Memory price hike expectations have been significantly upgraded, but Morgan Stanley warns: short-term momentum may have peaked

- Key Point: Morgan Stanley has sharply raised its memory price forecast for 3Q26, noting that memory prices, earnings expectations, and investor positions are already at elevated levels. Short-term stock momentum may weaken, but the long-term outlook driven by AI demand remains positive.

- Key Elements:

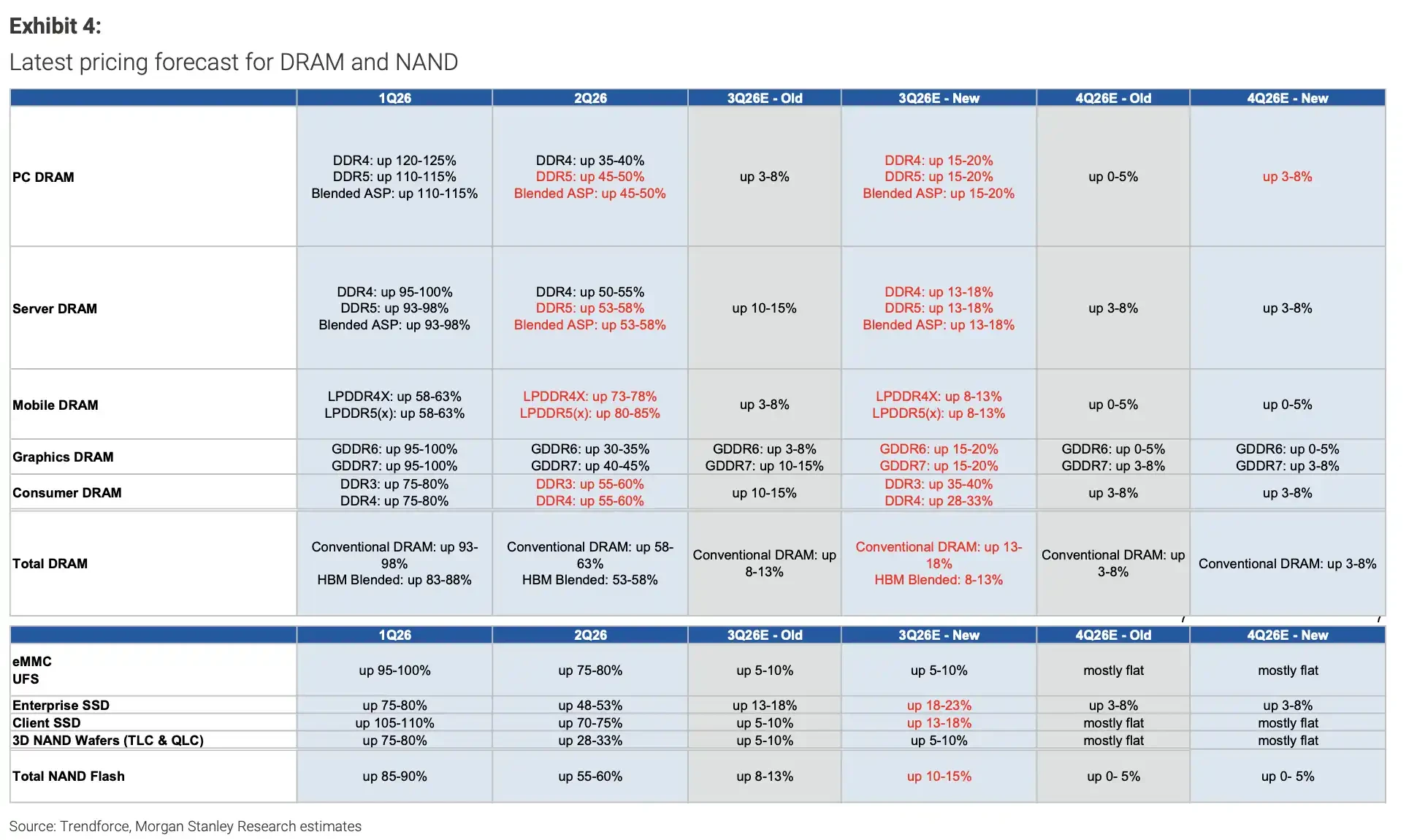

- Significant price forecast upgrade: Morgan Stanley raised its 3Q26 PC DRAM price increase forecast from 3-8% to 15-20%, enterprise SSD from 18-23%, and also revised up forecasts for server DRAM and other segments.

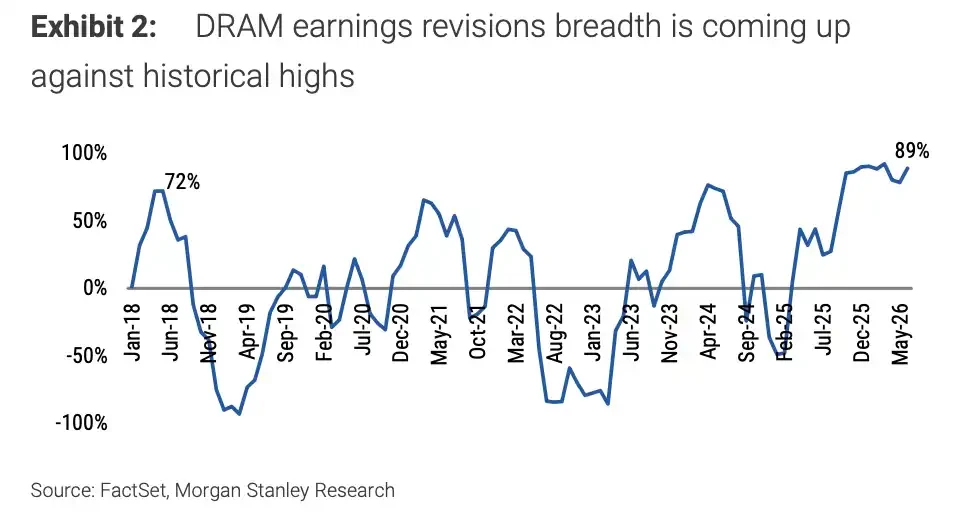

- Earnings revision breadth approaches 89%: The breadth of DRAM earnings revisions is near historical highs, implying that most analysts have already made upward adjustments, making future earnings beats more difficult.

- Short-term pullback risk note: The report is not bearish on the cycle but cautions that stock prices have already priced in positive developments. Following the upward revision of 3Q price forecasts, the market may enter a "good news priced in" phase.

- AI demand support remains intact: Morgan Stanley expects related companies' earnings to grow over 35-40% in 2027. Samsung and SK Hynix continue to be supported by AI demand, but Q3 earnings reports and capex guidance will be key to validating the price hike thesis.

- Shift in investor concerns: The market is beginning to worry about cloud vendors emphasizing efficiency, open-source models, or the risk of over-investment. As a result, memory stock trading sentiment is shifting from focusing on "price increases" to evaluating the "sustainability of price hikes."

TL;DR

- Morgan Stanley has raised its 3Q26 memory price forecasts across multiple categories, while warning that near-term momentum in memory stocks may weaken.

- Under this report's scope, the expected PC DRAM price increase has been raised to 15-20%, with the breadth of DRAM earnings revisions approaching 89%.

- Samsung and SK Hynix continue to be supported by AI demand, but earnings guidance, LTA developments, and capital expenditure commentary will influence the sustainability of the uptrend.

In a research report published on July 7, Morgan Stanley significantly raised its memory price forecasts for the third quarter, but simultaneously cautioned that memory stocks could face near-term correction pressure.

This is not a turn bearish on the memory cycle. The report maintains an 'Attractive' view on the Korean tech sector, continues to favor Samsung Electronics and SK Hynix, and models over 35-40% earnings growth for the related companies by 2027. The real caution lies in the fact that memory prices, earnings expectations, and investor positioning have all reached elevated levels, making it uncertain whether stock prices can continue to rise at the same pace as in recent months.

The most direct indicator is the price forecast revision. The report raised its 3Q26 PC DRAM blended ASP qoq growth estimate from the previous 3-8% to 15-20%, server DRAM to 13-18%, GDDR6 and GDDR7 to 15-20%, and enterprise SSDs to 18-23%.

Public pricing agencies are also aligning with this directional view. In a July 3 article, TrendForce stated that the 3Q26 DRAM market remains extremely tight, with contract prices expected to rise 13%-18% qoq and NAND Flash contract prices expected to increase 10%-15%. However, TrendForce also noted that while server DRAM remains in short supply, longer-term supply agreements could moderate the pace of increases.

Prices are still rising, but trading memory stocks is becoming more challenging. According to Morgan Stanley's report, the breadth of DRAM earnings revisions has recently approached 89%, nearing historical highs. The memory rally over the past two years, driven by AI capital expenditure, HBM, and server demand, has already priced in much of the positive news into stock valuations.

The Sharpest Price Hikes Are for Q3, and Concerns Are Concentrated There Too

The scope of this upward revision is broad. Beyond PC DRAM, price expectations for 3Q26 server DRAM, graphics DRAM, conventional DRAM, and enterprise SSDs have all been significantly raised. Among these, the 15-20% increases for PC DRAM and graphics DRAM represent the most easily identifiable price signals for the market. The 18-23% increase for enterprise SSDs indicates that the memory price rally is not confined to AI server-related categories.

That's where the problem lies. The faster price expectations are raised, the easier it becomes for stocks to enter a phase of 'pricing in good news'.

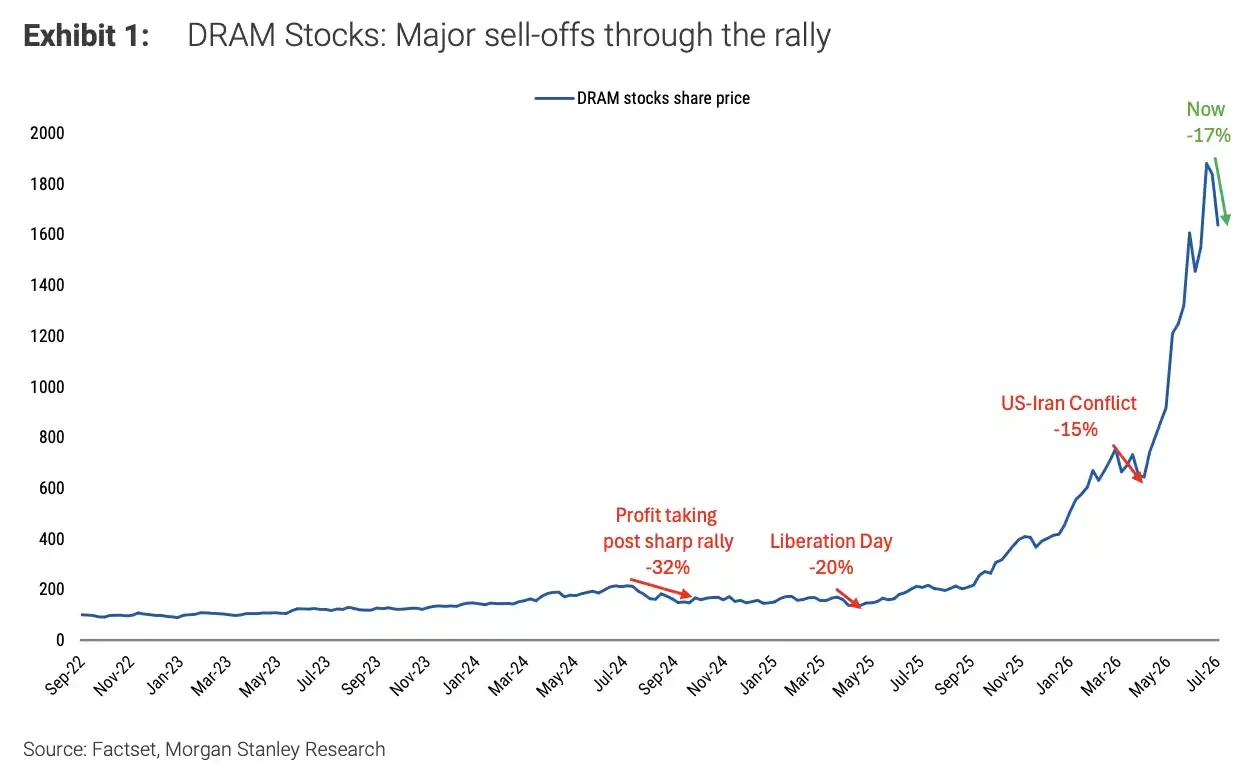

Memory stocks have experienced corrections over the past two years. Morgan Stanley's analysis shows that since the generative AI wave began in November 2022, DRAM-related stocks have seen three notable drawdowns, including profit-taking, event-driven shocks, and multi-week corrections. None of these interruptions derailed the secular trend driven by AI capex, but they serve as reminders that even in a strong cycle, significant interim declines can occur.

The three major corrections in DRAM stocks were approximately -25%, -25%, and -35%, respectively, yet the overall trend rose from 2022 lows to 2026 highs.

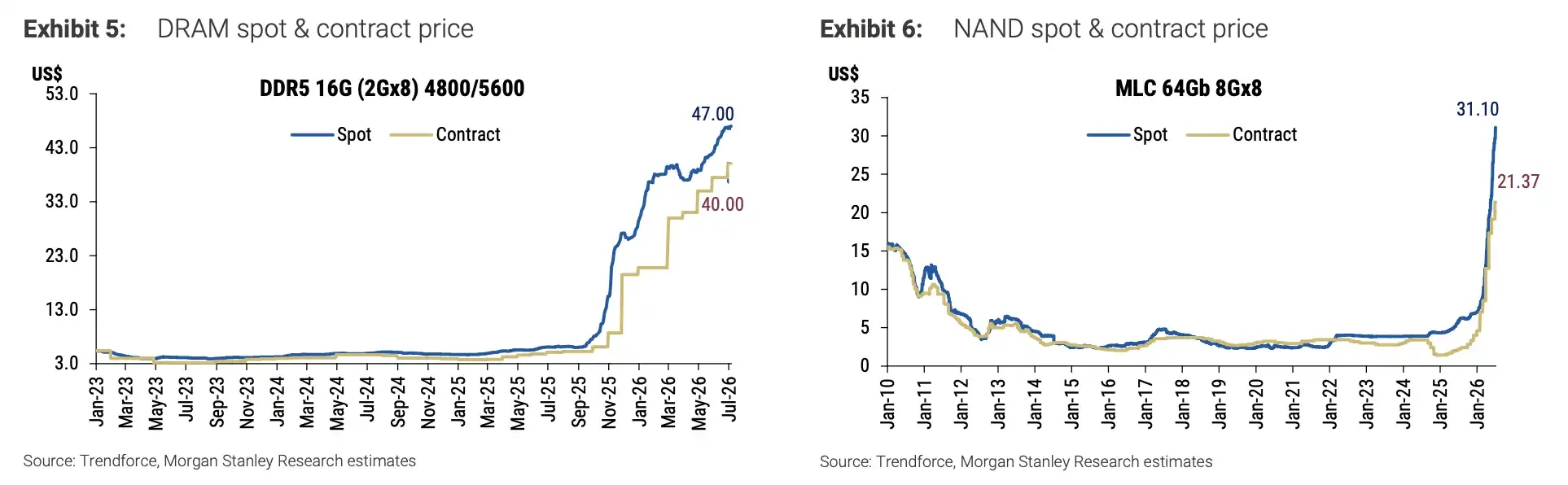

Spot prices also support the narrative of rising prices. The report's price tracking shows that DRAM spot prices have rallied sharply since early 2025, NAND spot prices have also rebounded significantly from recent lows, and while contract prices lag, they are trending in the same upward direction. In other words, the caution regarding a short-term correction is not because fundamentals have deteriorated, but because prices and expectations have risen too quickly.

DDR5 16Gb spot price has risen to around $47, while MLC 64Gb NAND spot price recently climbed to $31.10.

Earnings Revisions Near Highs, Memory Stocks Need to Digest Expectations

For stocks, more critical than the prices themselves is the remaining potential for upward earnings revisions.

The breadth of DRAM earnings revisions has recently reached approximately 89%, situated near historical highs. This metric indicates that a growing number of analysts are raising their earnings forecasts. When the majority has already revised earnings upwards, the difficulty of further positive surprises increases.

The breadth of DRAM earnings revisions rose to approximately 89% after 2025, approaching the historical peak range.

This is one reason why near-term momentum may diminish. It's not that memory stocks lack fundamental support, but that price increases, earnings upgrades, crowded positioning, and AI-linked sentiment have all converged. If earnings guidance proves insufficiently strong, capex commentary fails to impress, or large cloud company stocks come under pressure, the memory sector could experience amplified volatility.

Morgan Stanley still prefers DRAM and conventional memory, where capital expenditure flows are more tangible and supply bottlenecks are clearer, viewing their attractiveness as superior to NAND, and is least favorable towards memory module makers. This ranking suggests the market isn't simply betting on 'all memory prices rising,' but is focusing on whether price increases can genuinely translate into actual profits.

The expected PC DRAM price increase for 3Q26 has been raised from 3-8% to 15-20%, enterprise SSD to 18-23%, with upward revisions across multiple DRAM categories simultaneously.

Samsung Has Issued Guidance, SK Hynix Awaits End of Month

The earnings reports from South Korea's two memory giants will act as a key test for the price hike narrative.

Samsung Electronics released its 2Q26 earnings guidance on July 7. The company expects sales of approximately KRW 171 trillion and operating profit of around KRW 89.4 trillion, with the operating profit range between KRW 89.3 trillion and KRW 89.5 trillion. For Samsung, the market will look beyond just quarterly profit, focusing on the strength of its memory business recovery, progress in AI-related products, and whether continued price increases in traditional memory can further improve profitability.

SK Hynix's earnings release date is still pending. Public market calendars indicate the company is expected to report its next earnings on July 29. Given SK Hynix's more prominent position in HBM and AI server memory, the market will be more sensitive to its commentary on 3Q commodity memory prices, long-term supply agreements (LTAs), and capital expenditure plans.

If management confirms continued strength in Q3 commodity memory, an increase in LTA commitments, and only a moderate increase in capex, a short-term correction might resemble a healthy pullback. However, if guidance proves insufficiently strong, or if capex is interpreted as leading to overly rapid supply growth, the market may reassess how long the memory price rally can persist.

LTAs themselves are not risk-free signals. Historically, long-term agreements do not guarantee stock price increases; some have been renegotiated or have acted as constraints forcing clients to take delivery when demand shifts. The market will scrutinize not just 'how much was signed,' but also the pricing terms, duration, counterparty quality, and execution flexibility.

AI Demand Persists, But Market Questions Potential Oversupply

The long-term bullish thesis still rests on AI, specifically AI agents capable of executing tasks, using tools, and interacting continuously. Morgan Stanley expects the relevant companies' earnings to still grow over 35-40% by 2027, which is why the firm does not equate the short-term correction risk with the end of the cycle.

Nevertheless, the debate around AI demand is evolving. Previously, the market primarily bet on the continuous expansion of model training and inference scales, driving demand for computing power and memory. Now, some investors are beginning to worry that post-Q3, cloud providers might place greater emphasis on token savings, inference efficiency, open-source low-cost models, and the pressure of chip inflation on margins.

There is an even more sensitive issue: whether the largest AI spenders truly have *marketable* computing capacity, thus implying that prior buildouts might have been cyclically excessive. This notion has yet to form a definitive conclusion, but it is enough to make the market more cautious ahead of earnings reports from major cloud companies.

The divergence in this memory cycle is not about whether AI demand will vanish immediately, but whether price increases, earnings upgrades, and customer capex can continue to reinforce each other in the same direction. If Q2 AI supply chain earnings remain favorable, but Q3 guidance begins to weaken immediately after, memory stocks could first undergo a round of valuation and positioning adjustments.

The memory cycle remains within the broader context of AI capital expenditure. However, near-term trading has shifted from 'how much prices have risen' to 'how long the market can continue to believe in these increases.' The upcoming earnings communication from Samsung and SK Hynix, commentary on cloud provider capex, and the execution of LTAs will determine whether this correction is merely a pause within a bull market, or the beginning of a genuine slowdown in the pace of the uptrend.