Tiger Research: DeFi Yields Are Declining – What Real Value Does RWA Offer?

- Core Thesis: The DeFi token incentive model is no longer sustainable. The industry is shifting towards a genuine yield system anchored by Real World Assets (RWA), with institutional capital inflow driving the construction of sustainable on-chain financial infrastructure.

- Key Elements:

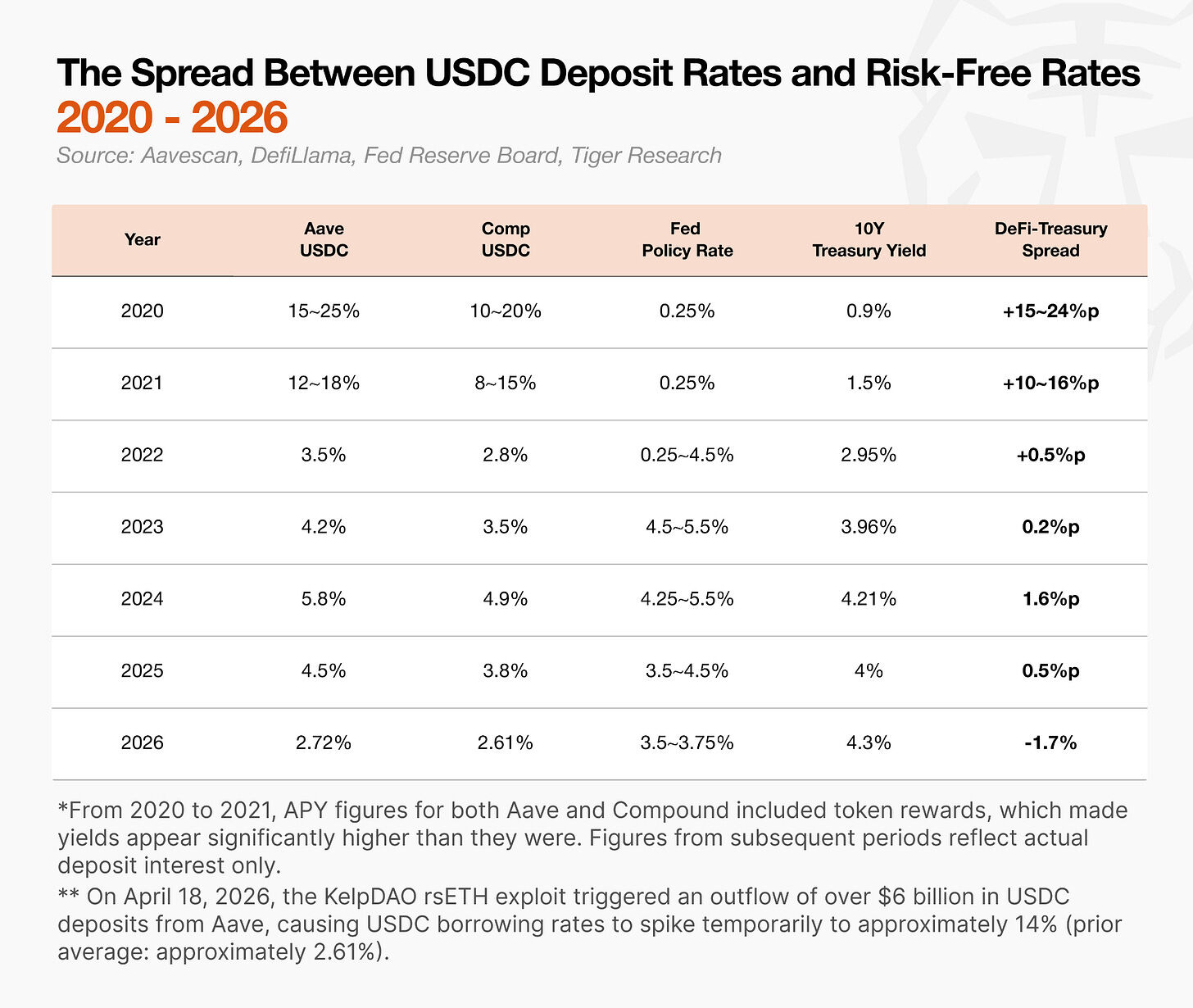

- DeFi yields continue to decline. The USDC deposit rate on Aave V3 (2.7%) is now lower than the 10-year US Treasury yield (4.3%), making traditional finance yields more attractive.

- Failures of Compound, Curve, and OlympusDAO reveal a core lesson: Models reliant on token incentives and internal circulation are prone to collapse when external capital dries up, lacking real value backing.

- The RWA and stablecoin market has grown to hundreds of billions of dollars. Institutional products like BlackRock's BUIDL and Franklin Templeton's BENJI tokenize real assets like US Treasuries, providing a source of genuine yield.

- Yield-bearing stablecoins (YBS) like Ethena's sUSDe and Sky's sUSDS embed yield into the token itself, essentially acting as on-chain money market funds with the advantage of composability.

- Projects like Theo, Plume, and Morpho are building a "value grid" connecting real-world assets with on-chain finance, focusing on asset curation, foundational infrastructure, and lending functionality respectively.

- The industry is establishing mechanisms for collaborative governance and accountability. For instance, the DeFi United alliance has raised over $300 million to address losses from hacker attacks, demonstrating increased industry maturity.

Core Points

- This report is authored by Tiger Research. The USDC deposit rate on Aave V3 is currently 2.7%, lower than the 4.3% yield of the 10-year US Treasury bond. The short-term dividends of DeFi driven by speculation are fading.

- The market is not dead. Although yields are declining overall, Real World Assets (RWA) and stablecoins have grown into a multi-hundred-billion-dollar sector, and the industry is heading in a new development direction.

- The failures of projects like Compound, Curve, and Olympus reveal a profound lesson: a model reliant on tokens supporting each other collapses instantly once external capital inflows dry up.

- Past DeFi was like a power strip without an external power source; RWA is connecting this circuit to a real external value grid.

- The industry is maturing: using RWA as a value anchor while gradually establishing mechanisms for collaborative governance and accountability, as exemplified by initiatives like DeFi United.

1. Declining Yields, Growing Market

Decentralized Finance (DeFi) is no longer a high-yield product.

Since 2022, the spread between DeFi yields and Treasury yields has narrowed to near zero, with periods of yield inversion. As of April 2026, the USDC deposit rate on Aave V3 is approximately 2.7%, lower than the US Federal Funds Rate (3.5%) and the 10-year US Treasury yield (4.3%).

In the past, users taking on risk had a clear return logic.

At that time, on-chain yields were far superior to bank deposits, an unparalleled advantage. But the situation has now reversed. If, after accounting for various on-chain risks like hacks and stablecoin de-pegging, DeFi's actual returns are lower than traditional financial products, the incentive for ordinary retail users to actively participate in DeFi will be significantly diminished.

However, the industry is continuously developing in a new direction. While native DeFi yields are declining, the deep integration of **Real World Assets (RWA)** and the stablecoin market with traditional finance has scaled to hundreds of billions of dollars. The entry of institutional capital is the core factor driving this shift.

But institutions often overlook DeFi's development history and native community ecosystem, blindly copying the rules and paradigms of traditional finance. Before the large-scale entry of institutions, DeFi was a market primarily driven by token incentives. Many protocols used incentive mechanisms to build market awareness and reshaped the industry's operational logic. This model still profoundly influences DeFi today. Aave, a flagship protocol born during DeFi Summer, has become the benchmark interest rate for the entire DeFi industry.

For new institutional participants, a deep understanding of the core market players who have survived market cycles is essential groundwork before entering. This article will review key protocols that shaped core narratives throughout the complete DeFi development cycle and summarize the lessons learned by the market.

2. History of DeFi: From Experimentation, Collapse, to Reinvention

DeFi wasn't initially built on promises of token incentives. The starting point was simple: Can we lend, borrow, exchange, and stake assets on the blockchain without intermediaries?

The early days of the industry were more of a financial experiment. The core value lay in the model itself: lending without banks, asset exchange without centralized exchanges, and liquidity provision by any user holding collateral assets. But after 2020, the market sentiment shifted rapidly, with token incentives becoming the primary means of attracting capital. A flood of protocols and innovative ideas emerged, but only a few projects survived the cycles. The industry learned lessons and continuously corrected its development path through successive narrative shifts.

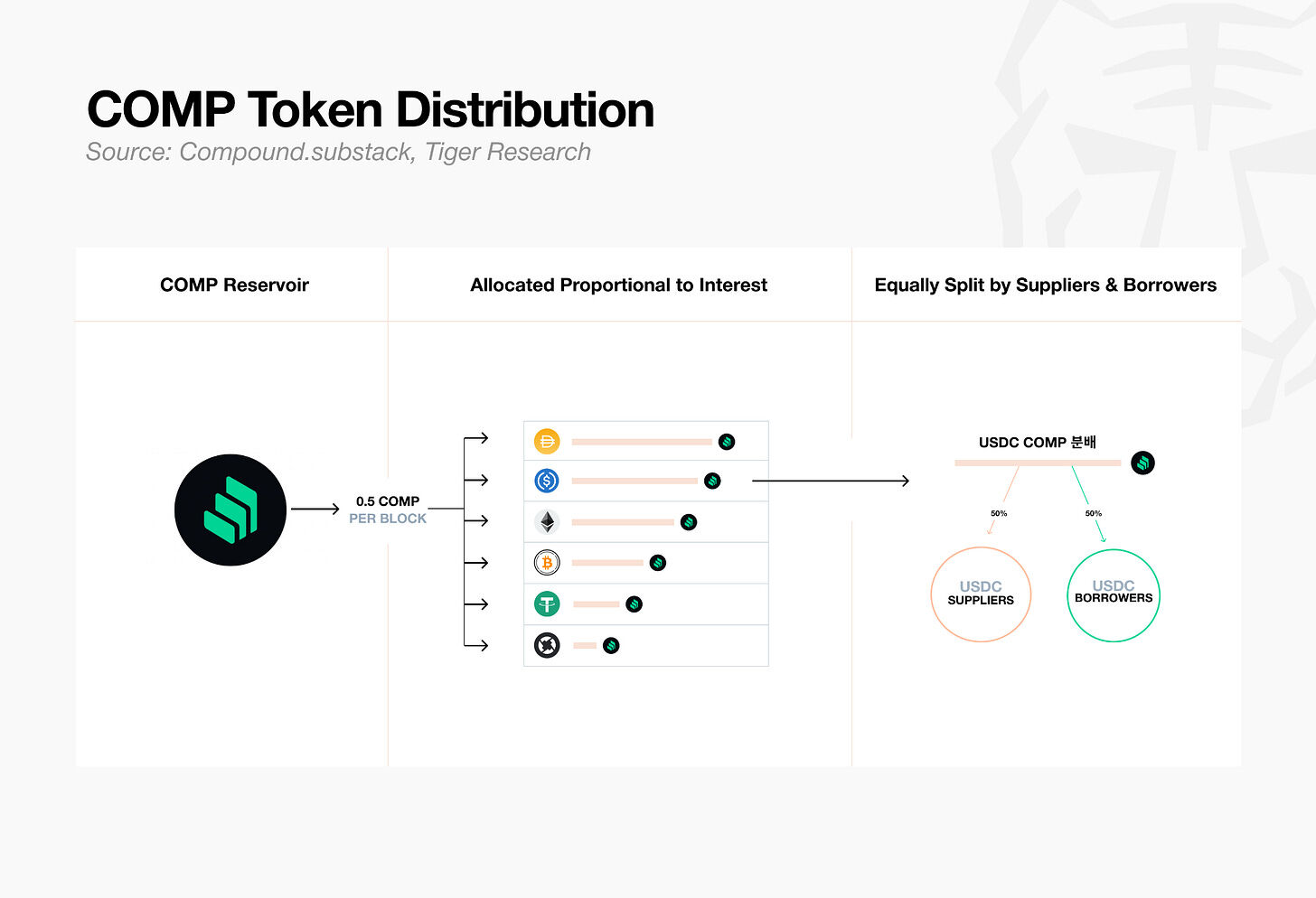

Compound integrated its native token $COMP into the yield incentive system to attract massive liquidity. However, when similar projects replicated this strategy, the inflow of new capital dried up, exposing the structural vulnerability of its model.

Curve transformed governance voting into a competitive arena for allocating yields across liquidity pools, turning yield competition into a fight for protocol control. This led the market to realize that DeFi governance could also become a tool for power and incentive monopolization.

OlympusDAO was the most extreme case. Promising exceptionally high Annual Percentage Yields (APY), it aimed to prove that DeFi could control its own liquidity without external capital. However, the vast majority of its returns came not from real cash flows but from minting new tokens and new capital inflows. Once capital inflows slowed, the price of its governance token OHM collapsed, and market confidence in the protocol was completely shattered.

These three projects collectively served as a wake-up call for the industry: If the core source of yield is the protocol's native token, the business model will ultimately be unsustainable. This history fundamentally reshaped the perception of DeFi among ordinary users, development teams, and institutional capital.

It was precisely after the burst of this model bubble that new tracks emerged: EigenLayer, Pendle, YBS (Yield-Bearing Stablecoins), and RWA.

2.1. Compound: A Bubble Built on Token Distribution

In June 2020, Compound began distributing governance tokens to users, rewarding both depositors and borrowers. In some phases, COMP rewards even exceeded borrowing costs, creating the peculiar phenomenon where borrowing actually generated profit.

This created a new industry paradigm. As users flooded in, transaction fees on the Ethereum network skyrocketed, with single transfer fees often reaching tens of dollars. Depositing and borrowing were no longer purely financial operations but rather tools for yield farming. Yield-seeking capital moved rapidly between protocols.

This period is known in the industry as "DeFi Summer." Projects like Uniswap, Aave, and Yearn Finance rose in succession, establishing on-chain finance as a legitimate independent track. However, the model Compound ultimately built was fundamentally a positive feedback loop: attracting capital with token incentives, which in turn drove up the token price. The current behavior of DeFi users, highly sensitive to yields, liquidity, and reward mechanisms, was gradually solidified during this phase.

2.2. Curve and veCRV: The Beginning of the Curve Wars

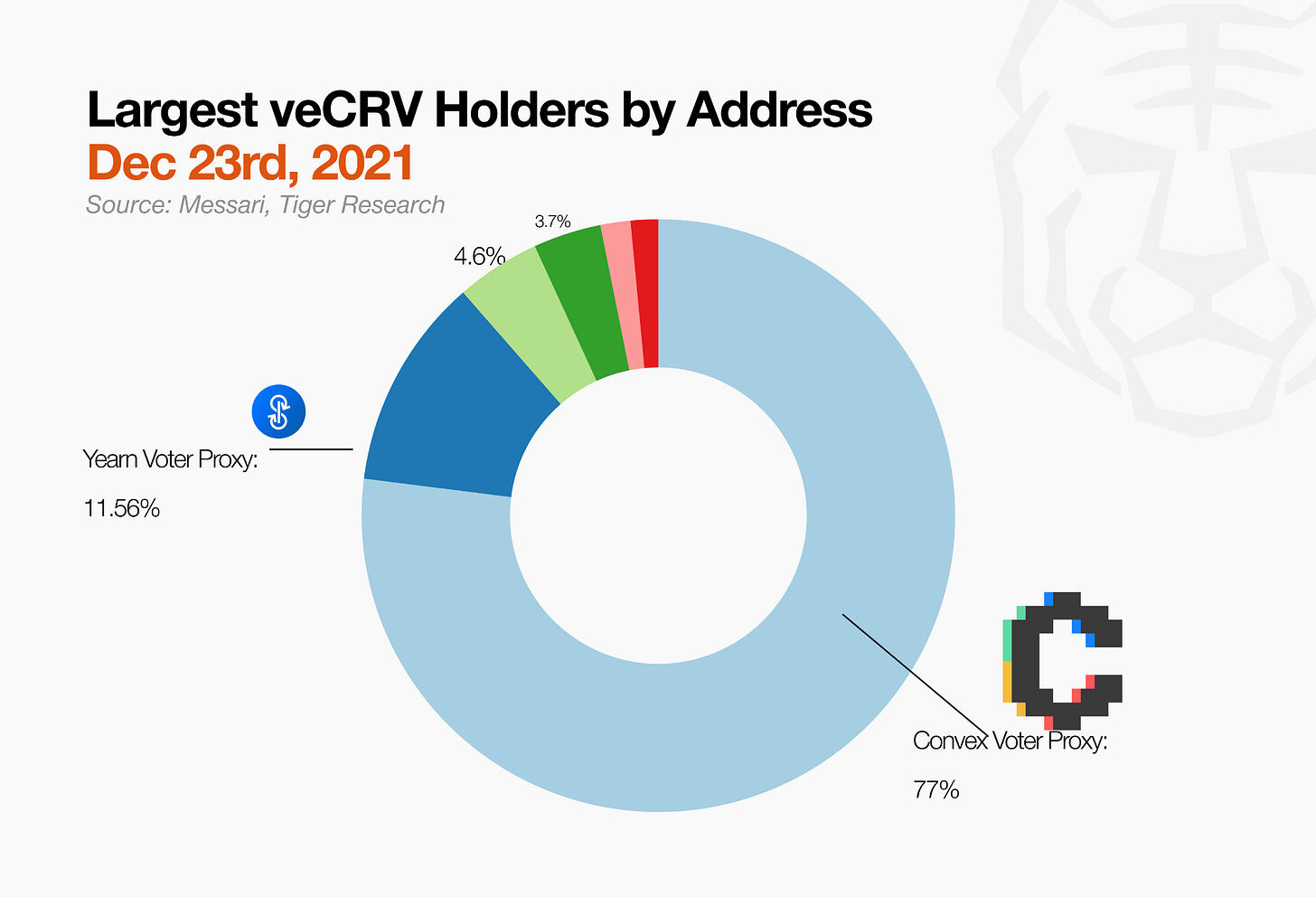

Curve started as a simple exchange platform for stablecoins, but the introduction of veCRV fundamentally changed its underlying logic. The longer users locked their CRV, the more veCRV they received. veCRV represented voting power, which determined the allocation of CRV rewards across different liquidity pools.

From this point, the core of competition shifted from the level of yield to the power to control yield distribution. Entities holding large amounts of veCRV could direct more token rewards to their own pools. Protocols began accumulating veCRV, leading to intense competition known as the Curve Wars.

Initially, this mechanism was attractive to both retail users and projects: users earned higher returns for longer lock-ups; projects could reduce token circulation and guide liquidity to their target pools. Consequently, similar lock-to-govern models proliferated across the ecosystem, notably Balancer's veBAL and Frax's veFXS.

However, over time, governance power no longer resided with ordinary users. Meta-protocols like Convex began aggregating and locking CRV on behalf of users, centralizing veCRV voting power in exchange for enhanced yields. The Curve Wars escalated, shifting the main battlefield to Convex.

veCRV ultimately proved a core conclusion: the power to control yields is more attractive than the yields themselves. Users delegated their governance power to more efficient intermediaries like Convex. Curve also revealed to the market that DeFi governance rights themselves could become yield-bearing assets, and such power is prone to centralization and monopoly.

2.3. OlympusDAO: A Golden Age Built on Game Theory

Even after Curve's veToken mechanism, liquidity remained a persistent major challenge for DeFi. Externally sourced liquidity would immediately withdraw if higher incentives appeared elsewhere, behaving like speculative hot money.

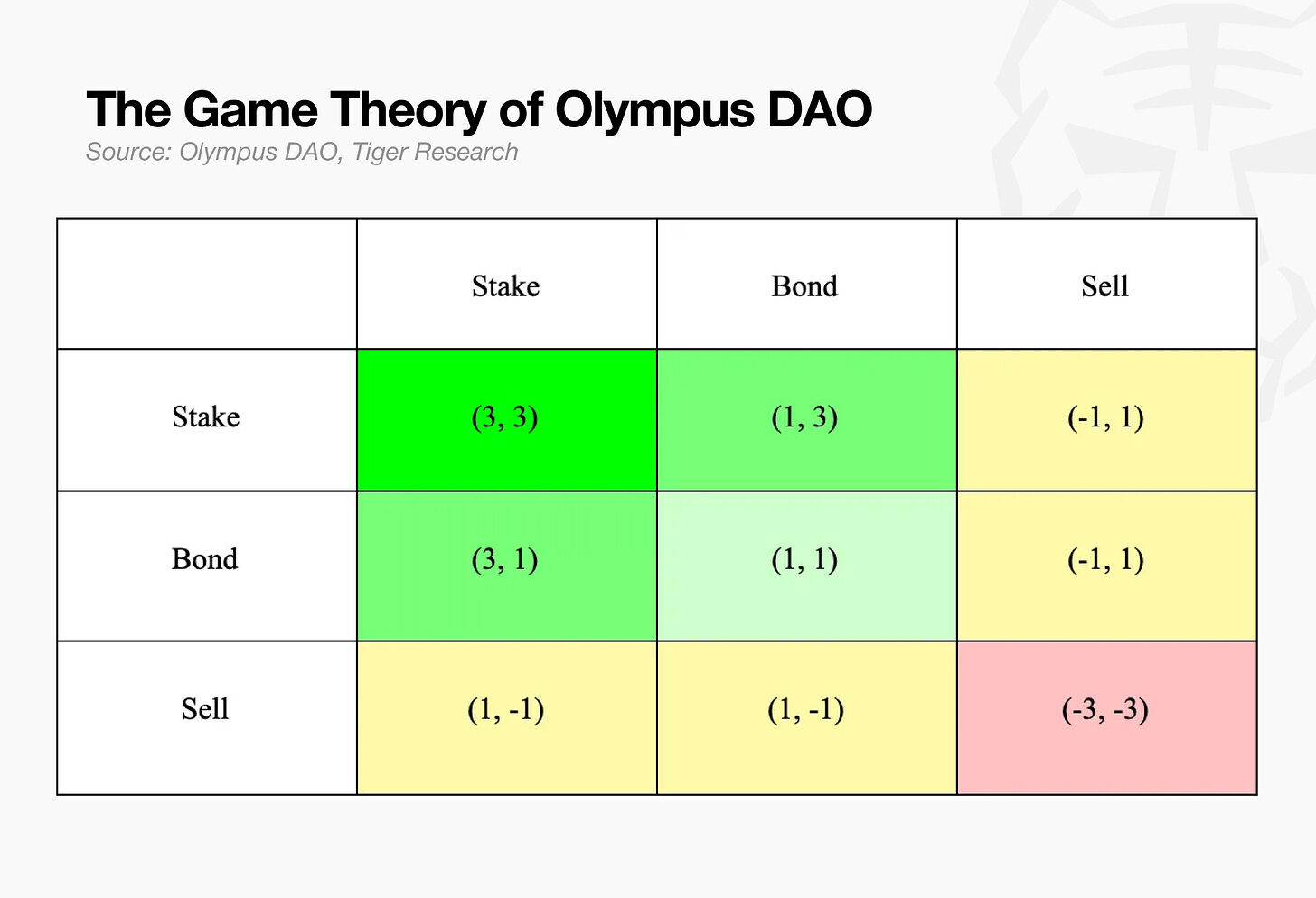

OlympusDAO, launched in the second half of 2021, gained attention as a potential solution to this problem. Its core design featured three elements: Protocol Owned Liquidity (POL), where the protocol directly holds its own liquidity; the (3,3) game theory model, suggesting that staking and locking tokens is the optimal strategy for all users; and an exceptionally high APY exceeding 200,000% at launch.

But this model ultimately proved unsustainable. OHM's yield was highly dependent on minting new tokens, not real business cash flows. Its bond mechanism spawned numerous forks and imitators, while the OHM token price eventually crashed by over 90%. This experience fundamentally shifted the mindset of developers and users: before chasing "how high can the yield be," people started prioritizing examining the true source of the yield.

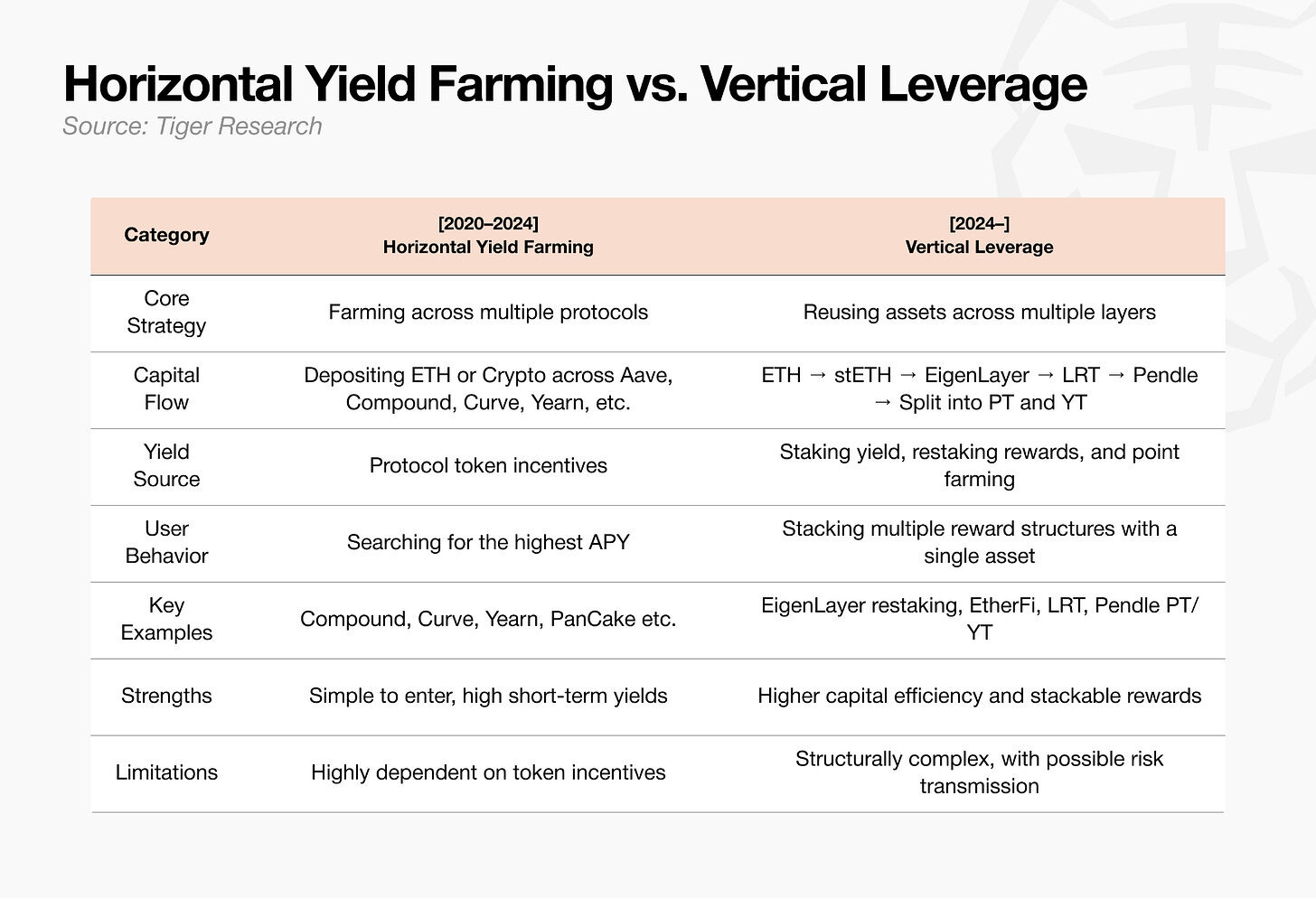

2.4. EigenLayer and Pendle: From Horizontal Yield Farming to Vertical Leverage

This crash fundamentally changed retail behavior. The strategy from 2020 to 2022 was simple and crude: farm the incentives first, then cash out. It was common for the same user to spread their capital across multiple protocols simultaneously. This period's farming was horizontal arbitrage: capital moving quickly between protocols chasing higher APY.

After 2022, the efficiency of this model plummeted. Token incentive models proved unsustainable, and airdrop competition became increasingly fierce. Simply depositing funds across multiple platforms yielded diminishing marginal returns. The market trend shifted, and capital began pursuing multi-layered yield stacking on a single asset: re-staking staked Ethereum (stETH), reinvesting Liquid Restaking Tokens (LRT) into DeFi, and splitting yield ownership to capture points and potential future airdrops.

EigenLayer and Pendle became the core representatives of this transformation. Starting in 2024, EigenLayer introduced a restaking framework allowing already staked ETH and Liquid Staking Tokens (LST) to earn additional rewards. In roughly six months, its Total Value Locked (TVL) surged from under $400 million to $18.8 billion, clearly indicating a massive capital shift from simple deposits to the restaking track.

Pendle splits yield-bearing assets into Principal Tokens (PT) and Yield Tokens (YT). PT represents near-principal-guaranteed rights; YT encompasses all interest, farming rewards, and point rights during the token's lifespan. YT value drops to zero at maturity but maximizes point and yield capture during the holding period. Even without understanding the underlying complex mechanisms, buying YT evolved into a mainstream farming strategy using both time and capital leverage.

The industry strategy was thus rewritten: from spreading capital across multiple protocols horizontally to focusing on a single asset and stacking multiple layers of yield vertically for compounding returns.

3. Restructuring Profit Models: RWA and YBS

In the past, projects heavily relied on token incentives to boost TVL. As TVL grew, the protocol appeared to expand, and the token price rose. However, a core flaw persisted: external liquidity was fleeting and difficult to retain.

Today, TVL remains an important metric, but the industry's focus has shifted entirely towards: fee revenue, real-world asset backing, and compliance capabilities. The key variable behind this shift is the entry of institutional capital. Institutions conduct rigorous due diligence on the source of yields and the true quality of underlying collateral. A new generation of products is iterating and upgrading to simultaneously meet retail demands and institutional compliance requirements.

3.1. Real World Assets (RWA): Institutional Entry in Force

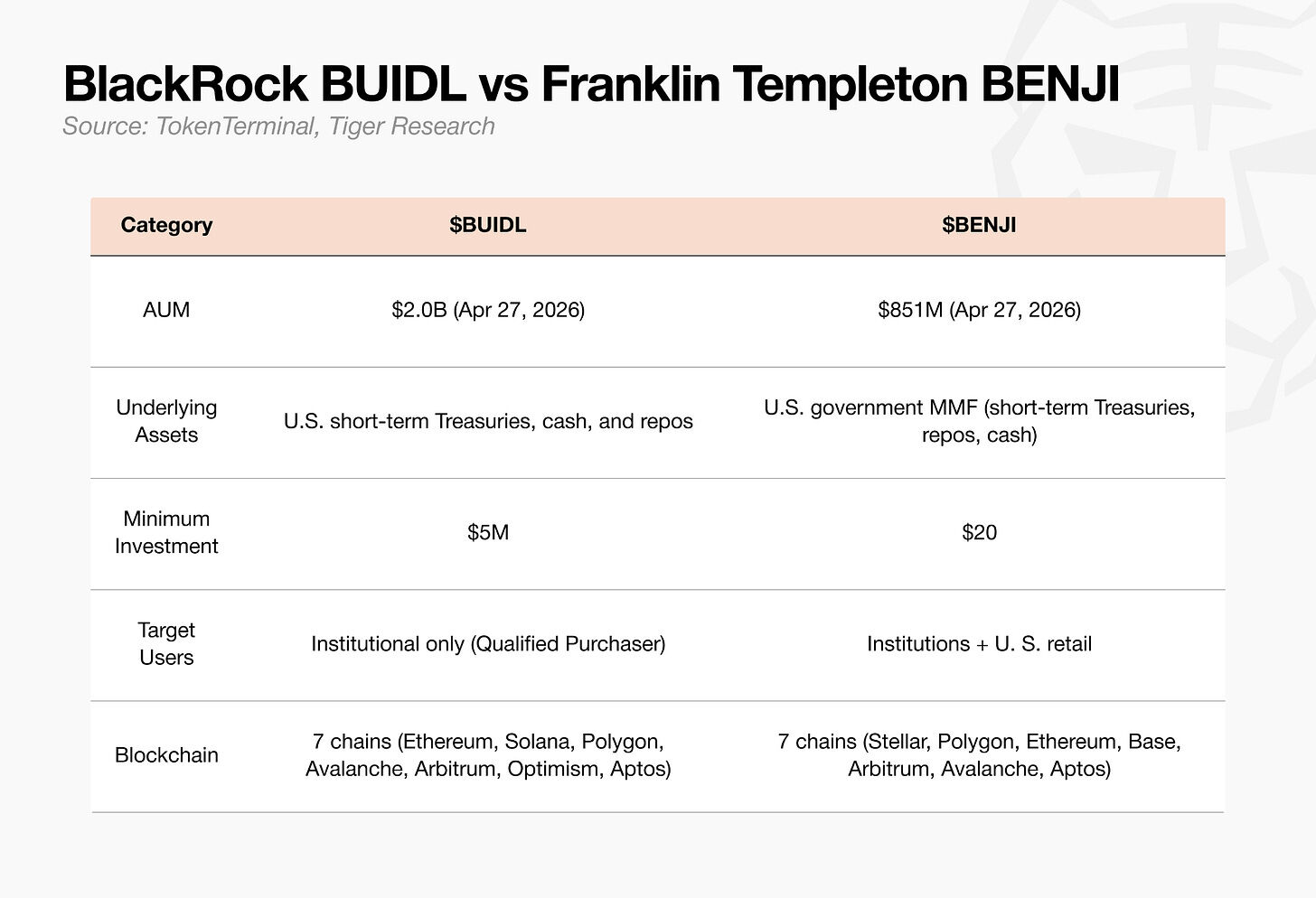

Since 2024, traditional financial institutions like BlackRock, Franklin Templeton, and JPMorgan Chase have entered the on-chain market via Real World Assets (RWA). Their model involves tokenizing off-chain real-world assets such as US Treasuries, money market funds, private credit, gold, and real estate, issuing and circulating them on the blockchain.

The on-chain RWA market has grown from tens of billions of dollars in 2022 to hundreds of billions by April 2026. Treasury tokenization and private credit are the primary drivers of this growth.

The current leading institutional products are represented by BlackRock's BUIDL and Franklin Templeton's BENJI. Both have similar underlying asset types but differ in operational model: BUIDL is strictly for institutional investors, while BENJI has a minimum investment threshold of only $20, making it accessible to ordinary US retail investors.

Furthermore, asset management giants like Apollo, Hamilton Lane, and KKR are partnering with on-chain issuance platforms like Securitize to accelerate the tokenization of private equity funds and private credit.

For traditional institutions, the on-chain market is not an entirely new frontier but a new distribution channel for assets. Consequently, various protocols serving institutional clients are building supporting infrastructure: compliant KYC/AML frameworks, custody solutions, multi-jurisdictional legal adaptability, and specialized risk management frameworks.

3.2. Yield-Bearing Stablecoins (YBS): Dollar Assets with Built-in Yield

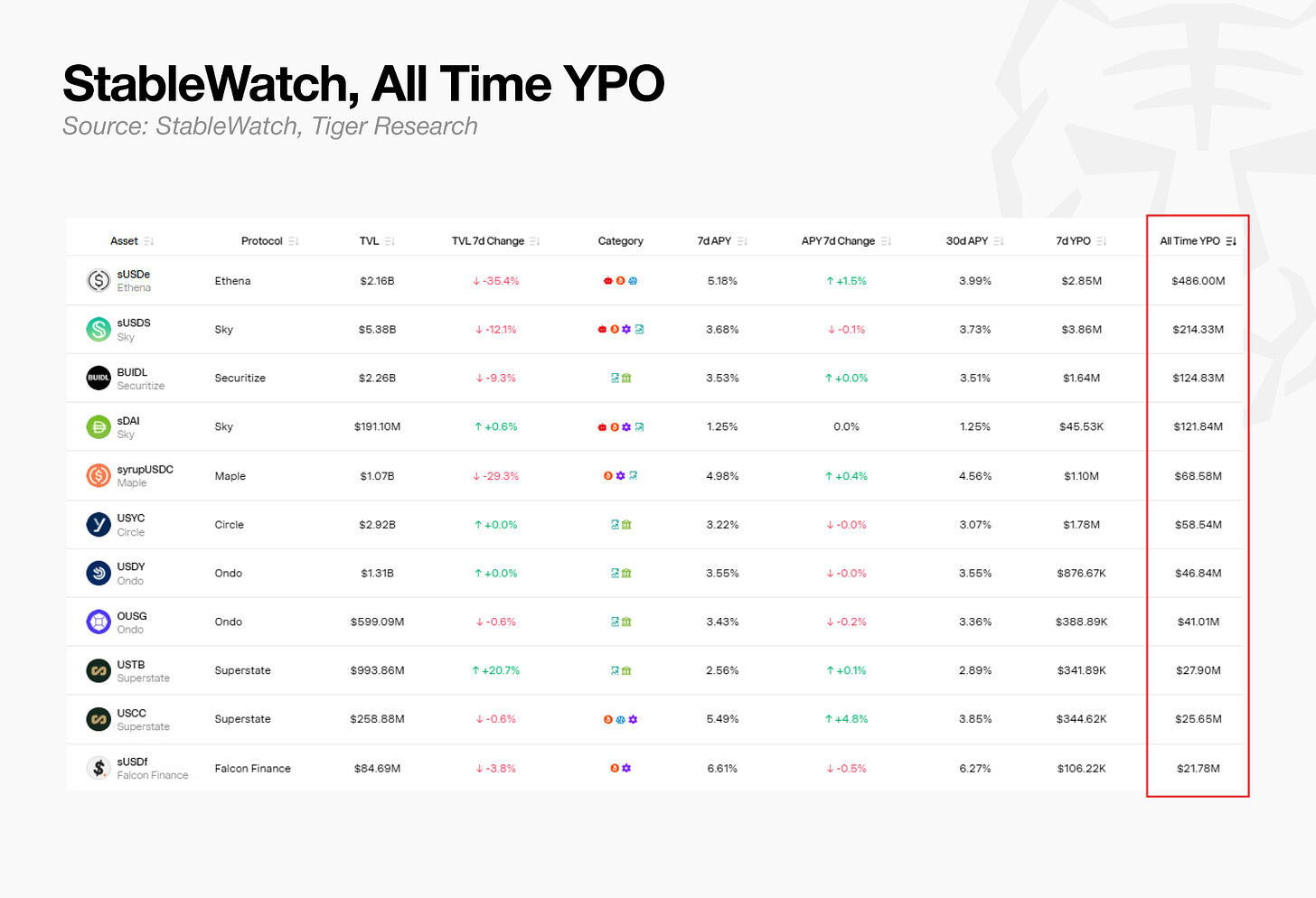

The most noteworthy sub-sector currently is Yield-Bearing Stablecoins (YBS). YBS are stablecoins with yield mechanisms embedded directly into the token itself. Examples include Ondo USDY, Sky sUSDS, Ethena sUSDe, and the previously mentioned BlackRock BUIDL and Franklin BENJI.

Users simply holding these assets automatically accumulate yields generated by the underlying assets. These underlying assets encompass US Treasuries, funding rate yields, staking interest, and money market funds. The entire structure is essentially an on-chain migration of traditional Money Market Funds (MMFs).

According to StableWatch's Yield Production Output (YPO) data, Ethena sUSDe, Sky sUSDS, BlackRock BUIDL, and Sky sDAI are among the top cumulative yield payers in the market. While data varies slightly across different metrics, it is undeniable that yield-bearing stablecoins have moved beyond niche experimentation into a mature sector capable of consistently distributing real interest.

Even so, simply putting money market funds on-chain does not constitute a core differentiating advantage. The true moat lies in composability. BlackRock's BUIDL makes up 90% of the collateral for Ethena's stablecoin USDtb, which can in turn be used as collateral within Aave's lending ecosystem.

In other words, basic financial products originally designed as real-world asset tools have now transformed into stable underlying components for on-chain finance. DeFi is no longer barely running on a limited internal "built-in battery"; it's beginning to be powered by external real-world value.

4. Building the RWA Value Grid: Learning from Past Failures

Before this, DeFi was essentially engaged in one activity: connecting an endless series of power strips in a self-referential loop, euphemistically called a growth flywheel.

One layer of leverage and derivatives was piled upon another, creating a closed, self-consistent system. The fatal flaw was that energy never came from the outside; the vast majority of yields were artificially created by protocol-native token incentives. Compound backed its lending with native tokens; Curve used its own token to retain liquidity providers.

On the surface, protocols seemed to be mutually supplying and circulating value, but in reality, the entire system relied on a single, finite shared battery. When the market faced a shock, the underlying value collapsed first, cascading upwards, causing derivative products at the end of the chain to fail first. This self-closing, self-endorsing model had a natural capacity limit.

RWA, for the first time, connects this system to a real external value grid. Real economy cash flows—bond interest, property rents, trade receivables—become the stable power running