美股 두 달 만에 16% 급등: 역사상 단 4번뿐, 최근 사례는 1987년 폭락 직전

- 핵심 관점: 미국 증시의 최근 두 달간 16% 상승은 경기 침체가 아닌 상황에서 극히 드문 현상으로, 1987년 '블랙먼데이' 직전에만 유사한 상황이 발생했다. 현재 시장은 신용 시장의 과도한 낙관, 소비자 스트레스 신호 누적, 주식-채권 시장 괴리 심화 등 다중 위험 요인이 존재하며, 테일 리스크가 비정상적으로 두드러진다.

- 핵심 요소:

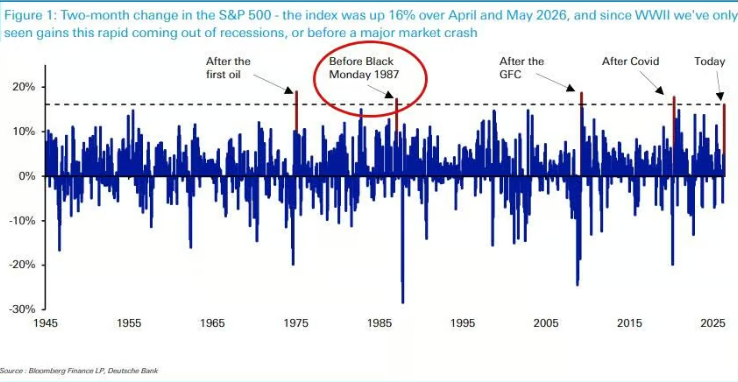

- 역사적 선례: S&P 500이 4~5월 동안 누적 16% 상승한 것은 제2차 세계대전 이후 단 4번뿐이며, 그중 3번은 경기 침체 후 회복기였고, 유일한 비경기 침체 선례는 1987년 폭락 직전이었다.

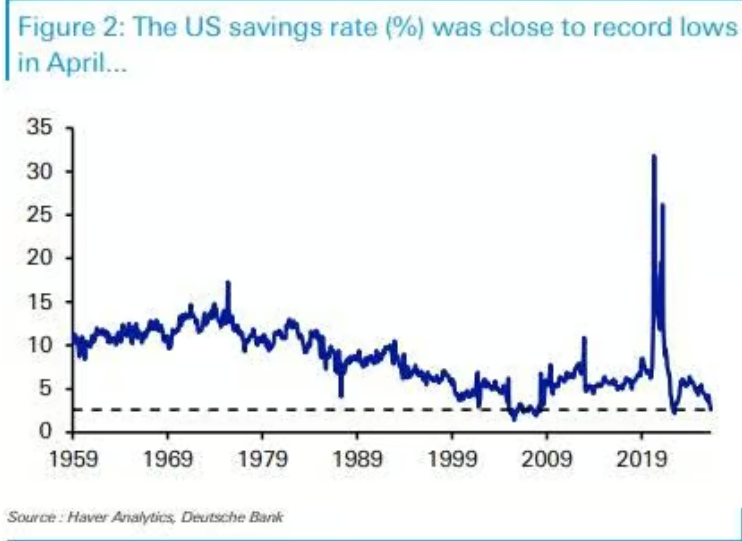

- 소비자 신호: 미국 4월 저축률이 2.6%로 하락, 이는 2022년 및 금융위기 직전과 유사한 수준이다. 5월 미시간 소비자 신뢰지수는 사상 최저를 기록했다.

- 신용 괴리: 미국과 유럽의 신용 스프레드가 갈등 이전 수준보다 낮아졌지만, 이는 중앙은행 금리 인상 기대 및 역사적 패턴(스프레드 확대 예상)과 대조를 이룬다.

- 채권 시장 압력: 10년물 미 국채 수익률은 유가 변동과 독립적으로 압박을 받고 있으며, 30년물 미 국채 수익률은 2007년 이후 최고 수준으로 상승해 주식 시장 고점과 괴리를 형성하고 있다.

- 유가 지지: 호르무즈 해협 봉쇄가 예상보다 심각하지만, 브렌트유 가격은 안정세를 유지하고 있다. 이는 스태그플레이션 가격 결정을 억제하며 위험 자산의 탄력성을 유지하는 핵심 요인이다.

Original Author: Zhao Ying

Original Source: Wall Street News

The strong rebound in US stocks over the past two months is sounding a historical alarm. The S&P 500 index rose by a cumulative 16% between April and May, a gain that has only occurred four times since World War II. Three of those instances happened during post-recession recovery phases, and the sole precedent outside a recessionary backdrop was in the months leading up to the "Black Monday" crash in October 1987.

Deutsche Bank macro strategist Henry Allen points out that the current rally is not occurring in the context of a recovery from a recession, making the historical comparison particularly stark. Meanwhile, credit spreads remain at historically low levels, but pressure signals on the consumer side are accumulating, expectations for a Fed rate hike are heating up, and the divergence between sovereign bond markets and the stock market continues to widen.

With multiple risk factors叠加, tail risks in the market are becoming exceptionally concentrated. Henry Allen wrote in his report, "The tail risk in the current distribution is unusually prominent, whether at the geopolitical or market level."

Rare Historical Precedent, The Only Case Outside a Recession

The S&P 500's two-month gain of 16% from April to May has only four precedents since World War II.

Three of these occurred during strong post-recession rebounds: the recovery after the COVID-19 pandemic from April to May 2020, the rebound from the Global Financial Crisis from March to April 2009, and the recovery rally after the first oil crisis from January to February 1975.

The fourth instance was from January to February 1987. That was just months before the "Black Monday" crash in October of that year—on that day, the S&P 500 plummeted 20% in a single session.

Henry Allen emphasized that while the current rally has fundamental support, including AI enthusiasm and strong economic data, "the pace of the rise itself has already broken all recent precedents." In an economy that is not emerging from a recession, a rebound of this speed has historically never ended well.

Furthermore, the S&P 500 is currently on track to record double-digit gains for the fourth consecutive year, a streak not seen since the late 1990s.

Excessive Optimism in Credit Markets, Consumer Stress Signals Ignored

The strength in the stock market has also spread to credit markets. Credit spreads in both the US and Europe are currently even tighter than before the outbreak of the US-Iran conflict, indicating a high tolerance for risk in the market.

However, warning signs on the consumer front are accumulating. The US savings rate in April was just 2.6%. Historically, such low levels have only been seen in two periods: a single month in 2022 (when excess savings accumulated during the COVID-19 pandemic were being depleted) and on the eve of the Global Financial Crisis. Meanwhile, the University of Michigan Consumer Sentiment Index hit a record low in May since records began in 1952.

The monetary policy environment is also tightening. The European Central Bank is widely expected to raise interest rates this month, and market bets on a Fed rate hike in 2026 are also heating up—US PCE inflation in April was 3.8% year-on-year, providing support for this expectation.

Henry Allen noted that historically, a hawkish Fed stance has often coincided with widening credit spreads, as seen in 2022, late 2018, and 2015-2016. The current calm in credit markets diverges significantly from this historical pattern.

Bond Market Under Pressure Alone, Divergence from Stocks Widens

While stock and credit markets show high immunity to geopolitical risks, sovereign bond markets have taken a distinctly different path.

Over the past month, the yield on the 10-year US Treasury note has almost completely followed oil price movements, clearly decoupling from other asset classes. In mid-May, sovereign bond yields hit multi-year highs: the 30-year US Treasury yield rose to 5.18%, its highest since 2007; the 10-year German Bund yield rose to 3.19%, its highest since 2011.

At that time, stocks were just a step away from all-time highs, while bond yields were at levels not seen for over a decade. This divergence has shown no signs of convergence since.

Henry Allen believes that bond markets, which more directly price inflation and fiscal risks, are more sensitive to geopolitical shocks. The persistent divergence between stocks and bonds is itself a manifestation of the current market fragility.

Unexpectedly Stable Oil Prices, A Key Pillar for Risk Assets

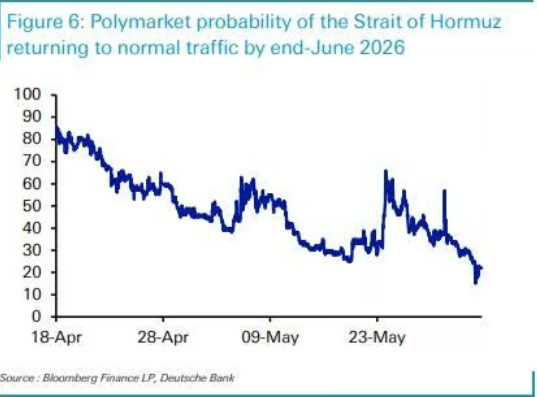

The blockade of the Strait of Hormuz has lasted far longer than the market initially expected, but the reaction of oil prices has been surprisingly mild, which partly explains the resilience of risk assets.

When the US-Iran conflict erupted on February 28, the White House initially estimated the operation would last 4 to 6 weeks. However, to date, the Strait of Hormuz remains blocked. According to data from the prediction market Polymarket, the probability of a return to normal navigation by the end of June has plummeted from around 80% in mid-April to 22%.

Despite this, the oil futures curve remains relatively stable. Just two weeks after the conflict erupted on March 13, the 6-month Brent crude futures contract settled at $85.66 per barrel; by June 1, the contract was trading around $84.88, virtually unchanged.

Henry Allen points out that it is precisely because the oil futures curve has not shifted significantly higher that investors have not priced in severe stagflation risks, thus avoiding a larger-scale sell-off in risk assets. However, he also warns that if the Strait of Hormuz remains blocked, it remains uncertain whether this support can be sustained.