal year ending March 2026, the company's revenue was 1.83 trillion yen, a record high, but only up 5.0% year-on-year. Operating profit was 281.8 billion yen, up only 0.8% year-on-year, essentially flat. Two factors dragged down profits: first, an impairment loss on goodwill related to the Surface Acoustic Wave (SAW) filter business, and second, ongoing price wars in mature applications like smartphones. In other words, no matter how impressive the AI line is, it only serves to offset the losses from the mature businesses.

Yet, in the same time frame, Murata's stock price has risen approximately 134.9% over the past year (according to Yahoo Finance data), with the latest share price above the 9,000-yen mark, pushing the market cap to around 17 trillion yen and the P/E ratio to about 75 times. A company that makes passive components with zero profit growth in the current period is being priced by the market at a 75x P/E ratio. This can only mean one thing: buyers don't care about this year's profits at all; they are betting on the story ahead.

The Real Trigger: A Briefing Session

The trigger for this surge wasn't a price hike or a financial report, but a small meeting held by Murata for securities analysts on May 27.

According to investment blogger kabuya66, citing content from the meeting, Murata's management made two key statements. The first was revising the expected peak for AI investment from the previously anticipated "around 2028" to "will continue until around 2030." For a capital-intensive component manufacturer operating on an order basis, an additional two years in the boom cycle means that order backlogs will continue to accumulate, and the return on investment for capacity expansion becomes more certain. The second statement was more direct: customers are now "prioritizing volume over price," with demand being roughly double the production capacity. This means downstream buyers are scrambling to secure supply, caring less about price and only about getting the quantities they need.

The impact of these two statements was evident in the next day's trading. While Murata surged 12.36% in a single day, peers like Taiyo Yuden rose 11.87% and TDK gained 8.22% (according to Tokyo Stock Exchange closing data). A briefing from the industry leader revalued not just one stock, but the entire passive component supply chain. On the same day, the Nikkei 225 index closed above 66,000 points for the first time, with the MLCC sector being one of the leading contributors to the rally.

What the Market is Buying: The "Next Year's" Pillar

The reason the briefing ignited the market was that it clarified Murata's profit elasticity for the coming year.

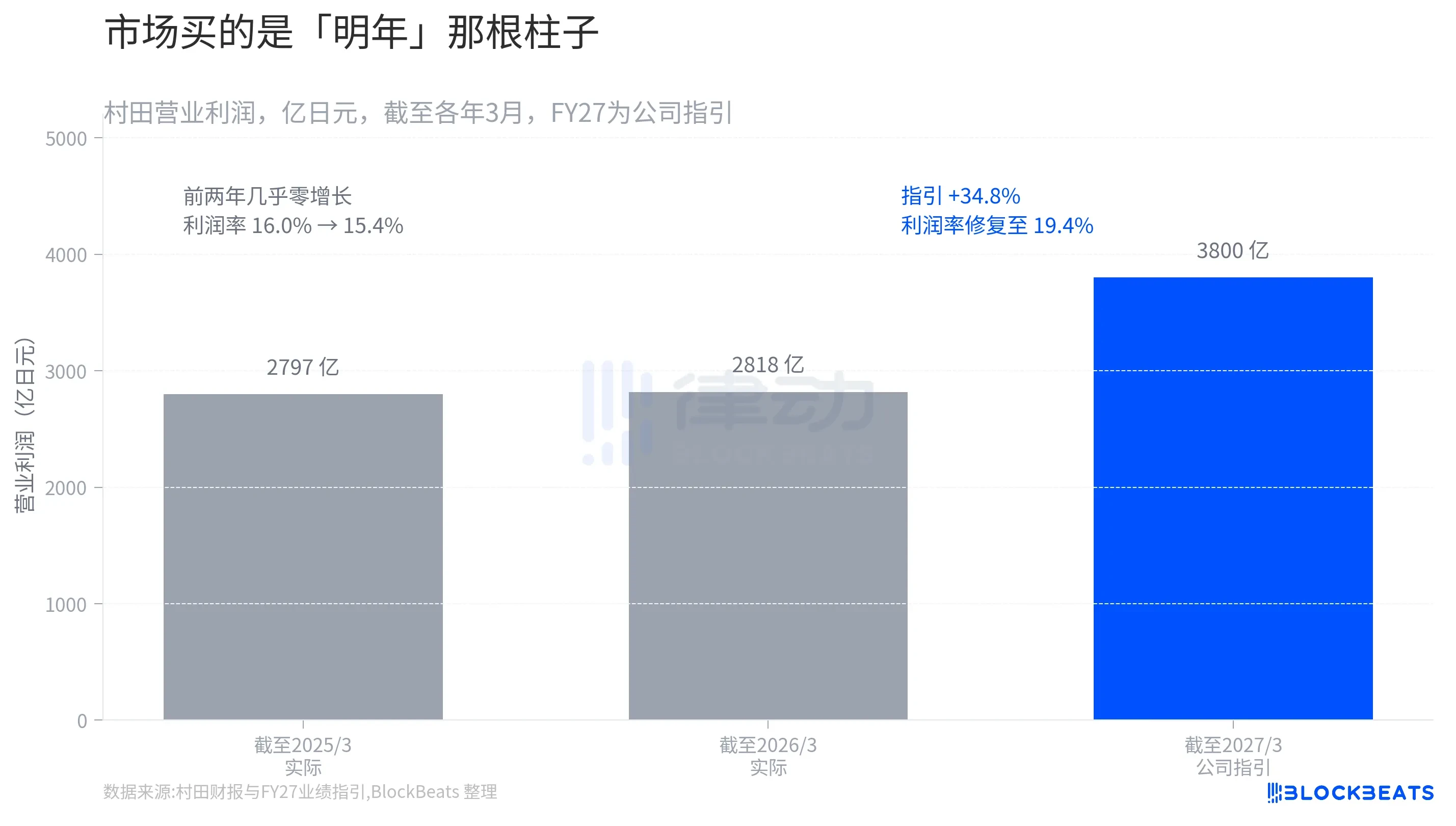

If you illustrate Murata's operating profit as three pillars, the story becomes clear. In the fiscal year ending March 2025, it was 279.7 billion yen; in the fiscal year ending March 2026, it was 281.8 billion yen, essentially zero growth for two consecutive years, with the profit margin slipping from 16.0% to 15.4%. However, Murata's guidance for the current fiscal year (ending March 2027) projects an operating profit of 380 billion yen, a sharp increase of 34.8% year-on-year, with the profit margin recovering to 19.4%.

All the growth is locked into that pillar on the far right. What the market is buying now is not the past two years of flat performance, but this yet-to-be-realized guidance pillar. A supporting piece of evidence is order backlog. According to a survey by Nikkei Veritas, among listed companies with a market cap over 50 billion yen expected to be profitable this fiscal year, Murata ranked first in the growth rate of its order backlog from the previous fiscal year. An order backlog directly translates into future revenue, providing the confidence to support that guidance pillar. Murata also casually announced a buyback plan of up to 150 billion yen, planning to repurchase 75 million shares, or 4.12% of its outstanding shares. By putting its own money on the line, management is essentially acknowledging that the current price isn't expensive.

Supporting This Pillar: AI Revenue Needs to Double Again

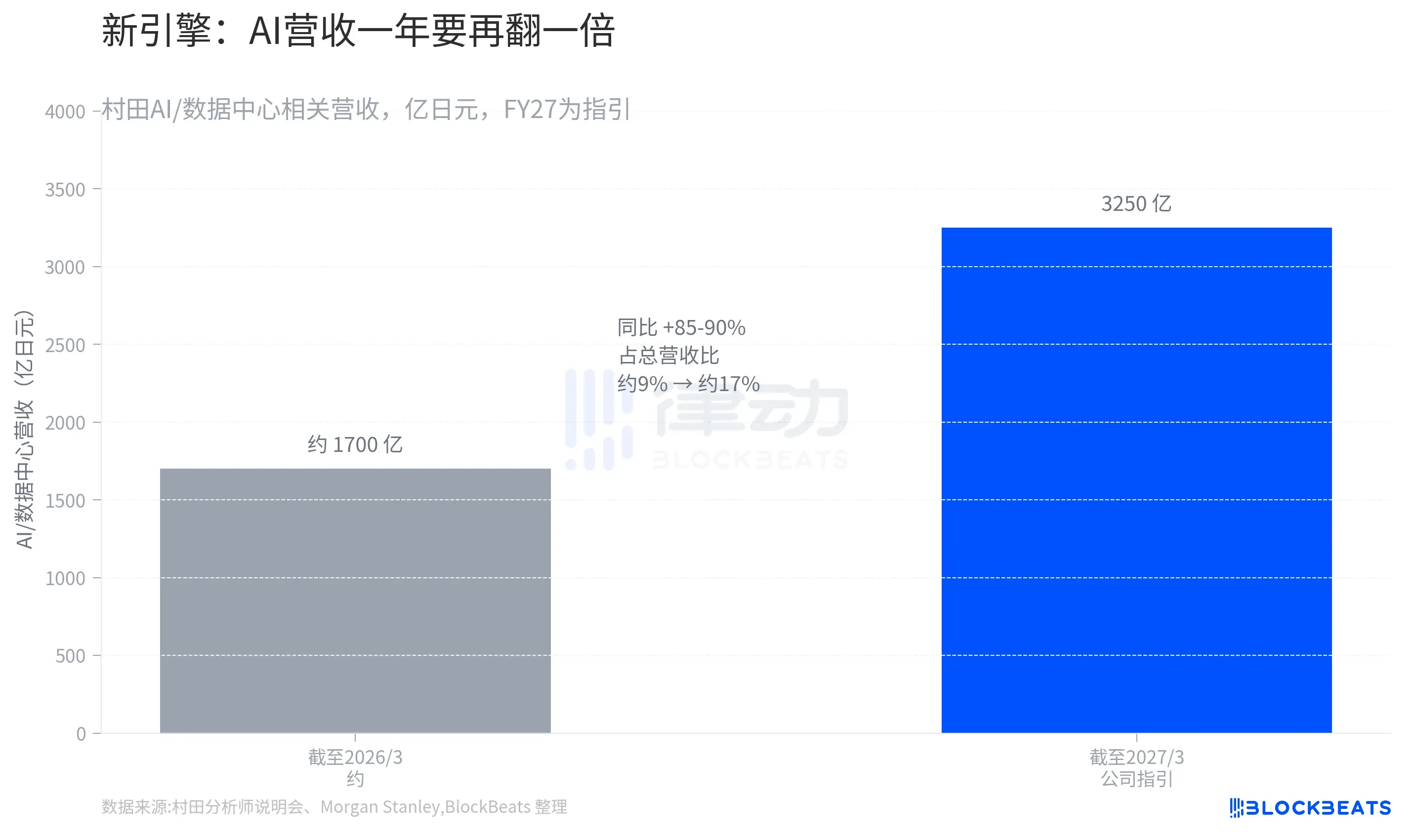

Where is that 34.8% profit growth coming from? The answer lies in one line of business.

According to data from Murata's briefing, the company's AI/data center-related revenue is expected to jump from approximately 170 billion yen in the previous fiscal year to a guidance of 325 billion yen for the current fiscal year, representing an 85-90% year-on-year increase. This line's share of total revenue will rise from about 9% to roughly 17%. In other words, within a span of one year, AI will go from being a fraction of Murata's revenue to a pillar accounting for nearly one-fifth of it.

More crucial is the "quality" of this growth. According to analysis by Morgan Stanley MUFG Securities, Murata's current round of AI revenue growth isn't driven by price increases on existing MLCC products but by an upgrade in product mix. A higher proportion of advanced products with smaller sizes and higher capacitance values is pushing up the average selling price (ASP). Murata holds over a 70% share of the cutting-edge MLCCs required for AI servers, with almost no competitor able to keep up. This means its price increases are not cyclical ("prices rise because of supply shortages") but structural ("expensive because only we can make it"). The market is willing to pay a 75x P/E ratio precisely to price this perceived sustainable pricing power.

Of course, the other side of buying expectations to record highs is that expectations have gotten ahead of themselves. Murata's President Norio Nakajima himself admitted that it's possible some customers' demand forecasts are "somewhat inflated." Should the pace of AI investment slow down or subsequent quarterly guidance fall short of expectations, such high valuations also carry the risk of a rapid correction. For high-valuation stocks, "not good enough" is the best reason to sell.

Murata is still the capacitor maker it always was. What has changed is the ruler the market has decided to use to measure it: from a cyclical component manufacturer "doomed to price cuts" to a "supply-constrained AI picks-and-shovels seller with pricing power."