NEAR Protocol: Is It Time to Buy the Dip?

- Core Thesis: NEAR Protocol is being undervalued by the market as a mid-tier L1, but has evolved into a "cross-chain execution layer" with both privacy and AI narratives. Its core fee engine (NEAR Intents) generates 18 times more revenue than LayerZero, yet its valuation multiple is only one-third of ZRO's, presenting an investment opportunity combining "grand narrative" with "hard data".

- Key Elements:

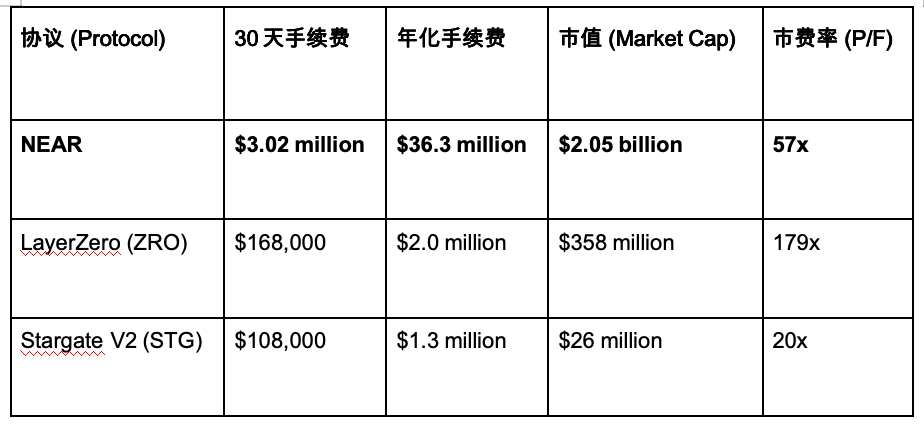

- NEAR's annualized P/F ratio is approximately 56x. After accounting for base layer gas fees and Intents fees, its valuation is cheaper than Ethereum, Solana, and most major L1s.

- NEAR Intents generates 18 times more 30-day fees than LayerZero, yet the valuation multiple of the ZRO token is over 3 times that of NEAR, indicating a market perception disconnect.

- Co-founder Illia Polosukhin is a co-author of "Attention Is All You Need," giving NEAR a technically authentic and legitimate foundation in the AI narrative.

- The privacy sector benefits from capital inflows into Zcash (ZEC). NEAR, via Intents as an execution layer, supports seamless swapping of ZEC for USDC, capturing fees generated by privacy applications.

- Tokenomics are improving: the inflation rate has been cut to 2.5%, and transaction fees are actively burned from the supply, pushing NEAR towards becoming a cash-flow-generating execution layer asset.

- Key risk: Total Intents fees are approximately $149,000 per month, which has not yet been fully converted into protocol revenue. Without a buyback or dividend mechanism, the market might prematurely price in both major call options.

- Arthur Hayes lists NEAR as a heavily weighted altcoin, with the core logic being that "privacy applications running on Intents" can create a positive cash flow model for the protocol.

NEAR Protocol: Is It Time to Buy the Dip?

NEAR is back on everyone's radar for three reasons:

1. Real Demand Driven by NEAR Intents

2. Privacy Sector Upside from Zcash Capital Inflows

3. AI Narrative Led by the Founder Himself

The clearest valuation logic is no longer just that "NEAR is cheaper than cross-chain bridges like LayerZero." If you factor the fees from NEAR Intents into the model, NEAR's annualized price-to-fee (P/F) multiple is only about 56x. Under the same valuation framework, it is cheaper than Ethereum, Solana, Aptos, Sui, Avalanche, and Injective.

The market is still pricing NEAR as a mid-tier L1, but NEAR is actually beginning to demonstrate the strength of a "cross-chain execution layer" with explosive potential in privacy and AI.

Core Summary

● NEAR is showing an attractive risk-reward ratio: on one hand, a real fee engine driven by NEAR Intents; on the other, "call options" from the grand narratives of privacy and AI.

● The OG Arthur Hayes has anointed NEAR as his next most favored altcoin, emphasizing its powerful combination of "privacy + positive cash flow potential."

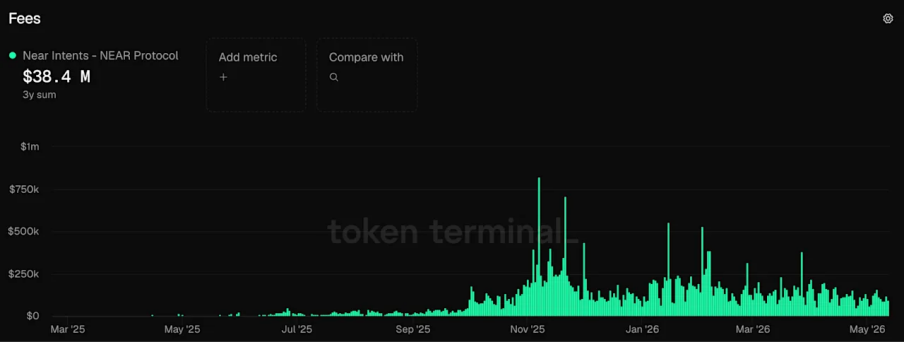

● The 30-day fees generated by NEAR Intents are roughly 18 times those of LayerZero, yet NEAR's valuation multiple is just a fraction of ZRO's.

● Tokenomics is improving. The inflation rate was recently slashed to 2.5%, and transaction fees actively burn the token supply, pushing NEAR towards becoming an execution layer asset with cash flow.

● Combining base layer gas fees and Intents fees, NEAR's annualized price-to-fee (P/F) ratio is only 56x, cheaper than Ethereum, Solana, and most major L1s. This valuation is highly enticing.

Current State of NEAR

NEAR is far from the outdated L1 public chain it once was. It is evolving into a cross-chain execution layer backed by the dual narratives of privacy and AI.

The value of the privacy sector has been validated by Zcash (ZEC). While NEAR doesn't directly compete with privacy coins, it benefits directly by serving as the "execution layer" catering to these tokens' privacy needs. A prime example is Zodl (formerly Zashi), the Zcash network wallet. Users can buy Zcash directly with Zodl without KYC and seamlessly use ZEC for payments. In payment scenarios, Near Intents can also help seamlessly convert Zcash into other tokens like USDC, facilitating trading while protecting privacy. Users simply "express" their desired outcome (intent), and solvers compete fiercely in the background to execute it.

AI is the second call option. Compared to most AI-themed air coins on the market, NEAR's credentials in this area are legitimate. NEAR co-founder Illia Polosukhin is a co-author of the foundational modern LLM paper, "Attention Is All You Need" (the Transformer paper). Furthermore, NEAR was an AI company before it pivoted to Web3.

The core question now is: Can AI actually generate real fees? NEAR AI is paving the way through AI Cloud, IronClaw, Agent Market, and Intents. Future AI agents will absolutely not manually cross chains, calculate gas fees, or compare transaction routes. They will only output results directly. NEAR Intents is built for this future AI world.

Why Must Altcoin OGs Pay Attention?

Arthur Hayes gave NEAR trading value again. In his essay "The Butterfly Touch," he argues the next crypto bull run will be liquidity-driven, linked to AI capex, war spending, infrastructure spending, and credit easing. Following HYPE and ZEC, he has listed NEAR as his next most favored altcoin for heavy investment.

The key is the underlying logic. His bullish thesis isn't solely about AI; he believes "privacy applications running on NEAR Intents" can create a positive cash flow model for the NEAR protocol. This is crucial because the best altcoin trades require both a "grand narrative" and "hard data support." Currently, NEAR possesses both.

On-Chain Signals: Where is the Market's Perception Gap?

The market is still fixated on old topics like LayerZero, Stargate, CCIP migration, and cross-chain bridge security, but current on-chain fee data points to a completely different profit direction.

The 30-day fees generated by NEAR Intents are roughly 18 times those of LayerZero, yet NEAR's valuation multiple is less than one-third of ZRO's. This is the market's first cognitive dissonance.

However, there is a critical risk to note (Caveat): "Total fees" from Intents do not equal "real revenue for token holders." The actual protocol revenue captured is still quite small, only about $149,000 in the past 30 days. Therefore, whether this long thesis ultimately succeeds depends on NEAR's ability to convert ecosystem activity into more revenue capture, token buybacks, burning, staking locks, or other value-accrual mechanisms.

Why is the Valuation Rerate Still in Progress?

If you only look at the gas fees of the underlying public chain, NEAR doesn't seem cheap at all. But this completely misses the point. The core logic for trading NEAR currently is "base layer activity + NEAR Intents," and the latter has begun generating significant cross-chain execution tolls.

This is the most powerful relative valuation logic. NEAR is still being mispriced like a mid-tier L1, but if Intents is considered a core part of NEAR's economic stack, its valuation is more akin to a "cross-chain execution company" with real revenue.

Risk Warning: What Pitfalls to Avoid?

For non-pure degens, this trade isn't as straightforward as buying HYPE. The biggest risk is that the market may have already priced in the value of these two "call options" before the token captures sufficient economic value. Although NEAR's valuation multiple is already low compared to other L1s, it may still be considered high by traditional institutional investors.

The most perfect confirmation signal for going long is: sustained strength in NEAR Intents fee revenue, and seeing substantial buybacks or real revenue distribution on NEAR's revenue dashboard—though this hasn't started yet.

Note: If NEAR pumps solely due to Arthur Hayes' call or AI/privacy sector headlines, but its Intents fees and actual AI product progress remain lackluster, we will choose to sell into strength (Fade it).

Final Take

In summary, NEAR currently holds a severely undervalued fee engine by the market, along with two powerful "call options" in privacy and AI.

The valuation model is key. Combining base layer and Intents fees, NEAR's annualized fee multiple is only around 56x. This is not only cheaper than mainstream L1s but also significantly better valued than LayerZero (ZRO) within the cross-chain bridge sector. While Arthur's recent blog post has brought massive attention, the hard on-chain data is what can truly sustain this trade.

Trading Suggestion: If we see NEAR launching new AI features, continued fee surges, and stronger protocol revenue capture mechanisms constantly validating this narrative, then decisively go Long (Long) NEAR.