ทำไม American Depositary Receipt (ADR) ของ SK Hynix ถึงมีส่วนเกินมูลค่าถึง 50%? การทดสอบแรงกดดันของโครงสร้างตลาด

- มุมมองหลัก: ส่วนเกินมูลค่าของ ADR SK Hynix ในช่วงแรกที่เข้าจดทะเบียนในตลาด Nasdaq ที่สูงถึง 52.5% เป็นผลจากความต้องการของตลาดสหรัฐฯ ที่แข็งแกร่งผนวกกับอุปทานที่ถูกจำกัดจากการเก็งกำไร ไม่ใช่การเปลี่ยนแปลงโดยพื้นฐานของมูลค่าพื้นฐาน

- ปัจจัยสำคัญ:

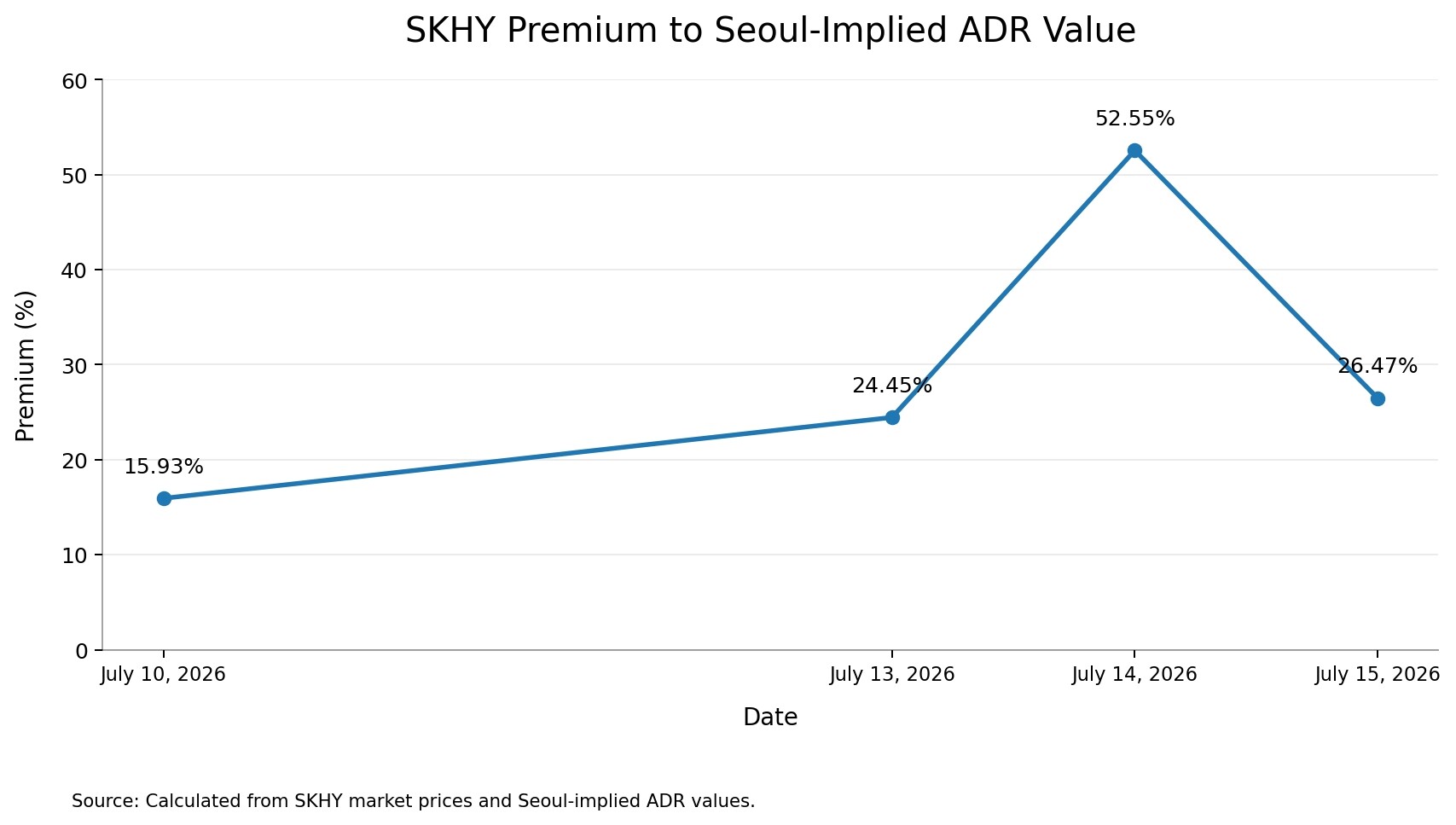

- ส่วนเกินมูลค่า ณ สิ้นวันที่ 14 กรกฎาคมของ SKHY อยู่ที่ 52.5% ก่อนจะลดลงอย่างรวดเร็วเหลือ 26.5% ในวันถัดมา แสดงให้เห็นว่าความผันผวนเกิดจากความไม่สมดุลของโครงสร้างตลาด ไม่ใช่การประเมินมูลค่าพื้นฐานใหม่

- ช่องทางการเก็งกำไรถูกจำกัด: การสร้าง ADR ใหม่ต้องเผชิญกับข้อจำกัดด้านกฎระเบียบของเกาหลีใต้ เงื่อนไขของสถาบันรับฝากหลักทรัพย์ และระยะเวลาล็อค 90 วัน ทำให้ไม่สามารถเพิ่มอุปทานของหลักทรัพย์ที่ส่งมอบได้อย่างรวดเร็ว

- ปริมาณการซื้อขายสูงควบคู่กับสต็อกเก็งกำไรต่ำ: ปริมาณการซื้อขายในช่วงสี่วันแรกสูงถึง 176% ของขนาดการออกหุ้น แต่อัตราการหมุนเวียนที่สูงนั้นเพียงหมุนเวียนสต็อกที่มีอยู่ ไม่ได้สร้างอุปทานเพิ่มเติม

- ส่วนเกินมูลค่าของ ADR เป็นการตั้งราคาสำหรับความสะดวกและความขาดแคลน: การจดทะเบียนในสหรัฐฯ ช่วยขจัดอุปสรรคในการซื้อขายในตลาดเกาหลีใต้ แต่อุปทานที่จำกัดและอุปสงค์ที่กระจุกตัวได้ผลักดันราคาในระยะสั้นให้สูงขึ้น

- ปัจจัยพื้นฐานสนับสนุนมูลค่าระยะยาว: SK Hynix มีรายได้เพิ่มขึ้น 47% ในปี 2025 และมีอัตรากำไรจากการดำเนินงาน 49% จากความต้องการ HBM ที่แข็งแกร่ง แต่ก็ไม่สามารถอธิบายส่วนต่างราคาที่รุนแรงในระยะสั้นได้

- การออกหุ้นใหม่ในวันที่ 29 กรกฎาคมเป็นการทดสอบโครงสร้างตลาด: การออกหุ้นใหม่อาจปรับปรุงเงื่อนไขการดำเนินงาน แต่ไม่ได้รับประกันโดยอัตโนมัติว่าจะมีการแปลงสองทางแบบไม่จำกัดหรือส่วนเกินมูลค่าจะหายไป

Key Takeaways

On July 14, 2026, SK Hynix's American Depositary Shares (ADS) listed on the Nasdaq traded at a premium of up to 52.5% over the implied value of its ordinary shares listed in Seoul. Just one trading day later, this gap narrowed to approximately 26%. This sharp reversal indicates that the premium was not merely a market repricing of the AI memory leader's fundamental valuation. Strong US market demand met the limited initial supply of SKHY shares, and arbitrage channels could not immediately create enough new securities or short exposure to keep prices aligned between the two markets. In other words, SK Hynix's fundamentals created the demand, but the structure of the ADR market dictated how far prices could deviate from the Seoul market in the short term.

News Brief

On July 14, 2026, the price of SK Hynix's American Depositary Shares (ADS) listed on the Nasdaq traded at a premium of up to 52.5% over the implied value of its ordinary shares listed in Seoul. Just one trading day later, this gap narrowed to approximately 26%. This sharp reversal indicates that the premium was not merely a market repricing of the AI memory leader's fundamental valuation. Strong US market demand met the limited initial supply of SKHY shares, and arbitrage channels could not immediately create enough new securities or short exposure to keep prices aligned between the two markets. In other words, SK Hynix's fundamentals created the demand, but the structure of the ADR market dictated how far prices could deviate from the Seoul market in the short term.

Core Points

Based on the US closing price, the latest Korean closing price, and the corresponding USD/KRW exchange rate, SKHY's closing premium on July 14 reached 52.55%. This premium dropped to 26.47% on July 15, indicating that most of the spread is highly sensitive to market capital flows and cross-market price discovery. In a conventional sense, SKHY is not illiquid, as its trading volume over the first four trading days in the US market was approximately 176% of the initial ADS offering size. The main constraint is not a lack of trading, but an insufficient number of securities that can be readily created, borrowed, or delivered for arbitrage trading. Additionally, July 29 is the official listing date for the newly issued underlying ordinary shares on the KOSPI market in Korea. While this is a significant market structure test, the public filings do not establish it as a guaranteed date for unrestricted two-way conversion.

How is the 52.5% SK Hynix ADR Premium Calculated?

SKHY is the Nasdaq ticker for SK Hynix's American Depositary Shares (ADS). Each SKHY ADS represents one-tenth of a Korean ordinary share, meaning ten ADS correspond to one SK Hynix share listed in Korea. Therefore, the implied value of one ADS can be calculated by dividing the Korean ordinary share price by 10, then dividing by the USD/KRW exchange rate. The ADR premium is then derived by dividing the SKHY price by the implied ADS value and subtracting 1.

On July 14, SKHY closed at $193.92, while SK Hynix's Korean stock closed at 1,913,000 KRW. Using the prevailing USD/KRW exchange rate of 1,504.9, the implied ADS value from the Korean stock was approximately $127.12. This resulted in a massive closing premium of 52.55%. In the preceding trading sessions, the premium was much lower, around 15.9% on July 10 and 24.5% on July 13. Subsequently, the premium expanded to over 50% on July 14 before retreating to about 26.5% on July 15.

This chronology is significant. A company's underlying business value rarely changes so drastically within a day to justify a premium swing from roughly 24% to 52% and back to 26%. Instead, this volatility points to a temporary imbalance in market access, available supply, and price discovery. The calculation also involves an unavoidable time lag, as Seoul and New York markets do not trade simultaneously. When SKHY closes in the US, the Korean market has already been closed for several hours. Therefore, part of the observed premium might reflect new information not yet priced into Korean shares. However, the gap remained abnormally large even after the Korean market had a chance to react. Comparing the Korean close on July 15 with the prior US close still yields a premium of about 39%. Ultimately, the time zone difference amplifies the overall premium figure but does not fully explain the phenomenon.

Why Didn't Arbitrageurs Immediately Close the Gap?

In theory, this trade seems straightforward. Arbitrageurs could, theoretically, buy the cheaper ordinary shares in Korea, deposit them with the relevant custodian, create new SKHY ADS, and then sell the more expensive ADS in the US, pocketing the difference after accounting for trading, financing, currency, and custody costs. If the conversion process were instantaneous, unrestricted, and perfectly symmetrical, a 50% spread would attract enough arbitrage capital to quickly narrow the gap.

However, SKHY does not appear to offer this frictionless mechanism. The deposit agreement grants ADS holders a contractual pathway to cancel their ADS and receive the underlying Korean ordinary shares, subject to fees, legal requirements, and settlement procedures. The reverse process, however, is much more restrictive. Depositing Korean shares to create new ADS may require proof that Korean regulatory conditions have been met. The depositary can refuse deposits under certain specific circumstances, may require the company's consent, and SK Hynix can impose limits on the number of shares deposited into the facility.

As detailed in SK Hynix's final US offering prospectus, the arbitrage channel is constrained by several factors, including a warning that investors who cancel ADS and withdraw Korean shares may not necessarily be permitted to re-deposit those shares to obtain ADS again. The offering also did not include an over-allotment or greenshoe option, and the company, along with certain related holders, is subject to a 90-day lock-up period. This creates an asymmetric arbitrage channel: converting expensive ADS into Korean shares is contractually feasible, but creating enough new ADS to sell and capture the premium is a process that may be slower, conditional, or quantitatively limited. A one-way exit from the expensive security does not exert the same price pressure as scalable new ADS creation and short selling capability. Therefore, the relevant arbitrage question is not whether conversion exists in legal theory, but whether traders can create, borrow, and deliver a sufficient number of securities quickly enough to meet US demand.

Is SKHY Illiquid?

Not in the conventional sense. SK Hynix sold 177.9 million ADS at $149 each in the offering, raising approximately $26.5 billion. Since each ADS represents one-tenth of an ordinary share, the offering corresponds to the issuance of 17.79 million new Korean shares. Trading activity has been exceptionally high, starting with a volume of about 107.7 million ADS on July 10. This was followed by 57.3 million on July 13, 72.6 million on July 14, and 76.3 million on July 15. The total volume over the first four trading days was approximately 313.9 million ADS, representing 176% of the initial offering size.

This is far from an illiquid market. However, high trading volume and ample arbitrage supply are not the same thing. The same ADS can change hands multiple times within a single trading day. High turnover merely cycles existing inventory; it does not automatically create additional securities for arbitrageurs to sell. Exacerbating this are supply constraints such as the deposit procedures, regulatory conditions, potential quantity limits, and a lack of publicly verifiable stock loan availability to confirm that short sellers can access a deep lending market. Therefore, a more accurate description is that SKHY is liquid in terms of trading volume but scarce in terms of readily deliverable arbitrage inventory. The premium arises because concentrated demand pushes the marginal price higher faster than arbitrageurs can expand the pool of available securities for sale.

What Is the US Market Actually Repricing?

The US market is not necessarily discovering that SK Hynix's factories, patents, or future cash flows are worth 50% more when represented by US securities. It is, to some extent, pricing the convenience and scarcity of immediate access to US market exposure. A dollar-denominated security listed on Nasdaq removes several hurdles for investors using Korean ordinary shares. These hurdles include navigating Korean market account and custody requirements, settlement in Korean won, different trading hours, local market operational procedures, fund mandates strictly favoring US-listed securities, and restrictions on using synthetic exposure like swaps.

Therefore, even though each ADS represents exactly the same underlying economic interest as a Korean share, a US-listed stock in limited supply could carry an access premium. But convenience alone is unlikely to sustain any level of premium. A mature ADR may trade at a modest persistent premium because investors value its convenience, liquidity, and inclusion in familiar portfolios. However, a premium exceeding 50% suggests that these structural advantages are combining with exceptionally concentrated demand, limited short-selling capacity, and temporarily constrained creation mechanisms. The market is not just repricing SK Hynix; it is pricing the scarcity of the specific security through which US investors want to hold their stake in the company.

Do SK Hynix's Fundamentals Support a Higher Valuation?

SK Hynix has a stronger fundamental basis than a typical newly listed foreign company. The company is a major supplier of High Bandwidth Memory (HBM), which is heavily used in advanced AI accelerators. Its earnings have greatly benefited from strong demand for HBM, server DRAM, and other high-value memory products. SK Hynix reported 2025 revenue of 97.15 trillion KRW, a 47% increase year-over-year, with an operating profit of 47.21 trillion KRW and an operating margin of 49%. The company noted its HBM revenue doubled over the year and that mass production of HBM4 is progressing smoothly.

Subsequently, the company's reported first-quarter 2026 results showed further acceleration, with revenue of 52.58 trillion KRW and an operating profit of 37.61 trillion KRW, driven by robust demand for higher-value AI memory products, as highlighted in SK Hynix's Q1 2026 Financial Results. These results explain why US investors want direct exposure. SK Hynix's positioning near the bottleneck of the core AI investment cycle infrastructure means its fundamentals can support a valuation re-rating relative to companies affected by the traditional "Korea discount" and can underpin a persistent convenience premium for the US-traded security.

However, this does not justify that the 52.5% ADR premium represents a sustainable fundamental valuation difference. Business risks remain significant. Investors must consider HBM competition from Samsung Electronics and Micron, the adoption speed and profitability of HBM4, customer concentration, massive capital expenditure needs, potential shifts in AI infrastructure spending, future down-cycles in traditional DRAM or NAND pricing, and increased memory supply as competitors expand capacity. Ultimately, fundamentals explain why demand is strong, but market structure explains why this demand temporarily creates such an extreme price spread.

What July 29 Means for the SKHY Premium

SK Hynix has stated that the newly issued ordinary shares from the ADR offering are scheduled for an additional listing on the KOSPI market on July 29, 2026, Korean time, a timeline supported by SK Hynix's official Nasdaq listing announcement. The company also plans to hold its Q2 earnings call on the same day. While some market commentary optimistically portrays July 29 as the date for smooth, open two-way conversion between ADRs and ordinary shares, the original documents do not support this definitive interpretation.

The confirmed event is the additional listing of the newly issued underlying shares on KOSPI, which could improve operational conditions for settlement, custody, and cross-market arbitrage. This does not automatically prove that unrestricted two-way conversion will commence, all quantity limits will disappear, or stock loan supply will become immediately ample. Therefore, July 29 should be viewed as a test of market plumbing, not a guaranteed date for price convergence. Key questions going forward will be whether the number of outstanding ADS begins to increase; whether the depositary accepts significant new Korean stock deposits; and whether publicly available short interest begins to develop. Furthermore, the market will closely watch whether the premium continues to narrow after the underlying shares are listed, whether Korean shares catch up to the US valuation, and whether Q2 earnings provide a new fundamental reason for movements in both markets. A narrowing premium would suggest operational constraints caused the initial spread, while a persistent premium would indicate the market is assigning an enduring value to US market access.

What Investors Should Verify Next

The most useful signal is not whether SKHY goes up or down on any isolated trading day, but whether the relationship between SKHY and Korean ordinary shares becomes more stable. Three indicators will be particularly important. First, the premium itself should be calculated using clearly stated timestamps, as comparing the US close with an outdated Korean close can exaggerate the apparent gap. Second, investors should monitor the supply of deliverable ADS, not just overall trading volume, as repeated trading of existing shares does not necessarily mean arbitrage capacity has expanded. Third, the market should carefully distinguish between fundamental repricing and security-level scarcity. Strong earnings and AI capital expenditure enhance SK Hynix's value as a company, but they cannot explain why identical economic interests trade at vastly different prices across two markets, subject to constraints on conversion, settlement, and investor access. SK Hynix's US listing did not create a second fundamental value for the company; it temporarily created a second market structure in which a premium for immediate access to a scarce US-listed security was priced much more aggressively than the underlying stock in Seoul.