แน่นอนครับ/ค่ะ นี่คือผลลัพธ์การแปลตามข้อกำหนดที่ได้รับ: NVIDIA รายงานผลประกอบการนับถอยหลัง: การทำผลงานเกินคาดแทบไม่มี悬念 แต่วอลล์สตรีทกังวลห้าประเด็นนี้มากที่สุด

- มุมมองหลัก: นักวิเคราะห์ของ BofA เชื่อว่ารายงานผลประกอบการไตรมาสแรกของ NVIDIA ที่ "ทำผลงานเกินคาด" แทบจะไม่ใช่เรื่องน่าแปลกใจอีกต่อไป โดยตลาดจะหันไปให้ความสนใจกับประเด็นสำคัญ 5 ข้อ ได้แก่ ผลตอบแทนแก่ผู้ถือหุ้น ความคืบหน้าของชิปเจนเนอเรชั่นถัดไป Vera Rubin แนวโน้มอัตรากำไรขั้นต้น และการอัปเดตขนาดตลาด AI โดยผลตอบแทนแก่ผู้ถือหุ้นที่ต่ำกว่าเมื่อเทียบกับบริษัทในกลุ่มเดียวกันอย่างมีนัยสำคัญ นับเป็นสาเหตุหลักที่ทำให้บริษัทมีส่วนลดมูลค่ากิจการในระยะยาว

- ปัจจัยสำคัญ:

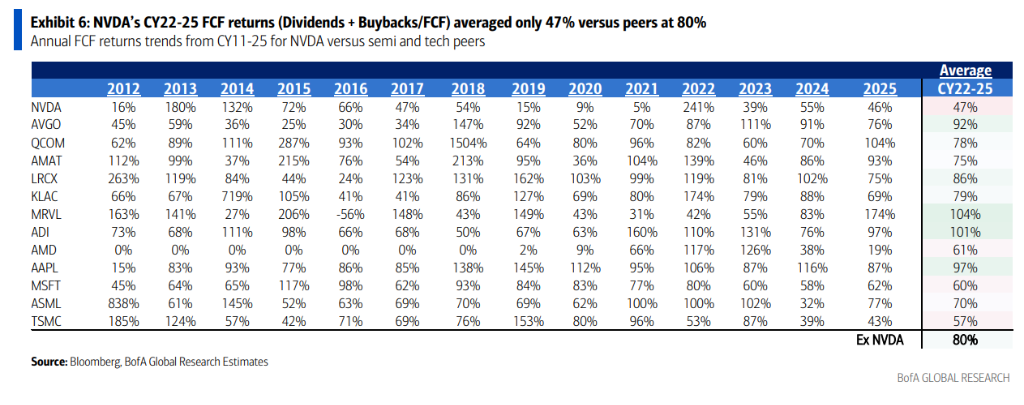

- ผลตอบแทนแก่ผู้ถือหุ้น: อัตราผลตอบแทนจากกระแสเงินสดอิสระ (FCF yield) โดยเฉลี่ยของ NVIDIA ในช่วงปี 2022-2025 อยู่ที่เพียง 47% ซึ่งต่ำกว่าค่าเฉลี่ยอุตสาหกรรมที่ 80% มาก อัตราผลตอบแทนจากเงินปันผล (Dividend yield) อยู่ที่ 0.02% ซึ่งต่ำกว่าค่าเฉลี่ยของคู่แข่งที่ 0.89% ส่งผลให้ถึงแม้จะเป็นบริษัทที่มีมูลค่าตลาดใหญ่ที่สุดในดัชนี S&P 500 แต่กลับต้องเผชิญกับส่วนลดมูลค่ากิจการเกือบ 50%

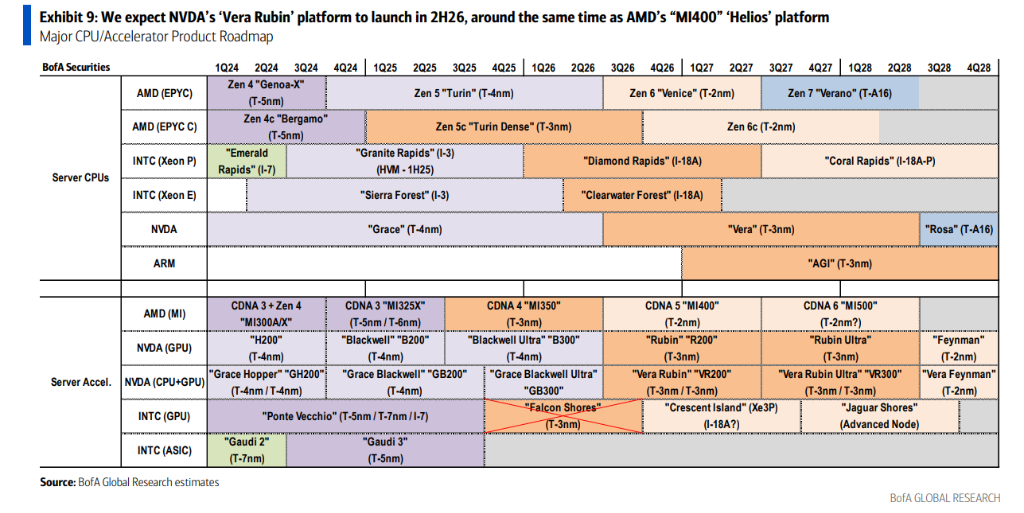

- ชิปเจนเนอเรชั่นถัดไป Vera Rubin: คาดว่าจะเริ่มผลิตจำนวนมากในช่วงครึ่งหลังของปี 2026 โดยใช้เทคโนโลยีกระบวนการ 3 นาโนเมตรของ TSMC ส่วน Vera Rubin Ultra จะเปิดตัวในช่วงครึ่งหลังของปี 2027 พร้อมกับสถาปัตยกรรมแร็คแบบใหม่ทั้งหมด

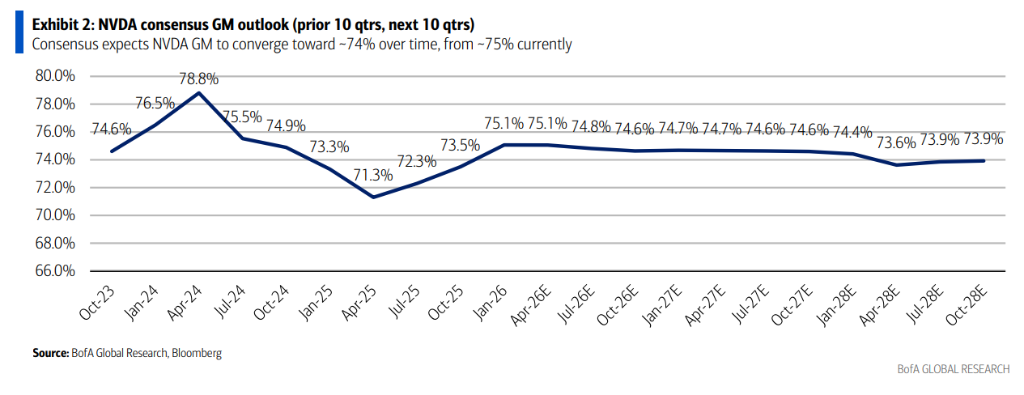

- การสนับสนุนอัตรากำไรขั้นต้น: ความเห็นพ้องต้องกันของตลาดคืออัตรากำไรขั้นต้นจะผันผวนอยู่ในช่วง 74% - 75% ในระยะสั้น เนื่องจากเป็นช่วงเปลี่ยนผ่านของผลิตภัณฑ์ที่ราบรื่น อัตรากำไรขั้นต้นจึงค่อนข้างคงที่ แต่ในระยะกลางถึงยาวจะเผชิญกับแรงกดดันจากต้นทุนหน่วยความจำแบนด์วิดท์สูง (HBM) ที่เพิ่มสูงขึ้น

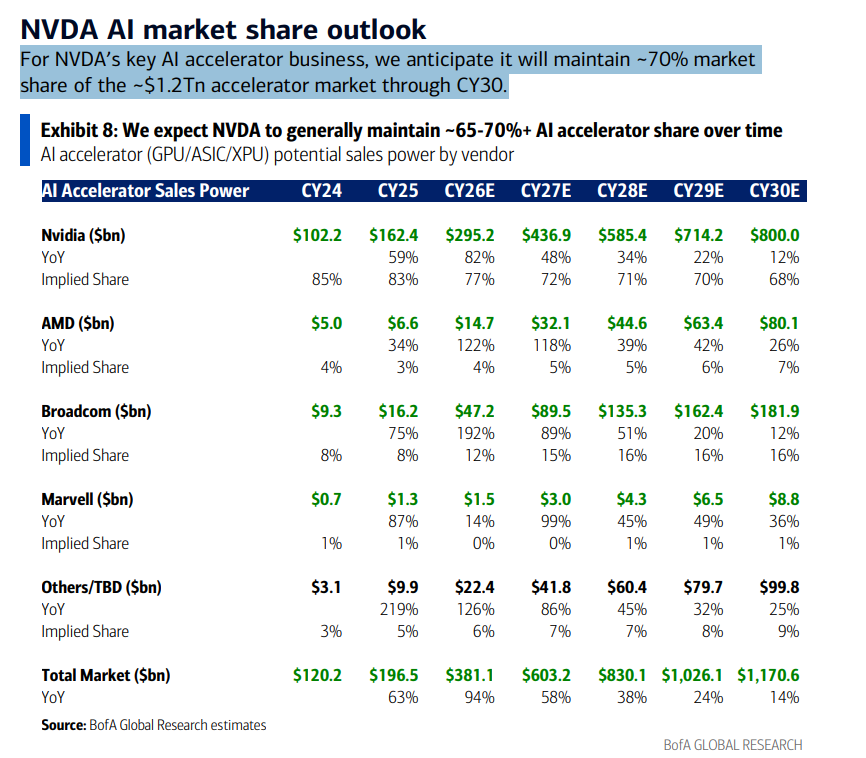

- การคาดการณ์ตลาด AI: BofA คาดการณ์ว่าขนาดตลาดตัวเร่งความเร็ว AI (AI Accelerator) จะอยู่ที่ประมาณ 1.17 ล้านล้านดอลลาร์สหรัฐภายในปี 2030 โดย NVIDIA จะรักษาส่วนแบ่งการตลาดไว้ได้ 68% - 70% และรายได้จะเพิ่มขึ้นจาก 102,200 ล้านดอลลาร์สหรัฐในปี 2024 เป็น 800,000 ล้านดอลลาร์สหรัฐในปี 2030

- การประเมินภัยคุกคามจากการแข่งขัน: กระแสที่ว่า CPU มีความสำคัญมากกว่า GPU นั้นถูกพูดเกินจริงไป ในการใช้งานจริง อัตราส่วนการติดตั้ง CPU ต่อ GPU อยู่ที่ 1:2 นอกจากนี้ NVIDIA จะเปิดเผยความคืบหน้าใหม่ของ CPU Vera ที่พัฒนาเอง ซึ่งตำแหน่งผู้นำในแวดวง AI ของบริษัทนั้นยากที่จะถูกโค่นล้มในระยะสั้น

Original Author: Long Yue

Original Source: Wall Street CN

In this Nvidia earnings season, the numbers themselves are no longer the most important thing.

On May 18, BofA Securities analyst Vivek Arya and his team released a preview report on Nvidia's Q1 earnings, which will be announced after the market close on Wednesday, May 20, Eastern Time.

According to historical patterns over the past ten quarters, Nvidia's actual revenue has, on average, exceeded management's guidance by 7% to 8%. Management previously provided F1Q27 revenue guidance of $78 billion. Based on this, actual revenue is likely to fall within the $83 billion to $84 billion range, while the current market consensus is only $78.7 billion.

In other words, "beating expectations" is almost a certainty. However, analysts believe the following five issues will be the real market movers after the earnings release.

Cash Returns: Can Nvidia's "Stinginess" Change?

This is the most extensively discussed topic in the report and the core reason they believe Nvidia has traded at a long-term valuation discount.

Nvidia is currently the largest company in the S&P 500 by market capitalization, accounting for a hefty 8.3% of the index weight, surpassing the historical peaks of both Apple (7.9%) and Microsoft (7.2%). However, the problem lies in the fact that Nvidia's shareholder returns are severely mismatched with its size.

The data is stark: From 2022 to 2025, Nvidia's average free cash flow yield (dividends + buybacks) was only 47%, compared to an industry average of 80% for similar companies. Even Nvidia's own average over the earlier decade was 80%.

Simultaneously, Nvidia's current dividend yield is a mere 0.02%, while the peer average is 0.89%. In equity income funds, Nvidia is held by only 16% of funds, whereas Microsoft is held by 57% and Apple by 32%.

Where is the money going? The analysts point out that Nvidia has invested heavily in its ecosystem – OpenAI, Anthropic, and technology partners. These investments are viewed controversially by some, with voices suggesting it's "circular financing," where Nvidia lends money to customers, who then use it to buy Nvidia's chips.

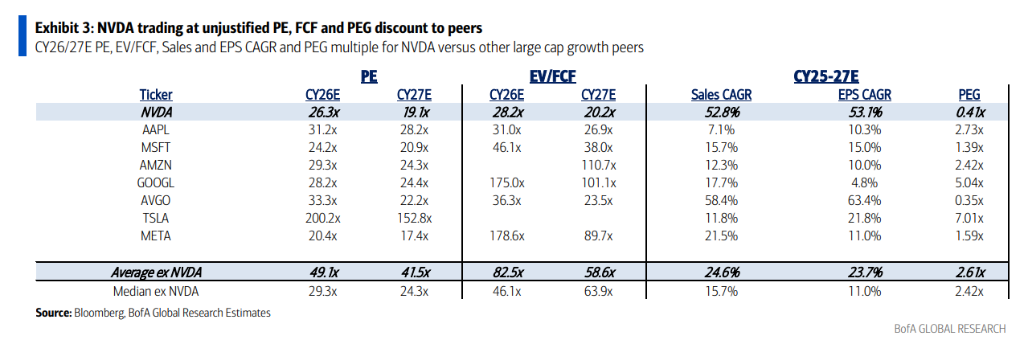

How significant is the valuation discount? Data shows Nvidia's P/E ratios for CY26/CY27 are 26x/19x, while the average for the other 'Magnificent Seven' members is 49x/42x, a discount of nearly 50%.

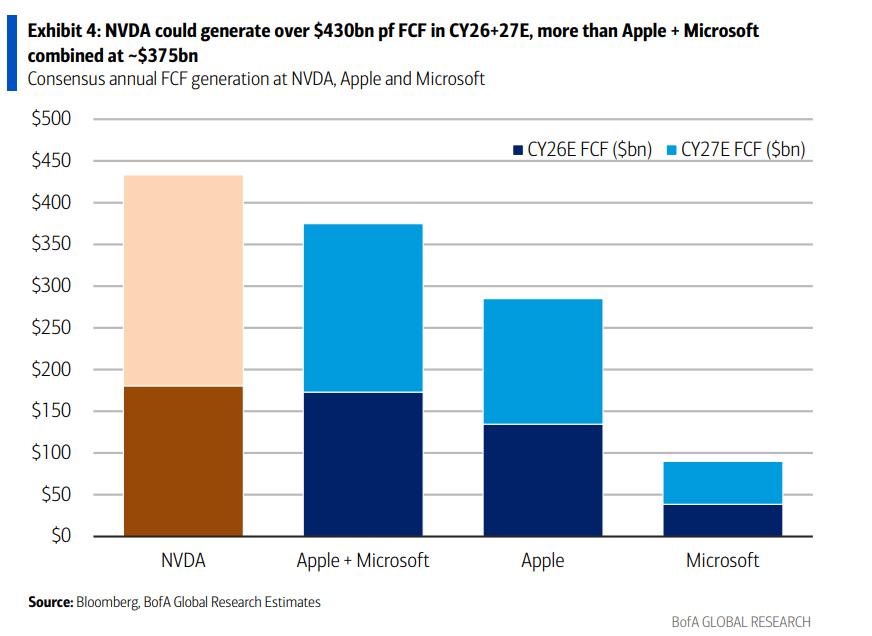

In a more specific comparison: Analysts forecast Nvidia's combined free cash flow for 2026 and 2027 will exceed $430 billion, higher than the combined total of Apple and Microsoft at approximately $375 billion. Yet, Nvidia's market cap of ~$5.46 trillion is about 28% lower than the $7.5 trillion combined market cap of Apple and Microsoft.

Analysts believe that if Nvidia increases its dividends and buybacks, it could attract more yield-focused long-term capital, narrow the valuation discount, and alleviate concerns about "circular financing." They label this change as a "potential catalyst for the second half of the year."

Vera Rubin: When Will the Next-Gen Chip Arrive?

Nvidia's current flagship product is the Blackwell series. The market wants to know: When will the next-generation Vera Rubin platform officially ramp up in volume?

The bank's judgment is the second half of 2026. Vera Rubin (codenamed R200) uses TSMC's 3nm process and shares the "Oberon" rack architecture with Blackwell Ultra, making the product transition relatively smooth, with limited expected impact on gross margins.

Looking further ahead, Vera Rubin Ultra (codenamed VR300) is expected to launch in the second half of 2027. It will feature a new "Kyber" rack architecture, and High Bandwidth Memory (HBM) will account for a larger share of costs.

The market also wants to hear Nvidia's latest stance on the "trillion-dollar revenue forecast" during the earnings call – Nvidia previously provided an outlook of $1 trillion in cumulative revenue from 2025 to 2027, but contributions from LPU racks, CPUs, and Vera Rubin Ultra were not yet included. Will this be updated this time?

Gross Margin: Can the 75% Defense Line Hold?

Gross margin is one of the core pillars supporting Nvidia's valuation.

The analysts' judgment: In the short term, as Vera Rubin reuses Blackwell's rack architecture, gross margins during the product transition should be relatively stable. However, in the medium to long term, the rising cost share of HBM memory is a continuous source of pressure.

Market consensus suggests Nvidia's gross margin will fluctuate within the 74% to 75% range. The bank has no issue with this but emphasizes that any gross margin performance exceeding expectations would be a positive catalyst.

Will the AI Accelerator Market Size Forecast Be Updated?

BofA previously provided a "trillion dollar" forecasting framework for Nvidia's AI market from 2025 to 2027. This earnings season, the market is watching to see if Nvidia will update this forecast, especially by incorporating three previously unaccounted growth drivers:

- LPU (Language Processing Unit) Racks

- Vera CPU (Nvidia's self-developed server CPU)

- Vera Rubin Ultra

The bank expects that by 2030, the total AI accelerator market will reach approximately $1.17 trillion, with Nvidia maintaining roughly 68% to 70% market share.

Specifically, Nvidia's AI accelerator revenue is projected to grow from $102.2 billion in 2024 to $800 billion in 2030. During the same period, AMD is expected to grow from $5 billion to $80.1 billion, and Broadcom from $9.3 billion to $181.9 billion.

Is the Competitive Threat from Google TPUs and CPUs Exaggerated?

A recent narrative circulating in the market suggests that as AI enters the "Agentic AI" era, the importance of CPUs will surpass that of GPUs, thereby threatening Nvidia's moat.

The bank explicitly disagrees with this view, providing two reasons:

First, Nvidia's self-developed "Vera CPU" will see new developments disclosed at the upcoming Computex conference, and its competitiveness in the standalone CPU market should not be underestimated.

Second, in the currently deployed large-scale Blackwell and TPU clusters, the ratio of CPUs to GPUs is already 1:2. This does not align with the narrative that "Agentic AI requires more CPUs."

The conclusion: While the CPU market is large, it is highly competitive (with strong rivals in both x86 and ARM architectures). Nvidia's dominant position in the GPU/AI accelerator market is unlikely to be challenged in the short term. It is projected that by 2030, Nvidia will maintain roughly 70% revenue share within a total AI addressable market exceeding $1.7 trillion.

Valuation: The 'Tech Leader' at a 50% Discount

Finally, back to valuation. The report uses a set of data to directly highlight Nvidia's current valuation paradox.

Based on CY26/27 expected P/E ratios, Nvidia trades at 26x/19x, while the average for the 'Magnificent Seven' (Mag-7) is 49x/42x – a discount of nearly 50% for Nvidia.

Based on EV/FCF (Enterprise Value / Free Cash Flow), Nvidia is at 28x/20x, compared to the Mag-7 average of 83x/59x – a discount exceeding 66%.

Based on PEG (Price/Earnings to Growth) ratio, Nvidia is at 0.41x, the Mag-7 average is 2.61x, and the S&P 500 overall is above 1.3x.

BofA maintains a "Buy" rating with a price target of $320, based on a CY27 expected P/E ratio of 28x (excluding cash), which is at the mid-to-low end of Nvidia's historical valuation range of 25x to 56x.