"We Are Not TradeXYZ": The Harsh Truth Behind the Closure of the First HIP-3 Platform

- Key Point: Hyperliquid's HIP-3 mechanism allows anyone to deploy an on-chain perpetual market, but within this ecosystem, the Matthew Effect is highly pronounced. The first entrant, TradeXYZ, leveraged its first-mover advantage, USDC pricing, number of trading pairs, and airdrop expectations to monopolize over 95% of the trading volume. This forced other participants, like Felix, to shut down due to high costs and razor-thin margins.

- Key Elements:

- HIP-3 requires staking approximately 500,000 HYPE tokens (worth about $30 million) as a deposit, and Tickers must be won through auctions (costing roughly $30,000 per pair), creating an extremely high barrier to entry.

- Growth Mode significantly reduces trading fees, limiting deployers to earning only about 10% of the total fee revenue. The resulting monthly income is hardly enough to cover the $60,000 opportunity cost of staking.

- TradeXYZ commands 95.85% of the trading volume and 96.81% of open interest. Its single trading pair, XYZ100/USDC, contributes a weekly trading volume of $4.53 billion.

- Felix's choice of USDH as the quote asset led to liquidity fragmentation. Users needed to exchange currencies, and market makers were reluctant to participate. Subsequent policy changes by Hyperliquid eroded its competitive advantage.

- Among non-TradeXYZ players, only dreamcash manages to be marginally profitable, thanks to approximately $867,000 in monthly incentives provided by Tether. The monthly income for all other platforms is below $5,000.

The opening price of a new IPO company on the US stock market, coupled with the movement of eager capital continuing to trade after the weekend close, led to an epic price discovery on Hyperliquid. HYPE, reaching a new all-time high, brought this 7x24 platform and a team called TradeXYZ to the attention of global traders.

Hyperliquid is a high-performance blockchain designed specifically for derivatives, featuring a fully on-chain order book. HIP-3 is its third improvement proposal: anyone can stake approximately 500,000 HYPE as collateral to launch their own perpetual market on this chain, trading stocks, indices, commodities, and even companies without an IPO. Hyperliquid provides matching, margin, and on-chain settlement, while the deployer defines which trading pairs to list, which oracles to use, and what leverage to offer.

TradeXYZ was the first trading platform deployed under the HIP-3 framework. Through weekend market pricing and pre-IPO contract trading, TradeXYZ attracted Wall Street's attention within less than a year of its launch.

Beyond TradeXYZ, several other HIP-3 trading platforms have been deployed sequentially, attempting to replicate HIP-3's success with their respective advantages.

However, the results have been disappointing.

Recently, Felix, a project within the Hyperliquid ecosystem, announced that its HIP-3 trading platform will begin shutting down on June 19, with all markets being liquidated individually.

Felix was the first HIP-3 trading platform on Hyperliquid to list silver and crude oil trading pairs. The OIL, GOLD, and SILVER trading pairs generated substantial fees and approximately $3 billion in trading volume for it from December last year to January. Now, it has become the first HIP-3 deployer to officially exit.

Why did a once-leading player shut down first?

"We Are Not TradeXYZ"

Felix founder 0xBroze reviewed the reasons for this failed attempt.

First, the choice of quote asset was wrong. An HIP-3 trading platform needs to select a stablecoin for its perpetual contracts. The earliest launched platform, TradeXYZ, chose USDC. At the time, this wasn't a particularly深思熟虑 decision, as Hyperliquid hadn't yet launched its stablecoin bidding process. Felix, launching later, naturally chose USDH because using USDH offered a fee discount.

However, they didn't anticipate that Hyperliquid would later activate Growth Mode, significantly reducing trading fees, leaving USDH with little advantage. Instead, it became a "burden of fragmented liquidity." Users holding USDC had to swap for USDH to use Felix, and market makers were unwilling to provide liquidity for USDH-related markets. In hindsight, 0xBroze sees USDH more as a pawn Hyperliquid used to pressure Circle into sharing revenue.

Secondly, TradeXYZ was the first mover. It launched on the day HIP-3 went live, about a month earlier than Felix. This wasn't just a time gap; the early brand captured user mindshare and had ample time to continuously roll out subsequent markets.

Furthermore, TradeXYZ listed more trading pairs. As the only deployer using USDC, TradeXYZ quickly built a moat with its number of trading pairs. 0xBroze believes this likely involved a balance sheet advantage. TradeXYZ could afford the auction fees for tickers and the costs of liquidity. In contrast, Felix had limited capital and had to be more cautious in selecting which trading pairs to open.

Finally, there was the "airdrop hint." Early users of TradeXYZ speculated that it would issue a token because the team behind TradeXYZ had previously won the auction for the spot ticker UNIT on Hyperliquid. The expectation of an airdrop progressively boosted TradeXYZ's early user count, trading volume, open interest, and liquidity, creating a flywheel effect that Felix could never catch up with.

In summary: We failed because we are not TradeXYZ.

The Matthew Effect

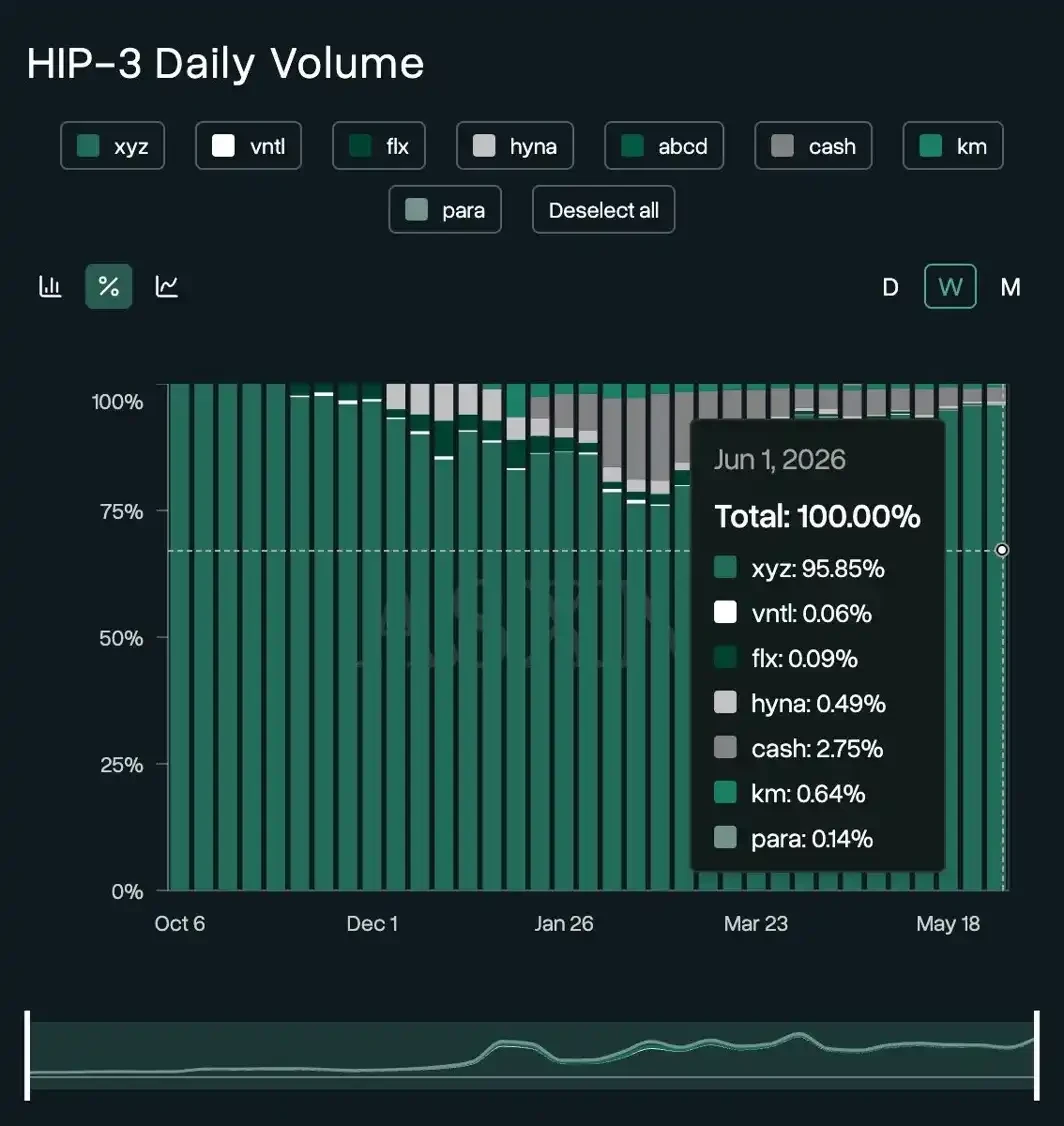

First, look at the trading volume. In the week leading up to early June, TradeXYZ accounted for 95.85% of all HIP-3 trading volume. The remaining seven platforms combined accounted for less than 5%. The second-place, dreamcash, had 2.75%, third-place Kinetiq Markets had 0.64%, and HyENA had 0.49%.

Source: ASXN

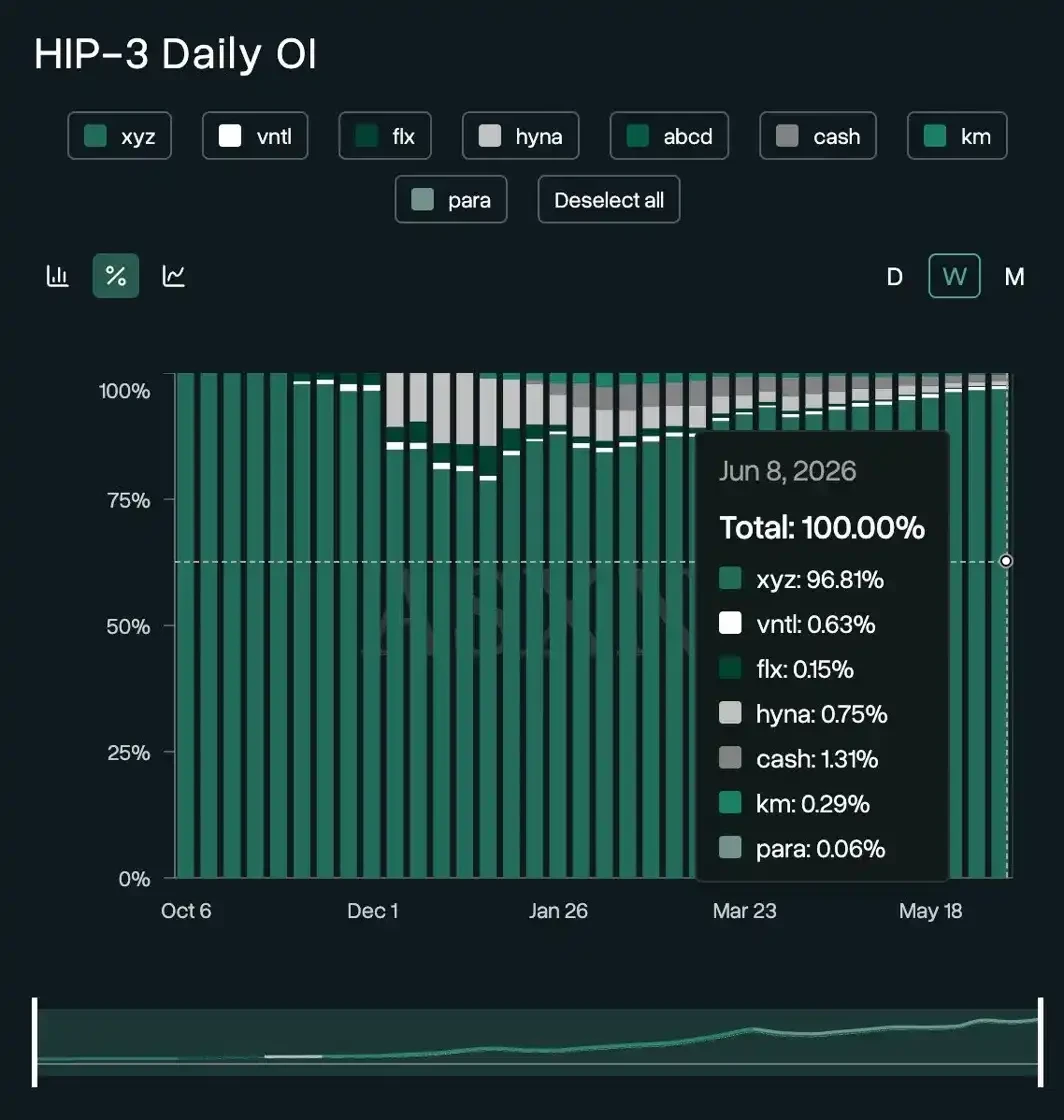

The concentration of open interest is even higher, with TradeXYZ holding 96.81%.

Source: ASXN

This monopolistic structure has been consistent from the start. From the launch of the HIP-3 proposal in October last year to May this year, TradeXYZ's volume share never dropped below 60%.

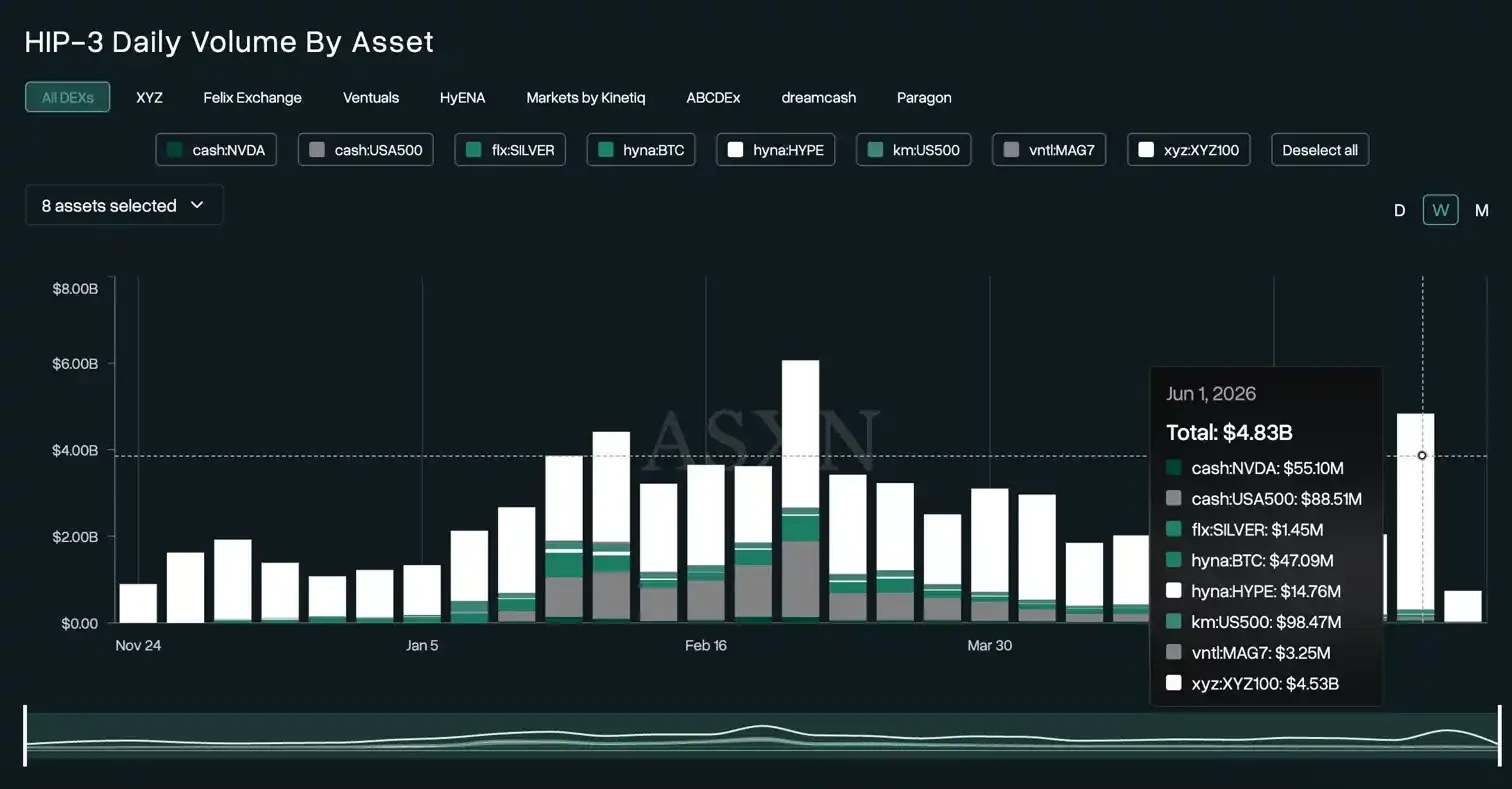

In the first week of June, total HIP-3 trading volume was $4.8 billion, of which TradeXYZ's XYZ100/USDC pair alone contributed $4.53 billion.

Source: ASXN

High Costs, Low Returns

To understand why other deployers struggle so much, one must break down the economics of running an HIP-3 trading platform.

Two costs are clearly defined. Deploying an HIP-3 platform requires staking 500,000 HYPE, approximately $30 million (at a HYPE price of $60).

Source: HypurrScan

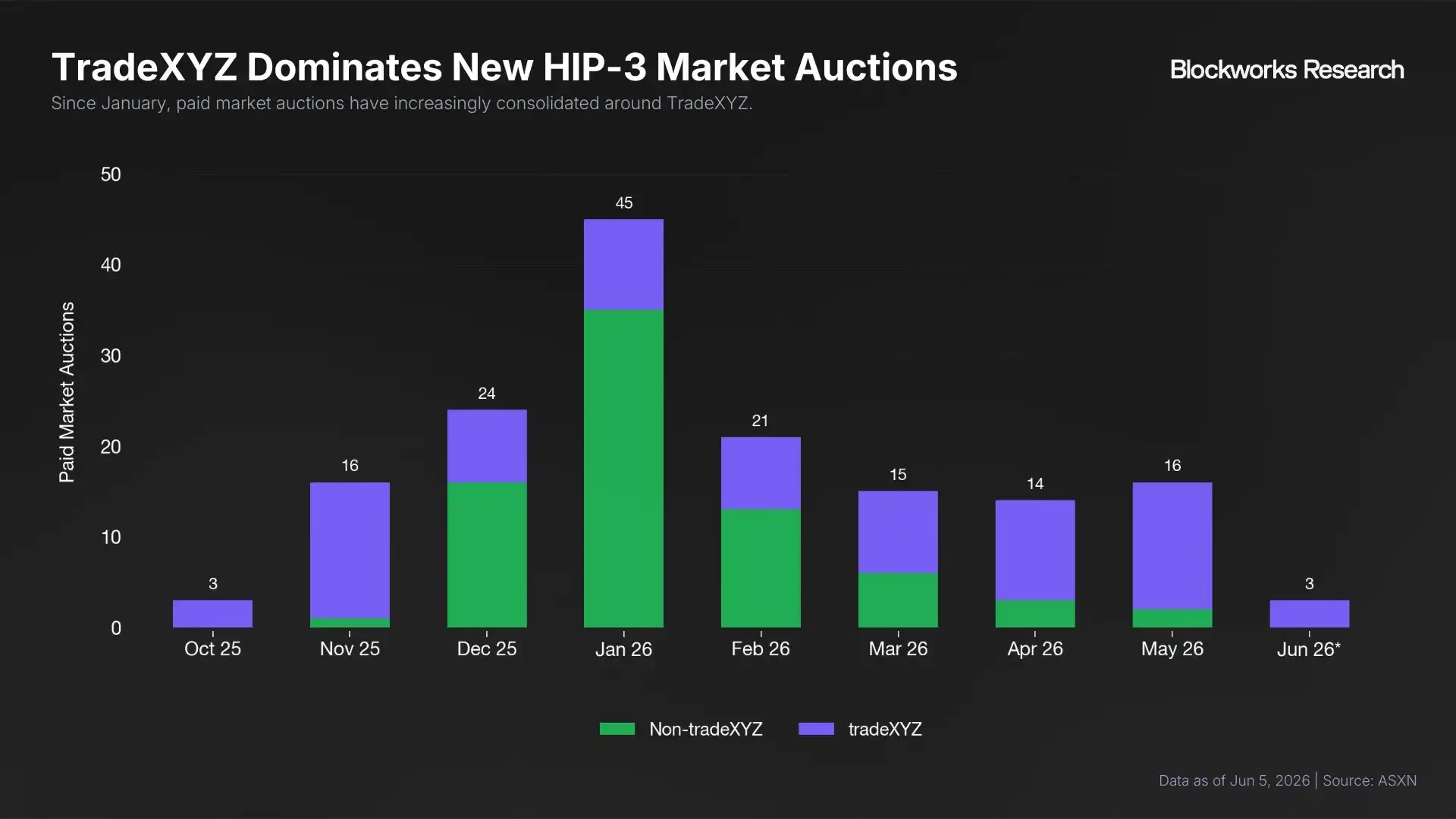

The second cost is the ticker auction. Every time a new trading pair is added, a ticker must be purchased via auction. The average winning bid is around 500 HYPE, roughly $30,000. Currently, this auction market is also dominated by TradeXYZ; since February, enthusiasm from non-TradeXYZ participants in these auctions has been waning.

Source: Blockworks Research

Starting an HIP-3 platform is not only costly but also offers razor-thin margins.

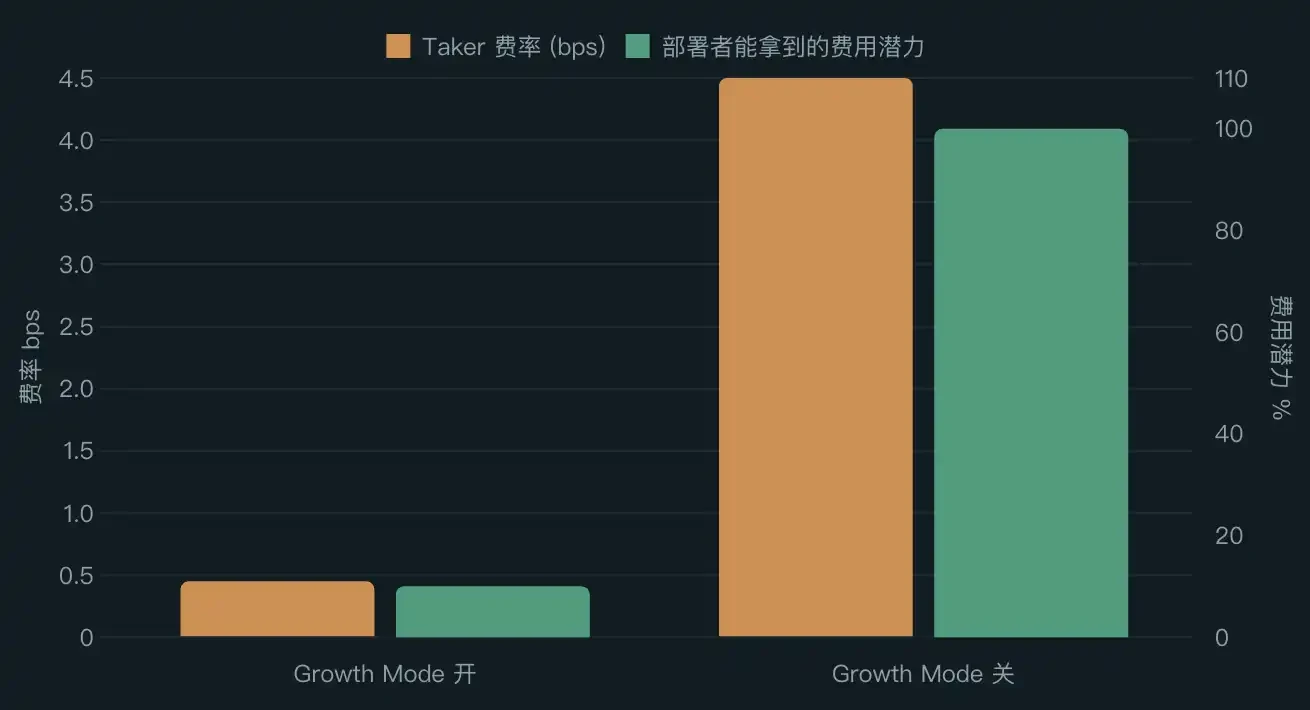

To align the fee rates of its perpetual contracts with traditional brokerages, Hyperliquid introduced Growth Mode. When Growth Mode is activated, the taker fee is slashed to a very low level. Opening an NVDA position here becomes cheaper than on Interactive Brokers. The trade-off is that the deployer receives only about ten percent of the potential fee revenue.

If a deployer chose not to operate a trading platform and simply staked the 500,000 HYPE, at an annual yield of roughly 2.3%, they could earn about $60,000 per month. This means that just to cover the opportunity cost of "doing nothing," a trading platform needs to generate over $60,000 in monthly fee revenue.

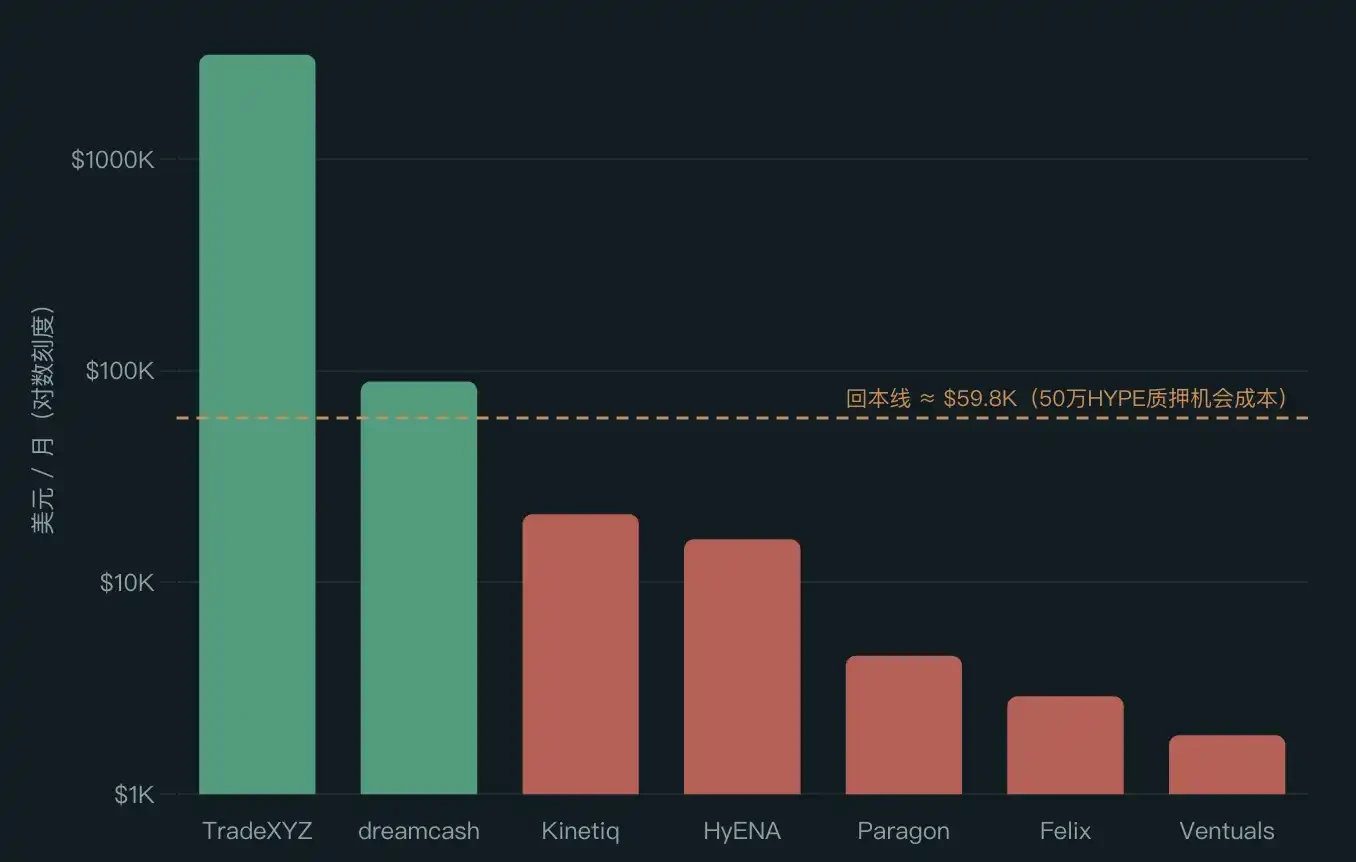

Here is the revenue situation for various platforms in May: TradeXYZ earned approximately $3.1 million, dreamcash around $89,000, Kinetiq about $21,000, and HyENA around $16,000. Platforms further down the list earned less than $5,000.

Excluding TradeXYZ, only dreamcash barely broke even. All other deployers failed to cover even the opportunity cost of staking 500,000 HYPE. This calculation doesn't even include harder-to-quantify expenses like market making, oracles, team salaries, and liquidity incentives.

Source: Blockworks Research

A Spectrum of Strategies

The few platforms still persisting each have their own survival strategy.

dreamcash uses USDT0 as its quote asset, backed by Tether. Tether provides it with approximately $200,000 in trading incentives weekly, translating to about $867,000 per month, far exceeding the platform's fee revenue. Coupled with an expectation of an airdrop, dreamcash holds a solid second place in volume.

Kinetiq Markets boasts a novel "crowdfunding mechanism." Kinetiq developed a platform called Launch. Founder Omnia describes it as a combination of "Shopify + Kickstarter," allowing others to deploy their own customized HIP-3 trading platforms using crowdfunded 500,000 HYPE. The Markets platform itself serves as a template for this model, intended to prove that the Launch concept works, rather than to compete with TradeXYZ for volume.

A Long Road Ahead

Felix certainly won't be the last HIP-3 trading platform to shut down. The room for maneuver left for other players is limited.

Perhaps they could focus on niche or novel markets that TradeXYZ is unwilling to touch. However, Felix has already proven for everyone that the end of this path is "once volume is generated, TradeXYZ copies it and siphons the liquidity."

Another option is to change the distribution channel, building a user base in net-new markets away from the red ocean of native Hyperliquid traders. Kinetiq's Launch is an attempt in this direction, but it hasn't truly succeeded yet.

However, if the cost side doesn't ease, the current dominant-player pattern is likely to persist.

The community has already proposed lowering the 500,000 HYPE staking threshold and setting a lower, floating auction price linked to HYPE's value. From this perspective, a decline in HYPE's price might not be a bad thing, as it could allow more projects to build on Hyperliquid at a lower cost.