超级无敌螺旋大爆炸,美光财报重燃半导体长牛

- Core Viewpoint: Micron's Q3 FY2026 earnings far exceeded expectations, with revenue of $41.456 billion, a year-over-year increase of 346%, and a Q4 revenue guidance of $50 billion. Behind this is AI demand spreading from HBM to the entire memory industry chain, with revenue locked in through long-term agreements. This validates that AI infrastructure construction is still in its early stages, reigniting confidence in the semiconductor bull market.

- Key Elements:

- Q3 Results and Q4 Guidance Beat Estimates: Revenue of $41.456 billion (+346% YoY) significantly surpassed the market expectation of $35.4 billion; Q4 revenue guidance of $50 billion far exceeded the market expectation of $42.9 billion.

- AI Demand Spreads Across the Entire Industry Chain: Cloud, data center, mobile, and other businesses grew synchronously, with gross margins generally exceeding 80%, indicating AI is driving the entire memory market into a robust pricing cycle.

- Long-Term Strategic Agreements Lock in Future Revenue: 16 long-term agreements have been signed, covering 20% of DRAM and one-third of NAND shipments. Adopting a "take-or-pay" model, the guaranteed revenue is approximately $100 billion.

- Customers Provide Performance Bonds: Customers have provided a total of approximately $22 billion in performance bonds, of which about $18 billion is cash, directly supporting capacity expansion and R&D.

- Capital Expenditure Accelerates Expansion: Q4 CapEx is expected to reach $10 billion, totaling about $27 billion for the full FY2026. Investments are directed towards HBM and advanced DRAM, but expansion is based on locked-in orders.

- HBM Capacity Sold Out: All HBM capacity for 2026 is sold out. HBM4 has begun volume shipments, with HBM4E planned for mass production in 2027, solidifying its leadership in AI memory.

- Positive Market Reaction: After the earnings report, Micron’s stock surged 16% in after-hours trading, driving gains across the global semiconductor sector. South Korea's stock market saw circuit breakers triggered, and the A-share semiconductor industry chain strengthened.

Original by Odaily (@OdailyChina)

Author: Azuma (@azuma_eth)

In the early hours of June 25, Beijing time, Micron's highly anticipated Q3 FY2026 earnings report was officially released.

Prior to this quarter's earnings release, Micron faced a somewhat awkward situation. On one hand, everyone knew it would deliver stellar results. On the other, everyone also knew the market had already priced in that "stellar" performance well in advance.

Over the past few weeks, market participants across the board have been grappling with essentially the same question: For a memory giant already at the epicenter of the AI wave, just how strong does its performance need to be to continue driving its stock price higher and inject further confidence into an already frenzied semiconductor bull market?

The answer is: Even more exaggerated than anyone anticipated!

The Market Was Aggressive Enough, But Still Too Conservative

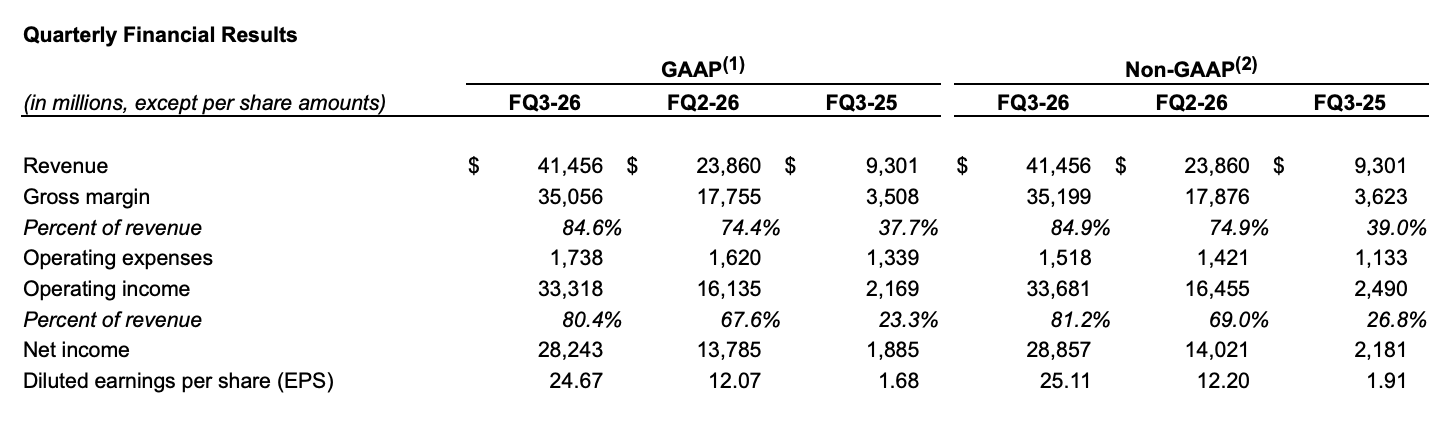

The Q3 earnings released this morning show that Micron's third-quarter revenue reached $41.456 billion (market consensus was around $35.4 billion), a staggering 346% year-over-year increase; GAAP net income was $28.243 billion, surging nearly 15 times year-over-year; adjusted earnings per share were $25.11.

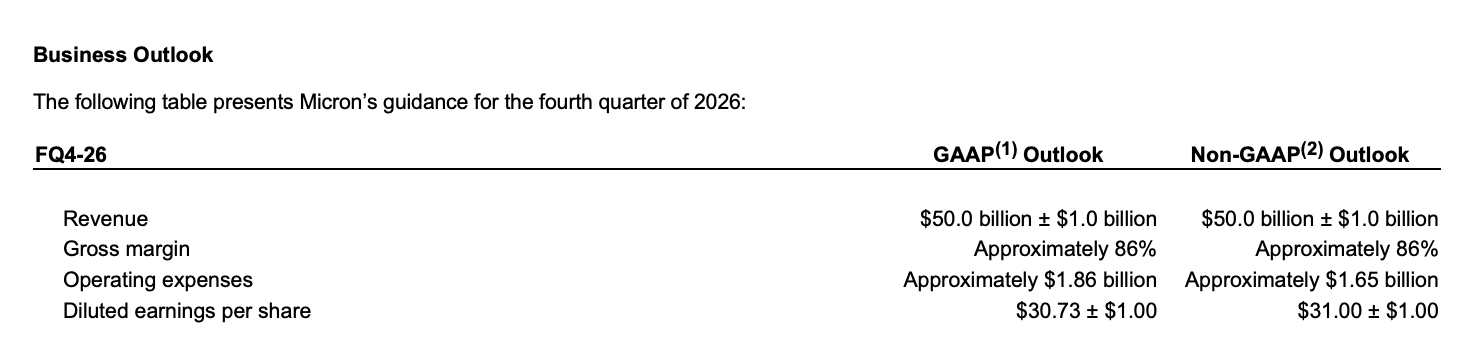

Even more striking was the next quarter's guidance. Micron expects Q4 revenue to reach approximately $50 billion (with a $1 billion buffer), far exceeding the market's prior expectation of around $42.9 billion and even surpassing Goldman Sachs's aggressive forecast of $48.8 billion (widely considered the most optimistic scenario). Q4 gross margin is projected to be around 86%, with earnings per share expected to be roughly $31.

This is why many investors exclaimed the same thing immediately after the earnings release: Now that's what you call a super, ridiculously explosive, parabolic, moon-shot earnings report!

From HBM to SSD, the Entire Memory Stack is on Fire

If we were to pinpoint a core driver for this growth, the answer remains AI. However, compared to the HBM-centric discussions of the past year, a more noteworthy aspect of this earnings report is that the impact of AI is now spreading across the entire memory supply chain.

From a business structure perspective, nearly all of Micron's core business segments are growing simultaneously. Specifically:

- Cloud memory business revenue reached $13.77 billion, up over 300% year-over-year;

- Core data center business revenue hit $11.52 billion, up over 600% year-over-year;

- Data center SSD revenue exceeded $5 billion;

- Mobile and client business grew over 250% year-over-year;

- Automotive and embedded business also achieved over 300% growth;

- Gross margins across business lines generally remained around 80% or higher.

This indicates that the current AI wave is no longer just boosting a single product line but is benefiting the entire memory supply chain comprehensively.

On one hand, HBM remains the most direct beneficiary. Micron stated that HBM4 has already begun volume shipments to lead customers, with samples sent to multiple end customers. HBM4E development is on track and expected to enter mass production in 2027. Concurrently, the company reiterated that its entire 2026 HBM capacity is already sold out.

On the other hand, the continuous expansion of AI training and inference demand is simultaneously driving growth in demand for high-end DRAM, enterprise SSDs, and NAND products. As more advanced capacity is preferentially allocated to HBM, supply in the traditional DRAM and NAND markets tightens further, pushing the entire memory market into its strongest pricing cycle in recent years.

This is why Micron remains extremely optimistic about the industry's outlook. Management expects that the supply-demand tightness in the DRAM and NAND markets will persist beyond 2027. In other words, in Micron's view, the current industry is not approaching the peak of the cycle but rather represents an early stage within the AI infrastructure buildout cycle.

Long-Term Agreements Already Locked In Through 2030

Simply interpreting this earnings report as a victory for HBM might still underestimate its true significance. Because more than the $50 billion revenue guidance, the most noteworthy set of numbers in this report is actually another one: $100 billion.

During the earnings call, Micron disclosed that it has signed 16 long-term Strategic Customer Agreements (SCAs) covering data center, consumer electronics, and automotive clients. Most of these agreements have terms spanning up to 5 years, with some automotive client agreements having 3-year terms, and coverage extending as far as the end of 2030.

These agreements already cover approximately 20% of total DRAM shipments and about one-third of NAND shipments. As more agreements are finalized, it is expected that over half of future revenue could come under long-term contract frameworks.

It is crucial to emphasize that these are not traditional supply agreements. Management confirmed that the relevant agreements adopt a strongly binding Take-or-Pay model. Even if customers do not fully take delivery in the future, they are still obligated to fulfill the established procurement commitments. Some top-tier agreements even include price floor and ceiling mechanisms. The price ceiling is anchored to market prices in Q2 FY2026. However, even if executed at the floor price, the corresponding gross margin level remains significantly higher than Micron's historical cyclical peaks.

Based on data disclosed by Micron's management, 14 current agreements correspond to a guaranteed minimum revenue of approximately $100 billion. Additionally, customers will provide total performance bonds of around $22 billion, with about $18 billion in cash form that can be directly used to support future capacity expansion and R&D investment.

For the memory industry, this is almost a historic change. For decades, the industry's operating logic was always "expand capacity first, then wait for demand to absorb it." Now, Micron is gradually shifting to a different model: lock in orders first, then expand capacity.

This is also what excites the capital market the most. Because it means Micron's current profitability is no longer merely based on expectations of a cyclical upturn but is backed by long-term contracts.

Expand, Expand, and Expand Again: $10 Billion in Q4 CapEx

If the long-term agreements answer "where does the demand come from," then capital expenditure answers another question: how Micron plans to meet this demand.

The earnings report shows that Micron expects fourth-fiscal-quarter capital expenditure to reach approximately $10 billion (higher than Wall Street's prior expectation of around $8.9 billion). It projects full-year FY2026 capital expenditure of about $27 billion, with quarterly capEx in FY2027 expected to be higher than the Q4 FY2026 level. The new investments will primarily be used for HBM, advanced DRAM, and advanced packaging capacity expansion.

In the past, such capital expenditure figures might have triggered market concerns. After all, "large-scale capacity expansion" is not an unfamiliar term for the memory industry. Historically, Samsung, SK Hynix, and Micron itself have all increased investment at cyclical highs, ultimately leading to oversupply, price crashes, and ending the previous bull run themselves.

But this time, the situation seems to be changing. The reason is simple: these new capacities are not built on optimistic forecasts of future demand but on already signed long-term orders.

On one side, there is $100 billion in guaranteed minimum revenue, $22 billion in performance bonds, and long-term agreements extending to 2030. On the other side, there is continuously expanding HBM, advanced DRAM, and advanced packaging capacity. Comparing these data points, the current expansion behavior looks more like executing already locked-in orders, rather than a traditional cyclical bet based on demand forecasting.

Micron's Earnings Rekindle the Semiconductor Bull Market

Before Micron released its quarterly earnings, market sentiment around the current massive semiconductor bull run had shown subtle signs of weakening.

Earlier this week, the South Korean semiconductor sector experienced a notable pullback, with leaders like SK Hynix and Samsung Electronics coming under collective pressure. Some investors began to worry whether, after over a year of frantic gains, AI trades had become too crowded.

Micron's answer was quite direct: demand hasn't peaked; rather, the market is still underestimating demand.

From the significantly beat Q3 earnings and the whopping $50 billion Q4 revenue guidance; from sold-out HBM capacity to long-term strategic agreements covering through 2030 – all convey the same signal: AI infrastructure buildout is accelerating, not decelerating.

Following the earnings release, Micron surged 16% in after-hours trading, driving a collective rally among U.S. semiconductor stocks like Intel, ASML, Marvell, and Qualcomm. South Korean and Japanese stock markets also opened higher today, with the South Korean market triggering circuit breakers again as Samsung and Hynix both rebounded strongly. Upon the opening of A-share markets, the semiconductor supply chain also strengthened, with memory and advanced packaging sectors leading the gains.

In a sense, this is no longer just a quarterly report belonging to Micron. It represents another reinforcement of confidence for the entire semiconductor industry. Because the market has confirmed once again that the AI story is far from over, and memory is becoming an increasingly important protagonist within it.