SpaceX used an IPO to rewrite the century-old listing process

- Core Thesis: By splitting the three core functions of a traditional IPO (price discovery, distribution & allocation, and share settlement), SpaceX completed its listing using novel public channels such as the semi-public market, prediction markets, and perpetual contracts. This challenged the monopoly of investment banks and revealed that the banks' future core value will shift towards underwriting credibility, share allocation rights, risk assumption, and market stabilization.

- Key Elements:

- SpaceX's IPO broke from tradition: Elon Musk directly set the offering price at $135, bypassing the banks' pricing process. Before the listing, the market had already formed a fair valuation through multiple public channels (e.g., Hiive, Polymarket, Hyperliquid).

- Validation of new pricing channels: For example, when chip company Cerebras went public, the price of the Hyperliquid IPO perpetual contract deviated only 1.3% from the Nasdaq opening price, proving that blockchain-based pricing channels can efficiently predict stock prices.

- Tokenized share settlement revealed custody vulnerabilities: Platforms like Binance failed to secure sufficient shares, leading to a full $557 million refund. The core issue lies in the actual existence of the underlying assets and compliant custody capabilities, not blockchain technology itself.

- Investment bank underwriting fees dropped to 0.67%: The ultra-low fee rate for SpaceX's mega-IPO reflects banks' diminished bargaining power in standardized tasks like price discovery. Their profit model is shifting from service fees to derivative trading commissions generated from securing share allocation rights.

- Banks' remaining irreplaceable functions: These include providing underwriting credibility (e.g., Goldman Sachs and Morgan Stanley each collected $100 million), risk-bearing capacity (fully purchasing the issued shares), and market-making ability to stabilize the market via the greenshoe mechanism. These are functions that on-chain platforms cannot replicate.

Original Author: Prathik Desai

Original Translation: Luffy, Foresight News

An initial public offering (IPO) is a significant ritual in the capitalist system. Company executives embark on multi-week roadshows, pitching business plans to major fund managers to secure institutional investment. Investment banks act as underwriting intermediaries, aggregating market demand, evaluating company valuations, finalizing the offering price, and completing share allocation. On the listing day, the bell is rung, and a private company officially becomes a public company. Subsequently, continuous buying and selling orders in the secondary market compete, establishing price discovery over several hours or days.

The enduring nature of this process—roadshows, pricing, and the bell-ringing ceremony—stems from the core reason that external parties cannot access the real operational data of private companies and must rely on investment banks for pricing. In the past, every company had to fully complete this process to list on an exchange.

However, SpaceX, which recently listed on the U.S. stock market, followed a completely different path to going public. Elon Musk directly set the offering price before investment banks could conduct pricing calculations or roadshows.

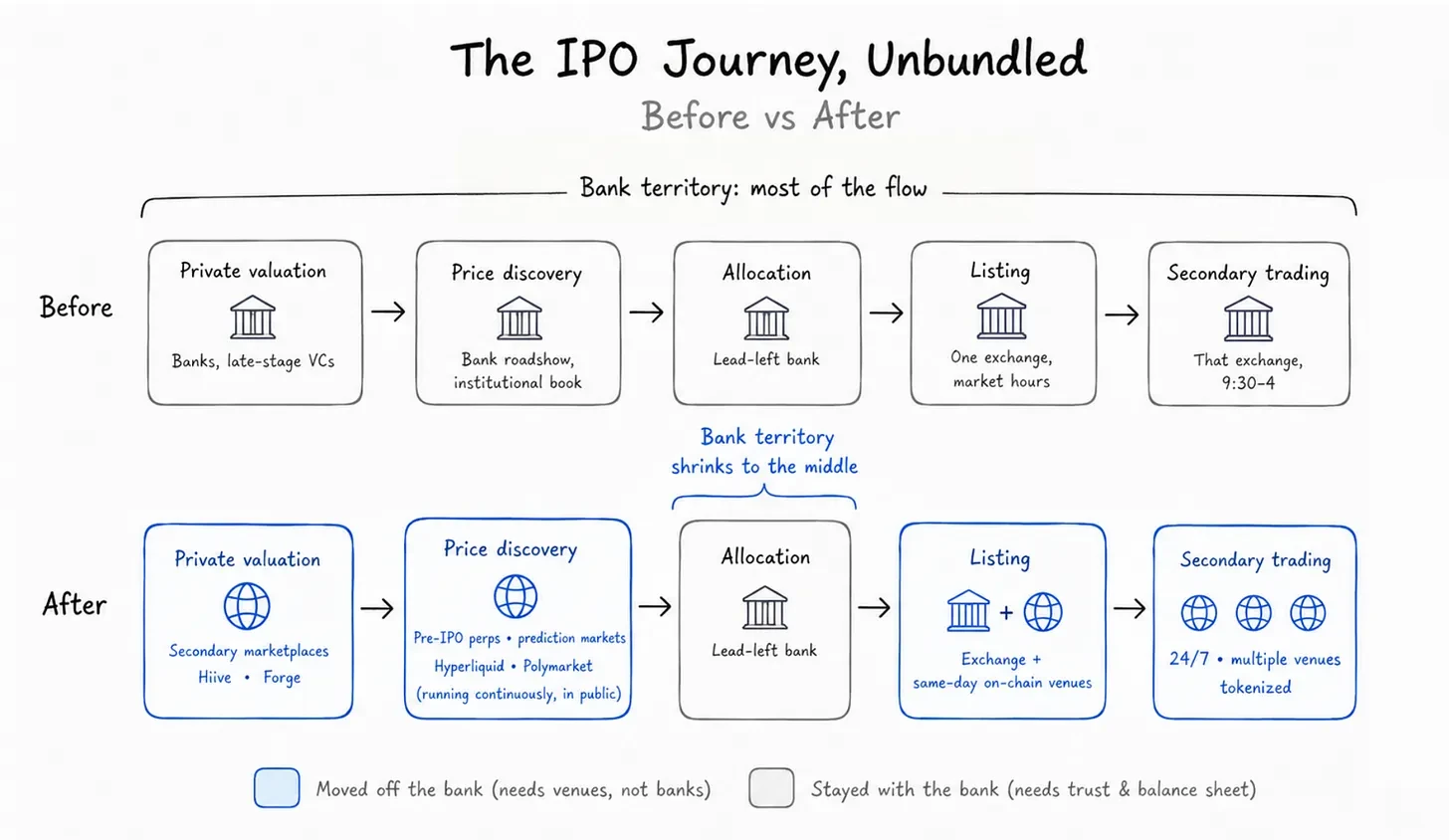

Traditional IPOs bundle three core tasks—price discovery, investor acquisition, and share settlement—into a single package handled by investment banks, which charge a bundled service fee. In contrast, SpaceX’s IPO completely unbundled these three stages, delegating them to different channels independently. Before the investment banks formally began the listing process, the market had already established a fair valuation for the company, and numerous investors were already queuing up to subscribe.

This article deconstructs how SpaceX is changing the way companies go public and the evolving role of investment banks in the new listing environment.

The Origin of Investment Bank Underwriting Fees

Investment banks charge underwriting fees to companies planning to go public. For nearly a century, this fee has typically been calculated as a percentage of the total capital raised by the company.

The complete underwriting process includes: the investment bank organizing global roadshows, collecting indications of interest from institutions and retail investors at various price ranges, determining a market-acceptable offering price, and ensuring the smooth settlement of shares. In a firm commitment underwriting, the investment bank purchases all the shares being offered and then distributes them to subscribing investors.

The long-standing bundling of the three functions—price discovery, distribution, and share settlement—was due to limitations in early market infrastructure. Investment banks were the only institutions with complete market information, making them best suited to assess market demand. They had early access to a company's complete financial data and development plans, allowing for precise stock price calculations. They possessed vast and diverse client resources and cross-industry collaboration channels to distribute shares to top institutions and retail investors, along with mature clearing and settlement systems to ensure proper share delivery.

Consequently, companies planning to go public had no choice but to purchase these bundled services and pay the fees.

The unbundled IPO has completely broken the monopoly of investment banks. Before banks even begin listing preparations, public channels such as perpetual contract trading platforms, prediction markets, and secondary markets for pre-IPO shares already fully display genuine market demand. Companies can now autonomously negotiate underwriting fees and select the most efficient service channel for each stage of the listing.

The average underwriting fee for mid-sized U.S. IPOs is about 7% of the total funds raised, but this rate drops significantly for large projects. For Alibaba's $25 billion IPO in 2014, the underwriting fee was only 1.2%. This time, SpaceX’s underwriting fee was as low as 0.67%. There may be many reasons for such a low rate on the largest IPO in history, but the unbundling of the listing process and the reduction of traditional investment bank roles are certainly among them.

Price Discovery: Investment Banks Lose Pricing Power

SpaceX broke the traditional IPO rules from the preparation stage. In a traditional process, investment banks set a price range, gradually test market acceptance, and ultimately finalize the offering price. In contrast, Musk directly announced a fixed offering price of $135, giving investors the simple choice to subscribe or pass.

SpaceX could skip the investment bank pricing step because the market had already established a valuation weeks before the listing.

Three types of public markets provided different price signals for SpaceX:

- Pre-IPO secondary markets like Hiive and Forge: Employees and early investors traded private shares. SpaceX’s on-platform trading price stabilized around $150, close to its first-day opening price.

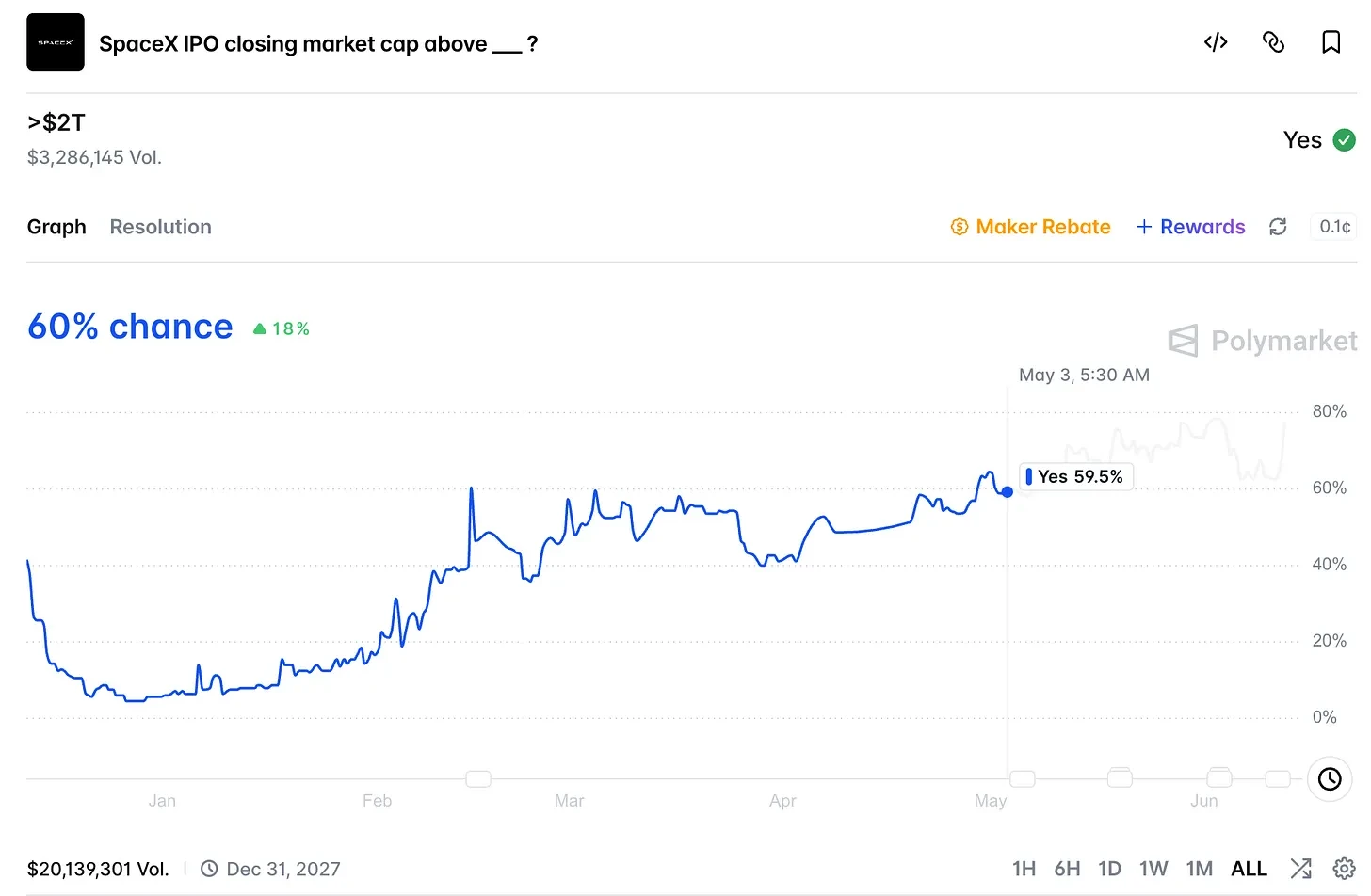

- Prediction market Polymarket: Users bet on the closing price of the first trading day. The highest betting volume corresponded to a company valuation exceeding $2 trillion. On Friday, June 12th, SpaceX officially listed, closing its first day at approximately $161, a 20% increase from the offering price, giving the company a total valuation of $2.1 trillion.

- Hyperliquid Perpetual Contract Platform: Traded synthetic perpetual contracts for SpaceX 24/7, providing a real-time reflection of the market's valuation expectations for the stock.

Before the official listing, these pre-IPO perpetual contracts had no actual underlying stock; they were essentially leveraged bets on the stock's first-day price. The vast majority of positions on the Hyperliquid platform were concentrated in the SpaceX contract. During the morning of the listing day, this perpetual contract traded in the range of $174–$185, a premium of 30%–35% over the $135 offering price. Meanwhile, SpaceX stock hit a high of $176 during the session. After the stock officially began trading on the exchange, the perpetual contract price quickly converged towards the $150 opening price.

Is this mere coincidence? Precedents have already shown the reference value of these new pricing channels. Weeks earlier, when chip company Cerebras went public, the price of its IPO perpetual contract on the Hyperliquid platform differed from its actual Nasdaq opening price by only 1.3%. The spread virtually disappeared once trading began. The market had effectively predicted the opening price even before the company had finalized its offering price.

By leveraging various public trading markets, SpaceX bypassed the first core function traditionally handled by investment banks: price discovery.

Share Settlement: The Tokenization Track Exposes Underlying Custody Vulnerabilities

After pricing, the second core function of traditional investment banks is distributing shares and matching investors. Let's skip distribution for now and deconstruct the third function: share allocation and settlement.

On the day of SpaceX's listing, stock trading was dispersed across multiple platforms, a model completely different from traditional IPOs. On the Solana blockchain, Backpack issued tokens; U.S. regulated entity Kraken launched corresponding products; Ondo issued tracking tokens; Hyperliquid listed synthetic perpetuals, all based on the underlying SPCX asset. Several centralized exchanges like Bitget, Bybit, and Binance also opened IPO subscription channels.

On the listing day, different platforms saw vastly different outcomes.

Products that directly held real shares or were connected to shares through regulated brokerage firms opened on time, with prices tracking the underlying stock. Backpack's Solana tokens were a 1:1 representation of real shares held by a custodian broker. Kraken's U.S. segment connected to the stock via Payward Securities. Ondo provided daily asset custody attestations, ensuring tokens were fully backed by the underlying asset. Hyperliquid's perpetual contracts did not require holding the stock itself, and their prices automatically synced after the stock listed.

Binance, Bybit, and Bitget launched tokenized subscription events. The xStocks platform promised its tokens were fully backed by real stocks. However, these platforms ultimately failed to secure sufficient share allocations. They all issued full refunds; Binance alone refunded $557 million.

The root cause was not blockchain technology itself. Regulated custody channels completed settlements normally. Demand for SpaceX's IPO far exceeded supply, reaching 3.5 to 4 times the $75 billion fundraising target. Centralized exchanges, relying on third-party intermediaries for share allocation, experienced settlement failures and had to fully refund their users.

When price discovery is completely public and freely accessible, pricing ceases to be a scarce, high-value part of the IPO process. The core of the industry competition shifts to the ability to deliver sufficient shares.

The challenge of share settlement is not new. Wall Street faced a similar crisis 60 years ago and built supporting infrastructure to solve it completely.

In the late 1960s, a surge in U.S. stock trading volume, coupled with paper stock certificates, overwhelmed back offices with mountains of paperwork. Every trade required locating, verifying, and physically delivering certificates. The exchange had to close every Wednesday just to handle the backlog. The industry eventually found a solution: eliminating the circulation of paper documents.

The Central Certificate Service was established in 1968 and reorganized into the Depository Trust Company in 1973. All physical stock certificates were deposited into a centralized vault, with ownership recorded solely through bookkeeping entries. By centralizing all assets with a trusted third party, settlement risk was eliminated. The depository could guarantee that sellers held the required shares and that buyers could complete the transfer.

This is the core problem custody infrastructure must solve: whether the seller truly holds the underlying asset and whether the asset transfer can be completed.

The tokenization model faces the same vulnerability. Tokens can be issued early, but the underlying stocks may not be deposited into a regulated custodian simultaneously. If the tokens are backed by real stocks held in a regulated broker's account, settlement is assured. If tokens are sold first without securing the underlying shares, the redemption promise lacks support. This incident in 2026 resulted precisely from platforms selling tokens without being able to obtain the corresponding real shares later.

The future challenge of IPOs will no longer be price discovery, but verifying that the underlying assets exist authentically and can be transferred normally.

What Irreplaceable Value Is Left for Investment Banks?

A complete review of the new listing process shows that the three traditional functions have been siphoned off by external channels.

Pre-IPO market price discovery is no longer monopolized by investment banks. Weeks, even months before listing, pre-IPO secondary markets, prediction markets, and perpetual contract platforms continuously provide public valuations. By the time SpaceX finalized its offering price, these channels had already offered fair market prices.

Listing and trading channels are no longer singular. While SpaceX listed on Nasdaq, multiple on-chain trading channels opened simultaneously. Blockchain supports 24/7 trading, meaning secondary market liquidity is no longer confined to a single traditional exchange.

The core barrier for share settlement is asset custody qualifications. Previously, this capability was exclusively held by investment banks, relying on depository institutions for settlement guarantees. Now, any institution with compliant custody qualifications can undertake this business.

So, what still requires the involvement of investment banks? Currently, they retain four intermediate core functions that are difficult to replace.

First is credit endorsement. The signature of the lead underwriter on the prospectus acts as a credit guarantee for the project, providing a safety net for conservative institutional investors. This industry reputation, built over decades, cannot be replicated by on-chain token platforms. Investment banks charge service fees for this endorsement. SpaceX paid a total of $500 million in underwriting fees, with Goldman Sachs and Morgan Stanley each receiving $100 million, even though these two banks had almost no role in pricing.

Second is share allocation authority. Lead underwriters still hold the decision-making power for allocating the vast majority of shares, autonomously selecting which investors can participate.

Next is risk absorption. SpaceX opted for a firm commitment underwriting. The banks contractually agreed to purchase all the shares offered and then distribute them. If market demand collapses and subscriptions fall short, the unsold shares are absorbed entirely by the investment banks. SpaceX bears no loss. On-chain platforms cannot take on such massive downside risk.

Finally is market stabilization. When stock prices are highly volatile in the early days of listing, the lead underwriter can use the greenshoe option to moderately overallocate shares and then repurchase them from the secondary market to curb extreme price swings. After SpaceX's listing, Morgan Stanley was responsible for post-listing stabilization operations. This activity requires a large balance sheet and a professional market-making team, capabilities currently exclusive to investment banks.

Aside from these, all other aspects of the listing process are being handled by new market channels that are more cost-effective, offer longer trading hours, and are completely transparent.

Blockchain-based pricing channels have validated their value, continuously calculating valuations for companies planning to go public with efficiency far surpassing traditional investment banks. SpaceX's heavily oversubscribed IPO, with a nearly 19% gain on the first day, is a textbook-perfect listing scenario, fully confirming the effectiveness of the new pricing channels.

The traditional IPO model has been completely unbundled. Each function is now handled by the most efficient channel. This kind of division of labor transformation is happening across all industries. As mentioned in the earlier article "Restructuring Private Market Valuations", the market no longer waits for investment banks to value private companies. In the new listing system, investment banks, which once monopolized the two core businesses of pricing and share settlement, can no longer rely on these standardized services to earn high fees.

Will Investment Bank IPO Business Revenue Completely Shrink?

No, it will not. SpaceX's underwriting fee of just 0.67% is not the core source of investment bank revenue.

Calculating based on the first-day gain, SpaceX raised $75 billion, and the paper profit for a single day was approximately $14 billion. The investors who could benefit from this profit were mostly existing clients of the underwriting banks. Investment banks cannot directly speculate and hoard shares for themselves, but they can secure high-quality IPO allocations for their clients, thereby earning substantial trading commissions.

This is the core reason why nearly twenty investment banks competed for underwriting mandates despite the low 0.67% fee. Underwriting fees have become a secondary consideration. The primary drivers for banks to compete for projects are share allocation rights, commissions from client derivative trading, and long-term wealth management business.

The profit logic for investment banks is evolving from standardized, commoditized pricing services to a scarce resource: the channel for accessing IPO share subscriptions.