SignalPlus晨报专题:债券末日与欧洲央行星期四

各位朋友,欢迎来到 SignalPlus 每日晨报。SignalPlus 晨报每天为各位更新宏观市场信息,并分享我们对宏观趋势的观察和看法。欢迎追踪订阅,与我们一起关注最新的市场动态。

今天的债券市场心情...

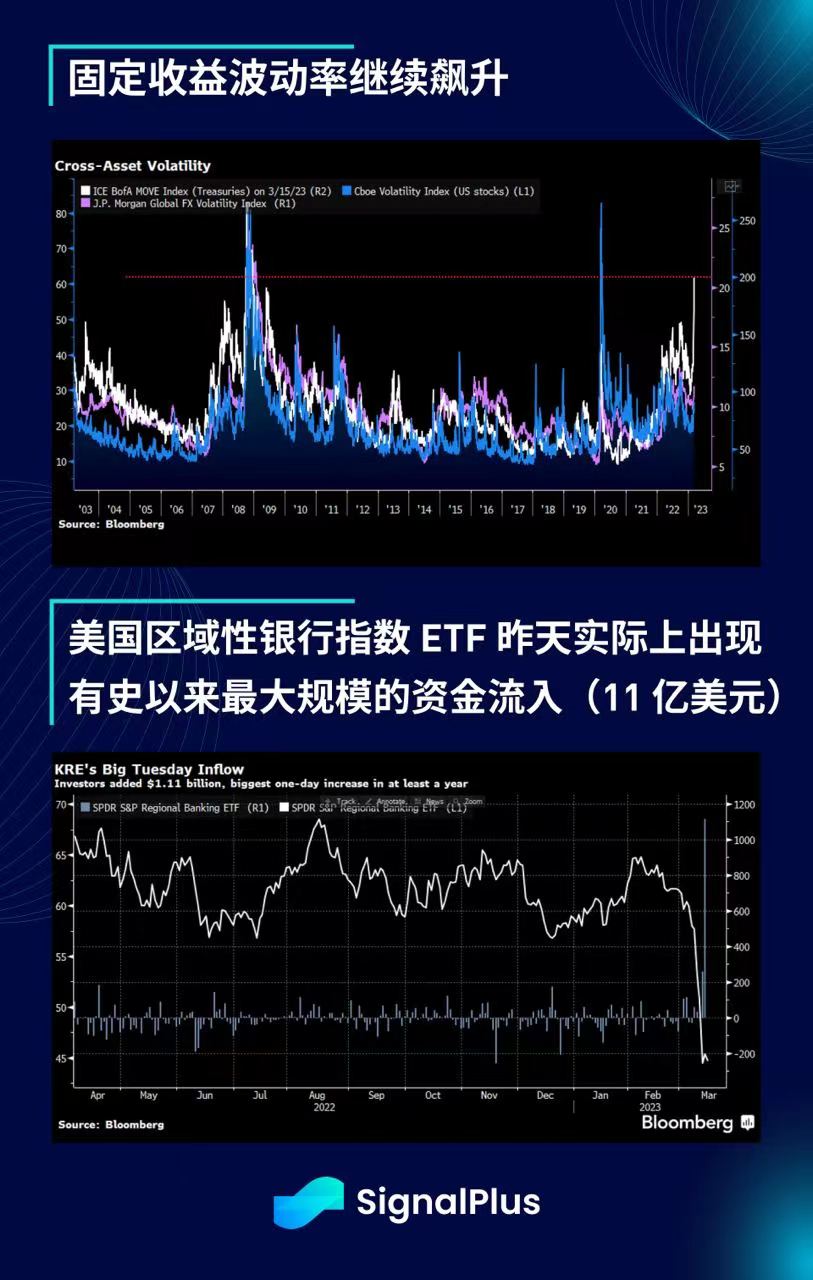

没有刻意夸大,昨天已开发市场的债市流动性完全消失,美国、欧洲和英国的政府债券波动幅度不亚于、甚至超过了雷曼危机的程度。

- 美国国债的买卖价差是平常的 2 倍, 2 年期收益率盘中波动幅度达 70 个基点(相当于 3 次加息), 12 月 23 日欧洲美元盘中波动幅度高达 90 个基点(相当于近 4 次加息),甚至 2/10 s 收益率曲线也出现了 40 个基点的日内波动,实际上,CME 在纽约开盘前后暂停了 6 月 SOFR 合约的交易,这是非常罕见的情况。

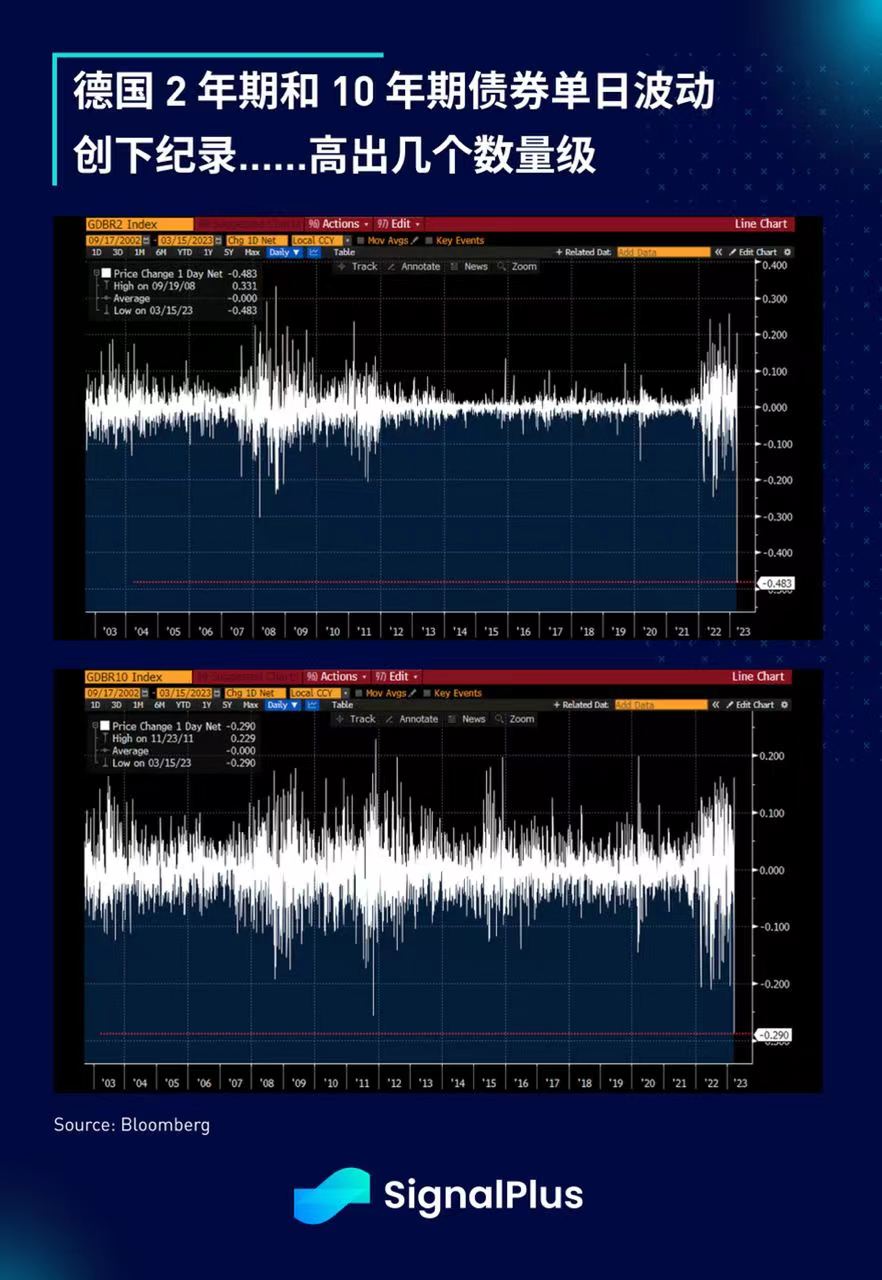

- 德国国债的市场深度彻底崩溃,流动性降至正常水平的 25% ,买卖价差几乎是平常的 3-4 倍, 2 年期收益率当天下跌 48 个基点, 10 年期则下跌 29 个基点,均创下单日记录并轻松超越 2008 年最震荡的时期。

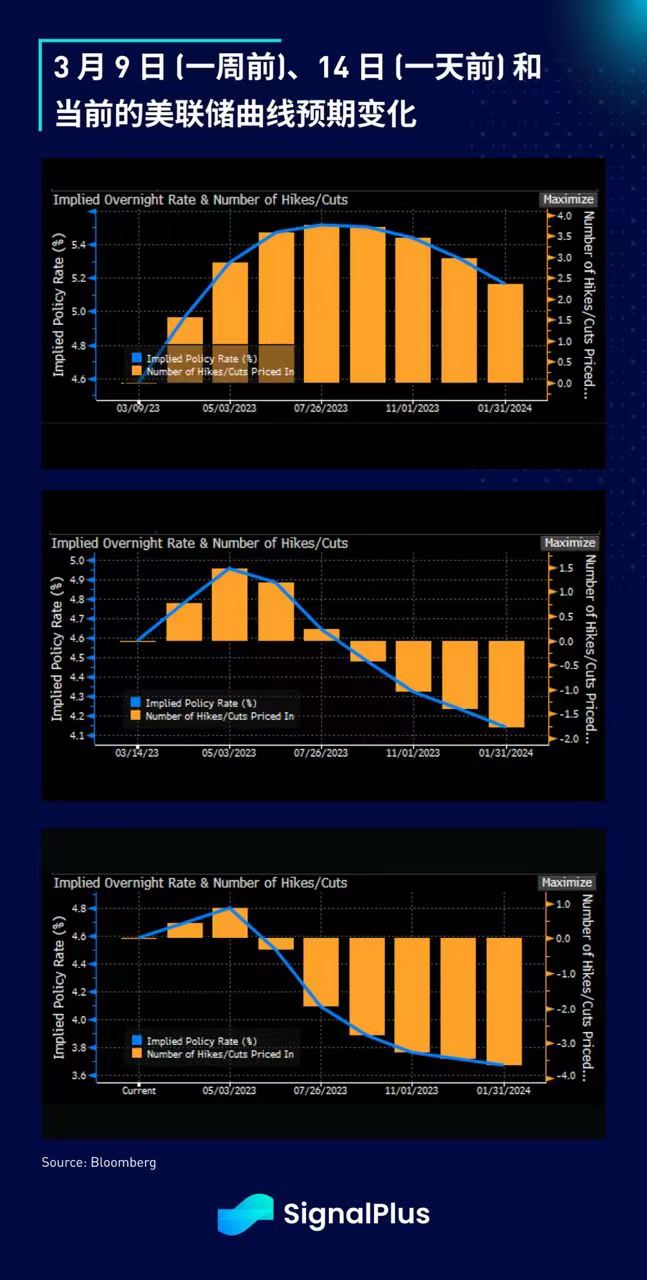

欧洲央行 2 月明确宣示抗击通胀,随后的 CPI 数据也都意外上行,上周的此时市场仍定价欧洲央行将加息 50 个基点,终端利率则徘徊在 4% 左右,短短一周后,随着 SVB 和瑞士信贷事件发生(稍后会有更多细节),终端利率已回落至 3% ,欧洲央行成为第一个在此情况下需要面对货币政策决议的央行。

从根本上说,通胀仍然很棘手,但对银行业系统性风险的担忧也同样重要,有关当局还必须在维护其对抗通胀的信誉以及保持冷静面对当前银行业的压力以避免发出错误信息中权衡,同时又要表现出适当的同情心以表明央行在真正必要时随时可以进行保护,毫无疑问,相较于欧洲央行在接下来 24 小时内面临的挑战,Tom Cruise 的工作可能更容易一些 (下图)。

祝欧洲央行好运

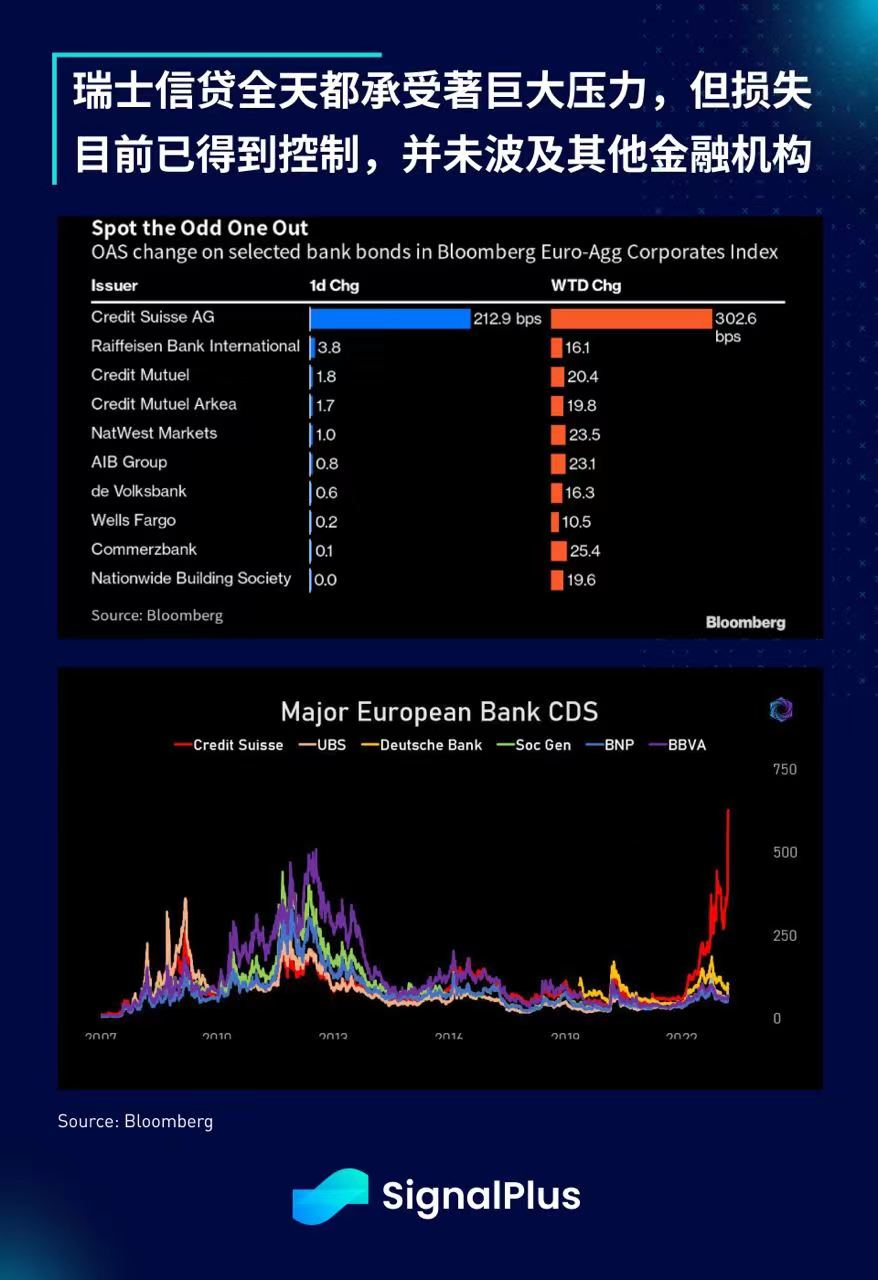

昨天最新受到银行危机波及的是瑞士信贷(CS),该银行在过去十年中一直面临着各种挑战,如今由于对其投资组合损失和流动性的质疑而承受着巨大的压力,随着某些欧洲银行和交易对手公开表明计划降低对 CS 的交易对手风险敞口,该银行迅速寻求 SNB(瑞士国家银行)的帮助,SNB 在交易时段结束前承诺如有必要将提供“流动性”支持,虽然 CS 股价在交易时段结束前收复了大约一半的跌幅,帮助推高整体股价,但 CS 的债券和 CDS 仍然疲软,值得庆幸的是,不像全球金融危机时期那样,到目前为止风险的蔓延仍受到控制,信贷危机没有延烧至其他欧洲金融机构,此外,截至撰写本文时,该行刚刚宣布他们将从 SNB 借款最多 500 亿美元瑞士法郎,以协助管理短期流动性。

回到美国方面,在数据部分, 2 月 PPI 下降了 0.1% ,弱于预期,所有的组成项目都走软, 1 月数据也被下修;2 月零售销售数据下降 0.4% ,汽车除外的销售数据下降 0.1% ,虽然较预期为弱,但在一定程度上被 12 月和 1 月数据的大幅上调所抵消,且对照组环比增长稳定保持在 0.5% 的水平。零售销售数据公布后,亚特兰大联储 GDPNow 模型预测从上周的 2.63% 跃升至 3.15% ,不过纽约联储制造业指数下降至 -24.6 ,明显低于预期,且是连续第 4 个月收缩,特别在就业和新订单部分表现疲软。另一方面,NAHB 房产市场指数创下 2022 年 9 月以来的最佳水平,显示房市依然强劲。

相对平淡的经济数据和欧洲利率带来的伤害导致美债收益率大幅下降,短期 ED 和 SOFR 期货在一天中的大部分时间里更象是加密 altcoin 而不是政府证券。在上周定价加息 50 个基点的机率还高达 60% ,但昨天市场定价 3 月加息 25 个基点的机率一度只有约 30% ,且终端利率已经完全崩溃,利率曲线预期最早将在 6 月开始降息,且圣诞节前将放宽超过 100 个基点。利率重新定价速度之快难以形容,同时美联储也被推到了一个两难的境地,必须在通胀和系统性风险之间做出选择。

随着市场预期会有更多的政府救助和更低的利率,股市实际上保持平稳,收盘和前一天持平,但美联储/欧洲央行最终仍将不得不让某些人失望(而且可能会很失望),我们没有办法想象他们打算如何解决目前的局面。我们仍然倾向认为没有系统性风险,央行将尽可能地选择对抗通胀,而只要能通过流动性支持的手段遏制风险蔓延,即使没有大规模货币宽松政策的支持,股市最终也会稳定下来。

相较于固定收益市场的大屠杀,加密货币市场感觉就像一片平静的绿洲,主要币种价格未能突破高位,隐含波动率也拒绝动摇,与过去几年相比,交易情绪仍相当麻木。在市场经历了艰难的时期之后,交易者似乎不太愿意花费权利金,且宏观形势仍然充满挑战,导致期权参与者的交易还是相对保守。在正面消息的部分,Fidelity Crypto 最近悄然上线,为其 3700 万散户帐户提供一个受监管的加密货币接入点;此外,Cathie Wood 推出了一个新的加密货币开放型基金(ARK Crypto Revolutions);而 Circle 宣布自周一早上以来,他们已经有效地清理了 38 亿美元的大部分赎回要求。

如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web 3 ,或者加入我们的微信群(添加小助手微信:chillywzq)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

Website: https://www. signalplus. com/