AI 산업 혁명, 우리는 지금 어디에 있는가

- 핵심 관점: 현재 AI 분야는 여전히 '구 공장에 새 기계를 설치하는' 초기 단계에 머물러 있으며, 진정한 변혁의 전환점은 아직 오지 않았다. 기업의 핵심 과제는 기술력 부족이 아니라, 산업 혁명 당시 공장주가 수력 방앗간을 떠나 동력 공장을 새로 지었던 것처럼, AI를 중심으로 생산 방식을 완전히 재구성해야 한다는 점이다. 미래의 핵심 자산은 산업에 깊이 통합된 워크플로와 고유 데이터에 있으며, 조직 형태와 개인의 경력 경로 모두 재편될 것이다.

- 핵심 요소:

- 기존 애플리케이션은 여전히 '물레방아 교체' 수준: 대부분의 조직은 AI를 기존 도구에 챗봇 형태로만 부착할 뿐, 이를 중심으로 워크플로를 재설계하지 않아 절약된 시간이 기존 프로세스에 소모된다. AI 도입은 '도구 업그레이드'와 '공장 재건' 사이에 갇혀 있다.

- 인프라 투자 과열은 위험을 수반: AI 인프라 자본 지출은 막대하며(2026년 예상 7650억 달러), 이는 1840년대 철도 열풍과 유사하다. 위험은 범용 컴퓨팅 파워는 과잉 공급되지만, 고부가 가치 영역(예: 금융 규정 준수)을 충족하는 전문 역량은 부족해 API 가격 하락이 투자 수익률을 무너뜨릴 수 있다는 점에 있다.

- 조직 변화의 선구자들은 이미 움직이고 있다: Notion과 YC 같은 기업들은 이미 '공장을 허물기' 시작했으며, AI 에이전트를 통해 팀 협업을 재구성하고(Notion은 700개 이상의 에이전트 보유), '재귀적 자기 개선' 조직 모델을 추진하고 있다. 관리자의 역할이 AI로 대체되면서, 기업은 조직의 두뇌를 형성하기 위해 AI에 '읽을 수 있는' 상태가 되어야 한다.

- 컨설팅 회사는 핵심적인 '철도 엔지니어' 역할을 수행: Anthropic은 KPMG, Accenture 등과 제휴하여 대기업이 기존 프로세스를 철거하고 AI를 중심으로 생산 라인을 재구축하도록 돕고 있다. 이들 거대 기업은 단순한 기술 사용자가 아니라 조직 변화를 촉진하는 촉매제가 되고 있다.

- 초급 직위가 압박을 받고 있다: 데이터에 따르면 22~25세에 AI 노출도가 높은 직종에 진입한 청년의 고용 확률은 동년배보다 14% 낮으며, 이는 초급 직위가 AI로 대체되거나 재편되고 있음을 시사한다. 개인이 가진 기존의 '물레방아'(예: 학력, 경험)는 가치가 하락하고 있다.

- 새로운 형태의 조직은 '인간-머신 협업'을 중심으로 구축된다: 미래 기업은 '인력 감축이 아닌 토큰 소모'를 논리로 삼을 것이며, 인간의 핵심 가치는 오프라인 판단, 전혀 새로운 상황 및 감정적 의사 결정으로 이동하고, AI 에이전트가 실행과 정보 흐름을 담당할 것이다. 기존의 위계 구조는 무너지고, 개인은 자신이 '철도 노선을 따라 서 있는지' 확인해야 한다.

Original Author: Will Awang

Over the past year, I attended several AI-themed industry conferences. Speakers on stage took turns demonstrating AI's latest tricks, while people in the audience held up their phones to capture the screen, posted it on their Moments, and then scrolled through their phones again. But back at the office, it was the same weekly meetings, the same approvals, the same weekly reports. Big tech companies have already written token consumption into KPIs, with some people scripting automated calls to become model workers. The same crowd on social media—today it's a Claude revolution, tomorrow Codex is amazing, the day after Gemini is hailed—are they truly embracing a revolution, or just rushing to the next big thing?

This is all noise, not the answer I'm looking for.

The real question isn't whether AI is powerful enough—the steam engine has already been built. The question is who will be the first to dismantle the old workshop.

The day the Industrial Revolution truly began wasn't when Watt improved the steam engine; it was when a factory owner in Lancashire decided to move away from the river and rebuild the workshop around the steam engine. The most important moment for AI will be the same—not the day the large model was invented, but the day the first organization decides to tear down the old processes and rebuild the mode of production around AI. That day hasn't arrived yet. But it's on its way.

Two people saw this coming early on. Notion CEO Ivan Zhao wrote "Steam, Steel, and Infinite Minds" in late 2025, offering a cold assessment: we're still in the "replacing the water wheel" phase—adding AI chatbots to existing tools, but no one is redesigning the factory. Leopold Aschenbrenner, a former OpenAI employee, took a different path: he wrote the 165-page "Situational Awareness," then built a fund that grew from $225 million to $13.68 billion, all-in on AI infrastructure. One looks inward; the other bets outward.

This article isn't about them. It's about us—where we stand now, and which part of history we are repeating.

(Power-loom weaving, engraving by J. Tingle after Thomas Allom, 1835 / Wikimedia Commons )

I. The Workshop is Still Old

This is how most people's day goes: In the morning, they use AI to write an email, saving ten minutes; then they spend two hours in a weekly meeting that didn't need to happen; in the afternoon, they copy and paste the same set of data between three different tools; in the evening, they post on social media, saying "AI is amazing." The ten minutes saved are completely consumed by the old processes.

Similarly, when the steam engine appeared, factory owners initially just replaced the water wheel with a steam engine, leaving everything else unchanged—the factory was still built by the river, still a multi-story building, still using a central drive shaft to power the entire production line. We put ChatGPT into Slack, add Copilot to Office, embed AI chat windows into workflows—we are doing the same thing. The tool has been upgraded, but the workshop hasn't changed.

But replacing the machine doesn't mean changing the workshop. McLuhan put it well:

We drive into the future using only our rearview mirror. Fitting new tools into old processes is like early films merely being recorded stage plays. The true breakthrough only comes when someone completely frees the steam engine from the river, redesigning the entire mode of production around the new power source.

Comparing the timeline of the Industrial Revolution with that of AI helps us roughly locate where we are on the map:

The timeline today is extremely compressed. It took 60 years from the steam engine to the railway mania in the Industrial Revolution; it took only 7 years from the Transformer to the AI data center construction boom.

Speed isn't the issue. The issue is where we are stuck—the first four rows all represent the stage of putting new machines into old workshops. The steam engine is installed, the railways are being laid, but the mode of production remains unchanged. The sixth row is the true watershed. We are likely stuck somewhere between these two steps.

We have the steam engine in hand, but the workshop is still old.

II. All the Money is Piled on the Layer Furthest from the Factory

Infrastructure is always overbuilt. In the end, it's the investors who go bankrupt, not the infrastructure.

In 1846, the British Parliament passed 263 railway acts, approving the construction of 9,500 miles of new railways. At its peak, railway investment accounted for 13% of UK GDP. Railway shares could be bought with just a 10% deposit, and the middle class flocked in. The bubble burst in 1847. One-third of the approved lines were never built, and countless investors lost everything. Darwin lost 60% on his railway stocks, and he was much luckier than most.

But the railways stayed.

Today's AI infrastructure is following the same path. Goldman Sachs estimates global AI infrastructure capital expenditure will reach $765 billion in 2026, projected to be $1.6 trillion annually by 2031. The ratio of capital expenditure to operating cash flow for the hyperscale cloud providers has risen from about 40% in 2023 to nearly 70% in 2025. AI-related investments now account for roughly a quarter of all U.S. investment. Aschenbrenner's $13.68 billion bet on this layer—he isn't betting on which application will win, but on the underlying computing power itself.

This capital cycle is isomorphic to real estate development. Building a data center is like building a building: land is power, building materials are GPUs and storage, the contractors are the data center construction companies, the developer is the cloud provider, the tenants are AI application companies, and the rent is API revenue. The cloud provider's business model is to pay for the building with rent—using API revenue to cover the capital expenditure of data centers, waiting for the valuation leap brought by the explosion of AI applications.

(Computing Power as Real Estate: Each generation has its own infrastructure)

The core risk is the same: Is the rate at which API unit prices are falling being offset by the growth rate of call volume? What if rents fall below the loan repayment line—this is the most familiar nightmare for real estate developers. The lesson from 2008 wasn't that too many houses were built, but that the houses built didn't match the structure of real demand. The equivalent risk for AI is: an oversupply of general-purpose computing power, but specialized capabilities that can truly handle high-value scenarios like financial compliance or medical diagnosis remain scarce.

Railways, real estate, AI—infrastructure investment across three eras shares the same rule: overbuilding is the norm, building material suppliers always lose pricing power, and long-term returns always belong to the owners of "prime locations." Just look at the holdings of Wall Street's Q1 funds—they're likely 80% concentrated in this infrastructure layer: NVIDIA, data centers, cloud infrastructure. But the railway mania taught us: this isn't the full picture of the AI revolution, nor is it even the layer with the highest returns.

What is the "prime location" for AI? It's unique industry data and deeply embedded workflows. For an individual, the real "prime location" isn't the stocks they hold, but their irreplaceable judgment and industry knowledge—provided they have already rebuilt the way they use them around AI.

The real returns are in the next layer. But the transition from infrastructure to value creation isn't seamless. There is a gap in between—historically, this gap has swallowed up decades.

III. Who is Dismantling the Workshop

Those who dismantle the workshop and those who "use AI to improve efficiency" are not doing the same thing.

Ivan Zhao's co-founder, Simon, used to be a "10x programmer"; now he rarely writes code himself—he simultaneously controls three or four AI coding agents, achieving 30 to 40 times efficiency. Notion now has 1,000 employees and over 700 AI agents. The gap isn't the tool; Simon dismantled his own old workshop, while most people just upgraded their water wheel.

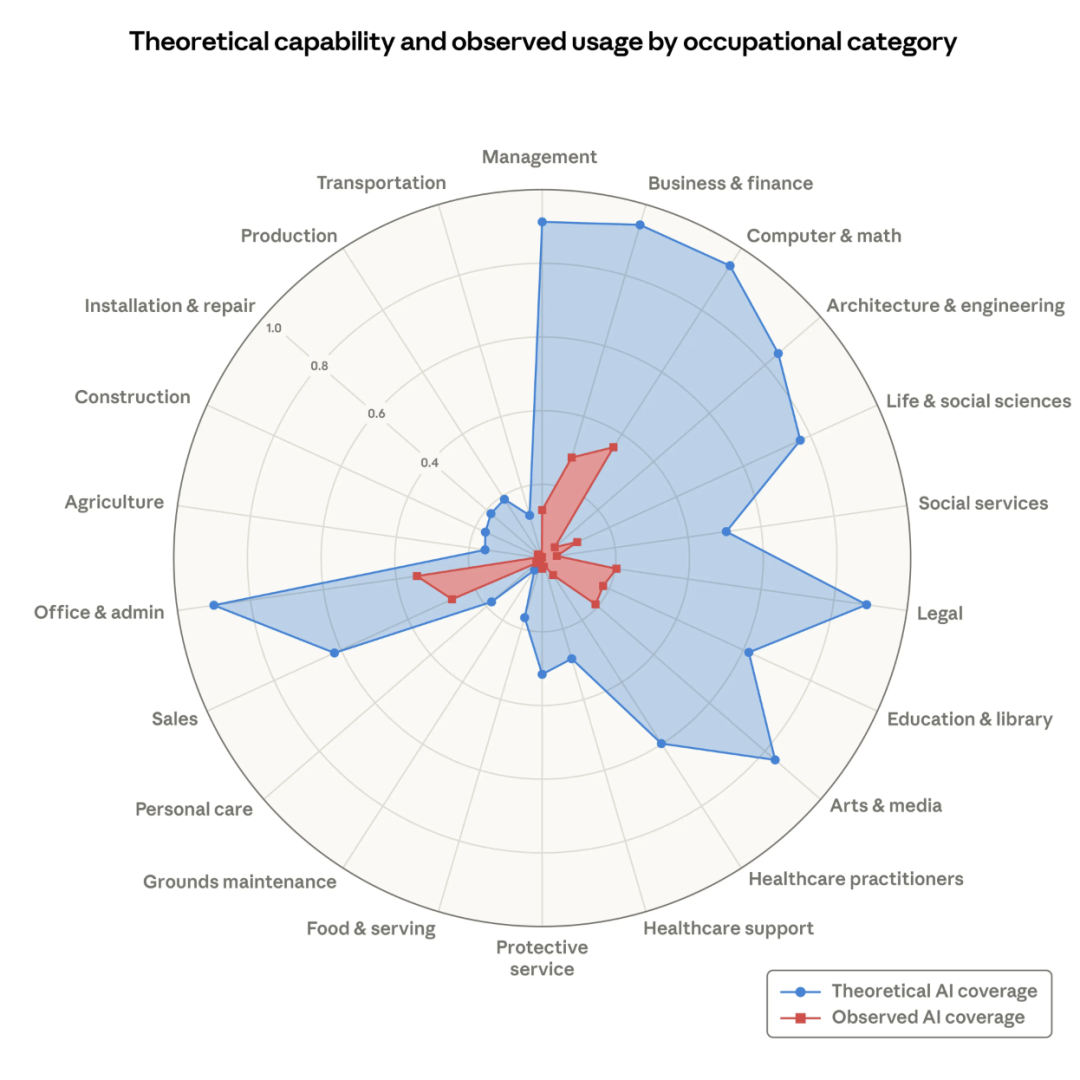

600 million Chinese users have used generative AI tools, a 142% year-over-year increase—making this the world's largest AI demand pool. Yet, almost no Chinese company has rebuilt its core workflows around AI. The world's largest demand side, paired with a supply-side organization that is practically static. This contrast itself is a signal: it's not that the tools are insufficient, it's that the organization hasn't kept up. The context of knowledge work is scattered across dozens of tools and dozens of people's minds, output is unverifiable, and no one knows how to judge whether a strategic memo is effective.

(Labor market impacts of AI: A new measure and early evidence)

Anthropic has already started making moves on a larger scale. They released the Economic Index, using real usage data to map which tasks and industries AI is replacing first, and then building according to this map: they formed a joint venture with Goldman Sachs, Blackstone, and Hellman & Friedman to create an AI-native enterprise service company; established a global alliance with KPMG, connecting 276,000 employees to Claude; Accenture formed a business group, training 30,000 people, focusing on finance, life sciences, and healthcare.

These consulting firms aren't playing the role of AI users; they are AI's railway engineers—they don't build the steam engines or lay the tracks, they help companies tear down the old factories and rebuild production lines around the new power source. Without this role, most factory owners wouldn't know where to start.

Signals are already flashing. The sharpest one comes from the job market.

Young people aged 22-25 entering occupations with high AI exposure are 14% less likely to find a job compared to their peers entering low-exposure occupations. Entry-level positions are already being squeezed.

If I were a new graduate, this number would directly affect my job search. If I were a manager, the next batch of entry-level positions I hire for might no longer be filled by humans.

Organizations are dismantling. What about individuals? My education, my resume, the industry experience I've accumulated over the years—these are my water wheels. They once powered my entire production line, but the steam engine has arrived. A degree from a top university is no longer a moat; it only proves I once built a decent factory by the river.

Now the question is, do we have the ability to leave that river?

Anthropic's data shows that users who have used AI tools for more than 6 months have a 10% higher task success rate than new users. Those who started half a year earlier already have a 10% lead, and this gap will compound over time.

But so far, no company has gone bankrupt for not using AI—my law firm, at least, is still making great strides centered around AI. The winners haven't been chosen by the market yet. The learning curve is real—those who started earlier are already accumulating advantages, but most people are still at the starting point.

IV. My Next Job Title Doesn't Have a Name Yet

Will my current job title still exist in ten years? How many of the tools I used daily five years ago are still around today? The answer to both is likely no. But I don't know what will replace them—because those things don't exist yet.

History repeats itself every time. New things aren't planned; they grow organically after old constraints disappear.

Before the railways were built, Britain was a collection of isolated local economies. The price of cotton cloth in Manchester could differ by 30% from London. Every city had its own local time standard, and no one thought it was a problem. Within twenty years of the railways being built, everything changed. A unified national market appeared for the first time, and price differences were flattened. Standard time was forced into existence by the railways, not invented. Station masters, telegraph operators, travel agents—these jobs simply didn't exist before the railways.

No one foresaw department stores when laying tracks. No one foresaw standard time when building the steam engine.

(Steam, Steel, and Infinite Minds)

The history of cities tells the same story. Cities from centuries ago were built on a human scale—a forty-minute walk could take you across Florence. Steel frames made skyscrapers possible, railways connected cities and their hinterlands, and elevators, subways, and highways followed. Tokyo, Chongqing, Dallas—these aren't just larger versions of Florence; they represent entirely new ways of living.

Today's knowledge work is also on a human scale. Teams of a few dozen people, paced by meetings and emails, become overwhelmed beyond a few hundred. We are building Florence with stone and wood. AI makes "Tokyo" possible—organizations consisting of thousands of AI agents and employees, with workflows running continuously across time zones. The old weekly meetings, quarterly plans, and annual reviews may no longer make sense.

Simon doesn't write code anymore—his job has become "managing AI agents." This position didn't exist two years ago. My next job title probably doesn't have a name yet. But some people are already building that future, even if we can't name it yet.

V. What the New Workshop Looks Like

After dismantling the old workshop, what do you build? YC's answer is: let the company improve itself.

Their internal system now rewrites its own code at night. One day, an employee ran a query during the day, and it failed. A supervisory agent read this failure, deduced the cause, wrote code to fix it itself, submitted it for review, and deployed it. The same query worked the next morning. All of this happened while everyone was asleep.

This isn't AI helping humans produce 30% more. This is the system completing an entire loop on its own, figuring out how to get better by itself.

YC partner Tom Blomfield, in an internal talk, called this company form a "recursively self-improving AI loop." His assessment was direct: most companies are still like Roman legions—orders passed down layer by layer, information reported up layer by layer, with humans acting as conduits of information. AI doesn't just break the efficiency of a single link; it breaks the very premise that this whole hierarchical structure exists.

His new logic is: burn tokens, don't burn heads. The bottleneck is shifting from human power to computing power. The data YC sees is that in the batch of companies reaching Demo Day, revenue per employee is about 5 times higher than 18 months ago. The role of middle management is being taken over by AI—"coordination" no longer requires humans. Everyone should be an IC, a builder, an operator. Every task should have a named person responsible, not a committee.

There is also