U.S. Stock Market "Chosen One" Latest Rebalancing: 20% Bet on Anthropic, $9 Billion Short Nvidia, Firepower Aimed at Power and Memory

- Core Thesis: The latest portfolio adjustment by Leopold Aschenbrenner, considered the world's most aggressive AI investor, is not a bet on an AI bubble burst but rather emphasizes a rotation signal from "chips first" to "energy, networks, and data center construction first." He is shorting popular chip stocks like Nvidia while heavily investing in deeper assets such as power, memory, data center networking, and Anthropic.

- Key Elements:

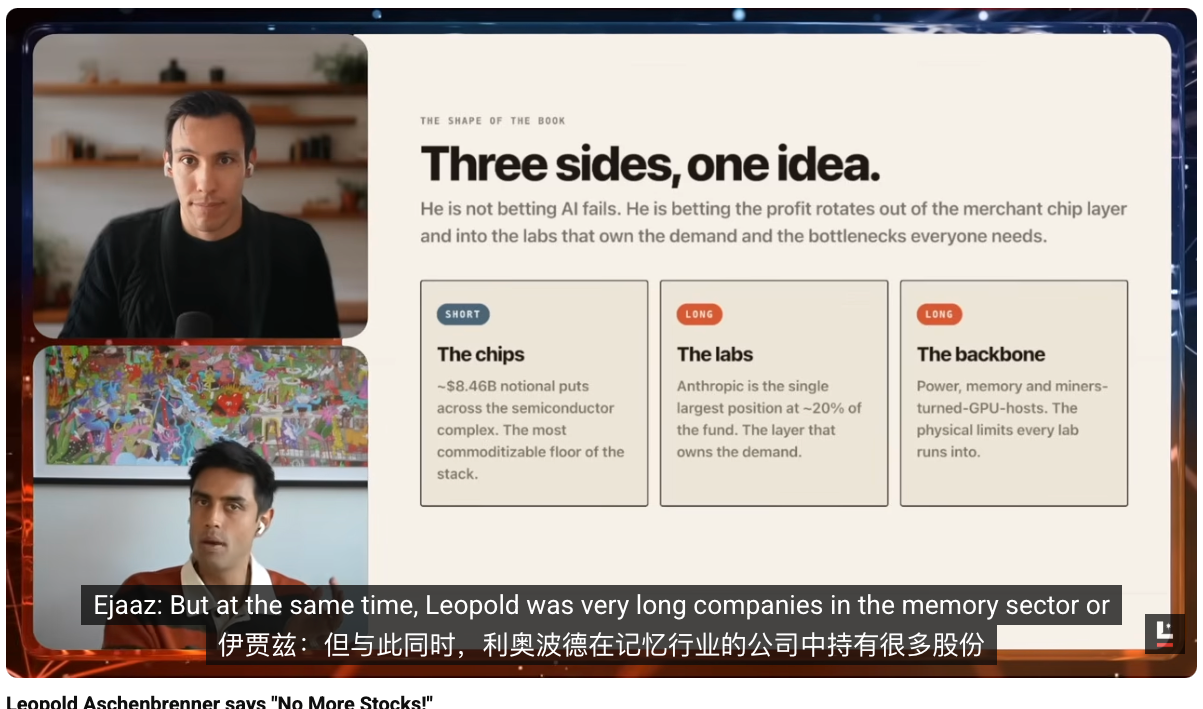

- Leopold is using approximately $9 billion in notional value to short Nvidia, ASML, and Oracle, judging the "picks and shovels" trade in semiconductors as too crowded.

- He is rotating capital towards the next infrastructure bottlenecks: power, memory, and data center networking, while making a substantial bet on Anthropic (around 20% of the portfolio), a direct "mining" asset in the model space.

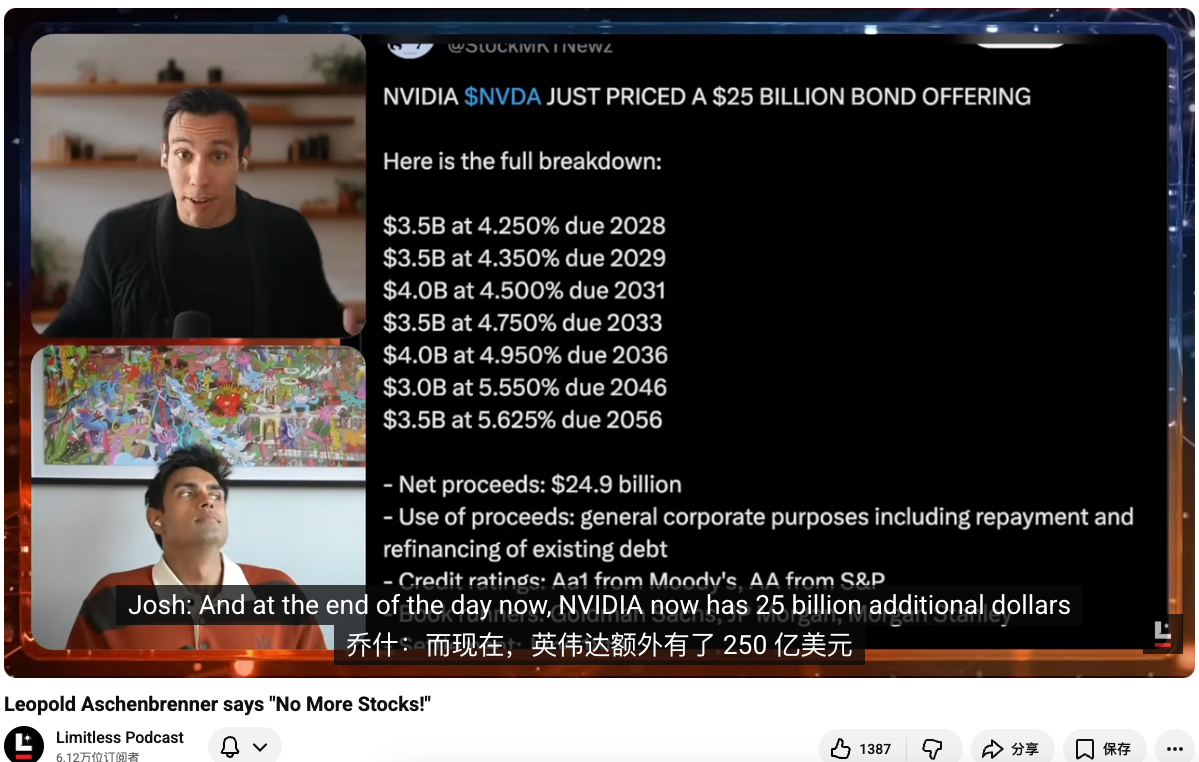

- Nvidia completed a $25 billion bond offering. Despite having ample cash on hand and increasing buybacks and dividends, this is seen as a signal of shifting financing methods in the AI track, not a sign of needing cash, but leveraging cheap capital.

- The true bottleneck has shifted from GPUs to power supply, memory production capacity, the physical ability to build data centers, and regulatory approvals. Whoever can build data centers can make money.

- Optical modules and fiber optics represent the next upgrade direction for data transmission, while copper remains crucial for short-distance, high-bandwidth transmission. The combined demand for both is robust.

- Energy is considered the safest long-term bet because, regardless of whether AI demand slows down, the rigid global demand for electricity will continue to grow.

- Leopold's fund has ballooned from roughly $200 million to around $20 billion within a year and a half through public and private investments, and his strategy has an amplifying effect on market signals.

Compiled & Edited by: Odaily TechFlow

Speakers: Josh Kale, Marketing at Anthropic; Ejaaz Ahamadeen, former Product Manager at Coinbase

Podcast Source: Limitless Podcast

Original Title: Leopold Aschenbrenner says "No More Stocks!"

Release Date: June 17, 2026

Key Takeaways

Leopold Aschenbrenner, considered one of the world's most aggressive AI investors, is shorting NVIDIA, ASML, and Oracle with a notional position of approximately $90 billion in public markets, while simultaneously rotating capital into deeper AI infrastructure and model assets like power, memory, data center networking, and Anthropic. The two hosts believe this doesn't signal the bursting of the AI bubble, but rather a rotation within infrastructure trades from "chips first" to "energy, networks, and data center construction first." This assessment is rapidly gaining market significance, especially after NVIDIA's just-completed $25 billion bond offering and following Anthropic's valuation hike.

Highlights of Key Insights

Leopold's Core Trading Thesis

- "The classic 'picks and shovels' trade in AI has become too crowded. Leopold's recent position changes are signaling exactly that."

- "His judgment isn't that AI infrastructure has peaked. Rather, certain layers within the infrastructure stack, particularly semiconductors and traditional hot targets, have become overly crowded."

- "If the question becomes where capital will rotate next, there are two answers. The first and most direct is that it flows into the next real infrastructure bottlenecks: power, memory, and data center networking. The second answer is the mysterious investment that was only revealed a few weeks ago."

- "His bets have consistently been very infrastructure-oriented, investing in both these optical companies and power-related companies."

- "If he's cautious on NVIDIA, then capital will flow to power, memory, and similar areas. At the same time, he wants to invest directly in the 'mine' itself, not just continue buying 'shovels.' Anthropic is his most favored mine."

Signals from NVIDIA's Financing

- "The issue isn't whether NVIDIA will continue to make money. It's why a company with extremely high profit margins and plenty of cash on hand would need to borrow an additional $25 billion externally."

- "If a company is aggressively buying back stock and massively increasing dividends in the same month while also borrowing money, it's clearly not borrowing because it's short on cash. A more plausible explanation is that this is cheap capital, and there's a subtle shift in how this AI cycle is being financed."

Next Wave of AI Infrastructure Dividends

- "The real bottleneck is no longer just GPUs. It's power, memory, data center networking, and the actual capacity to build these things out."

- "No matter how much money you raise, you can't build data centers fast enough, scale up memory chip production capacity fast enough, or instantly expand the power grid, transmission lines, and related infrastructure. There aren't enough people on the ground, and approvals, regulations, and various processes stand in your way."

- "Whoever has the capability to build data centers will be the one to make the money."

Optical Modules, Copper, and Fiber Optics

- "As GPU clusters scale larger, copper wires generate more heat and energy loss becomes significant, making efficiency very poor. In this scenario, fiber optics becomes the next upgrade direction."

- "For short-distance, high-bandwidth transmission, copper is almost the only material people truly want to use. Only when it becomes unsuitable, such as with long distances or excessive heat, do they switch to fiber optics. So the market currently has very strong combined demand for both copper and fiber."

- "Copper futures have been performing strongly recently. Essentially, it's because everyone needs it. It's the most critical base material for short-distance, high-bandwidth transmission, while fiber optics is the next step."

- Copper remains the most critical material for short-distance, high-bandwidth transmission, but fiber optics becomes necessary once distances lengthen or heat becomes too high.

- "The next capital flows will land on infrastructure companies that don't sound glamorous."

Why Energy is the Safest Bet

- "I've always been bullish on energy because even if AI demand slows down, energy itself remains a global necessity, and this demand will only increase."

- "The single trend that will continuously rise regardless of the scenario is our demand for energy, electricity, and power. These are the companies I'm most willing to hold long-term."

- "What I most want to follow are the companies that Jensen Huang is investing in, which also intersect with Leopold's logic. So the ticker I'm closest to mirroring right now is Marvell."

- "The best long-term positions aren't necessarily the hottest chip companies, but the power infrastructure that is unavoidable regardless of the macro scenario."

Leopold's AI Investment Portfolio

Josh Kale:

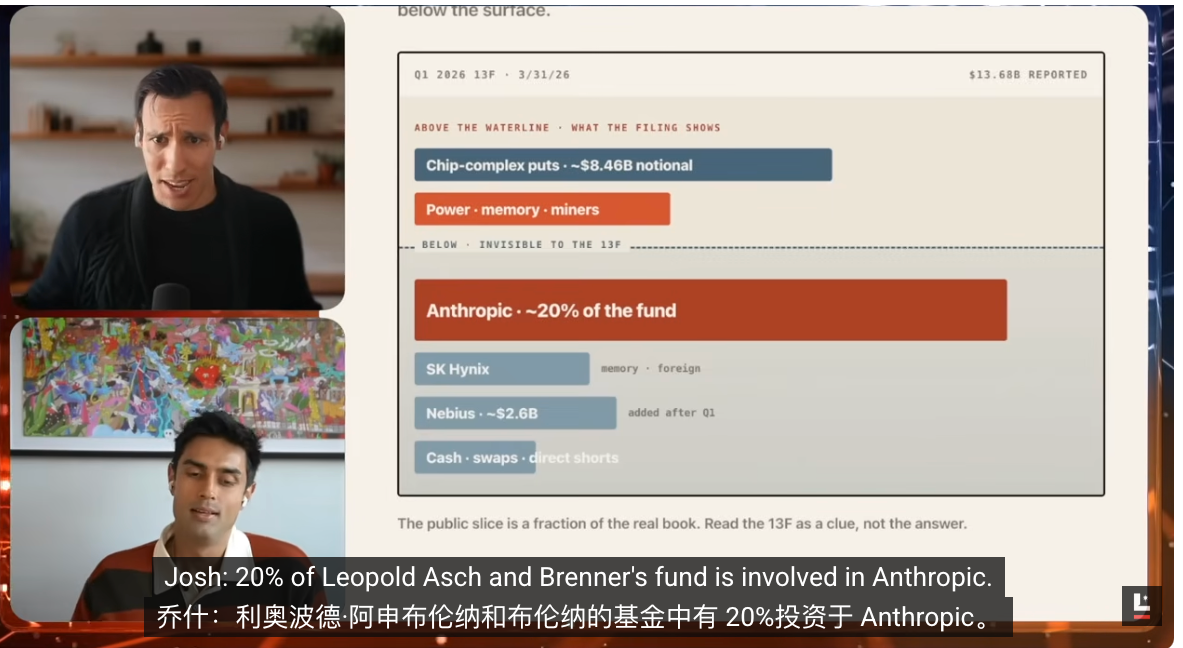

Leopold Aschenbrenner, the 24-year-old focused on AI investing, is now almost regarded by the market as the world's top AI investor. Rumors suggest his fund's notional position size has exceeded $20 billion. When we looked at Ejaaz's post a month ago, the fund size was only $13.7 billion, meaning it's roughly doubling every quarter.

This time, we have several significant new changes in his recent investment moves. In our last episode, we discussed his portfolio, where the most surprising aspect was his short position in a company almost everyone knows: NVIDIA, the world's most valuable company with the highest AI hype. Many couldn't understand why he would establish a short position of over $9 billion against such a company.

Now we have a new clue that might explain this. NVIDIA is actually raising capital, and through debt financing. On the surface, this seems illogical. A company of NVIDIA's massive scale and extremely high profit margins, why would it need to take on an additional $25 billion in cash from a just-completed offering? Today, we want to combine this with Leopold's portfolio, discuss why he's making so much money, what he's looking at next, and what this NVIDIA financing actually means.

Ejaaz Ahamadeen:

Let me give some background. Leopold Aschenbrenner was previously a researcher at OpenAI. About a year and a half to two years ago, he raised a fund. Initially, the size was small, I believe around $200 million. But based on his most recent 13F filing, the fund's public holdings are already valued at $13.7 billion.

So naturally, the market is very curious about exactly what positions he holds, his core investment thesis, and where his next big trade will be. To understand this, you first need to know that about a month ago, Leopold was very optimistic about the entire AI sector, particularly favoring the "picks and shovels" logic, i.e., GPU and upstream hardware suppliers like NVIDIA.

But about a month ago, the market discovered he wasn't so bullish on the semiconductor line. He remains bullish on the real bottleneck sectors like memory and power, and possibly new types of cloud providers, but he is specifically bearish on the world's most valuable company, NVIDIA. More specifically, he had built a roughly $9 billion bearish position against NVIDIA, ASML, Oracle, and several other companies seen as core beneficiaries of AI infrastructure.

The Logic Behind Shorting NVIDIA

Ejaaz Ahamadeen:

When this news came out, many people started worrying, thinking the AI bubble might be about to burst. On the surface, NVIDIA is still selling GPUs like crazy, and demand hasn't shown significant weakness. So where is the problem?

Later, we dug up a few more new clues. The most important one is that NVIDIA just raised $25 billion externally through a bond offering. This means it's not just using its own cash on hand; it's adding leverage. So the question becomes: Why does the world's most profitable company with the highest margins and strongest cash flow need to borrow $25 billion from outside?

Josh Kale:

And initially, they planned to raise only $20 billion, but ended up expanding it to $25 billion, with subscriptions exceeding 3x. In our last episode discussing this portfolio, we said not to worry about a bubble yet because, despite enormous capital expenditures, these companies had high enough revenues to support expansion theoretically from their own balance sheets.

But this is NVIDIA's first significant move to raise capital off-balance-sheet since 2021, instead of just using its own cash. I recall it has about $12+ billion in cash on its books currently. Putting all this together creates a strange tension: Leopold is shorting, while NVIDIA, seemingly with infinite cash and profits, is issuing debt. So what's happening?

Deconstructing NVIDIA's Bond Financing

Josh Kale: Ejaaz, can you break down this deal itself? Because this isn't ordinary financing; it's a bond issuance. Essentially, NVIDIA now has another $25 billion on its balance sheet, and the interest rate seems very low.

Ejaaz Ahamadeen:

I'll lay out both interpretations. NVIDIA originally had about $13.7 billion in cash on its books, meaning it could easily spend its own money. So why raise capital externally? The simplest analogy is buying a house. Many people, even if they have enough cash, still choose a mortgage because their own capital can be deployed elsewhere, and if borrowing costs are low enough, it's actually more advantageous.

The interest rate environment hasn't been favorable in recent years, but if you're NVIDIA, one of the world's most valuable and sought-after companies, you can borrow on very favorable terms. This $25 billion bond offering, with maturities ranging from 2 to 30 years, is practically very cheap money, with rates close to US Treasury yields.

Moreover, this financing was likely oversubscribed by about 4 times. In other words, there were $85 billion in funds trying to get into this $25 billion allocation, giving NVIDIA almost its pick of investors. If you look at the official statement, NVIDIA's explanation is mainly financial management, to repay and refinance some existing debt. Google did something very similar a few weeks ago and also in February this year. So you can accept this explanation as financial optimization.

But the other side is hard to ignore: Over the past month and a half, NVIDIA, Amazon, Google, and several other hyperscale cloud providers have all been increasing external financing. Some issue debt, others sell stock. Perhaps Leopold's view isn't entirely without merit. Could this be a sign that the bubble is starting to loosen, that the house of cards is shaking? However, if you look purely at the financial structure, it doesn't yet point clearly to danger.

Josh Kale:

That's how I see it too. $9 billion shorting NVIDIA is a very large position. But in our research, we saw another thing: on May 18th, NVIDIA's board authorized an additional $80 billion in buybacks and increased the dividend from $0.01 per share to $0.25 per share, a 25x increase.

If a company is aggressively buying back stock and massively boosting dividends in the same month it's borrowing money, it's clearly not borrowing because it's short on cash. The more reasonable explanation is cheap capital and a minor shift in how this AI cycle is being financed. Everyone wants to participate in these capital activities. NVIDIA also realizes that issuing debt is even cheaper than other financing methods, so it just went ahead and did it. At least for now, NVIDIA itself is still doing very well.

Why He Rebalanced

Josh Kale: This brings us back to another question. What is Leopold thinking? Why did his judgment change? The stock price chart you just showed also indicates NVIDIA hasn't been particularly strong recently, but it hasn't been terrible either. It's still the world's largest company near a $5 trillion market cap, down just 7% in a month. That's nothing compared to the surge in other AI stocks.

Ejaaz Ahamadeen:

I don't think NVIDIA is going away. I believe its GPUs, including the newly launched CPU product line from a few weeks ago, will perform very well. Demand for AI products is currently exponentially excessive, and the primary supplier of the core machines to meet this demand is still NVIDIA.

But I do think the classic 'picks and shovels' trade in AI has become too crowded, and Leopold's recent position changes signal exactly that. Looking at his latest 13F, his bearish positions are clearly tilted towards the semiconductor line, including NVIDIA, ASML, Oracle, and a few other infrastructure-level companies.

Yet, at the same time, he's heavily invested in memory, power, and new types of cloud. This shows his judgment isn't that AI infrastructure has peaked, but that certain layers within the infrastructure stack, particularly semiconductors and the traditional hot targets, have become overly crowded.

If the question becomes where capital will rotate next, there are two answers. The first and most direct is that it flows into the next real infrastructure bottlenecks: power, memory, and data center networking. The second answer is the mysterious investment that was only revealed a few weeks ago.

The Unexpectedly Exposed Anthropic Position

Josh Kale:

This surprised me the most. I only learned about it from you yesterday. My first reaction was disbelief. Could Leopold's fund, 'Situational Awareness,' actually have 20% allocated to Anthropic equity? Rumors now suggest this company accounts for about one-fifth of Leopold's fund. The Wall Street Journal and several other outlets have reported this, and sources very close to the deal have confirmed it.

This becomes a completely unexpected card in his portfolio. 13F filings only disclose public market holdings, not private equity. Anthropic happens to be a large piece of unlisted equity. This is why people are beginning to understand why the market values his portfolio at $20 billion.