Decoding Figure Q3: Why is it the Undisputed Top RWA Stock?

- Core Viewpoint: Figure reconstructs financial middle and back-office operations through blockchain technology, achieving highly efficient profitability.

- Key Elements:

- Blockchain technology reduces loan processing costs by over 100 basis points and shortens the time to 5 days.

- Q3 net profit reached $90 million, with a net profit margin of nearly 57%.

- Built a closed-loop ecosystem spanning from asset origination and securitization to DeFi financing.

- Market Impact: Provides a verifiable, highly efficient business model template for the RWA sector.

- Timeliness Note: Medium-term impact

Original Author: @BlazingKevin_, Researcher at Movemaker

1. Executive Summary

Figure Technology Solutions (hereinafter referred to as "Figure") is at the forefront of transforming the financial services industry, dedicated to reshaping traditional lending and capital markets through blockchain technology. As a vertically integrated fintech company, Figure is not only the largest non-bank Home Equity Line of Credit (HELOC) originator in the United States but also a key infrastructure provider in the Real World Asset (RWA) tokenization space. As of December 2025, Figure has successfully completed its IPO, with its market capitalization stabilizing in the range of $7.5 billion to $9 billion.

The core thesis of this report is that Figure represents the third stage of fintech evolution: from "online" (e.g., Rocket Mortgage) to "platform" (e.g., SoFi), and now to "on-chain." By leveraging its public blockchain, Provenance Blockchain, developed based on Cosmos SDK, Figure has successfully addressed the most challenging "middle and back-office efficiency" problems in traditional finance. By directly minting, registering, and trading assets (such as mortgages and title records) on-chain, Figure can reduce loan origination and securitization costs by over 100 basis points and shorten processing times from the traditional 30-45 days to under 5 days.

2025 was a pivotal year for Figure. The company not only achieved GAAP profitability, with Q3 net profit approaching $90 million, but also completed a strategic merger with Figure Markets, reintegrating its lending business with its digital asset trading platform. This move has created a closed-loop ecosystem: consumers can obtain funds by pledging their property, with funds disbursed in the form of an interest-bearing stablecoin ($YLDS), which can then be directly invested on the Figure Markets exchange or restaked in the Democratized Prime protocol. This integration of the "asset side" and "funding side" showcases the ultimate vision of the RWA track.

This report will dissect Figure's Q3 financial report and evaluate whether its "blockchain-native" strategy constitutes a true moat and its long-term investment value in the increasingly crowded RWA space, based on recent updates to its revenue sources and business model.

2. Business Segments and Product Lines

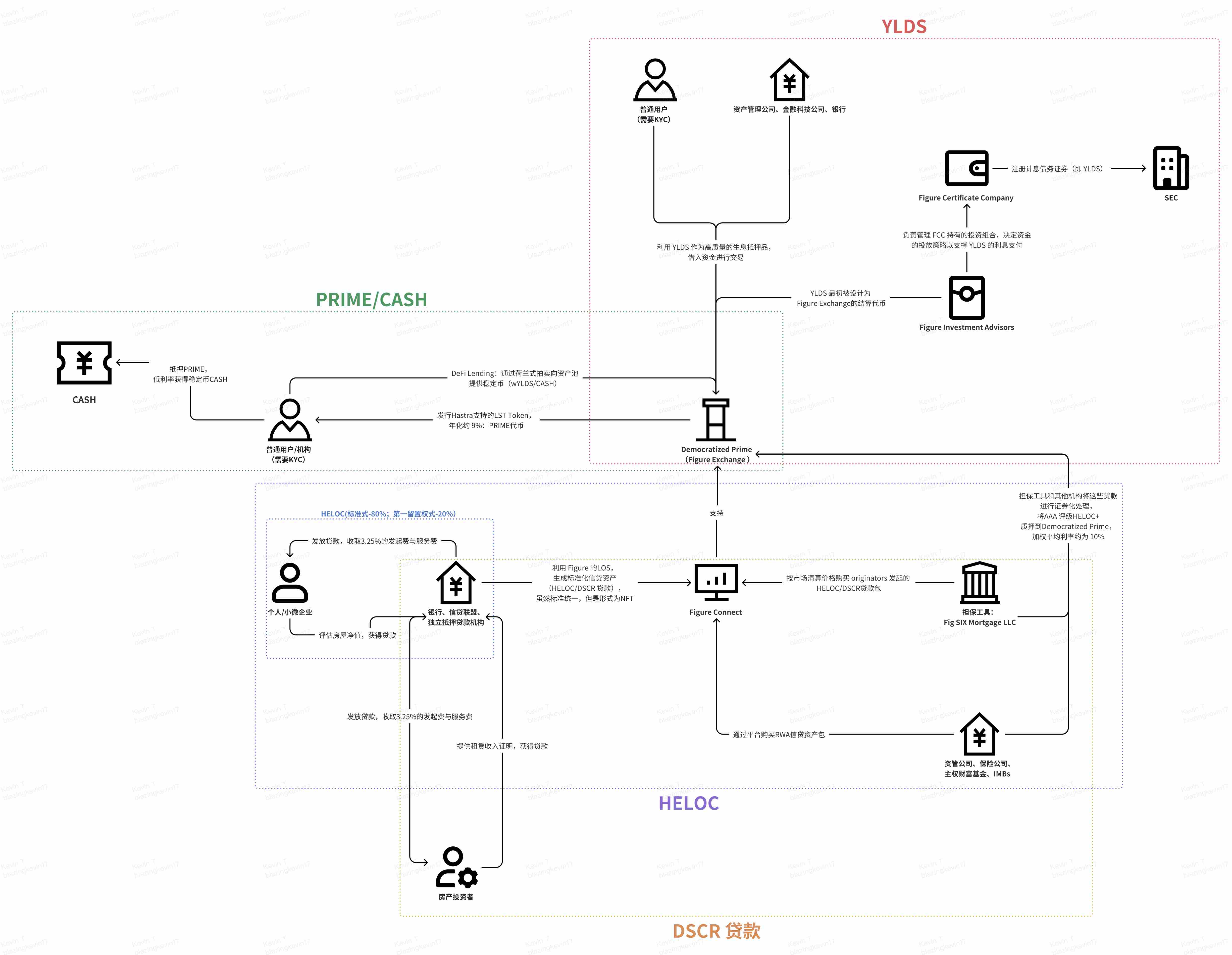

Following the completion of its merger with Figure Markets in July 2025, Figure's business structure has become more cohesive and vertically integrated. Figure's core competency lies in digitizing the entire lifecycle of assets (origination, registration, trading, financing, settlement) via the Provenance blockchain. **Based on this, we have organized Figure's four core business models: RWA Asset Origination and Distribution, Capital Protection and Securitization, DeFi Financing and Lending, and Interest-Bearing Stablecoin and Payment Settlement.** As shown in the diagram below, we connect these four businesses to clarify Figure's complete commercial model.

2.1 RWA Asset Origination and Distribution

2.1.1 HELOC

This is Figure's "foundation," aimed at solving the pain points of traditional credit markets: manual operations, paper dependency, and high costs (industry average $11,230). Primarily HELOC, it's noteworthy that DSCR loan transaction volume surged significantly in Q3. Starting with HELOC, it is Figure's flagship product.

Product Mechanism and User Experience: Traditional banks typically take 30 to 45 days to process a HELOC, involving cumbersome offline appraisals and notarization. Figure utilizes Automated Valuation Models (AVM) and immutable records on the blockchain to achieve an extreme experience of "5-minute approval, 5-day funding." This speed advantage directly addresses a market pain point, especially in a high-interest-rate environment where homeowners prefer accessing liquidity via HELOC rather than selling their homes to avoid losing their original low-rate mortgages.

Market Position: Since its inception, Figure has originated over $19 billion in loans, making it the largest non-bank HELOC originator in the United States. Its market share among non-bank institutions is dominant.

HELOC+ is the highest-grade premium loan pool within the protocol. Its underlying collateral consists of HELOC asset packages originated by Figure and its partners and tokenized on the Provenance blockchain. The credit quality of these assets is comparable to those that receive a AAA rating from S&P.

From another perspective, regarding the HELOC business, from loan origination to the final securitization of RWA assets, the involved stakeholders and their objectives are as follows:

Borrowers (Individuals/Small Businesses):

- Apply for Home Equity Lines of Credit (HELOC) or Small Business Loans (SMB) through Figure's 100% digital process.

- Authorize the system to automatically verify income, assets (AVM valuation), and credit scores, achieving "5-minute approval, 5-day funding."

Originating Partners (Banks, Credit Unions, Independent Mortgage Lenders):

- Utilize Figure's white-label Loan Origination System (LOS) to produce standardized credit assets under unified underwriting standards.

- Pay transaction volume-based technology processing fees to Figure.

- Place the produced credit asset packages on the Figure Connect marketplace for bidding or sell based on forward commitments, achieving rapid capital turnover without long-term balance sheet occupancy.

Figure Connect Platform (Matchmaker):

- Transforms credit assets into "digital twin" tokens on the Provenance blockchain, ensuring uniqueness and immutability of ownership, composition, and performance history.

- Facilitates transactions between originating banks and capital market buyers (institutions), providing real-time, atomic on-chain settlement services.

Institutional Buyers (Asset Managers, Insurance Companies, Sovereign Wealth Funds):

- Purchase homogeneous credit asset packages with AAA-rated potential through the platform, gaining transparent, data-rich credit exposure.

- Enjoy settlement speeds several times faster than traditional secondary markets (reduced from months to days/seconds).

2.1.2 First Lien HELOC

Within Figure's business model, the cash-out refinance business is being reshaped through its innovative product, "First Lien HELOC." This business is growing extremely fast, with transaction volume in the first half of 2025 increasing nearly 3 times year-over-year. Next, we explain the core differences between cash-out refinance and HELOC businesses.

In both traditional finance and Figure's blockchain-native credit model, while both are means for homeowners to extract home equity, they differ significantly in loan nature, lien priority, and capital market performance.

1. Loan Nature and Credit Structure: Open-End vs. Closed-End

- HELOC: Under legal and regulatory frameworks (e.g., Truth in Lending Act - TILA), HELOC is defined as "open-end credit." Its core characteristic is that homeowners can repeatedly draw and repay funds during a specified draw period (typically 2 to 5 years). Figure's HELOC product allows borrowers to make multiple withdrawals as needed without incurring additional out-of-pocket fees or closing costs.

- Cash-Out Refinance: This typically falls under "closed-end credit." The homeowner applies for a new loan larger than the existing mortgage, pays off the old loan, and receives the remaining cash difference in a lump sum. It is not a revolving line of credit but a one-time debt restructuring action.

2. Difference in Lien Priority

- HELOC: Typically exists as a "second lien." This means it is an additional liability on top of the homeowner's existing first mortgage. In liquidation, its repayment priority ranks after the first mortgage, hence it usually carries a higher risk weight.

- Refinance Business: Inevitably involves a "first lien." Since it replaces an old loan with a new one, the new lender obtains the primary lien on the property. One of Figure's fastest-growing products in recent years is the "First Lien HELOC," which is essentially designed as an alternative to traditional cash-out refinance.

- 3. Efficiency and Cost Differences in Figure's Model

According to Figure's business data, it has achieved a step-change reduction in costs for both types of businesses using blockchain technology:

- Cost Comparison: Figure's cost to process a first lien loan (refinance alternative) is only $1,000, while the industry average cost is as high as $12,000. For traditional HELOC, Figure's average production cost is only $730, far below the mortgage industry average of $11,230.

- Funding Time: Whether for refinance or HELOC, through Figure's automated Loan Origination System (LOS), homeowners can typically get approval within 5 minutes, with a median funding time of 10 days, compared to an industry median of about 42 days.

4. Capital Market and Securitization Logic

- HELOC Securitization: Figure has successfully issued multiple Asset-Backed Securities (ABS) backed by HELOCs, with senior tranches repeatedly receiving AAA ratings from Standard & Poor's and Moody's. Since HELOCs are often second liens, rating agencies typically assume a higher loss given default compared to first lien assets.

- Refinance (First Lien) Performance: Since refinance business holds first liens, its assets are more attractive in capital markets, often commanding more favorable risk pricing. Figure's first lien business volume grew nearly 3 times in Q3 2025.

Why are more and more American homeowners choosing First Lien HELOC, and what benefits can they obtain?

◦ Extreme Cost Savings: Figure's first lien production cost is approximately $1,000, while the industry average cost is $12,000, saving users a step-change in closing fees.

◦ Time Efficiency: Approval takes only 5 minutes, and median funding time is shortened from an industry average of 42 days to 10 days.

◦ Flexibility: Obtain lower interest rates than personal loans, often with the flexibility to extract equity again in the future.

From the data disclosed in the Q3 financial report:

In Q3 2025, Figure's total transaction volume in the consumer credit market reached $2.5 billion, a 70% year-over-year increase.

First Lien HELOC Performance:

◦ Q3 2025: First Lien HELOC transaction volume accounted for 17% of total consumer credit volume. Based on this calculation, the quarterly transaction amount was approximately $425 million. Its share increased by 650 basis points from 10.5% in the same period of 2024.

◦ First Half 2025 Performance: Its transaction volume accounted for 15% of total origination volume. The corresponding transaction amount was approximately $480 million.

◦ Growth Rate: This business exhibited exponential growth, with Q3 2025 transaction volume nearly tripling year-over-year.

Open-End/Standard HELOC (Typically Second Lien):

◦ Since HELOC constitutes 99% of the total, the vast majority excluding first liens fall into this category.

◦ Despite rapid first lien growth, Figure's balance sheet shows that as of September 30, 2025, 80% of its held HELOC assets were still in non-first priority positions (i.e., existing as second or third liens).

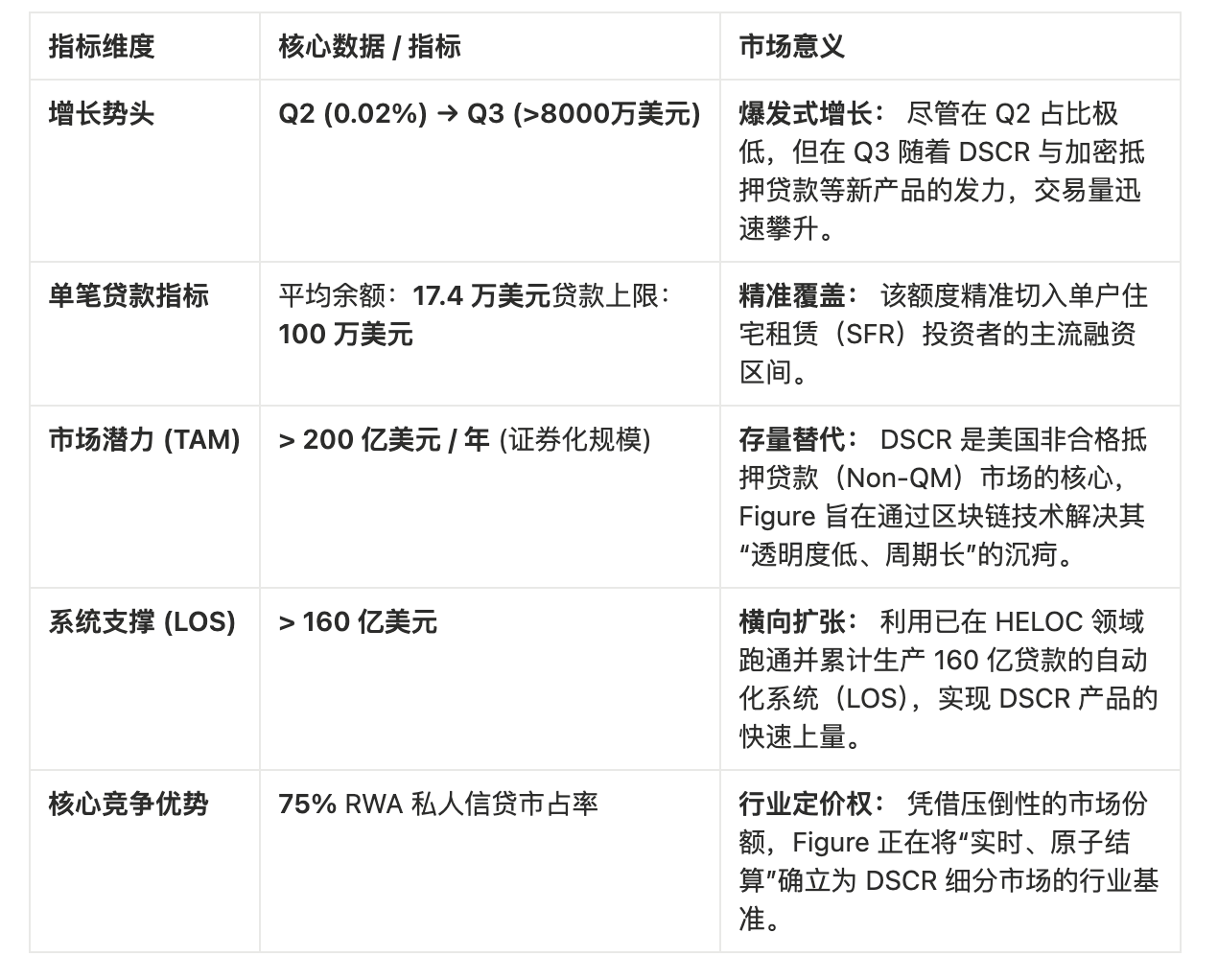

2.1.3 DSCR Loans

Designed specifically for real estate investors. This product does not consider the borrower's personal income but approves based on the property's Debt Service Coverage Ratio (DSCR).

DSCR loans are one of the core paths for Figure to expand its successful model from the HELOC space into broader consumer credit asset classes.

In Q3 2025, new product categories including DSCR loans contributed over $80 million in transaction volume, showing strong growth momentum.

Its participant structure, behavior patterns, and profit distribution logic are highly consistent with HELOC, but the underlying asset attributes focus more on the cash flow of investment properties. In terms of stakeholder profiles, apart from the borrower, it remains largely consistent with HELOC.

DSCR loan borrowers primarily finance rental properties. Borrowers submit applications through Figure's or its partners' portals. The special feature of DSCR loans is that, in addition to regular credit assessment, borrowers must provide proof of rental income (typically a lease) to calculate the Debt Service Coverage Ratio.

The logical core of DSCR loans lies in "replacing trust with facts (data)." Similar to HELOC, it achieves a "Pareto optimization" between the asset side and the funding side by transforming highly illiquid real estate debt claims into standardized, homogeneous tokens on-chain: borrowers get funds, institutions reduce friction costs, and ordinary DeFi users, originally on the periphery of finance, become co-beneficiaries of these high-quality RWA assets.

2.2 Capital Protection and Securitization

To enhance market liquidity and act as a "buyer of last resort," Figure has established strategic partnerships with top investment institutions.

Sixth Street (Strategic Joint Venture Partner):

- Provides $200 million in equity capital to the joint venture entity Fig SIX Mortgage LLC.

Fig SIX Mortgage LLC (Guarantor Vehicle):

- The jointly established entity Fig SIX Mortgage LLC is defined as a key "Guarantor Vehicle" within the Figure ecosystem and has received a $200 million recoverable equity capital commitment from Sixth Street.

- At the operational level, Fig SIX plays a crucial role as a "permanent buyer" on the Figure Connect electronic trading marketplace. This mechanism addresses the distribution concerns of originating partners like banks, credit unions, and independent mortgage lenders, ensuring their blockchain-native assets receive certain execution and more competitive market pricing. This "always-on" bidding mechanism essentially transforms what was once a fragmented and opaque private credit market into a standardized market with efficient price discovery.

- Fig SIX's risk hedging function is even more significant in the structuring of securitization products. When initiating securitization transactions, this vehicle actively retains and holds the "residual interest" or "first-loss piece" within the asset pool. This arrangement makes Fig SIX the "primary absorber" of credit risk, bearing losses first in case of defaults on the underlying HELOC loans, thereby protecting the interests of senior creditors.

2.3 DeFi Financing and Lending

This model democratizes capital flow by eliminating traditional prime brokers and warehouse financing intermediaries.

Asset Holders:

- Typically banks or lending institutions, they deposit tokenized credit assets (e.g., HELOC asset packages) generated through the LOS system or crypto assets into smart contracts as collateral. This model allows institutions to obtain real-time liquidity using their held RWA assets, often at a financing cost lower than traditional bank warehouse lines.

- The protocol uses an hourly Dutch auction to determine the clearing rate. Borrowers set the maximum acceptable interest rate, while lenders bid for their target yield. Ultimately, all incoming funds accrue interest at a unified market clearing rate. This mechanism ensures instant and fair price discovery, allowing the market to dynamically adjust within a wide interest rate range of 1% to 30%.

Liquidity Providers:

- Figure has successfully "granularized" the private credit market, which was previously accessible only to top-tier financial institutions.

- Ordinary DeFi users can participate in financing global credit assets through this protocol with as little as $100, which is unimaginable in the traditional financial system.

- As of mid-2025, lenders earned an annualized return close to 9% through this protocol, significantly higher than holding the YLDS stablecoin or returns in traditional money market funds. This attractiveness prompted Figure to further extend this model to Layer 1 ecosystems like Solana and Sui, amplifying RWA yield leverage by introducing PRIME, a liquid staking token.

Democratized Prime Protocol:

- To ensure the safety of lender funds, Democratized Prime has established a robust, code-based risk management system.

- Asset Perfection: Utilizes DART technology to achieve perfect security interests, ensuring lenders have indisputable legal and technical recourse to the underlying RWA assets.

- Liquidation Logic: The protocol monitors LTV in real-time. When LTV triggers the 90% threshold, the smart contract automatically initiates an on-chain liquidation process, auctioning the credit assets through weekly BWICs (Bids Wanted in Competition), with proceeds prioritized to repay lender principal. Furthermore, if market liquidity is insufficient to meet redemptions, the interest rate automatically jumps to 30% to force borrowers to deleverage or attract new capital.