Citi Analysis: S&P 500 Baseline Could Reach 8,100 Points, But the Bull Market "Ceiling" Is Approaching

- Core View: Citi has raised its baseline target for the S&P 500 by end-2026 to 8,100 points, reflecting earnings surprises and accelerating AI capital expenditure. However, sentiment has entered exuberance territory, valuation pressure is rising, upside elasticity is narrowing, and the risk-reward profile has become asymmetric.

- Key Elements:

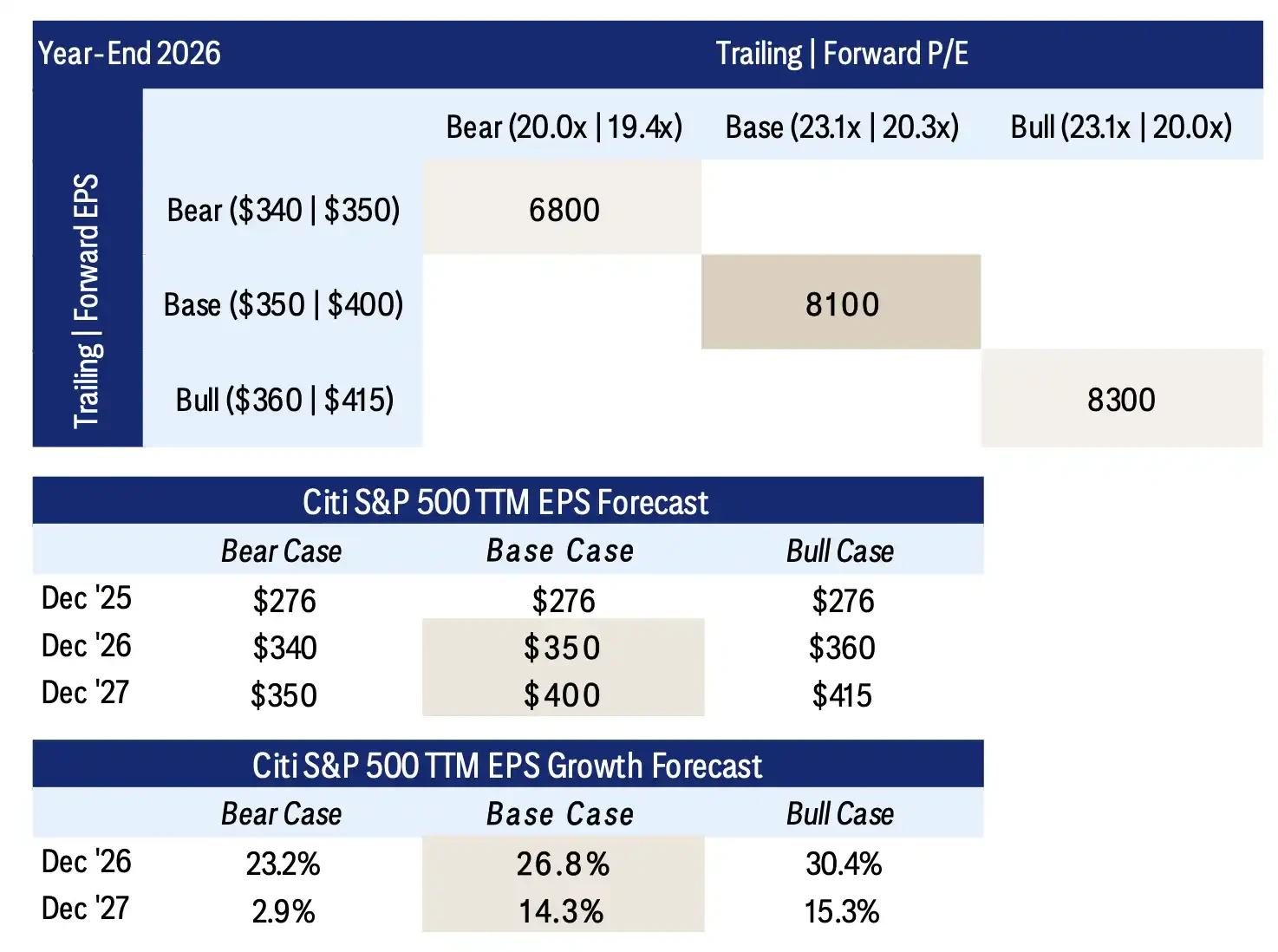

- Citi raised its S&P 500 baseline target to 8,100 points, corresponding to $350 in EPS and a 23.1x trailing P/E ratio. However, the bull case target remains unchanged at 8,300 points, a mere 200 points higher, suggesting limited upside.

- The upgrade is primarily driven by earnings surprises: Q1 2026 EPS reached $81.0, surpassing forecasts by 13.1%; the Mag 7* group's Q1 earnings upward revision was 34.5%, remaining the core of earnings improvement.

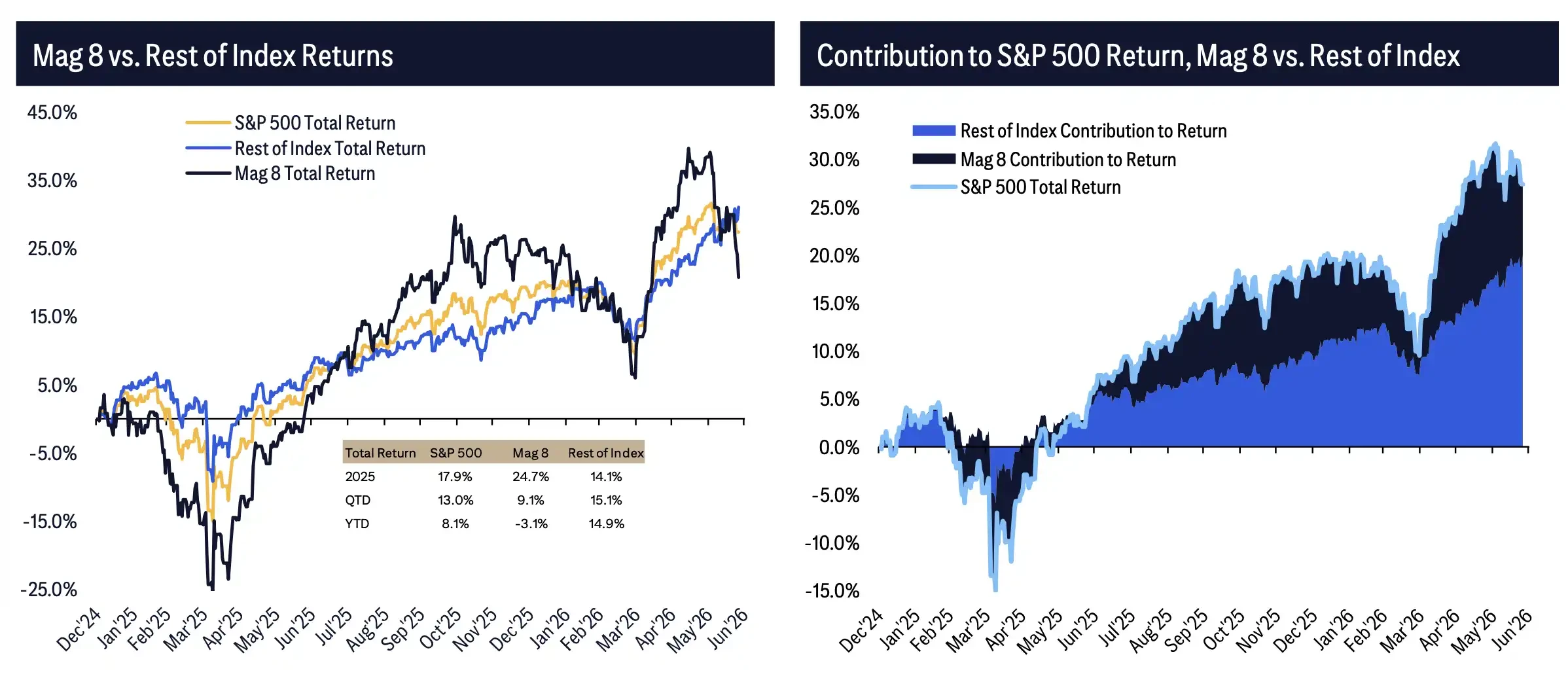

- Market breadth is improving, with gains spreading from the Mag 7: Year-to-date in 2026, the total return for the "other 492 companies" is approximately +14.9%, while the Mag 7 has fallen about 3.1%; the S&P 600 small-cap index has a year-to-date return of roughly +22.3%, outperforming the broader market.

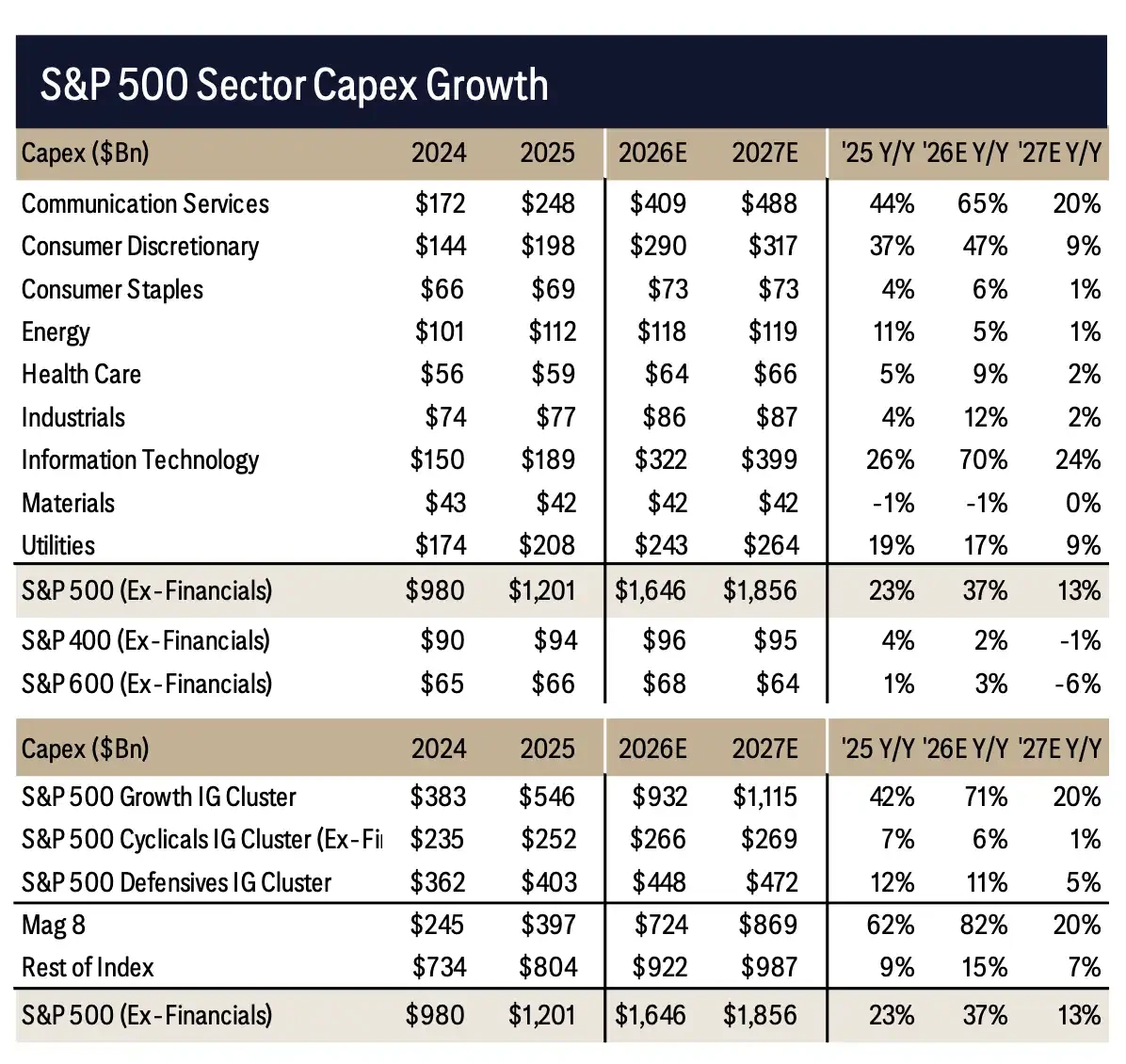

- AI capital expenditure continues to accelerate: Excluding financials, S&P 500 CapEx for 2026 is projected at approximately $1.65 trillion, a growth rate of 37%; Mag 7 capital expenditure is expected to grow by 82% in 2026, but the market is beginning to question the return on investment.

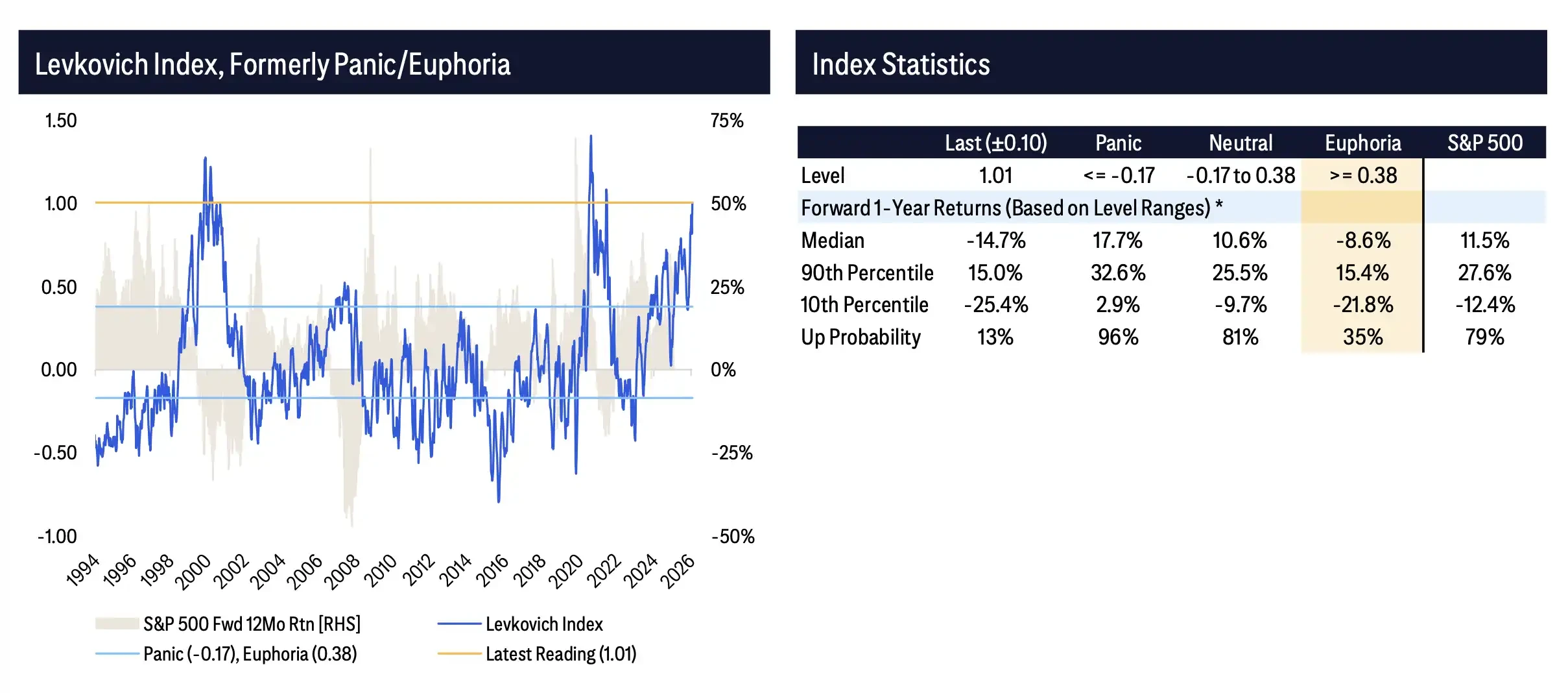

- Sentiment indicators have entered exuberance territory: The Levkovich Panic/Euphoria Index reads 1.01, exceeding the Euphoria threshold of 0.38. Historically, at this level, the median return over the following year has been -8.6%, with only a 35% probability of an upward move.

- Fund flows are crowded: Foreign net purchases of U.S. equities as a percentage of market cap are near 30-year highs. Fund flows into mutual funds and ETFs are at 10-year highs, leaving the market with less buffer room for bad news.

TL;DR

- Citi raised its year-end 2026 S&P 500 base target from 7,700 to 8,100 points, but maintained its bull case target at 8,300 points.

- The upward revision is primarily driven by better-than-expected Q1 earnings and accelerated AI capital expenditure, with $350 EPS becoming the new base case assumption.

- The US stock market rally has broadened from the Mag 8 to other companies and small-mid caps, but sentiment has entered euphoric territory, limiting upside potential for chasing highs in 2H.

In its 2H 2026 US Equity Strategy report, Citi raised its year-end S&P 500 base target from 7,700 to 8,100 points, while keeping the bull case target unchanged at 8,300 points, and cautioned that risk-reward for US stocks in the second half has become asymmetric.

The key signal from this report is: Citi acknowledges stronger fundamental earnings and that the index has continued support for an upward move, but after raising the base case, the bull case is only 200 points higher, implying diminishing elasticity for further upside.

The 8,100 target corresponds to a 23.1x trailing P/E and $350 EPS. Compared to the ~$320 EPS estimate entering 2026, the earnings assumption has been significantly revised upward. The bear case target is 6,800, corresponding to a 20.0x P/E and $340 EPS. In other words, Citi does not deny the improvement in US stock fundamentals; it merely suggests that current prices already discount a considerable amount of positive news.

Base case 8,100, Bull case 8,300, Bear case 6,800, Base EPS $350.

Earnings Stronger than Expected, Citi Lifts Base Target to 8,100

The direct reason for the target upgrade is earnings. The S&P 500 recorded Q1 2026 EPS of $81.0, 13.1% above expectations from late last year, representing a positive surprise of 13.4%.

Technology, Communication Services, and Energy drove full-year earnings estimates higher during the reporting season, with Information Technology contributing the most. The upward revision for Mag 8 Q1 EPS reached 34.5%, indicating large-cap tech remains the core source of earnings upgrades.

However, earnings improvement is beginning to broaden from a handful of mega-caps to a wider range of companies. Consensus S&P 500 EPS growth for 2026 is projected at 24.2%, with the Growth cluster growing 41.8%, Cyclicals at 17.6%, and Defensives at only 5.8%. Mag 8 EPS growth is estimated at 38%, while the rest of the index components also see roughly 19% growth.

This makes the rally's logic more dependent on "earnings broadening." If earnings growth can transmit from the Mag 8 to more sectors and companies, the high-valuation index still has fundamental support; if the broadening falls short, the valuation pressure corresponding to the 8,100 level will become apparent more quickly.

Rally No Longer Solely Driven by Mag 8, Market Breadth Improving

The internal structure of the US stock market has changed this year. Year-to-date in 2026, the "other 492 companies" have delivered a total return of approximately +14.9%, while the Mag 8 have actually declined by about -3.1%.

Small and mid-cap performance has also improved markedly. The S&P 600 small-cap index is up about +22.3% year-to-date, and the S&P 400 mid-cap index is up about +16.3%, both outperforming the large-cap index. For investors, this is significant: the more concentrated the rally in a few tech giants, the easier it is perceived as valuation-driven; as earnings and stock performance broaden to more companies, the foundation for the index's rise becomes wider.

Small-cap value stocks are also in a supporting role. The S&P 600 Value forward P/E is around 13.8x, below its 20-year median of 17.2x, with 2026 EPS growth expectations of 25%. This supports a more diversified US equity allocation approach, where capital doesn't need to continue concentrating on large-cap growth stocks.

However, the broadening of the rally also means more sectors have already been bought by capital. Increased market participation can enhance the uptrend's resilience but can also widen the scope of a correction when earnings realization slows. If fundamentals subsequently disappoint, the pullback may not be limited to a few large-cap tech stocks.

Market Participation YTD 2026: Mag 8 Return -3.1%, Other 492 Companies ~+14.9%.

AI Spending Still Accelerating, But Market Begins Questioning Returns

AI remains a key pillar of this earnings upgrade cycle. S&P 500 capex (ex-Financials) is projected to rise from approximately $1.20 trillion in 2025 to about $1.65 trillion in 2026, with growth accelerating from 23% to 37%; it could potentially increase further to around $1.86 trillion by 2027.

Mag 8 capex growth is even higher, projected to increase by 82% in 2026. Information Technology and Communication Services are the primary drivers, underpinned by continued expansion in data centers, chips, cloud infrastructure, and AI training and inference demand.

This explains why Citi was willing to raise its base case: AI infrastructure investment continues to boost revenue, orders, and earnings expectations. But risks are also accumulating simultaneously. The larger the capex scale, the more the market needs to see these investments ultimately translate into revenue, margins, and free cash flow. If AI spending continues to expand but commercialization returns are slower than expected, current earnings upgrades could morph into future valuation pressure.

Stock buybacks also provide a layer of support. The S&P 500's total buybacks over the past 12 months are close to $990 billion, up 10% year-over-year. However, buyback growth for the Growth cluster and Mag 8 has already slowed, with more resources directed toward capex. This suggests that large-cap tech companies' cash deployment focus is shifting from directly rewarding shareholders to continuing investment in AI infrastructure.

Capex Acceleration: S&P 500 ex-Financials 2026E Capex ~$1.65 Trillion, Mag 8 2026E Growth 82%.

Sentiment Enters Euphoric Territory; Target Upgrade Doesn't Mean Risk-Free Chasing

Citi's most cautious part focuses on sentiment and valuation.

The latest reading of the Levkovich Panic/Euphoria Index is 1.01, which has entered the Euphoria zone, whose threshold is 0.38. Historically, starting from similar levels, the median S&P 500 return over the next year is -8.6%, with only a 35% probability of being positive.

These numbers make the 8,100 target seem less aggressive. Earnings and fund flows can explain why US stocks still have upside potential, but sentiment indicators suggest the market is already in a relatively crowded position. Foreign net buying of US stocks remains strong, with the past 12 months' proportion relative to S&P 1500 market cap near 30-year highs; equity fund flows for mutual funds and ETFs are also in their 10-year high territory this year. Capital is still flowing in, but the fuller the positions, the smaller the buffer for the market to absorb bad news.

Consumer resilience provides some macro support. Approximately 70% of US household debt is mortgage-related, much of it locked in at lower fixed rates, weakening the transmission of Fed rate hikes to household cash flows. Post-fiscal stimulus deleveraging also leaves household balance sheets relatively sound.

However, high valuations, euphoric sentiment, pressure for AI capex to deliver returns, and potential geopolitical supply shocks could still disrupt market performance in the second half. Citi raised its base target but refrained from further lifting the bull case ceiling. The core implication is clear: US stocks still have earnings support, but the first half's rally logic cannot be simply extrapolated. For investors, 8,100 looks more like a reasonable midpoint after earnings upgrades, while 8,300 serves as a reminder that the room for chasing highs has narrowed.

Levkovich Sentiment Indicator. Current reading 1.01, entering Euphoria, historically median forward 1-year return is -8.6%.