十年 투자 Cerebras: '웨이퍼 레벨 AI 칩'이 나스닥에 오르는 방법

- 핵심 견해: 본 기사는 Cerebras의 초기 투자자가 작성했으며, 2014년 구상부터 2025년 IPO까지 19년에 걸친 협력 과정을 되돌아봅니다. Cerebras의 성공이 AI 컴퓨팅 아키텍처의 근본적인 재구성에 대한 선견지명, 웨이퍼 레벨 칩의 시스템 공학적 난제를 해결하려는 결단력, 그리고 투자자와 창업 팀 간의 거래를 초월한 장기적 신뢰 관계에 기반하고 있음을 밝힙니다.

- 핵심 요소:

- Cerebras는 2025년 5월 14일 나스닥에 상장했으며, 상장 첫날 종가가 공모가 대비 약 68% 상승하여 2026년 이후 가장 주목받는 AI 하드웨어 IPO 중 하나가 되었습니다.

- 2014년 AI와 GPU가 아직 보편적인 합의가 아니었던 상황에서, 팀은 제1원칙(First Principle)에 기반하여 메모리 대역폭이 AI 연산력의 핵심 병목이며 GPU 아키텍처가 최적의 해결책이 아니라고 판단했습니다.

- Cerebras는 업계의 관성과 반대 방향을 선택하여 면적이 46,000 제곱밀리미터(기존 칩의 58배)에 달하는 웨이퍼 레벨 칩을 개발했으며, 이를 위해 전력 공급, 방열, 전기적 연속성 등 일련의 공학적 난제를 새롭게 해결해야 했습니다.

- 팀은 SeaMicro의 핵심 멤버(Andrew Feldman 등)로 구성되어 수십 년간의 칩 및 시스템 경험을 보유하고 있으며, '승수 효과'와 같은 능력 조합으로 반도체부터 소프트웨어까지 전방위적인 도전에 대응하고 있습니다.

- 팀 문화는 규율, 인내, 신뢰를 강조하며, 초기 직원 중 약 100명이 창업자를 따라 여러 회사를 거쳐 왔을 정도로 장기적이고 비거래적인 업무 관계를 반영합니다.

- 창업자의 원동력은 점진적 개선이 아닌 '1000배 도약'을 실현할 가치가 있는 문제를 해결하는 데서 비롯되며, 노벨상 수상자와의 교류 등 성장 환경이 '똑똑하고 선한' 가치관을 형성했습니다.

- 투자 과정은 장기적인 관찰과 깊은 신뢰를 기반으로 했으며, 투자자는 만우절에 담장을 넘어 직접 조건표(term sheet)를 전달할 정도로 자본의 인내와 파트너십의 중요성을 보여주었습니다.

Original title: Reflections on a decade with Cerebras

Original author: Steve Vassallo

Original translation: Peggy, BlockBeats

Editor's note: On May 14, Cerebras officially listed on Nasdaq under the ticker CBRS. Closing its first day up about 68% from its IPO price, it became one of the most closely watched AI hardware IPOs since 2026.

This article, written by Steve Vassallo, an early investor in Cerebras, reflects on his nineteen-year partnership with Andrew Feldman, spanning from SeaMicro to Cerebras. On the surface, it tells the venture capital story from term sheet to IPO. In reality, it chronicles how a cutting-edge hardware company, during a period when consensus was against it, bet on a fundamental restructuring of AI computing architecture. From wafer-scale chips and memory bandwidth bottlenecks to a series of engineering challenges in power delivery, cooling, and electrical continuity, Cerebras faced not just singular technical hurdles, but the reinvention of an entire modern computing system.

What is most noteworthy is not that Cerebras ultimately built a wafer-scale chip 58 times larger than traditional chips, but that the company chose a path opposite to industry inertia from the very beginning. When GPUs became the default answer for AI training, it sought to redefine "what a computer built for AI should be." This required not only technical judgment and patient capital but also a long-term, non-transactional trust relationship between investors and the founding team.

For today's AI hardware competition, Cerebras's significance lies in reminding the market that the computing revolution is not just about stacking more GPUs; it can also stem from reimagining the computing architecture itself.

The following is the original text:

On Friday, April 1, 2016, I sent Andrew Feldman an email telling him I would climb over his backyard fence and personally deliver the term sheet for our investment in Cerebras to his hands.

It was April Fools' Day, but I wasn't joking.

Strictly speaking, this is not standard operating procedure for a venture capital firm. But by then, I had known Andrew for nine years and had been discussing his next company with him for nearly two years. I wasn't going to miss out on this deal just because of a few sentences in a term sheet being revised repeatedly on a Saturday afternoon.

I first met Andrew in October 2007. He and Gary Lauterbach had just founded SeaMicro. I didn't invest in that round, but I connected with them deeply, especially admiring their way of thinking from first principles. I've kept an eye on them ever since.

Truly valuable relationships take time to mature. The same goes for truly valuable companies. Today, from the outside, Cerebras is a ten-year-old company about to go public. But to me, it's a nineteen-year relationship finally reaching the moment of ringing the bell.

August 2019. Andrew and I at the Hot Chips conference on the Stanford campus. At that event, Cerebras unveiled the first-generation Wafer-Scale Engine.

Deep Relationships and Unreasonable Ambition

When AMD acquired SeaMicro in 2012, I had a hunch: Andrew wouldn't stay long at a big company. He possesses a fierce competitiveness and a rebellious spirit. By early 2014, he was already looking for an exit, and we began meeting frequently to discuss what might come next.

At that time, two things were far from being consensus: first, that AI would actually become useful; second, that GPUs were not the ideal computing architecture for AI.

Regarding the first point, many smart people I knew disagreed. After AlexNet emerged in 2012, some corners of the research community were already achieving near-magical results with convolutional neural networks. But in the broader software industry, AI still hovered between a marketing buzzword and a research project.

The second point, the hardware issue, was barely even raised. GPUs had become the default choice for neural network training, mainly because researchers had stumbled upon the fact that they were "less bad" than CPUs. Building a new computing system specifically for AI workloads meant challenging the dominant architecture used by researchers worldwide.

But Andrew, Gary, and their co-founders Sean, Michael, and JP saw a different direction. They each had decades of accumulated experience in chips and systems: Gary's background included pioneering work in dataflow and out-of-order execution from the 1980s; Sean focused on advanced server architecture; Michael was responsible for software and compilers; JP specialized deeply in hardware engineering. They were an exceptionally rare group: individually brilliant, but with a multiplicative effect when combined. They could envision a completely new kind of computer.

They believed that if AI truly unlocked its potential, the resulting market size would far surpass the sum of all existing computing forms.

They also saw the nature of the GPU: originally a chip designed for graphics processing, temporarily promoted to an AI training tool for a new battlefield. While better than CPUs for parallel processing, if one were designing from scratch for AI workloads, no one would design a GPU-like architecture. The real bottleneck limiting neural networks wasn't raw compute power, but memory bandwidth. This meant the chip they needed to create should optimize not for matrix multiplication within isolated cores, but for the efficient flow of data throughout the entire computing structure.

Internally, investing in Cerebras was far from a consensus decision. Several of my partners had witnessed the previous wave of semiconductor investments yielding mostly losses and were very frank about their concerns. But ultimately, we reached an agreement as a team. That weekend in April 2016, we made it clear to Andrew: We want to be the first investor to give him a term sheet.

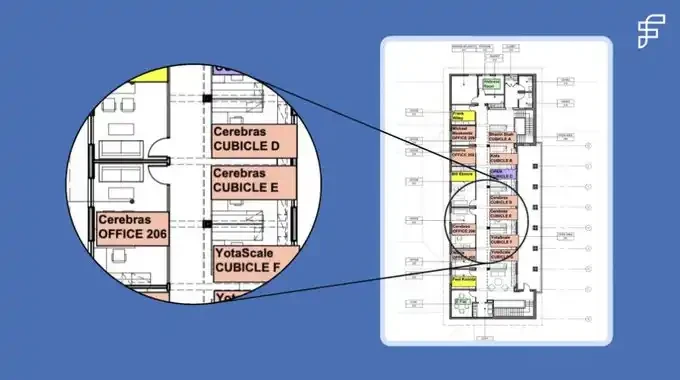

A few weeks later, Andrew, Gary, Sean, Michael, and JP moved into our EIR office space on the second floor at 250 Middlefield. I still have the floor plan the office manager drew then. On that plan, Cerebras sat next to one of Foundation's founders, just a few doors away from Bhavin Shah, who later founded Moveworks. It was a floor conducive to startup growth.

Cerebras's first headquarters, located on the second floor of our old office at 250 Middlefield.

Knowing Which Rules to Bend and Which to Break

Before Cerebras, the largest chip in computing history was about 840 square millimeters, roughly the size of a postage stamp of silicon. The chip Cerebras made was 46,000 square millimeters, 58 times larger.

Choosing a wafer-scale chip meant accepting all the downstream design challenges that followed. In nearly 80 years of computing history, no one had truly succeeded in making this work. This meant no one had systematically solved these problems: how to power such a massive chip? How to cool it? How to maintain electrical continuity across tens of thousands of connection points?

To achieve wafer-scale computing, Cerebras had to essentially reinvent nearly every aspect of modern computing simultaneously: semiconductors, systems, data structures, software, and algorithms. Each direction alone could have been a startup. Andrew and his team chose to start by tackling the most difficult technical problems head-on. With their intense, almost tireless effort, they pushed through these problems one by one.

We held board meetings every six to eight weeks. They would brief us on their attempts since the last meeting: a new system design variation, a new power solution, or a thermal management adjustment. Repeatedly grappling with systemic problems from every angle, they developed a hard-earned clarity of expression. They would explain where they thought things went wrong and what they planned to try next.

We would ask questions and then work deeply with the team, mobilizing the necessary people, resources, and relationships to help them find new breakthroughs. Six to eight weeks later, when we met again, the story would repeat with another technical problem: another frontier to explore. Each solution revealed the next problem that had to be solved.

Their first prototype wafer smoked the moment it was powered on for the first time. The team called it a "thermal event"—a common euphemism for a fire when you don't want to alarm the board or the landlord.

I was constantly calculating the power per square millimeter, partly out of curiosity, partly because the numbers seemed too high to be real. So, we brought in engineers from Exponent, a failure analysis firm formerly known simply as Failure Analysis. They confirmed that the power figures were indeed as audacious as they looked, and helped us brainstorm solutions that didn't require defying the second law of thermodynamics. After all, that was one law Andrew was smart enough not to argue with.

The discipline of engineering lies in knowing which rules can be broken, which can be bent, and which must be respected. Andrew and his team had a battle-tested judgment for this distinction. They knew when they were challenging convention—which was exactly what they intended to do—and when they were challenging the laws of physics—which they did not intend to do.

When you are building cutting-edge technology, failure is inevitable. The only way to navigate failure is through discipline, perseverance, and most importantly, trust: trust in the mission, trust in each other, and trust in the fact that after the first prototype self-destructs, you'll still be back in the lab the next morning to start the next iteration.

This kind of work has no transactional version. It only has a long-term version: staying in the room through incomplete solutions and patient explanations, so that when it finally succeeds, you are there to witness it firsthand.

That moment arrived in August 2019. Andrew, Sean, and their team stood in the lab, watching a brand new computer they had designed themselves run for the first time. To an outsider, it didn't seem to be doing anything interesting. According to Andrew, it was about as exciting as watching paint dry. But the difference this time was: no such "paint" had ever truly dried before. They stood there together for 30 minutes, then went back to work.

Who You Build With Matters Immensely

Some people choose problems based on what they know they can solve. Andrew chooses problems based on what he believes is worth solving. Incremental iteration doesn't excite him; he wants 1000x leaps. From day one, he wanted to build Cerebras into a generational, one-of-a-kind company.

This drive stems partly from his personality. Andrew describes it as an "affliction" of computer architects—being haunted by a single idea for decades. But to me, it's more broadly an "affliction" of founders. He looks at a problem and asks himself first: Can I create something that causes a step-function improvement? Then he asks: If I succeed, will people care? If the answer to both is yes, he dedicates the next ten years of his life to it.

Another part of this drive comes from his upbringing. Andrew grew up surrounded by geniuses as naturally as most kids watch TV. His father was a pioneering professor of evolutionary biology who played doubles tennis every Sunday with the same six people. Among them, three later won Nobel Prizes, and one won the Fields Medal.

According to Andrew, these giants would patiently explain their work in physics, mathematics, and molecular biology using language a child could understand. This gave him a profound understanding of what true intelligence looks like, while also realizing, as his mother said, that being smart doesn't mean you have to be a jerk.

I've come to realize this is one of Andrew's core traits, as important as his rebellious ambition and his almost phototropic instinct for truly worthwhile problems. He firmly believes that the most remarkable people he has met are often also exceptionally kind.

This belief shaped how his team came together to accomplish incredibly difficult things. The first 30 people Cerebras hired had all worked with him before; some had been following him since 1996. Today, Cerebras has about 700 employees, around 100 of whom have followed him across multiple companies.

August 2022. Cerebras founding team at the Computer History Museum. From left to right: Sean Lie, Gary Lauterbach, Michael James, JP Fricker, and Andrew Feldman.

Importantly, kindness and competitiveness are not contradictory. Andrew desperately wants to win. He likes to say he is a professional version of David, fighting Goliath. Goliath is slow and always guarding against a frontal attack, leaving openings for every other strategy. David's advantage lies in appearing in ways and places Goliath cannot.

At SeaMicro, Andrew's largest channel partner in Japan was NetOne. NetOne's main supplier was Cisco, which entertained partners with private jets and yachts worth more than most homes in Palo Alto. Andrew's budget was far more modest, so he invited NetOne's CEO to his backyard for a barbecue. Later, the CEO told him he had done business with Cisco for decades but was never invited to anyone's home. This small, deeply human gesture—something Goliath would never think to do—cemented their relationship.

From the First Term Sheet to the IPO

This morning, Andrew rang the opening bell at Nasdaq. I stood by his side. It has been ten years and 2600 miles since everything began in our 250 Middlefield office.

Today, there are still rare founders doing what Andrew did back then: drawing on whiteboards at 3 AM, wrestling with unsolved technical problems. They share the same fierce competitiveness and rebellious spirit. They are trying to find a true partner willing to fight alongside them: someone who will dive in and solve problems when the first prototype won't power on, and who will stay until it finally runs.

These are precisely the founders I want to support: those who choose problems worth solving, imagine solutions 1000 times better than the status quo, and persistently refine and persevere through the inevitable challenges along the way.

For founders like Andrew, Gary, Sean, Michael, and JP, I'm willing to climb over a backyard fence on a Saturday afternoon to personally hand them a term sheet.