NVIDIA Earnings Snapshot: After AI’s Long Rally, Is Compute Demand Still Delivering?

- Key Takeaway: NVIDIA's latest earnings confirm that demand for AI compute power has not yet peaked. Data center revenue and guidance for the next quarter both surpassed expectations, while stable gross margins indicate solid pricing power. The company is transitioning from a high-growth stock into an "AI cash flow platform" with shareholder return characteristics.

- Key Highlights:

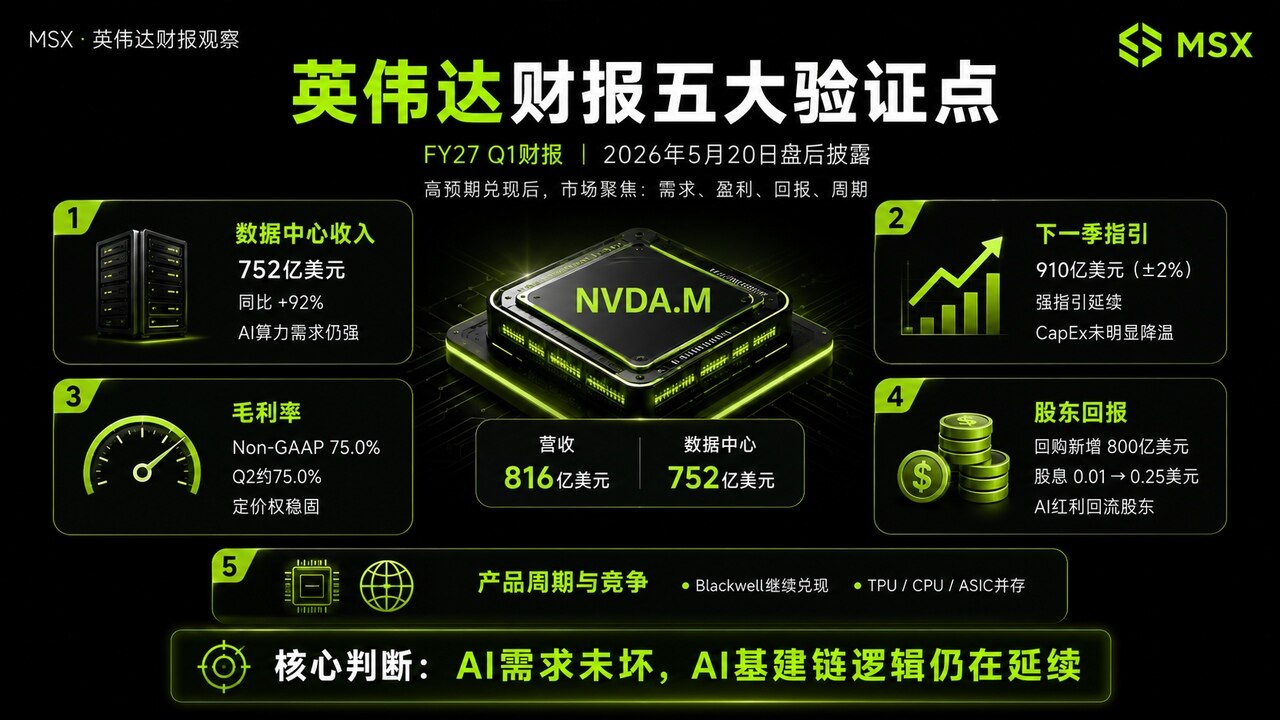

- Revenue of $81.615 billion (+85% YoY), with data center revenue reaching $75.2 billion (+92% YoY, accounting for 92%+ of total revenue). Networking revenue hit a record high of $14.8 billion (+199% YoY).

- Q1 revenue guidance of $91 billion (exceeding market expectations of $86-87 billion), and this guidance does not include data center revenue from China, indicating that strong overseas demand is underpinning growth.

- GAAP gross margin of 74.9%, Non-GAAP gross margin of 75.0%. The company maintains guidance for gross margins around 75%, showing that profitability remains intact even with higher costs associated with systems like Blackwell.

- Significant increase in shareholder returns: Approximately $20 billion returned to shareholders in Q1, a new $80 billion share repurchase authorization, and a dividend increase from $0.01 per share to $0.25 per share.

- Continued product cycle momentum. The announcement of the Vera Rubin platform (including the Vera CPU, BlueField-4 STX) and a partnership with Google Cloud demonstrates ongoing platform iteration capabilities.

Google and Nvidia, representing the application and underlying infrastructure endpoints of the AI sector respectively, both delivered their quarterly reports this week.

If Google I/O showcased the imaginative potential of AI applications, then Nvidia's earnings report verified whether the computing power demand behind these visions has actually materialized.

After the market closed on May 20th, Eastern Time, Nvidia reported its FY2027 first-quarter financial results. Revenue reached $81.615 billion, an 85% year-over-year increase and a 20% sequential increase; Data center revenue hit $75.2 billion, up 92% year-over-year and 21% sequentially. Nvidia also announced an additional $80 billion in stock repurchase authorization and raised its quarterly cash dividend from $0.01 per share to $0.25 per share.

These figures are already impressive enough, but what the market truly cares about isn't just "whether Nvidia is still growing." The real question, given already high market expectations, is whether it can continue to prove that the AI narrative remains intact, that demand for computing power hasn't peaked, and that Nvidia's pricing power is still secure.

1. Reviewing Revenue, Guidance, and Gross Margin: Is the AI Engine Still Accelerating?

First, it's crucial to clarify that Nvidia's core business is no longer "graphics cards" in the traditional sense, but rather its Data Center segment, which serves as the computing infrastructure behind AI factories.

In this quarter, Nvidia's Data Center revenue reached $75.2 billion, accounting for over 92% of total revenue. Breaking it down using the old business classification, Data Center compute revenue was $60.4 billion, a 77% year-over-year increase; Data Center networking revenue hit a record $14.8 billion, surging 199% year-over-year.

This highlights a key point: AI demand isn't just concentrated on individual GPUs; it's expanding towards a complete AI infrastructure ecosystem. GPUs handle the computation, while networking connects the computing power. Entire rack-scale systems, NVLink, InfiniBand, Ethernet, optical communications, power, and cooling all become integral parts of an AI factory.

Therefore, the significance of this Data Center revenue goes beyond "Nvidia selling a lot." It indicates that global cloud providers, AI model companies, enterprise clients, and sovereign AI have not significantly reduced their investment in computing power. From this perspective, if Data Center revenue continues to exceed expectations, the risk appetite for the AI hardware chain is likely to expand further. However, if this metric starts to fall short, it would be a real signal for the market to worry that AI capital expenditure has peaked.

Of course, for a high-expectation stock like Nvidia, the share price reaction post-earnings often depends not only on the quarterly numbers but also, more importantly, on the guidance for the next quarter.

Nvidia guided FY2027 Q2 revenue at $91 billion (plus or minus 2%), significantly higher than the pre-earnings market consensus around $86-87 billion. The company also explicitly stated that this guidance does not assume any Data Center compute revenue from China. This is critical. If China Data Center compute revenue is excluded, and guidance still reaches $91 billion, it suggests that demand from overseas cloud providers, AI factories, enterprise AI, and other regions is sufficient to sustain high growth.

In other words, the market was worried that Nvidia's growth was already so fast that surpassing expectations would become increasingly difficult. This guidance signals that, at least for the next quarter, demand for AI computing power hasn't shown any significant slowdown.

However, it's important to note that as market expectations skyrocket, Nvidia needs to deliver not just a "good earnings report," but one that is "clearly better than expected." Therefore, whether the stock price surges in the short term still depends on whether investors view this guidance as sufficient to justify the high valuation.

Furthermore, Nvidia's high valuation isn't solely due to rapid revenue growth, but also its exceptionally strong profitability.

In this quarter, Nvidia's GAAP gross margin was 74.9%, and Non-GAAP gross margin was 75.0%. The company's guidance for the next quarter remains similar, with GAAP and Non-GAAP gross margins both expected at 74.9% and 75.0%, respectively, plus or minus 50 basis points.

This demonstrates that despite higher costs associated with the Blackwell system, HBM, advanced packaging, and rack-scale solutions, Nvidia can still maintain a gross margin around 75%. For the market, this undoubtedly represents two things:

- Nvidia still possesses significant pricing power. Clients aren't just buying a chip; they are purchasing a complete platform capability.

- While competition in the AI chip space is intensifying, it hasn't materially compressed Nvidia's margins yet. Competition from Google TPU, Amazon Trainium, AMD GPUs, and ASIC custom chips persists, but based on this earnings report, Nvidia's profitability remains largely unchallenged.

Of course, if gross margins were to fall significantly below 74% in the future, the market would begin to worry about product transition costs, customer bargaining power, and pressure from alternatives – a trend that requires long-term monitoring.

2. Is Nvidia Transitioning into an "AI Cash Flow Platform"?

A noteworthy change in this earnings report is the focus on shareholder returns.

In Q1, Nvidia returned approximately $20 billion to shareholders through stock buybacks and cash dividends. By the end of the quarter, the company had $38.5 billion remaining under its existing repurchase authorization. Subsequently, the board approved an additional $80 billion in stock buyback authorization and increased the quarterly dividend from $0.01 per share to $0.25 per share.

The implication goes beyond the company simply having ample cash. More importantly, Nvidia is sending a strong signal to the market that the benefits of the AI dividend are not only flowing to ecosystem partners, AI startups, and the supply chain but are also starting to return to shareholders.

Historically, there were concerns that Nvidia's significant investments in AI ecosystem partners like OpenAI and Anthropic might represent a form of "circular financing." However, simultaneously increasing buybacks and dividends can partially alleviate long-term investors' worries about capital allocation efficiency.

This positions Nvidia less as a pure high-growth AI stock and more as an entity with the characteristics of an "AI cash flow platform."

3. Beyond Blackwell, What is the Market Looking At?

Another key aspect for Nvidia is whether its product cycle can continue.

In this quarter, Nvidia highlighted the Vera Rubin platform, which includes the Vera CPU, BlueField-4 STX, and other products. The company also mentioned its collaboration with Google Cloud, including A5X instances powered by Vera Rubin and a preview of the Google Gemini model on NVIDIA Blackwell and Blackwell Ultra GPUs.

This indicates that Nvidia isn't stopping its story with Blackwell; it is proactively laying the groundwork for its next-generation platform.

For investors, this is crucial. If Blackwell were merely a strong cycle, the market would fear a growth decline after the peak. However, if Vera Rubin can smoothly succeed, it suggests Nvidia isn't dependent on a single product generation's success but possesses a sustained platform iteration capability.

Regarding whether Google TPU and CPU pose a threat to Nvidia, the analysis needs to be two-fold.

In the short term, TPUs, ASICs, and CPUs will indeed take on more tasks in specific scenarios, especially for large tech companies' internal models and inference workloads. However, in the medium term, this looks more like a multi-path approach driven by massive AI demand, rather than an immediate replacement of Nvidia.

Nvidia's true advantage isn't just the GPU itself, but the "platform capability" combining GPU, CPU, networking, software, rack-scale systems, and an ecosystem of partners. As long as clients need to rapidly deploy large-scale AI factories, Nvidia remains at the core of the industrial chain.

Final Thoughts

This earnings report proves at least one thing: the AI narrative is intact.

Data Center revenue hit a new record, next quarter's guidance exceeded expectations, gross margins held firm around 75%, share buybacks and dividends increased significantly, and the product cycle has been extended from Blackwell to Vera Rubin. All these factors demonstrate that Nvidia remains at the core of AI infrastructure expansion.

However, for the stock price, the question isn't "was the earnings report good?" but "was it good enough to surpass already sky-high expectations?" If the market views this report as merely confirming existing expectations, short-term volatility could occur. If investors further upgrade their estimates for AI capital expenditure and Nvidia's long-term revenue potential, risk appetite across the AI chain could continue to broaden.

Furthermore, from an industry chain perspective, a strong Nvidia report doesn't just impact the NVDA stock; it also prompts the market to reassess the entire AI infrastructure chain:

- ASIC / Manufacturing / HBM: AVGO, TSM, MU

- Network Interconnect: ANET, MRVL, CRDO

- Optical Communications: COHR, LITE, AAOI

- Power & Cooling: VRT, ETN, MPWR

Of course, if we reason backwards from the application endpoint, this week's Google I/O proved that AI applications are still proliferating. It's easy to understand why the computing power demand seen in Nvidia's earnings report is being realized – as long as the application side continues generating demand, the AI infrastructure chain is far from its finale.