Oil Prices Surge, Interest Rates Remain High, and the "Seven Sisters" Stagnate: Which Key Themes Should Drive Excess Returns in US Stocks in Q2?

- Core View: The US stock market in Q2 will exhibit structural characteristics of high volatility and strong divergence. Beta returns at the index level will be limited, with excess returns (Alpha) flowing more concentratedly towards a few sectors that can clearly deliver on their industry logic and earnings visibility.

- Key Factors:

- Macro Constraints: The high oil price and high interest rate environment compress overall valuation expansion space. Market trading logic is shifting from relying on valuation imagination to depending on deliverable metrics such as orders, revenue, and profits.

- Spillover from AI Infrastructure: The market's trading focus is shifting downwards from core hardware like GPUs to more specific industry chain segments such as network interconnectivity (optical communication), storage, power, and data center infrastructure. Attention is on the actual transmission path of capital expenditures.

- Financial and Cyclical Sector Revaluation: The logic is not simply waiting for interest rate cuts, but rather focusing on the profit elasticity and valuation repair opportunities brought by marginal improvements in regulation, adjustments to capital rules, and a recovery in M&A activity.

- Commercialization of Aerospace: The sector's logic is shifting from thematic narratives to defense budget support and the fulfillment of commercial space orders. Stock selection should be based on delivery progress and business models.

- Earnings Visibility Priority: The market's tolerance for "high investment" is decreasing, showing a preference for companies that can provide clear earnings guidance and translate industry trends into their financial statements.

Original Authors: DaiDai, Frank, Maimaiteng MSX Research Institute

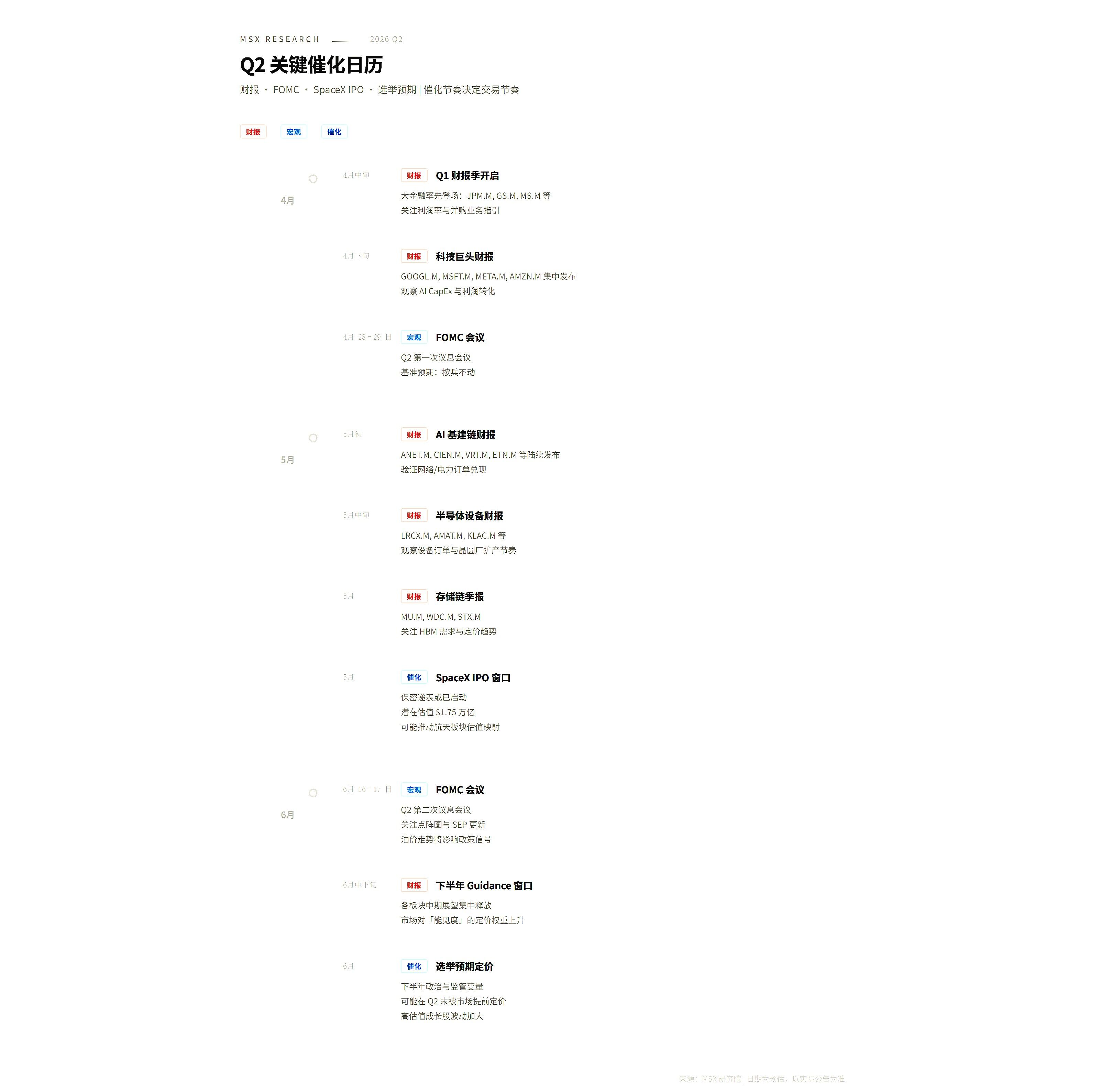

Q1 has just concluded, and the market has delivered a not-so-easy report card.

The "Magnificent Seven" broadly declined, and indices were generally weak. However, if you had positioned yourself in optical communications, AI hardware, and energy/resources, your Q1 returns were actually not bad. Maimaiteng MSX listed 39 targets in Q1, with the four that gained over 100% all concentrated in the two main themes of AI hardware and optical communications (Extended reading: What 2026 US Stock Market Temperature Code is Hidden in a Top Performer's Q1 New Listing Checklist?).

This reflects a very important line of thinking: when the index no longer easily provides Beta, market money will flow more concentratedly towards the few directions that can deliver on industrial logic.

So the question arises: entering Q2, will this "weak index, strong themes" structure continue? Where should the money go?

Based on this, this article provides a systematic outlook on Q2's macro environment, sector themes, and trading logic. The core judgment is just one sentence—Q2 is more like a quarter of high volatility, strong differentiation, and predominantly structural opportunities. Beta returns at the index level are limited, but Alpha has not disappeared; instead, it will be more concentrated, more selective, and more reliant on understanding the evolution of the main themes than in Q1.

I. Macro Backdrop: Oil Price is the Anchor, Interest Rates are the Wall

To understand Q2's market rhythm, one must first see the two ceilings currently pressing down on risk assets: one is oil prices, the other is interest rates.

Over the past period, market expectations for the crude oil price center have clearly risen, with Brent prices once trading into a higher range. Meanwhile, US inflation data continues to show strong stickiness, and the Fed's stance has not truly turned dovish. Under such a combination, the reality the market most needs to accept is that rate cuts may come, but not in a fast or smooth enough manner.

This means Q2 is unlikely to be a quarter that relies on "denominator expansion" to broadly lift valuations. After all, if rates don't come down, long-duration assets are naturally under pressure; if oil prices go up, corporate cost structures and inflation expectations are hard to ease, creating a cycle of high oil prices → sticky inflation → delayed rate cuts → compressed valuation expansion space.

For the market, this almost draws the trading boundaries in advance, making directions that rely on valuation imagination increasingly difficult, while directions that speak with orders, revenue, profits, and cash flow are more likely to gain capital recognition.

However, constraints do not mean no opportunities. What's truly worth noting at the macro level is that the current environment does not treat all industries equally:

- For example, marginal improvements in regulation, revisions to capital rules, and a rebound in M&A activity are more likely to first benefit the financial sector and some pro-cyclical industries;

- While AI infrastructure expansion, military budget releases, and rising energy and resource prices will concentrate opportunities into more specific industry chain segments;

Therefore, Q2 is destined not to be a quarter of "broad-based gains," but more like a quarter where "earnings visibility determines premium, and industrial realization speed determines elasticity."

II. Five Main Themes for Q2: Where Will the Money Flow?

If the current environment is summarized as "high oil prices + high interest rates + indices unlikely to have a trending uptrend," then Q2's excess returns will likely still come from a few clear main themes.

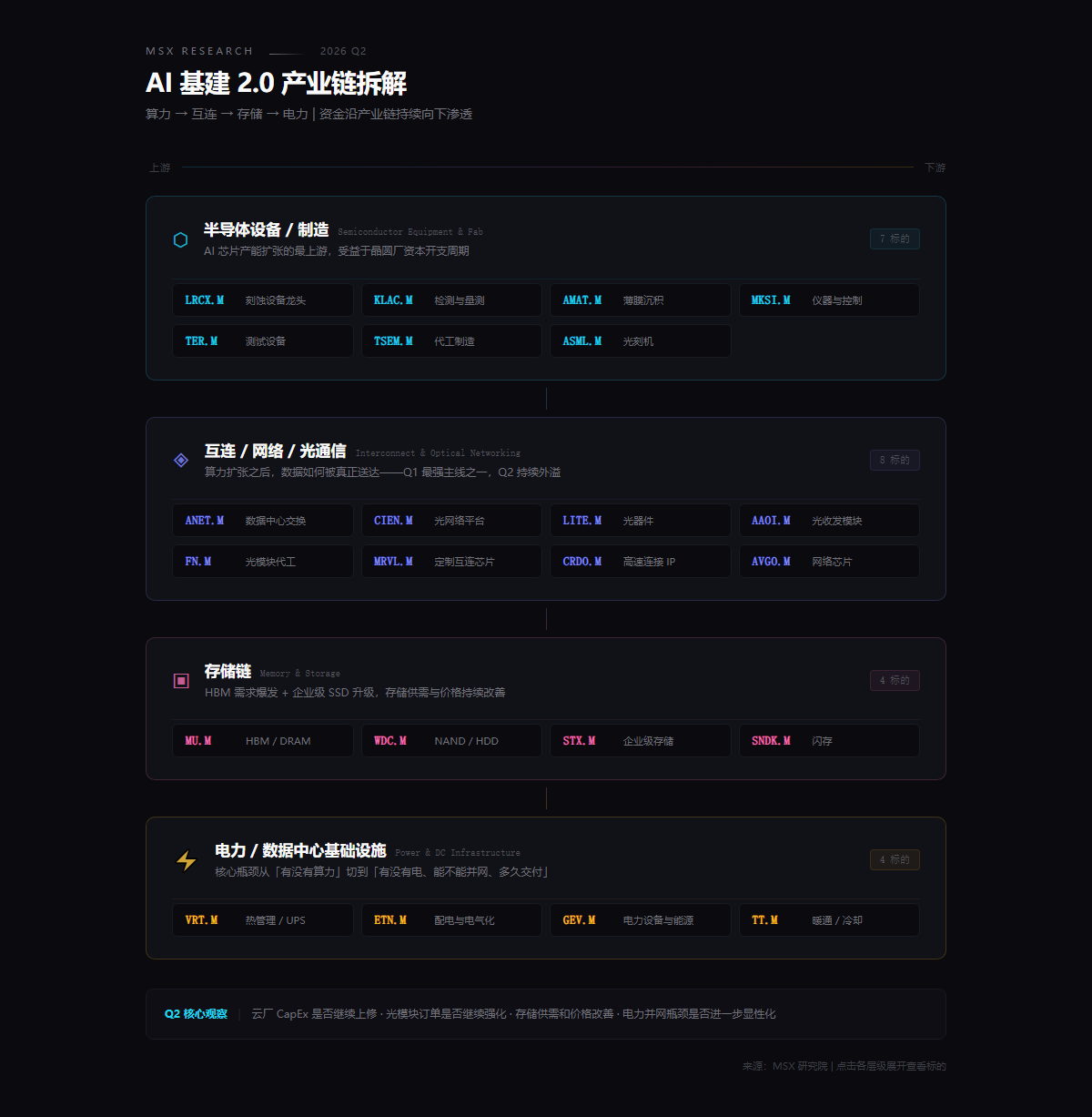

1. AI Infrastructure 2.0: From GPU to Network, Storage, and Power

The AI story is far from over, but the market's trading focus has clearly shifted downwards.

Over the past two years, the market was mostly trading GPU, platform companies, and the large model narrative itself. Entering 2026, capital is starting to ask more realistically: along which paths are the continuously expanding capital expenditures of major tech companies being transmitted downstream? Who is first to convert this money into orders, and who is first to convert orders into revenue and profits?

This is also why Q2's AI theme is closer to a "infrastructure spillover" logic, which can be broken down into four more specific directions.

Including Lam Research (LRCX.M), KLA (KLAC.M), Applied Materials (AMAT.M), etc. The logic of this line has already started to materialize in Q1. In Q2, we need to continue observing whether cloud providers' CapEx is revised upwards and whether equipment orders persist. This represents the most front-end, most hardcore capacity expansion logic.

The second is interconnection, networking, and optical communications, corresponding to the comprehensive amplification of high-density connectivity demands within data centers. This includes Arista Networks (ANET.M), Ciena (CIEN.M), Lumentum (LITE.M), Applied Optoelectronics (AAOI.M), Fabrinet (FN.M), Marvell Technology (MRVL.M), etc. MSX's eight new optical communication listings in Q1 averaged a 64.6% gain, essentially reflecting the explosion in demand for optical interconnects driven by AI data centers. Therefore, this line remains worth focusing on in Q2.

Looking further ahead, the benefits to the storage chain are also becoming clearer. This includes Micron Technology (MU.M), Western Digital (WDC.M), Seagate Technology (STX.M), etc. The core observation point is whether storage supply-demand dynamics and prices can continue to improve.

Finally, there is power and data center infrastructure, including Vertiv (VRT.M), Eaton (ETN.M), GE Vernova (GEV.M), etc. The core bottleneck for data center expansion is shifting from "is there computing power?" to "is there electricity, can it be connected to the grid, and how long will delivery take?" Power and grid connection capabilities are becoming the most realistic constraints for AI infrastructure, making this an incremental variable worth tracking separately in Q2.

In other words, Q2's AI theme is no longer just about simply "buying AI," but is closer to "infrastructure spillover." That is, capital will continue to permeate down the industry chain from computing power → interconnection → storage → power. The market needs to answer a more specific question: whose financial statements is the AI investment ultimately flowing into? The clearer this answer, the easier it is for trading to shift from thematic speculation to systematic opportunities.

2. Finance & Cyclicals: Not Waiting for Rate Cuts, But for Capital Release

Finance and cyclicals deserve a revaluation in Q2, but the logic is not just "waiting for the Fed to turn dovish."

The more noteworthy change is that marginal improvements in regulation, adjustments to capital rules, and a recovery in M&A activity are providing new profit elasticity for some financial stocks. For large investment banks and comprehensive financial institutions, the real positive catalyst may not come from an immediate drop in rates, but more likely from eased capital requirements, restored buyback capacity, a rebound in M&A financing, and an overall re-acceleration of financial activity.

Therefore, for top financial institutions like Goldman Sachs (GS.M), Morgan Stanley (MS.M), and JPMorgan Chase (JPM.M), the focus in Q2 is whether they can translate policy improvements into earnings expectation revisions earlier.

As for industrials and manufacturing, such as Caterpillar (CAT.M), Deere (DE.M), Parker-Hannifin (PH.M), etc., they are better understood within the framework of "high nominal growth + pro-cyclical revaluation." As long as industrial orders, equipment investment, and capital expenditure expectations can be maintained, capital will still be willing to give them some room for revaluation.

Therefore, the core of this line is not about who is cheapest, but about who first demonstrates the complete chain of marginal policy improvement → improved earnings visibility → valuation repair.

3. Aerospace & Defense: From Narrative to Commercial Realization

Aerospace is the most easily underestimated but also most likely to be repeatedly traded theme in Q2.

On one end is the more certain defense budget. For instance, US "Golden Dome" related cost estimates have been revised up to $185 billion. Space and defense capability building is moving from thematic narratives to real budget support. Corresponding targets include defense leaders like Lockheed Martin (LMT.M), Northrop Grumman (NOC.M), RTX (RTX.M), corresponding to the high-certainty defense spending logic; as well as more elastic defense names like Kratos (KTOS.M) and AeroVironment (AVAV.M), which capture the market's revaluation expectations for unmanned systems, low-cost combat capabilities, and new defense needs.

On the other end, commercial space itself is gradually moving out of the long-term narrative stage and entering a screening period of "who can deliver, who can commercialize." Targets like AST SpaceMobile (ASTS.M), Rocket Lab (RKLB.M), and Planet Labs (PL.M) actually correspond to different tracks like satellite communications, launch services, and space data, respectively. The market is increasingly willing to re-rank them based on execution progress, order quality, and business models (Extended reading: With SpaceX IPO Approaching, What MSX's Space Sector Should Really Revalue is Not Just 'SpaceX').

Furthermore, potential capital market actions surrounding SpaceX, even if they remain at the expectation level in the short term, are enough to constitute an important sentiment catalyst for the entire sector. Its real significance is not just bringing attention, but potentially pulling the market back to a question: if commercial space is turning from a dream industry into a cash flow industry, then among the existing listed companies, who is most qualified to enjoy valuation mapping?

This is also why Q2's aerospace theme is likely not a one-time surge, but a direction that will be repeatedly traded alongside event catalysts, budget progress, and earnings validation.

4. The Magnificent Seven & Software: A Repair Window, Not an Undifferentiated Return

The Magnificent Seven remain important in Q2, but they are more like a "style signal" than the "sole main theme."

The value of this group of assets lies not in whether they will once again lead the index in a one-sided rally, but in who can first prove that high capital expenditures are not merely consuming profits but are paving the way for future growth and profitability.

From this perspective, among them, Alphabet (GOOGL.M), Apple (AAPL.M), and NVIDIA (NVDA.M) are relatively stable. Microsoft (MSFT.M), Amazon (AMZN.M), and Meta (META.M) still need more validation regarding profit margins and monetization efficiency. Tesla (TSLA.M) will most likely remain within a framework of high volatility and strong event-driven moves.

The same goes for the software sector. In Q1, many SaaS