Goldman Sachs Semiconductor Earnings Preview: Can AMD and AMAT Continue to Rise After the SOX Surge?

- Key View: Goldman Sachs believes there is still room for upward revisions in semiconductor earnings for the second quarter, but the sector has already rallied significantly (SOX up 87.8% in a single quarter), making a broad-based rally unsustainable. The core themes are AI capex, DRAM/HBM, advanced packaging, and EDA tools, while individual stock performance divergence will intensify.

- Key Elements:

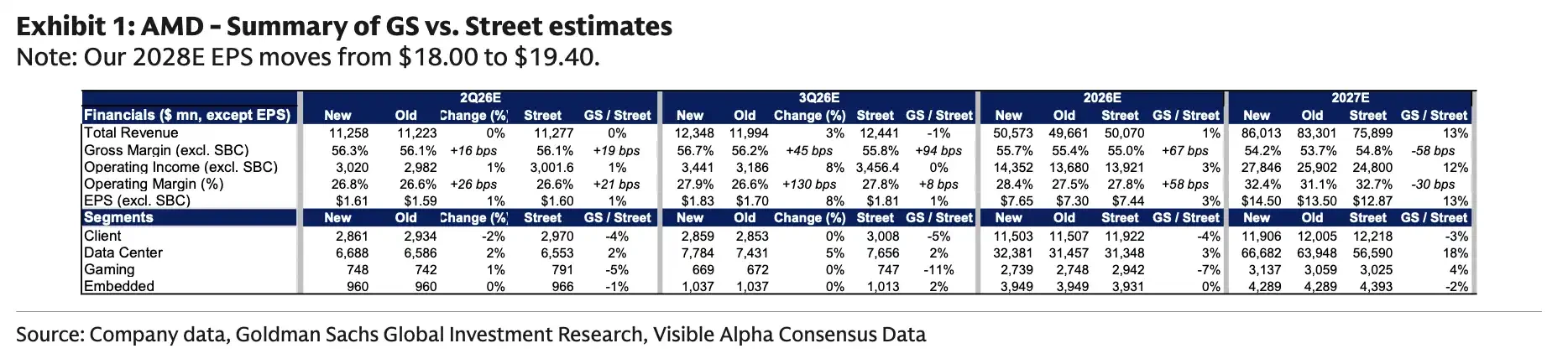

- AI CapEx drives the computing segment: AI server CPUs, cloud provider ASIC projects, and AI accelerators support data center revenue for companies like AMD. AMD's 2027 EPS forecast has been raised to $14.50, 13% above market consensus.

- Memory and equipment benefit from mid-term demand: DRAM/HBM supply-demand remains tight, HDD pricing is improving. Equipment company order visibility extends to 2028, with Applied Materials' price target raised to $645, driven by DRAM investment boosting 2026 growth.

- Analog semiconductors show clear divergence: Goldman Sachs prefers companies with high exposure to industrials, aerospace & defense, and data centers (e.g., ON Semiconductor), while being more cautious on names reliant on smartphones or traditional automotive cycles.

- ARM and KLA require caution: ARM faces pressure from weak smartphone demand and high operating expenses, maintaining a Sell rating. KLA may underperform peers due to WFE spending shifting towards DRAM.

- EDA and Qualcomm benefit from AI diffusion: Cadence is driven by agentic AI tools and EDA demand, with potential for revenue guidance upgrades. Qualcomm's data center business is incorporated into its growth narrative, with FY27-28 revenue models set at $5.0-8.2 billion.

TL;DR

- Goldman Sachs expects most semiconductor sub-sectors to have room for upward revisions in Q2, but the SOX has already risen approximately 87.8% in the single quarter.

- AI capex, DRAM/HBM, advanced packaging, and EDA tools are the primary drivers of this round of earnings upgrades.

- Goldman Sachs prefers AMD, AMAT, and ON, while being more cautious on ARM and KLAC; Qnity requires holding an attitude subject to limitations after its price surge.

Before the semiconductor earnings season, stock prices had already run up significantly. A review of the Nasdaq's second quarter shows the PHLX Semiconductor Index rose 87.8% in Q2, marking its best quarterly performance since its inception in 1994, far outperforming the broader US stock market. In a semiconductor Q2 preview, Goldman Sachs assessed that while fundamentals still have room for upward revision, the sector post-rally is no longer suitable for a "buy everything" approach. AI servers, memory, advanced packaging, and design software remain the strongest themes, while weak smartphone demand, shifts in equipment spending structure, and export restrictions will amplify individual stock differences.

Semiconductors Still Have Room for Upgrade, but the AI Chain is Starting to Diverge

Goldman Sachs reported that Q2 results or subsequent guidance for companies in computing, memory storage, semiconductor equipment, and some analog semiconductor firms could still exceed market expectations.

The main theme in the computing sector remains AI servers. Server CPU demand, cloud provider ASIC projects, and the ramp-up of AI accelerators continue to support data center revenue expectations for companies like AMD. Memory and storage benefit from tight DRAM/HBM supply-demand dynamics, improved HDD pricing, and positive NAND cycle expectations, with limited near-term pressure from new supply additions.

The equipment chain narrative is more medium-term focused. AI servers require more HBM and advanced packaging, and memory manufacturers' capacity expansion and technology upgrades will drive demand for deposition, etching, and other process steps. Some equipment companies already have order visibility extending into 2028.

The analog semiconductor sector is not experiencing a broad-based recovery. Goldman Sachs prefers companies with higher exposure to industrial, aerospace & defense, and data center end-markets, while remaining more cautious on names more dependent on smartphones or the traditional automotive cycle.

This divergence is also reflected in Goldman Sachs' tactical choices. The report shows a preference for Applied Materials, AMD, and ON Semiconductor, while being more cautious on ARM and KLA. For semiconductor materials and electronic solutions company Qnity, Goldman Sachs remains positive on wafer fab utilization improvements and execution performance but believes the risk-reward profile has become more balanced after the stock price rally, a judgment primarily derived from the report's tone.

AMD and Applied Materials are Goldman Sachs' Two Most Clear Long Picks

AMD is one of Goldman Sachs' most definitive long cases within the computing chain. Goldman Sachs' model estimates AMD's 2027 EPS forecast at $14.50, approximately 13% higher than the consensus market estimate. The 2027 data center revenue forecast is $66.682 billion, roughly 18% above market expectations.

Supporting this judgment are strong server CPU demand, improving gross margins in the data center business, and operating leverage from the subsequent ramp-up of AI chips. AMD previously announced that its Advancing AI 2026 event will be held live in San Francisco on July 23, 2026. Beyond the earnings season, the market will be watching whether AMD can provide a clearer AI server roadmap, customer progress updates, and revenue trajectory during this event.

Goldman Sachs model shows AMD 2027E EPS at $14.50, above the market consensus of $12.87. 2027E data center revenue is $66.682 billion, higher than the market estimate of $56.590 billion, with server CPU and MI450 ramp being key drivers.

Applied Materials represents the end of the equipment chain with stronger order visibility. Goldman Sachs raised its price target for Applied Materials from $520 to $645, based on 32x a normalized EPS of $20. A key assumption in the report is that strong DRAM investment will drive the company's best-in-class growth in 2026, with WFE demand visibility extending to 2028.

DRAM is the focal point here. Rising demand from AI servers for HBM and high-performance memory will drive capacity expansion and process upgrades for memory manufacturers. The advantage for equipment companies lies in their longer order cycles and higher revenue visibility. The risk is also direct: a slowdown in capex by cloud providers or memory makers would quickly lead to downward revisions in market expectations for medium-term revenue.

Goldman Sachs model shows AMAT CY2027E total revenue of $45.972 billion, up 25% year-over-year. The DRAM segment is expected to contribute $12.4 billion, up 41% year-over-year, serving as the primary driver for equipment upside.

ON Semiconductor is positioned in a relatively positive portfolio context, not because of significant upward revisions, but because near-term expectations have already been lowered. On June 25, the company announced its intention to acquire Synaptics in an all-stock transaction valued at approximately $7 billion, expected to close by mid-2027, subject to approvals including Synaptics' shareholders. Goldman Sachs believes that after investor expectations have pulled back, there is more focus on the potential for ON Semiconductor's quarterly performance to slightly beat expectations.

ARM and KLA Show: The Bigger the Rally, the Harder it is to Ignore Earnings Blemishes

Goldman Sachs maintains a Sell rating on ARM with a 12-month price target of $150, based on 50x a normalized EPS of $3. Pressure stems from two main areas: persistently weak smartphone demand and higher-than-expected operating expenses.

ARM is still viewed by the market as a potential beneficiary of AI and high-performance computing, but the more immediate revenue and profit pressures in near-term earnings come from licensing revenue on the handset side and cost expansion. For stocks already priced up by the AI narrative, the market will pay more attention to whether near-term revenue, margins, and guidance can materialize.

KLA's pressure comes from the composition of equipment spending. Goldman Sachs expects its quarterly results and guidance could see slight upside but still underperform peers because WFE spending is tilting towards DRAM. Compared to logic chips and foundry, DRAM has lower intensity for inspection and metrology equipment. While the overall equipment cycle is moving upward, it doesn't mean all equipment segments benefit equally.

Qnity's situation sits between the two. The company's Q1 announcement reported Q1 2026 net sales of $1.315 billion and raised its full-year guidance. Goldman Sachs still holds a positive view on improving wafer fab utilization and the company's execution, but the report judges that the upside potential is now more balanced with downside risks after the stock price increase. For individual stocks that have already priced in a recovery, earnings need not only to deliver good results but also to provide sufficiently strong forward guidance for the next phase.

EDA and Qualcomm Also Pulled into the Earnings Spotlight by AI

AI expectations are not confined to the GPU, CPU, and memory chain; they are also spreading to chip design software and data center chips.

Cadence is one of the companies in the EDA chain favored by Goldman Sachs. Public information shows that after the first quarter, the company raised its 2026 revenue outlook to approximately 17% year-over-year growth and launched an engineering solution with NVIDIA for agentic AI chip and system design. Goldman Sachs further expects that driven by the monetization of agentic AI tools, IP business, and core EDA demand, the company's 2026 revenue guidance still has room for upward revision.

Qualcomm's data center business is also being re-evaluated. The company mentioned in its previous Investor Day materials that the data center business would start contributing billions of dollars in revenue from FY27 onwards. Goldman Sachs' model sets Qualcomm's FY27 and FY28 data center revenue at $5 billion and $8.2 billion, respectively. For Qualcomm, this represents an expansion of the growth narrative from mobile chips to data centers, but orders, customers, and gross margins still need to be consistently delivered.

The question this earnings season needs to answer is straightforward: Can AI capital expenditure continue to drive earnings upgrades for semiconductor companies? Over the past quarter, stock prices have already reflected optimistic expectations. Going forward, the strength of server CPUs, ASICs, HBM, EDA, and equipment orders must be incorporated into 2026 and 2027 revenue and profit models to sustain valuations post-rally.

Whether Upgrades Can Catch Up to Stock Prices Will Determine the Degree of Earnings Season Divergence

The key for the semiconductor Q2 earnings season is not whether the market still has upside expectations, but whether the magnitude of the upside can cover the stock prices that have already risen.

Goldman Sachs' preview offers a more divergent answer. AI capex, DRAM/HBM, advanced packaging, and the monetization of EDA tools continue to push up earnings expectations for some companies. After the SOX has significantly outperformed the broader market, market tolerance for imperfections is declining.

Weak smartphone demand will pressure ARM, the tilt of WFE towards DRAM will erode KLA's relative advantage, and supply chain constraints, export restrictions, and geopolitical risks could also impact order fulfillment. Companies like AMD and Applied Materials, which still have room for model upgrades, will face questions about the pace of execution. Companies that have already rallied significantly but have limited short-term fundamental flexibility are more likely to face pressure during the earnings season if their guidance is not strong enough.