8万ドルのビットコイン:回復は明確だが、強気相場への確信は依然として不足

- 核心見解:ビットコインは8万ドル台まで回復した。これはETFへの資金流入、スポット需要の増加、ポジションの改善によるものだが、資本流入の弱さと8万6千ドル付近での供給圧力は、市場の信頼感が依然として以前の強気相場の水準まで回復していないことを示しており、現在はブレイクアウト上昇というよりも、構造的な回復に近い。

- 主要要素:

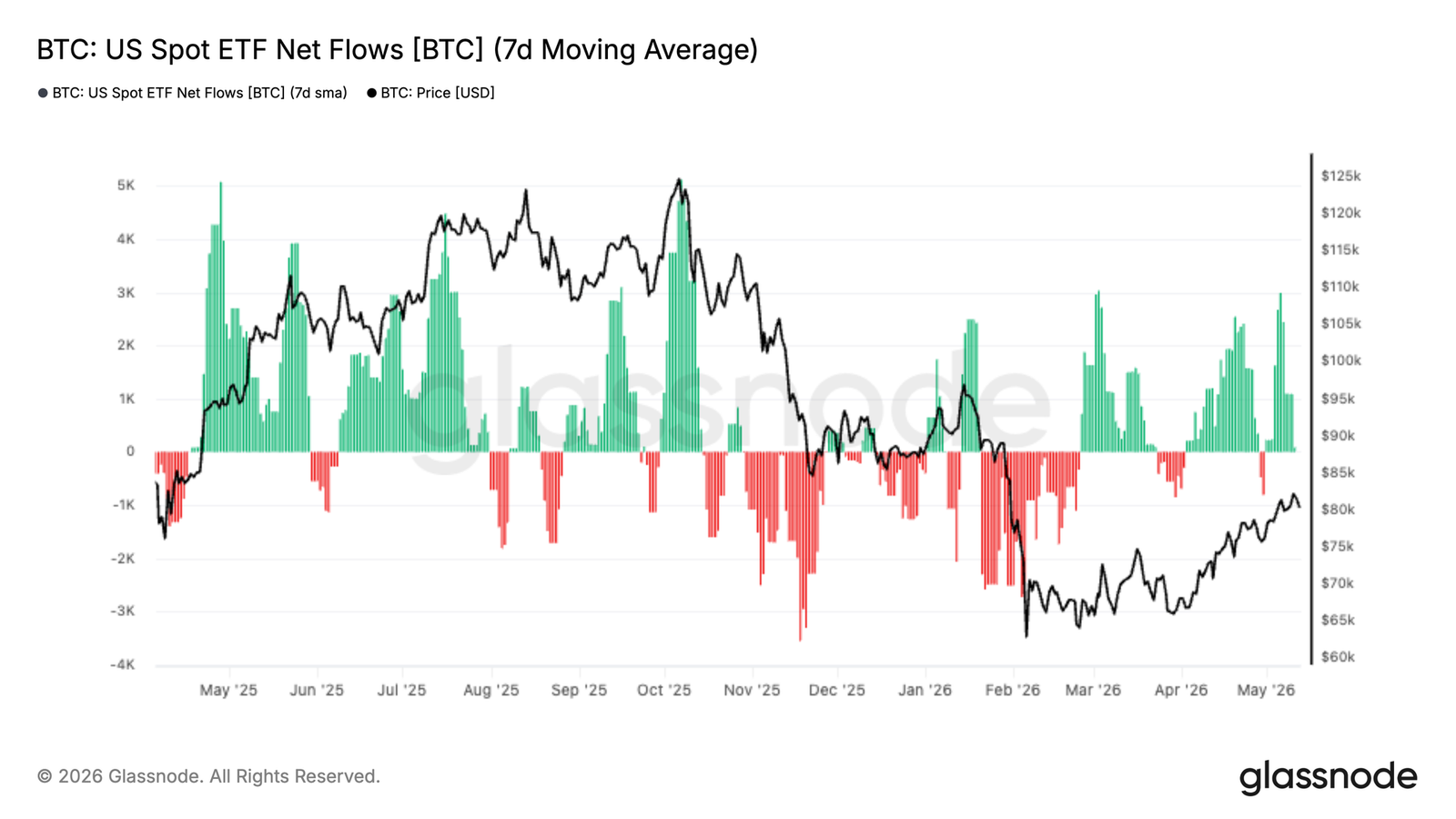

- 米国スポットビットコインETFへの資金流入は明確にプラスに転換し、機関投資家の需要が再燃しているが、その規模は以前の強気相場期における月間100億ドル超の水準には依然として及ばず、資本流入の力強さが不足していることを示している。

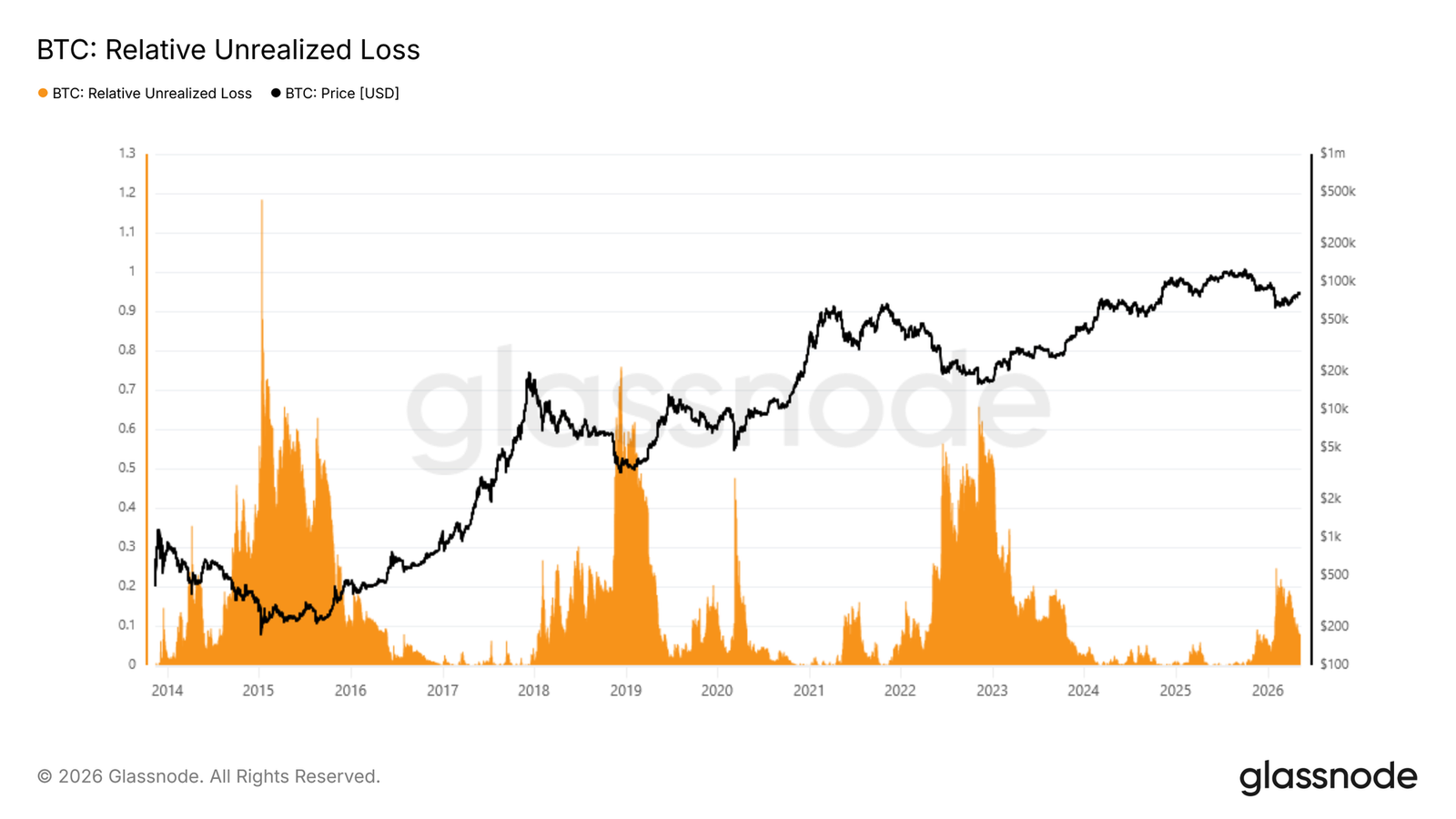

- 相対的未実現損失は2月の売り浴びせ期間中に時価総額の25%に達した後、8%まで圧縮された。6万ドルが維持されれば、今回の相場は浅い弱気相場であるという見方を支持する。

- 30日コストベースの7万6900ドルが短期的なサポートを構成する一方、11月から2月にかけての accumulation レンジである8万6900ドルは直近の重要なレジスタンスであり、上値の供給圧力が重いことを反映している。

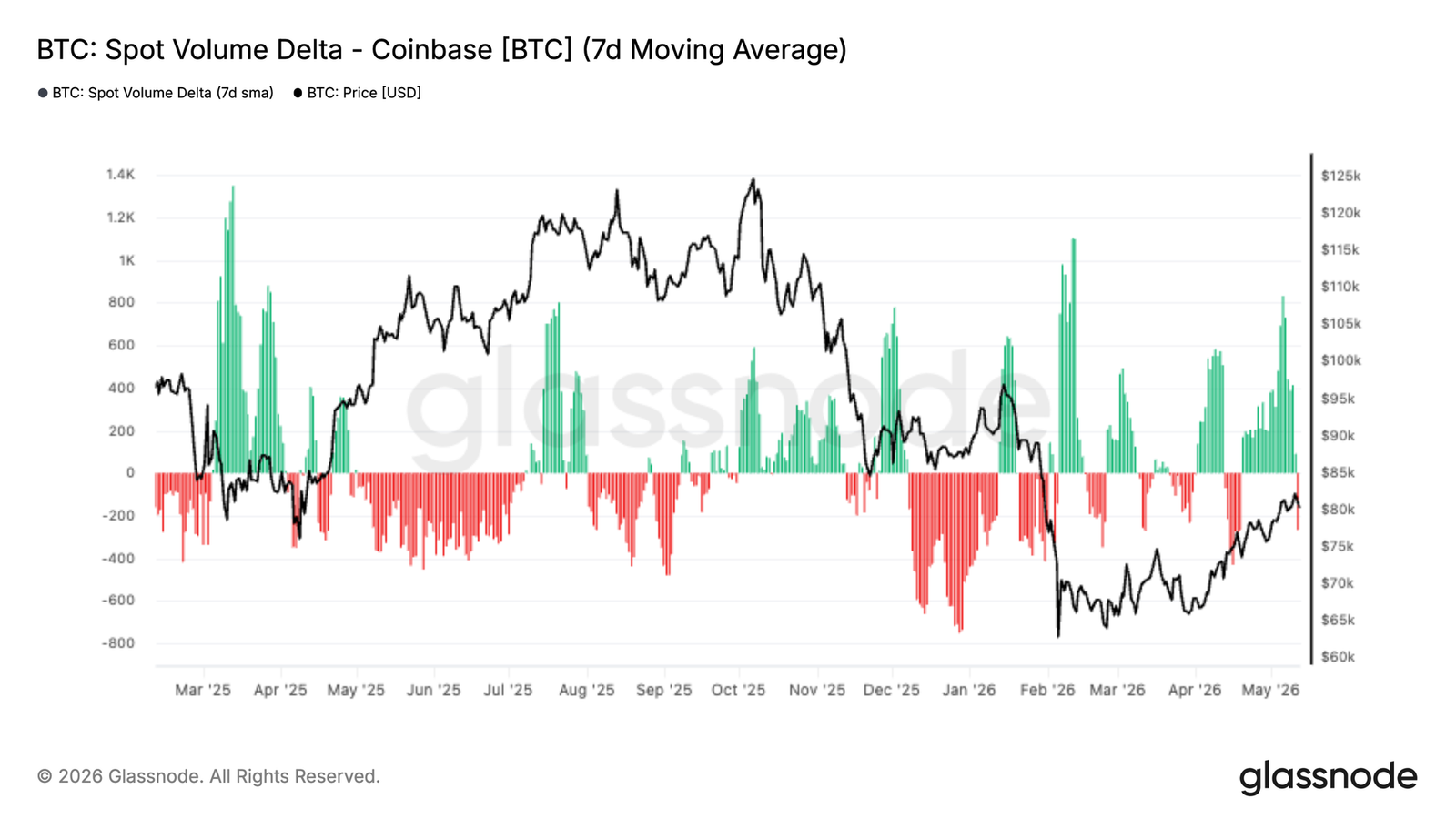

- Coinbaseスポット出来高デルタは積極的に上昇しており、ETFへの資金流入と同期している。これは米国本土および機関投資家の買い手が再び参加し、スポット需要が強化されていることを示している。

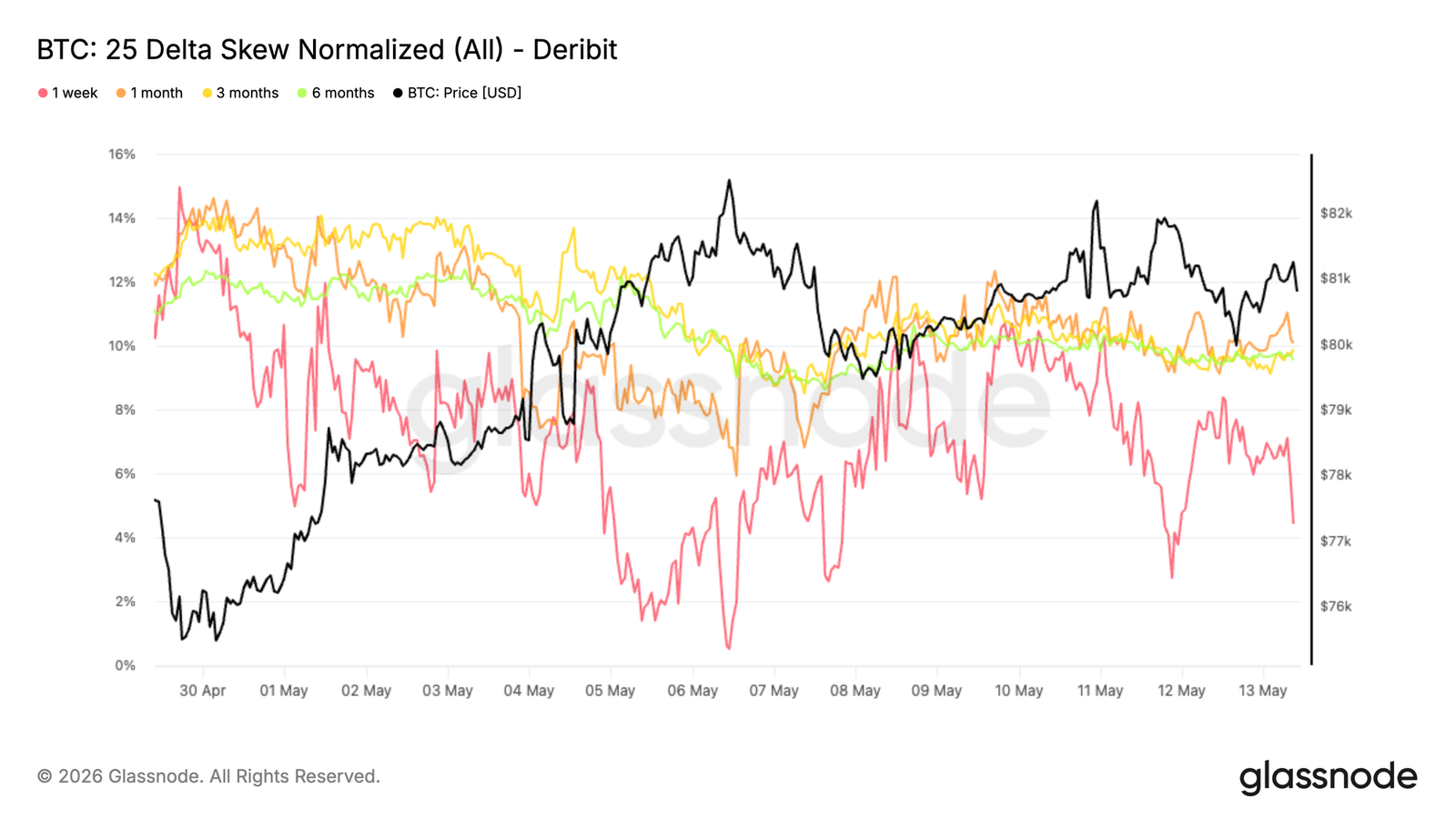

- インプライド・ボラティリティは継続的に圧縮され、スキューは正常化している。これは市場がより平静な短期の値動きを織り込んでおり、下値ヘッジの需要が弱まり、オプション構造がより均衡していることを示している。

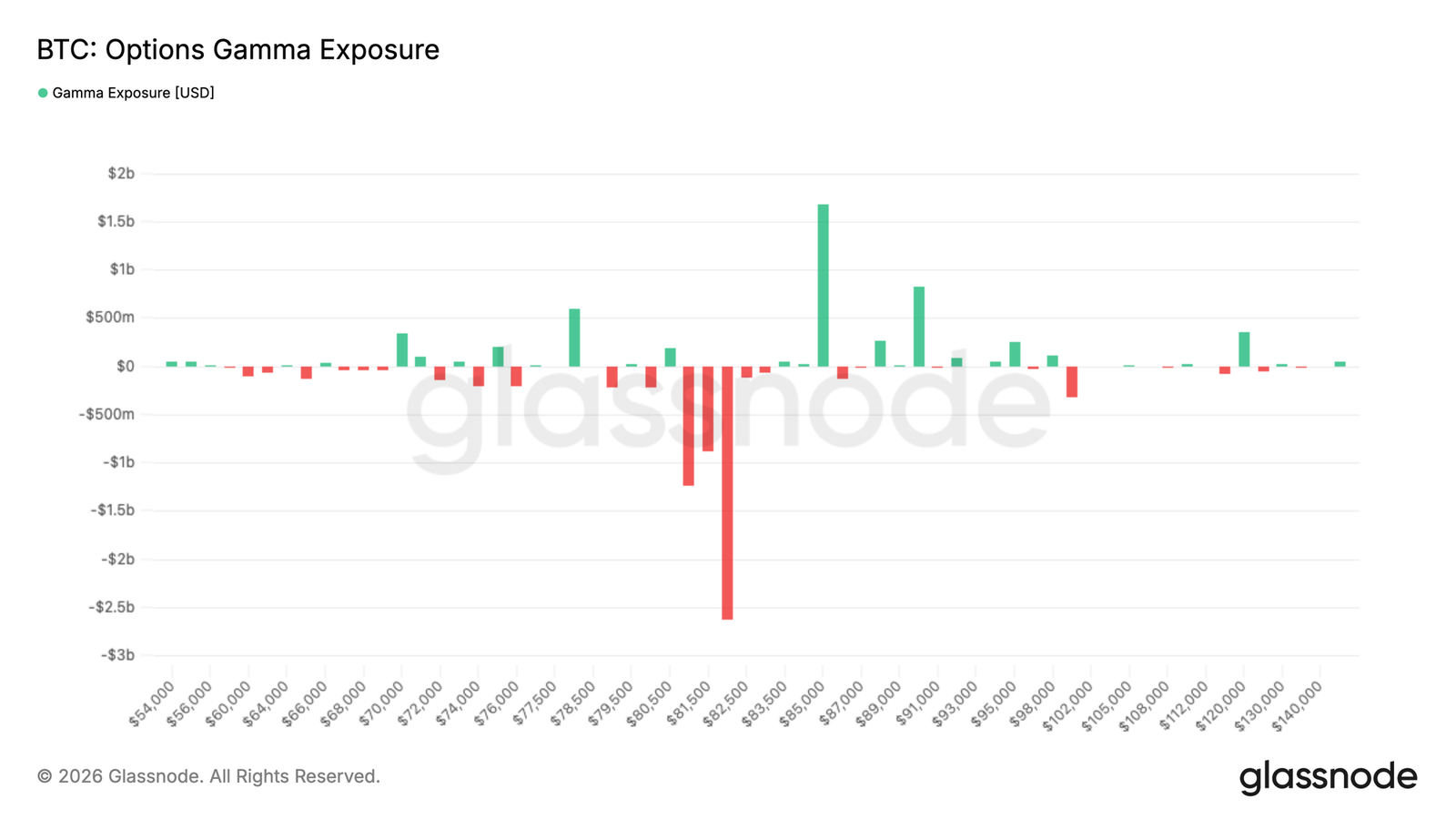

- マーケットメーカーのポジションは8万2千ドル付近に大量のネガティブ・ガンマ・クラスターが存在し、スポット価格がこのゾーンに再び入った場合、値動きを増幅させ、短期的な感応度を高める可能性がある。

Original Author: Glassnode

Original Translation: AididiaoJP, Foresight News

Bitcoin has returned above $80,000, with improvements in ETF inflows, spot demand, and positioning. However, weak capital inflows and heavy overhead supply near $86,000 keep market conviction below that of previous bull market phases.

Summary

- U.S. spot Bitcoin ETF inflows have turned clearly positive again, with institutional demand reigniting as Bitcoin recovers from the mid-$60,000 range to the low $80,000s.

- Bitcoin's Relative Unrealized Loss peaked at 25% of market cap during the February sell-off, compressing to 8% after reclaiming $80,000, supporting the view that this remains a shallow bear market if $60,000 holds.

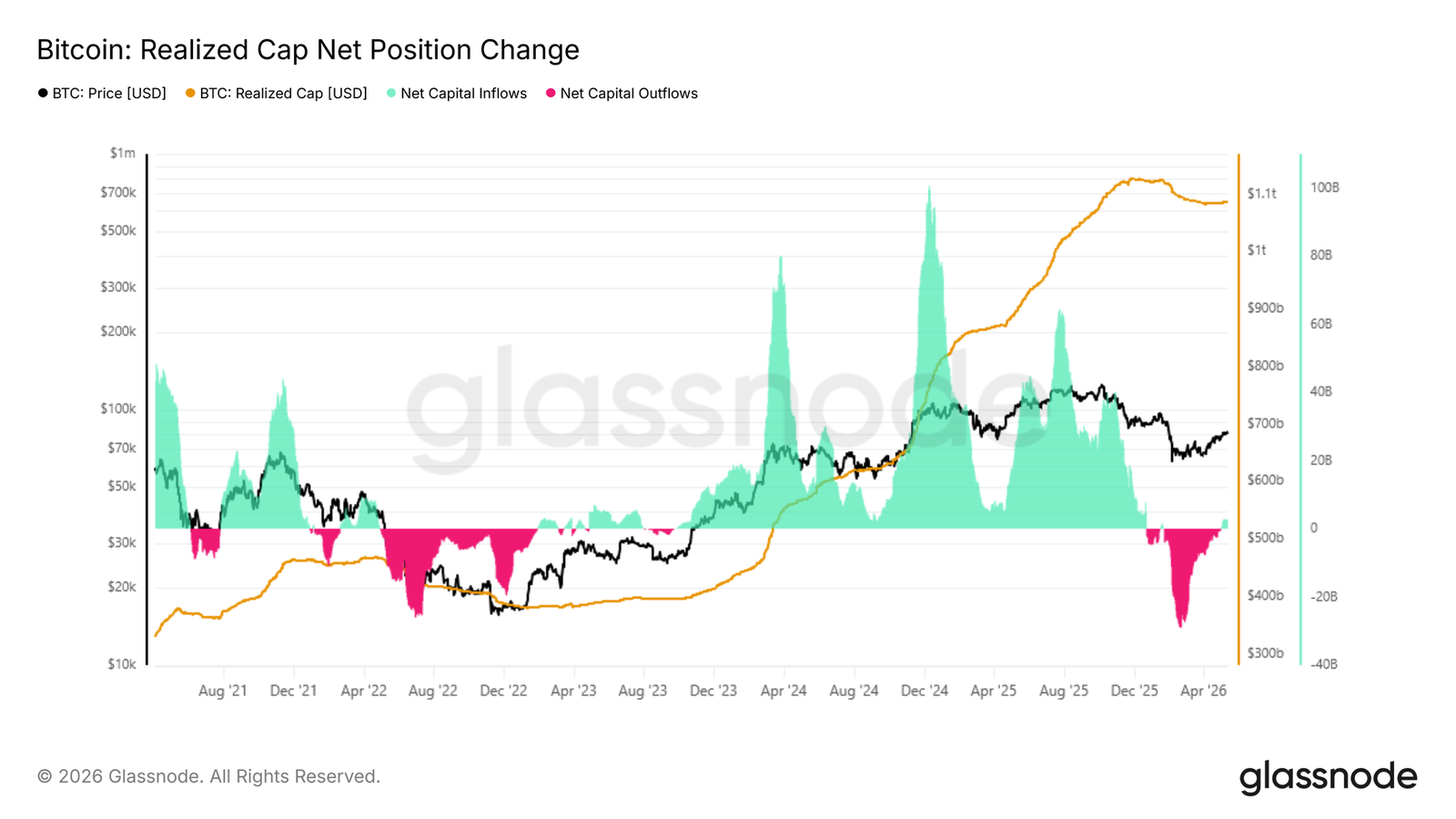

- Realized Cap 30-day Net Position Change has rebounded to $2.8 billion per month, indicating improving capital inflows, though still well below the >$10 billion monthly levels seen in previous bull market expansions.

- The 30-day Cost Basis at $76,900 provides short-term immediate support, while the $86,900 level from the November-February accumulation range remains a key near-term resistance for the recovery.

- Coinbase Spot Volume Delta has turned sharply positive over the past two weeks, indicating increasingly aggressive buyer activity and strengthening spot market demand.

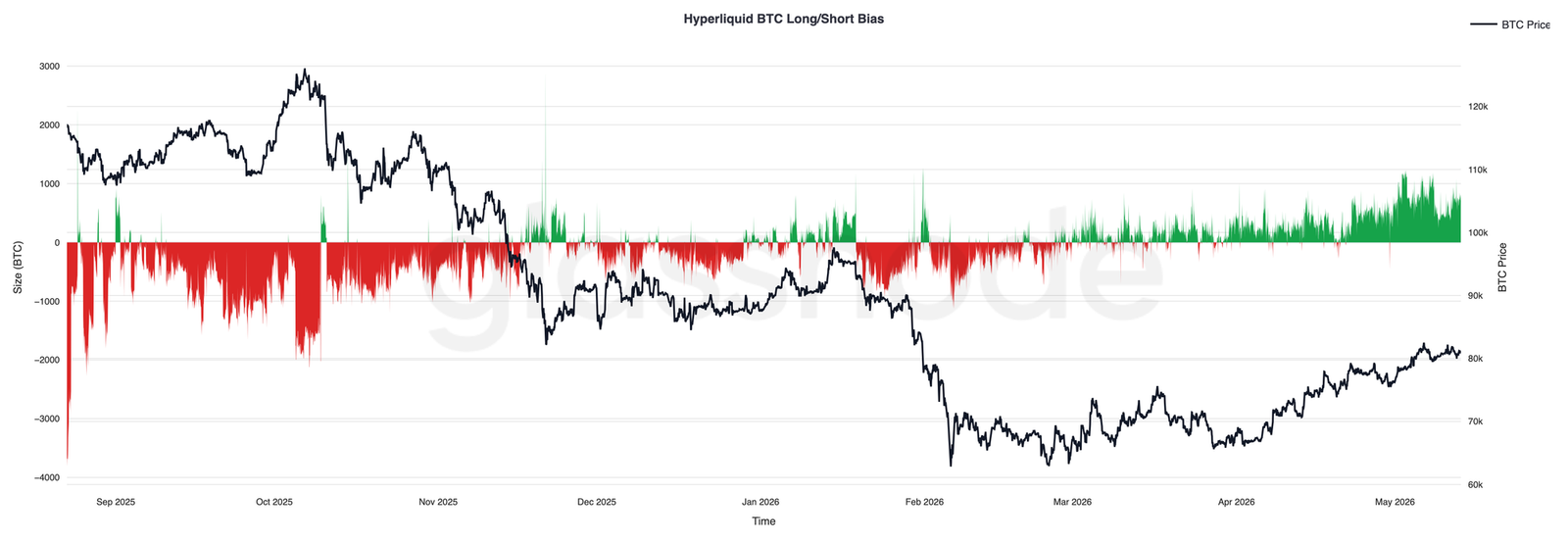

- Hyperliquid traders have steadily rebuilt long exposure as prices rise, reflecting improved speculative sentiment and growing confidence in further upside continuation.

- Implied volatility continues to compress across the curve, led by the front end, while realized volatility trends lower, with the market pricing in a calmer short-term outlook.

- Skew compression indicates waning demand for downside hedges, with options structure around $80,000 becoming more balanced.

- Market maker positioning remains a key driver of short-term dynamics, and a large negative gamma cluster near $82,000 could still amplify price moves if spot re-enters that zone.

Macro Insights

The macro backdrop remains a tug-of-war between slowing economic growth and sticky inflation. Recent U.S. inflation data has come in stronger than expected, while the labor market has proven more resilient than many anticipated. Consequently, markets have pushed back rate cut expectations, keeping Treasury yields elevated and financial conditions relatively tight.

Liquidity remains a key driver for risk assets. Equities continue to grind higher, but the underlying environment remains fragile as markets adapt to the reality of higher-for-longer interest rates. Meanwhile, strength in oil and commodities continues to push up inflation expectations, especially amidst ongoing geopolitical tensions.

For digital assets, the picture remains constructive but selective. Bitcoin has shown resilience despite tighter liquidity conditions and a strong dollar, suggesting underlying demand remains intact. However, weak ETF inflows and high real yields imply that more sustained upside may require looser financial conditions or a fresh catalyst to reignite broader risk appetite.

On-Chain Insights

From Fear to Uncertainty

Against a macro backdrop of sticky inflation, high Treasury yields, and tighter financial conditions, Bitcoin continues to demonstrate relative resilience, suggesting underlying demand remains intact even as the broader risk environment remains unsettled. To structurally assess the current cycle phase, Relative Unrealized Loss—measuring the total dollar value of unrealized losses held by all investors as a percentage of market cap—provides a precise cyclical barometer. During the February flash crash, this metric peaked at 25% of market cap, indicating significant stress, but still far below the extremes recorded in prior bear cycles. After subsequently reclaiming $80,000, the metric has compressed to around 8%, a shift moving mainstream sentiment from fear to uncertainty, rather than outright collapse.

If $60,000 proves to be the cycle low, this bear market would be the shallowest on record—it captured fear, but fell far short of the widespread washout that historically marks durable cycle bottoms.

Scale of Capital Inflows

As sentiment shifts from fear to uncertainty, the key question is whether the current rally is a typical bear market bounce or the early stage of a genuine bull regime shift. The most direct gauge is net capital inflows, measured by the Realized Cap 30-day Net Position Change, which tracks the monthly change in total capital stored on-chain. With the recent rally to $82,000, this metric has reached $2.8 billion per month, a positive reading explaining the constructive momentum of recent weeks.

However, context is crucial: during the early stages of each major upswing in the 2023-2025 bull market, this metric rapidly accelerated from ~$2 billion per month to over $10 billion. While encouraging, the current reading remains well below that threshold, indicating the capital inflows supporting this recovery lack the conviction seen at similar inflection points in previous cycles.

Support and Resistance through the Lens of Cost Basis

Despite a 37% rally from $60,000 to $82,000, capital inflows remain moderate and uncertainty persists. The Realized Price metric, segmented by holding period, provides a granular framework for identifying the most immediate support and resistance levels. This model tracks the average acquisition price of coins by holding period, mapping behavioral anchors of different investor cohorts onto the price chart.

The current rally's momentum is primarily driven by the accumulation wave of the past 30 days. The cost basis for this cohort currently sits around $76,900, forming the most immediate support floor in the short term. Above, the cost basis for investors who accumulated during the November to February range consolidation is concentrated near $86,900, representing the most probable near-term resistance zone as these holders approach breakeven and face increasing distribution incentives.

Off-Chain Insights

Rebuilding ETF Demand

U.S. spot Bitcoin ETF inflows have turned clearly positive in recent weeks, with consistent inflows returning as Bitcoin reclaims $80,000. After months of uneven demand and significant Q1 outflows, this latest shift indicates institutional demand is beginning to re-emerge in a more meaningful way.

Importantly, the resurgence in ETF demand has been sustained rather than driven by a single allocation surge, suggesting institutions are steadily accumulating as market conditions improve. Inflow intensity has also accelerated alongside price, reinforcing the view that traditional capital is again supporting momentum rather than fading rallies.

The current structure shows significant market structure improvement relative to earlier this year. ETF inflows are now acting as a tailwind rather than a source of persistent sell pressure, removing one of the key headwinds that previously constrained recovery attempts. If sustained, continued institutional accumulation could provide the demand base needed for Bitcoin to challenge higher overhead supply zones in the coming weeks.

Coinbase Spot Buying Reaccelerates

Coinbase spot volume delta has turned sharply positive over the past two weeks, with aggressive buyer activity returning as Bitcoin reclaims the low $80,000s. This latest shift contrasts sharply with the persistent sell pressure that dominated most of Q1, when negative volume deltas consistently reinforced downward momentum.

Importantly, the latest leg higher has been accompanied by repeated increases in positive spot buying volume rather than isolated buying surges, indicating sustained demand beginning to absorb overhead supply. The strengthening of Coinbase activity is also highly correlated with the resurgence in ETF inflows, suggesting U.S.-domiciled and institutional buyers are re-engaging.

The current structure suggests spot demand is once again acting as a supporting force for price rather than a source of distribution. The continued strength of Coinbase buyer flow, especially rising in tandem with ETF inflows, indicates improving market conviction and healthier underlying demand conditions for the latest rally.

Hyperliquid Traders Increasingly Bullish

Over the past few weeks, positioning on Hyperliquid has become increasingly skewed towards the long side, with BTC net positioning steadily rising as Bitcoin climbs back to the low $80,000s. This shift marks a significant reversal from the persistent short bias that dominated most of Q1, when the market corrected to the low $60,000s.

Importantly, the recent increase in long exposure has been gradual rather than a surge via a single crowded position, indicating traders are steadily rebuilding directional bullish exposure as market conditions improve. Net positioning is now approaching its strongest bullish bias since late 2025, reflecting growing confidence in upside continuation.

The sustained long positioning alongside rising price action indicates improving trader sentiment and a more constructive speculative backdrop, although increasingly crowded long exposure could make the market more sensitive to short-term volatility and liquidation-driven pullbacks.

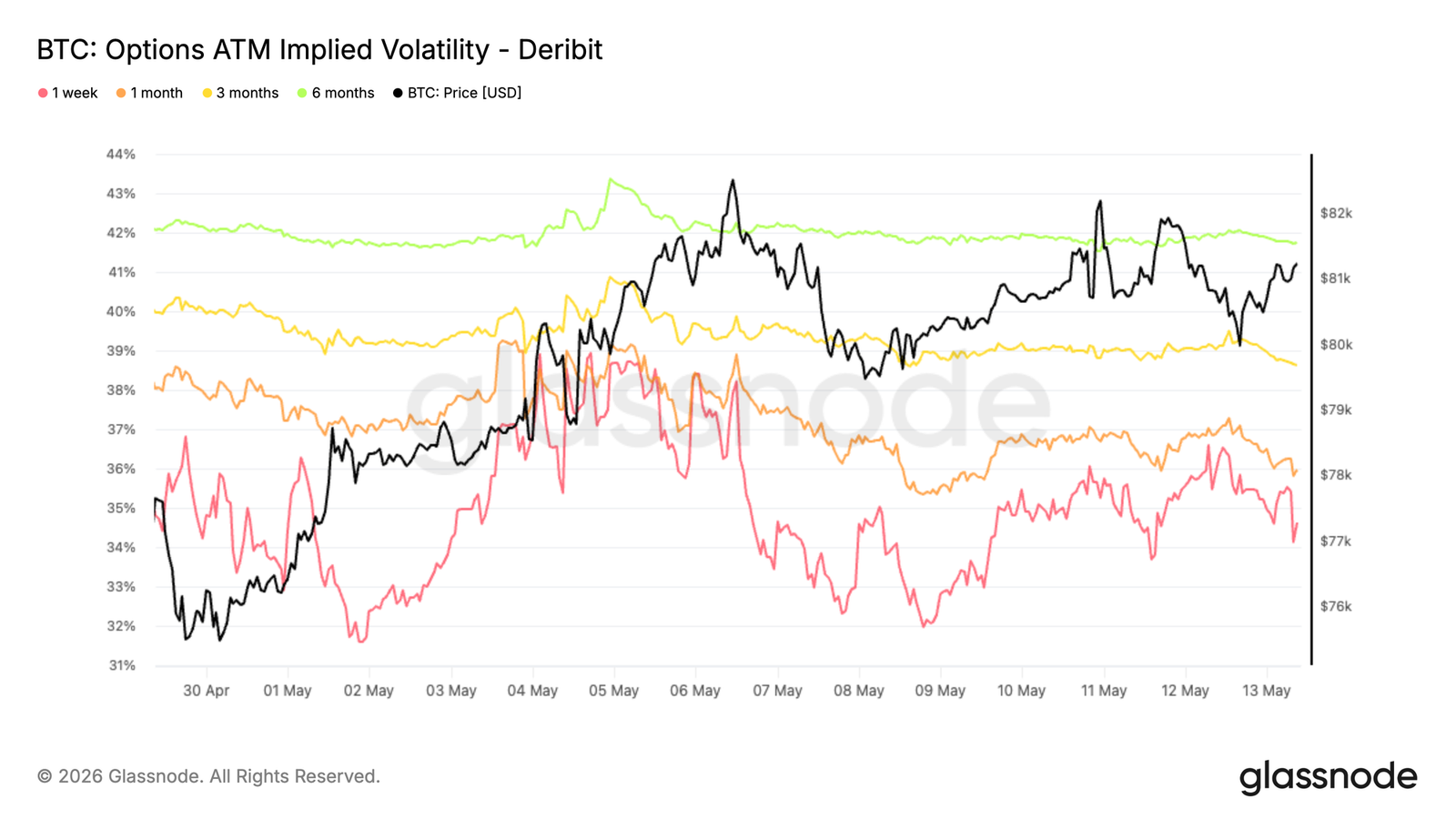

Implied Volatility Declines

Over the past week, Bitcoin implied volatility has turned lower, with the front-month contract falling from 39% to 34.6%. Longer tenors have followed suit, declining by about 1 to 2 vol points across the curve.

This move reflects a broad repricing of the term structure lower, as traders reduce expectations for short-term realized volatility. The decline follows a recent volatility spike and coincides with more controlled spot action, reinforcing the view that the market is returning to a calmer regime.

As implied volatility compresses, option costs decline across tenors, particularly at the front end which is most sensitive to positioning and demand shifts.

The current structure reflects reduced market pricing for significant moves ahead, with volatility supply continuing to outpace demand across the curve.

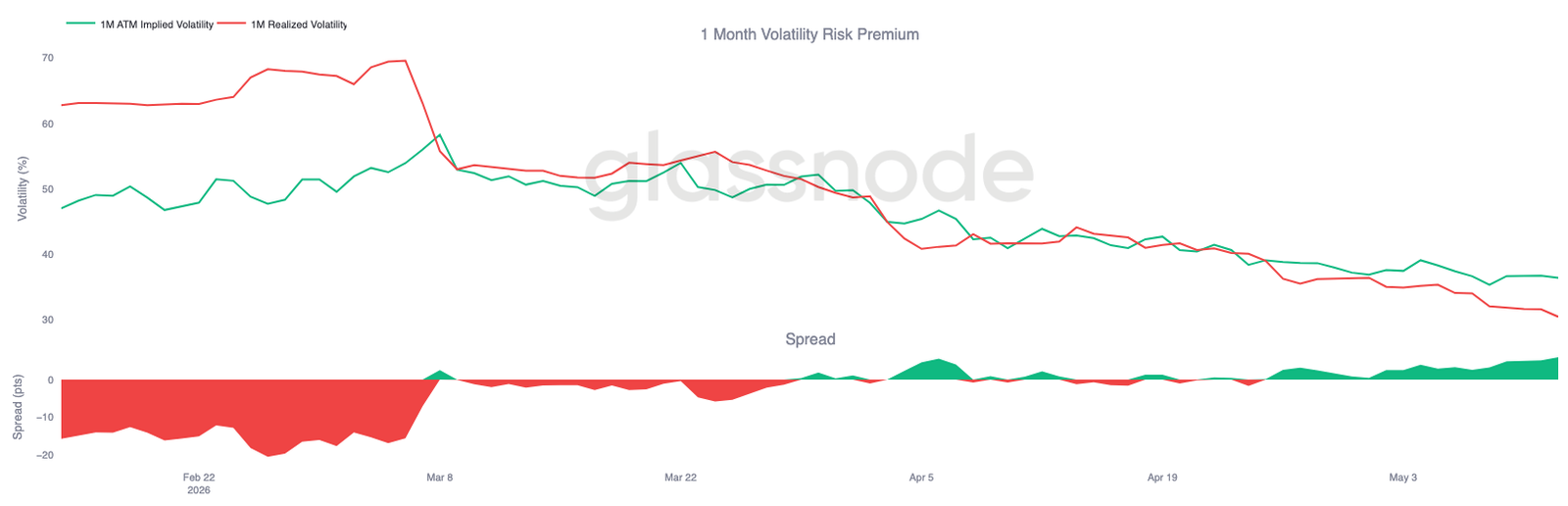

Volatility Risk Premium Remains Positive

While implied volatility continues to compress across the curve, realized volatility is falling faster. Bitcoin's 30-day realized volatility currently stands at 30.48%, steadily declining over the past few weeks as spot action remains relatively contained.

Meanwhile, front-month implied volatility remains around 36.4%, meaning implied continues to exceed realized, maintaining a positive volatility risk premium. In other words, options continue to price in more volatility ahead than Bitcoin's recent spot moves have delivered.

The spread between implied and realized volatility has also been rebuilding over the past two to three weeks, recovering from a brief compression to flat in April to around 6 vol points. This suggests that despite the overall volatility reset lower, option demand relative to realized volatility remains elevated.

Therefore, while overall volatility continues to soften on both the implied and realized dimensions, hedging conditions remain favorable for volatility sellers.

Skew Compression Suggests Waning Downside Hedging Demand

As volatility expectations continue to reset lower, skew is also normalizing across the curve. This move is most pronounced at the front end, with 1-week 25-delta skew compressing from approximately -10% to -4% over the past week. Longer tenors have softened in sympathy, with 1-month, 3-month, and 6-month tenors all losing roughly 1 to 2 points of put premium.

Notably, this compression is occurring against a backdrop of Bitcoin consolidating around the $80,000 range and a less supportive macro environment. The options surface is not showing increased demand for downside protection, but is instead continuing to reprice towards a more balanced structure.

This upside movement reflects a steady reduction in the premium of put options relative to calls, indicating that demand for downside protection across the curve is gradually waning rather than strengthening.

While skew across tenors remains in bearish territory, the ongoing compression suggests that downside hedging demand is gradually easing rather than intensifying.

Market Maker Gamma Keeps Spot Sensitive Near $82,000

Market maker positioning continues to create reactive structures around the current price level. The largest negative gamma concentration is at the $82,000 strike, with exposure around $2.6 billion, while positive gamma accumulates near $85,000, approaching $1.8 billion.

With spot still below the negative gamma cluster at $82,000, a return to that level could trigger reactive market maker hedging flows, strengthening momentum and amplifying price action. Higher up, the positive gamma concentration near $85,000 could act to dampen volatility.

Flows also reflect positioning shifts. Over the past 7 days, put buying accounted for 71% of premium flow, reflecting elevated demand for downside protection during the recent consolidation. 58% of flows over the last 24 hours came from put selling, suggesting some of that hedging is being unwound.

This structure makes the market increasingly sensitive to amplified hedging flows if spot re-enters the large negative gamma cluster near $82,000.

Conclusion

In summary, Bitcoin's recovery continues to strengthen beneath the surface, with spot-driven demand, resurgent ETF inflows, and improved speculative positioning all contributing to a more constructive market structure. The sharp compression in Relative Unrealized Loss, alongside stabilization in key on-chain profitability and liquidity metrics, suggests the February decline is increasingly viewed as a cyclical reset rather than the start of a deeper bear market.

At the same time, the character of this rally is distinctly different from the aggressive expansion seen during the 2023-2025 period. Capital inflows are recovering, but remain well below prior breakout thresholds, while volatility compression and calmer derivatives positioning point to a market gradually rebuilding confidence rather than entering a euphoric phase. This makes the current advance appear more like a structurally supported recovery than a fully confirmed momentum breakout.

With Bitcoin now re-entering the dense overhead supply zone between $82,000 and $87,000, the market is moving into territory where price discovery becomes increasingly important. Sustaining a hold above this zone will likely require stronger spot participation and deeper capital rotation to absorb the remaining overhead supply. Until then, the broader structure continues to improve, but conviction appears to be rebuilding rather than fully restored.