没有了Strategy的买盘,比特币还能涨吗?

- ประเด็นหลัก: การเคลื่อนไหวล่าสุดของ Bitcoin ขึ้นอยู่กับพฤติกรรมการซื้อของ Strategy เป็นอย่างสูง โดยในฐานะผู้ซื้อรายใหญ่ที่สุด Strategy ได้เข้าซื้อจำนวนมากในช่วงวันที่ไม่ได้รับสิทธิ์ปันผลเพื่อพยุงราคา ความต่อเนื่องของการซื้อหลังจากสิ้นสุดช่วงดังกล่าวจึงกลายเป็นตัวแปรสำคัญต่อการเคลื่อนไหวระยะสั้นของตลาด

- ปัจจัยสำคัญ:

- สัปดาห์ที่แล้ว Strategy ซื้อ BTC จำนวน 34,164 เหรียญด้วยมูลค่า 2.54 หมื่นล้านดอลลาร์ ทำให้การถือครองรวมอยู่ที่ 815,061 เหรียญ โดยกลยุทธ์ TWAP ของพวกเขาได้เพิ่มอุปสงค์ในตลาดสปอตอย่างมีนัยสำคัญ

- หลังจากช่วงวันที่ไม่ได้รับสิทธิ์ปันผลในเดือนมีนาคม ปริมาณการซื้อของ Strategy ลดลงอย่างรวดเร็วจาก 1.18 หมื่นล้านดอลลาร์เหลือเพียง 765 ล้านดอลลาร์ และการออกหุ้นสามัญ MSTR ผ่าน ATM ก็หยุดลง ส่งผลให้ราคา BTC ร่วงลงมาอยู่ที่ประมาณ 70,000 ดอลลาร์

- เดือนเมษายนมีความแตกต่าง: ณ วันที่ 22 เมษายน ราคา BTC มีเสถียรภาพที่ประมาณ 77,500 ดอลลาร์ โดยไม่แสดงสัญญาณอ่อนแอทันทีหลังช่วงไม่ได้รับสิทธิ์ปันผลเหมือนในเดือนมีนาคม ซึ่งบ่งชี้ว่าอาจมีการซื้ออย่างต่อเนื่อง

- เอกสาร 8-K ที่จะเผยแพร่ในวันที่ 27 เมษายนมีความสำคัญอย่างยิ่ง จะเปิดเผยว่า Strategy ยังคงซื้อต่อไปหลังจากปิดช่วงวันที่ไม่ได้รับสิทธิ์ปันผลหรือไม่: หากการออก STRC ยังคงคึกคัก หรือ ATM ของ MSTR เกิน 150 ล้านดอลลาร์ จะถือเป็นการเปลี่ยนแปลงกระบวนทัศน์ของตลาด

- ความเสี่ยงระยะยาว: อัตราเงินปันผลที่สูงถึง 11.5% ของ Strategy มีต้นทุนสูง หากตลาดทุนตึงตัวหรือราคา BTC หยุดนิ่ง อาจถูกบังคับให้ขาย BTC หรือเจือจางหุ้นเพื่อระดมทุน

Over the past month, Bitcoin's price action seemed to signal a clear pattern: when Strategy enters the market, BTC finds support; conversely, once Strategy steps back, the market quickly weakens.

Last week, the company spent $2.54 billion to acquire 34,164 BTC, bringing its total holdings to 815,061 BTC. Strategy's TWAP strategy has injected genuine spot demand into the market, while the market remains cautious: near the critical resistance level of $80,000, it's unclear whether the current trend can establish an independent foothold.

Looking back at March, after the ex-dividend week, Strategy significantly slowed its pace of buying BTC, which subsequently dragged down BTC's price. The reason BTC was able to hold its price was solely because Strategy was providing support. The next move depends entirely on whether this buying pressure persists after the ex-dividend window closes.

March's performance already exposed the risk. Strategy aggressively accumulated during the window, then quickly went dormant, and BTC's price almost immediately "stalled and fell." Entering the post-ex-dividend period in April, the situation was identical. The real question now is whether Strategy will continue buying once the ex-dividend window closes.

If April can avoid repeating March's "post-ex-dividend weakness," the bullish thesis will be much stronger. If not, it's just a replay of last month's script.

Core Summary (TL;DR)

- Marginal Buyer: Strategy is the largest marginal buyer in the market. The recent rebound during US trading hours proves that Bitcoin's gains over the past month have been largely driven by it.

- March's Playbook: Strategy aggressively bought BTC before the $STRC ex-dividend window, but BTC's price plummeted over the following two weeks.

- April's Difference: As of April 22, BTC has not yet experienced post-ex-dividend weakness, with prices remaining firm near $77,500.

- Key Signal: The upcoming 8-K filing (due April 27) is critical; it will determine whether Strategy continued buying after the ex-dividend window closed.

- Long-Term Risk: Strategy's dividend yield of 11.5% is expensive. If capital markets tighten, they may eventually be forced to sell BTC or dilute stock to fund it.

Bitcoin's Largest Marginal Buyer: Strategy

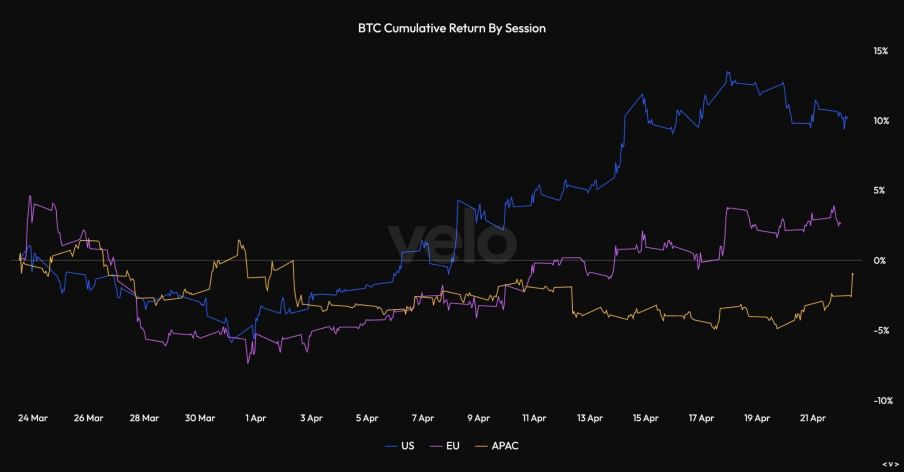

Over the past month, almost all of BTC's gains occurred during US trading hours. This was partly thanks to spot ETFs, but more so due to buying pressure from Strategy. The best way to understand this rally isn't as a vague "risk-on" rebound, but as concentrated US buying interest supported by ETF flows. Daily data from Farside shows net inflows of approximately $1 billion, highlighting tangible market demand.

However, this alone doesn't fully explain the price action. In the week ending April 19, Strategy's massive $2.54 billion purchase exceeded net ETF inflows. This confirms a more reasonable interpretation: it's not that "ETFs are absent," but that both ETFs and Strategy are buying, and Strategy's buying volume is large enough to be one of the most important marginal buyers in the market, perfectly aligning with the trading session charts. Since almost all gains occurred during US trading hours, and one of the largest US buyers spent $2.54 billion, Strategy's absolute influence on BTC's price is self-evident.

The Real Test for the Rally Comes After the Ex-Dividend Date

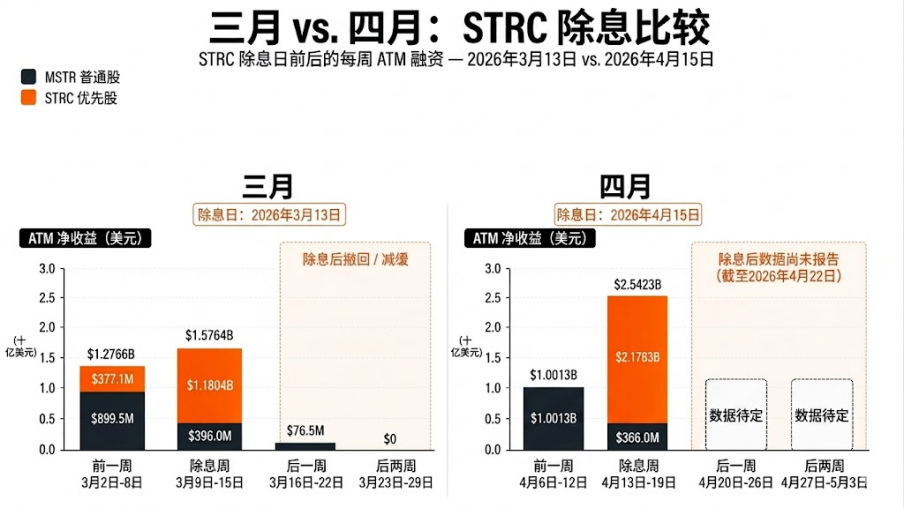

In March, Strategy bought aggressively during the $STRC ex-dividend window, but BTC's price fell sharply in the subsequent two weeks. In the week ending March 22, demand for $STRC plummeted from $1.18 billion to just $76.5 million. ATM (At-The-Market) issuance of MSTR common stock also dropped to zero. By the week ending March 29, total ATM proceeds were zero. This was also the first time in 13 weeks that Strategy did not purchase any BTC.

Strategy's two-week absence, coinciding with BTC's decline, is the clearest evidence of its decisive role in BTC's price action. BTC gradually fell to just above $70,000, hitting around $70,400 on March 20 and $70,600 on March 23. The price action reflected reality: when STRC issuance stopped and MSTR common stock didn't fill the gap, buying power was significantly weakened.

Therefore, the core question now is whether April will repeat March's "hangover" or break the spell.

The next 8-K filing (due April 27) will cover the week ending April 26. If STRC issuance again drops to negligible levels and MSTR common stock ATM remains near zero, then April is just a larger version of March, not a true paradigm shift. However, if STRC remains active and MSTR common stock ATM reaches a significant scale (over $150 million), then the narrative truly changes.

April is Crucial Because BTC Has Remained Strong So Far

April 15, 2026 was the ex-dividend date for $STRC in April. STRC's annualized dividend yield remains at 11.50%. In the week ending April 19, Strategy raised $2.5 billion and bought 34,164 BTC, releasing enormous demand. However, the real test is BTC's performance afterward: unlike in March, BTC hasn't immediately experienced a price plunge.

We could argue that Strategy has changed market dynamics. But the upcoming filing is much more important than the last one. If the usual "post-ex-dividend weakness" reappears, then April might just be a replay of March. If it doesn't, the market must seriously consider that Strategy isn't just buying during the window but is supporting BTC over a longer timeframe.

Will the Buying Continue?

This is the part traders really care about.

Just noticing that Strategy bought a lot of BTC last week doesn't make money. What truly matters is whether this buying continues once the pure ex-dividend logic plays out.

March's lesson is that a strong ex-dividend week alone isn't enough. Strategy bought 22,337 BTC in the reporting period ending March 15, but largely disappeared over the next two weeks, causing BTC's price to weaken.

April's performance suggests there's still hope, because Strategy bought even more — 34,164 BTC — and BTC's price hasn't yet repeated March's decline.

The logic here is very straightforward. If the next 8-K filing shows significant buying after the ex-dividend date, the market must assume this buying remains active. If it shows issuance crashing again, then March's performance was their standard operating procedure, not an anomaly.

Why It's Bullish Now — But Future Concerns Remain

As of April 2026, STRC's annualized dividend yield is a high 11.50%. As long as the market is happy to pay for this structure and BTC's price is cooperating with an uptrend, it's not a problem. But if BTC stalls and capital markets become less generous, things could get very tricky.

While this is a medium-term issue, not the immediate trading logic, the risk is real. This flywheel only works perfectly when BTC is rising and investor appetite is strong.

Therefore, the clearest framework is: As long as Strategy is buying, it's bullish for BTC, but that doesn't mean its capital structure is risk-free. For now, though, the market only needs to focus on the first half of that sentence.

Final Conclusion

Recent BTC price action looks like a market propped up by an extraordinary super-marginal buyer. March showed us what happens when that buyer disappears. If Strategy halts capital raising with $STRC in the first two weeks after the ex-dividend period, April's price action is likely to follow suit.

So, the correct way to interpret the current market isn't to obsess over the headlines of the last purchase number, but to ask a simpler question: Once the obvious window is over, is Strategy still bidding for BTC?

If the answer is yes, BTC will likely continue to find support. If the answer is no, BTC will immediately feel what it's like to lose the support of the largest visible marginal buyer. If it can still rally then, that would be the clearest and most ultimate bullish signal.