美股芯片股,距熊市仅一步之遥

- 核心观点:芯片股引领的AI交易正快速降温,费城半导体指数逼近技术性熊市。市场关注焦点已从AI投入规模转向商业化回报,资金从高估值芯片板块流向金融、消费等经济敏感板块,等待财报验证AI投资逻辑。

- 关键要素:

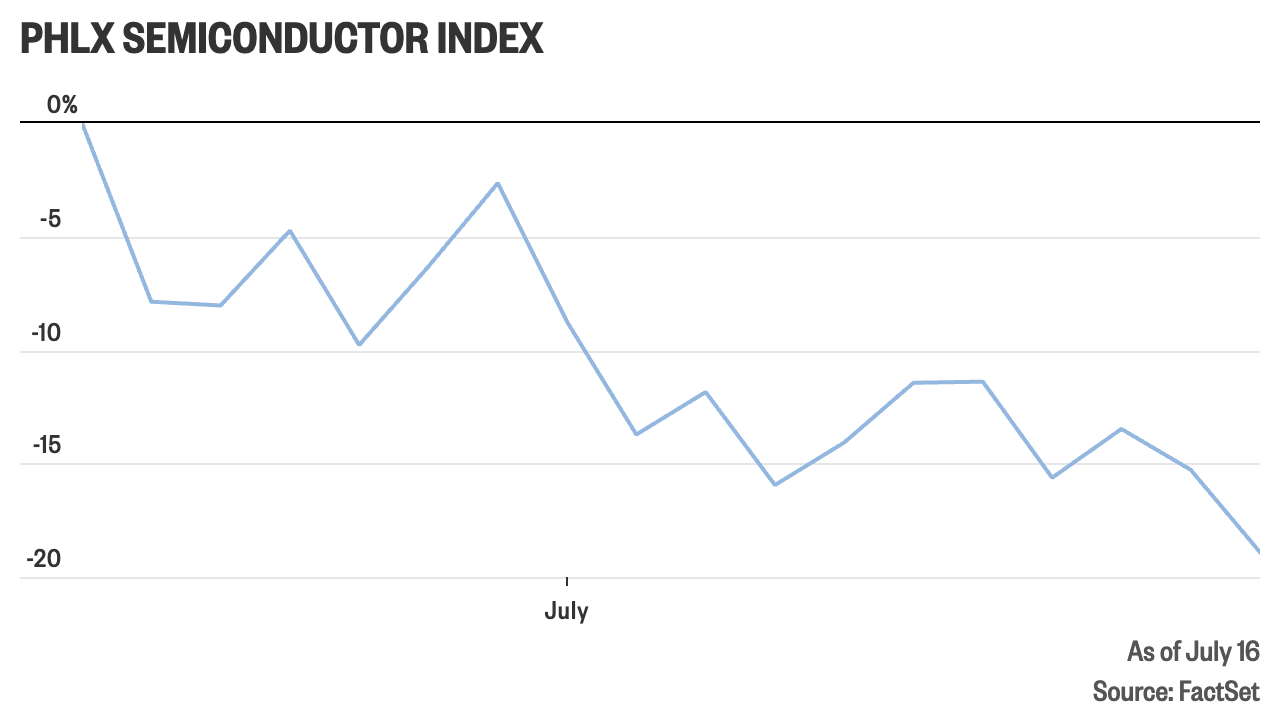

- 费城半导体指数从6月高点回落约19%,若再跌至20%将确认进入技术性熊市,30只成分股均较纪录高位走低。

- 资金正从高估值的芯片和存储股撤出,转向银行、零售和运输等直接受益于经济韧性的板块,市场广度扩大。

- 芯片行业Q2盈利增速预计高达131%,但市场质疑高增长的持续性,强势业绩未能阻止股价下跌。

- 高盛警告AI资本开支与变现回报之间存在张力,超大规模云企业投入速度超过自身现金流增长。

- AI交易逆转拖累全球风险偏好,日本日经225指数收跌4%,台积电、ASML等芯片股承压。

Original Author: Zhao Ying

Original Source: Wall Street News

The AI-driven chip trade is experiencing a rapid cool-down. The Philadelphia Semiconductor Index has fallen about 19% from its June peak, just a step away from confirming a bear market. Capital is rotating out of high-valuation chip and memory stocks and into sectors like financials, retail, and transportation that benefit more directly from economic resilience.

In Thursday's US stock trading, the Philadelphia Semiconductor Index fell 4.3%, with all 30 component stocks declining from their record highs on June 22. According to Dow Jones Market Data, if the index falls further into a 20% decline from its peak, it would confirm a technical bear market. On Friday, the sell-off spread to Asian and European markets, with Japan's Nikkei 225 closing down 4%, while TSMC, Kioxia, and European chip equipment maker ASML all came under pressure.

The reversal of the AI trade is dragging down global risk appetite. The Philadelphia Semiconductor Index fell 8.5% this week, on track for its worst weekly performance since last year's "Tariff Day" tariff shock. Nasdaq 100 futures fell 1.6%, and S&P 500 futures dropped 0.9%, as market concerns simultaneously intensified over the return on AI infrastructure investment, inflation risks, and the outlook for monetary policy.

Goldman Sachs' head of trading describes the current AI market as a "rubber band" being stretched ever tighter. As hyperscale cloud companies continue to ramp up capital expenditure, the key question for the market has shifted from "how big is the investment scale" to "when and how will these investments translate into returns." The upcoming earnings reports from tech giants could become the first key milestone to test this logic.

Chip Index Nears Bear Market, Profit-Taking Turns into Broad Cooling

Chip stocks were among the most favored trades this spring. As investors once worried that the "Magnificent Seven" bore most of the cost of building AI data centers, capital flowed into chip manufacturing, memory, and semiconductor equipment companies, betting they would be the direct beneficiaries of the capital expenditure cycle.

But this trade is rapidly reversing. As of Thursday, the Philadelphia Semiconductor Index had fallen 19% from its all-time high on June 22. The index fell 4.3% that day, just a step away from the 20% retracement threshold that would confirm a bear market.

Individual stock movements are even more dramatic. Marvell Technology has fallen nearly 40% since the Philadelphia Semiconductor Index peaked, yet it is still up 121% year-to-date. This reflects that the current adjustment is more concentrated on AI beneficiaries that had previously seen large gains, as investors re-evaluate whether high growth expectations have been fully or even excessively priced into stock prices.

In Thursday's US market, Sandisk, Western Digital, and Seagate all fell over 9%, while Intel and Micron dropped around 6%. The sell-off continued in Asian markets on Friday, with Japanese memory chip maker Kioxia falling as much as 16%, down more than half from its June highs; TSMC shares also fell sharply.

Earnings Still Strong, But Market Begins to Question Growth Sustainability

The chip sector does not face a near-term earnings collapse. FactSet data shows the market expects second-quarter earnings for S&P 500 companies to grow 23.6% year-over-year, while earnings growth for the semiconductor and related equipment industry is forecast to be as high as 131%.

The problem is whether strong current earnings are sufficient to support valuations that already reflect years of growth expectations. David Russell, Global Market Strategy Head at TradeStation, stated that while tech companies may deliver stellar results, the market is now asking whether this growth is sustainable over the next one to three quarters.

TSMC's performance highlights this contradiction. Despite the company reporting a record quarterly profit, its stock price weakened significantly this week. The Financial Times reported that TSMC fell over 7% on Friday. The fact that earnings exceeded expectations failed to stop the stock price decline shows the market's focus has shifted to order sustainability, capital expenditure returns, and the slope of AI demand growth, rather than single-quarter profits alone.

Kevin Gordon, Senior Investment Strategist at Schwab Center for Financial Research, believes the sharp adjustment in chip stocks may not necessarily constitute a serious warning signal. Over the past decade, the Philadelphia Semiconductor Index has experienced six drawdowns exceeding 20% and 31 corrections of at least 10%, showing significantly higher volatility than the S&P 500. But these frequent adjustments also mean the sector is highly sensitive to changes in valuations, inventory cycles, and capital expenditure expectations.

Capital Rotates to Economically Sensitive Sectors, Market Breadth is Widening

As chip stocks come under pressure, there's a clear rotation of capital within the US stock market. The financial sector closed at a record high for a second consecutive day on Thursday, driven by strong bank earnings. The Dow Jones Transportation Average rose over 30% year-to-date, nearing its historical high, while the retail ETF also climbed towards levels last seen in early 2022.

David Royal, Chief Financial and Investment Officer at Thrivent, stated that widening market breadth is a healthy sign, and recent employment and retail sales data also show the economy remains resilient. The flow of capital from high-valuation tech sectors to financials, consumer, and transportation means investors are not exiting risk assets entirely, but are reallocating towards assets more sensitive to economic growth.

This rotation also weakens the previous relative advantage of chip stocks. When the economic outlook remains stable, investors have more choices and don't have to continue concentrating their bets on the highest-valuation, most crowded companies in the AI infrastructure chain.

Goldman Sachs Warns: Tension Between AI Capex and Monetization Returns

Goldman Sachs' Mark Wilson, Head of EMEA Equity Hedge Fund Sales, and Rich Privorotsky, Head of EMEA Equity Flow Intermediation, believe that the mismatch between AI infrastructure investment and commercialization returns is becoming the core risk variable for the market.

They point out that hyperscalers like Microsoft, Amazon, Alphabet, and Meta are investing in AI infrastructure at a scale exceeding their own operating cash flow growth rates. But in the short term, there remains significant uncertainty about how much revenue, profit, and cash return these investments will generate.

Privorotsky describes the AI market as a "rubber band."The key question isn't whether the market still believes in the long-term direction of AI, but how long this stretching of valuations and capital expenditures can continue. Goldman Sachs also notes that the rapid proliferation of frontier models and the decline in inference costs could alter the AI value chain: the scarcity premium for hardware and computing power may decrease, while platform companies controlling distribution channels and workflows could capture more value.

If any one of the hyperscale cloud companies takes the lead in cutting capital expenditure, the market could rapidly reassess the demand outlook for the entire AI hardware chain, triggering a broader chain reaction.

Earnings Season Will Test if the AI Trade Can Regain Support

The market's next focus will shift to the earnings reports and capital expenditure guidance of big tech companies. Alphabet and Tesla will report results on July 22. Their commentary on AI investment, data center construction, and commercialization progress could influence whether the chip sector can halt its decline.

In the short term, the high earnings growth rate of chip stocks still provides some valuation support, but the market is no longer satisfied with "high growth" alone. Investors need to see improvements in revenue, margins, and cash flow resulting from AI spending. They also need confirmation that the capital expenditure of hyperscale cloud companies won't slow down due to funding pressures, rising inflation, or returns failing to meet expectations.

Whether the Philadelphia Semiconductor Index officially falls into a bear market may just be a technical dividing line. For the market, the more important dividing line is whether the AI trade can transition from an advance on years of future growth to a validation of realistic return pathways.