Gate Research Institute: Will the Weakening US Dollar in 2026 See Stablecoins Absorb Marginal Dollar Demand?

- Core View: Against the backdrop of structural US dollar depreciation and constrained supply from the traditional banking system, stablecoins, as "shadow dollars," are absorbing the spillover dollar demand. Their scale expansion has already made them a significant marginal force influencing short-term US interest rates and is reshaping the circulation and pricing structure of the dollar.

- Key Elements:

- US dollar depreciation is a structural process driven by the combined effects of declining real purchasing power, strengthened fiscal dominance, and changes in real interest rates, not merely a simple weakening of the exchange rate.

- The traditional banking system is contracting its dollar supply due to regulatory and compliance constraints. Stablecoins are absorbing the displaced marginal dollar demand for cross-border payments, transaction settlements, etc., in a lower-friction form.

- As of early 2026, the total market capitalization of stablecoins has exceeded $309 billion, with on-chain transaction volume reaching approximately $33 trillion in 2025, demonstrating their counter-cyclical expansion.

- The market has already established a "safety tiering" for stablecoins. Collateral quality, transparency, and issuer creditworthiness have become the core variables determining their price stability and liquidity.

- Stablecoin reserves are heavily allocated to short-term US Treasuries. Their scale expansion significantly impacts short-term interest rates. Research indicates that a 1 percentage point increase in their market share can depress the yield on 1-month US Treasuries by approximately 14-16 basis points.

- Stablecoins influence short-term funding prices through a bottom-up pathway, forming a closed-loop mechanism from absorbing spillover demand to suppressing short-term interest rates.

- Looking forward, stablecoins are more likely to play the role of a US dollar "reservoir" and distribution layer, rather than challenging the credit of the US dollar itself. Their penetration rate (currently about 1.3% of M2) still has immense room for growth.

Summary:

• The depreciation of the US dollar is the result of a combination of declining real purchasing power, the gradual intensification of fiscal dominance, and long-term changes in real interest rates and holding costs.

• The traditional banking system, constrained by regulation, capital requirements, and risk weighting, creates a spillover demand for dollars, which stablecoins precisely fill within this gap.

• Due to differences in regulation and business positioning, the collateral structures of different stablecoins vary, while an implicit credit hierarchy has formed internally among them.

• The quality of stablecoin collateral, transparency, and issuer credibility are becoming core variables determining their price stability, liquidity priority, and long-term capital preferences.

• After reaching a certain scale, stablecoins have begun to become an important structural force influencing short-term US dollar interest rates.

• Looking ahead to 2026, stablecoins are more likely to play the role of a US dollar "reservoir" and distribution layer. Their reserve assets' stable buying pressure on short-term US Treasuries is, in turn, affecting the US dollar's own pricing structure.

1. Introduction: The US Dollar is Depreciating, But It's Not Exiting

Discussions surrounding the US dollar have become noticeably more complex recently. On one hand, the Fed has gradually shifted towards interest rate cut expectations since 2024, with real interest rates peaking and falling. On the other hand, the national fiscal deficit continues to widen, pressure from Treasury supply remains high, and long-term fiscal sustainability is repeatedly placed under the spotlight. Against this backdrop, narratives such as "dollar weakness," "dilution of dollar credit," and "accelerating de-dollarization" frequently emerge. Market sentiment seems to be forming a certain consensus: the US dollar is standing at a significant structural inflection point.

On the surface, this judgment is not entirely unfounded. Persistent inflation erodes the dollar's real purchasing power, fiscal deficits and debt expansion undermine its certainty as a long-term store of value, and frequent geopolitical friction and financial sanctions prompt some countries and institutions to consciously reduce their direct reliance on the traditional dollar system. Whether viewed from macroeconomic indicators or the political and institutional environment, the dollar appears to be weakening.

However, if we shift our perspective slightly away from the macro narrative and instead observe real capital behavior and usage structures, we discover a non-intuitive yet crucial phenomenon: the dollar is not being abandoned. On the contrary, globally, the US dollar still firmly occupies the core position for pricing, settlement, and safe-haven assets. Particularly noteworthy is that on-chain dollars, represented by stablecoins, have not only not shrunk in recent years but have shown a trend of continuous expansion.

Whether in crypto asset trading, DeFi collateral and liquidation, cross-border transfers, or daily payments in emerging markets, the frequency of dollar usage has not declined alongside discussions of dollar depreciation; it has simply increasingly bypassed the traditional banking system. This constitutes a core contradiction worthy of in-depth discussion: If the dollar is depreciating, why is the world still chasing it? If dollar credit is under pressure, why is dollar usage actually spreading, just in a different form?

This article attempts to start from this contradiction, moving beyond simplistic binary judgments of "strong or weak" or "exit or stay," to re-examine the real flow of dollar demand against the backdrop of dollar depreciation in 2026. It focuses on analyzing how stablecoins, as an extra-systemic form of dollar, absorb the marginal dollar demand squeezed out by traditional financial structures.

1.1 Dollar Depreciation is More Than Just a Concept

When discussing dollar depreciation, the most intuitive understanding is often the dollar weakening against other currencies or a decline in its exchange rate. But in reality, this understanding is too narrow. Dollar depreciation is more like a continuously operating structural process. It doesn't necessarily manifest as an immediate, sharp decline in the dollar's value but rather slowly and persistently changes the real cost of holding dollars through the influence of multiple factors.

The first layer is the decline in real purchasing power. Even if the dollar remains stable nominally, or even appreciates against other currencies in certain phases, as long as inflation persists, the real wealth of dollar holders is constantly eroded. From an economic perspective, nominal price stability is not equivalent to purchasing power stability. For example, the same $1 can buy an apple in one country but a full meal in another.

The second layer is the gradual intensification of fiscal dominance. When a country runs persistent fiscal deficits and government debt scales continuously expand, the independence of monetary policy faces structural constraints. In such an environment, the objectives of monetary policy will increasingly serve debt sustainability. In other words, interest rate cuts become a choice forced to lower financing costs and create operational space for fiscal policy. When monetary policy begins to shoulder the function of supporting fiscal policy, the long-term value anchor of the dollar naturally comes under pressure.

The third layer is the long-term change in real interest rates and holding costs. When nominal interest rates are suppressed and inflation is high, real interest rates tend to be low or even negative. This means holding dollars itself carries an implicit cost, where savers are invisibly subsidizing debtors. At this point, the dollar remains the world's most important currency, but "whether holding dollars is worthwhile" becomes the key question.

1.2 Fed Monetary Policy and Dollar Trends: The Policy Cycle Provides Space for Stablecoin Development

Monetary policy determines the pace and channels through which the aforementioned dollar depreciation mechanisms transmit to the real world. Policy choices at different stages directly impact the dollar's strength, weakness, and usage cost.

• 2008–2014: The QE Era, Passive Dollar Weakness

○ Following the global financial crisis, the Fed launched multiple rounds of quantitative easing, massively expanding its balance sheet and suppressing interest rates to repair the damaged financial system. Dollar supply expanded rapidly during this phase, with real interest rates staying low for an extended period, significantly reducing the dollar's scarcity. At this time, there were more dollars, but they weren't "easily usable"; liquidity mainly remained trapped within the banking system and financial assets.

• 2015–2018: Gradual Rate Hike Cycle, Structural Dollar Strength

○ As the economy recovered first, the Fed began raising rates and shrinking its balance sheet, leading to global capital flowing back into dollar assets and putting pressure on emerging markets. During this stage, the dollar re-established itself as the global monetary anchor. Its availability decreased, usage costs rose, and the dollar's financial attributes were significantly strengthened.

• 2019: Policy Shift Towards Easing, Dollar Peak Begins to Loosen

○ Against the backdrop of a global economic slowdown, the Fed conducted precautionary rate cuts. The dollar index oscillated at high levels, its strength loosening somewhat, but a fundamental turn had not yet occurred.

• 2020–2022: Aggressive Hikes Post-Pandemic Shock, Dollar Enters Super-Strength Cycle

○ During the pandemic, the Fed implemented unlimited QE and zero-interest-rate policies, leading to unprecedentedly loose dollar liquidity. Subsequently, high inflation quickly backfired, forcing the Fed to adopt the fastest rate hike pace in history. During this phase, the dollar index hit a 20-year high, simultaneously undermining confidence in the dollar's long-term value.

• 2023–2025: Rising Rate Cut Expectations, Dollar Enters Structural Decline Phase

○ As inflation receded, the market continuously anticipated a rate cut path starting in 2023. Although the dollar remained at high levels, marginal tightening had ended. Fiscal deficits, debt scales, and the long-term interest rate anchor began to dominate the dollar narrative. It was precisely during this phase that a key change emerged: the dollar was still needed, but dollars within the traditional system became slower, more expensive, and more constrained.

2. Traditional Dollar Deceleration: How Stablecoins Absorb Spillover Demand

As monetary policy adjusts and fiscal constraints intensify, the traditional banking system actively shrinks its dollar balance sheet under regulatory, capital, and risk-weighting constraints. Simultaneously, strict AML, cross-border compliance, and account access thresholds exclude a large number of non-core users and marginal capital from the traditional dollar system, creating structural dollar spillover demand. Stablecoins precisely fill this gap, providing quasi-dollar liquidity with lower friction, becoming an important container for extra-systemic dollar circulation.

2.1 Dollar Depreciation ≠ Decline in Dollar Usage, The Counter-Trend Expansion of On-Chain Dollars

When discussing dollar depreciation, a common intuition is: if the dollar's purchasing power declines and its credit is questioned, its usage scope and demand should contract accordingly. But reality is恰恰相反. Over the past few years, especially after experiencing interest rate hike shocks, bank risk exposures, and volatile risk assets, the on-chain dollar form represented by stablecoins did not shrink with them. Instead, they showed signs of recovery or even expansion across multiple dimensions.

First, in terms of total value, the overall market capitalization of stablecoins gradually stabilized and rebounded after periodic pullbacks. By early 2026, the total stablecoin market cap had surpassed $3.09 trillion, reaching a new historical high. Although market structures changed and shares among different stablecoins adjusted, dollar stablecoins as a whole were not marginalized. This phenomenon itself indicates that the market did not abandon dollar-denominated tools due to concerns about the dollar's long-term prospects.

Second, in terms of usage, stablecoin activity significantly increased. Throughout 2025, the total on-chain transaction volume for stablecoins was approximately $33 trillion, a year-on-year increase of about 70%. During the same period, USDT and USDC dominated all stablecoin transactions, with USDC processing about $18.3 trillion in on-chain transactions and USDT about $13.3 trillion, together accounting for the vast majority of the flow.

Looking at monthly transaction volume, the monthly transfer volume of stablecoins on main chains like Ethereum once reached levels around $8.5 trillion, demonstrating their core role in trading, cross-chain liquidity, and pricing.

In other words, even as risk preferences towards the dollar changed at the macro level, stablecoins in crypto trading did not retreat to the margins. Instead, they continued to play important roles in liquidity and settlement.

2.2 Stablecoins as "Shadow Dollars," Absorbing Demand Squeezed Out by the Banking System

In recent years, friction in cross-border dollar settlements has increased. Dollar transfers within the traditional banking system often involve multiple intermediaries, complex compliance reviews, and high time and capital costs. Against the backdrop of rising geopolitical risks, issues like account freezes, payment channel disruptions, and sanction compliance have also made using the dollar itself no longer neutral.

In such an environment, stablecoins have begun to function like shadow dollars. They do not challenge the dollar's pricing status but, without changing the dollar standard, reduce institutional friction to meet marginal demand. For example, for many cross-border merchants, the core appeal of stablecoins lies not in yield but in accessibility, transferability, and settlement certainty, specifically: not relying on local bank accounts,不受营业时间限制, and near-instantaneous cross-border transfers.

It is worth mentioning that the essence of stablecoins is US dollar liabilities issued by private entities. That is, the value of stablecoins in investors' hands does not directly come from sovereign credit but is built on trust in the issuer's balance sheet. To support this trust, mainstream stablecoin issuers typically allocate a large portion of their assets to short-term US Treasuries and repo assets collateralized by Treasuries.

In 2024, these stablecoins purchased $400 billion in US Treasuries, a scale comparable to the largest local government money market funds and exceeding the purchase volume of most foreign investors.

This structure not only maintains the peg between stablecoins and the US dollar but also allows stablecoins to functionally延续 the dollar's settlement attributes while remaining游离于 the public financial system in terms of credit hierarchy. Because stablecoins can meet the persistent demand for dollars without increasing the burden on the banking system. For issuers, they are off-balance-sheet liabilities; for users, they are a form of dollar that can be held and transferred without a bank account. This is not the disappearance of dollar credit but its migration.

It must be emphasized that stablecoins are not necessarily safer than traditional dollars, nor are they necessarily superior in risk control. They lack central bank lender-of-last-resort support and deposit insurance mechanisms; under confidence shocks, they can still experience volatility or even de-pegging.但从使用角度看, stablecoins are often more convenient—lower access barriers, faster transfer speeds, and fewer usage restrictions.

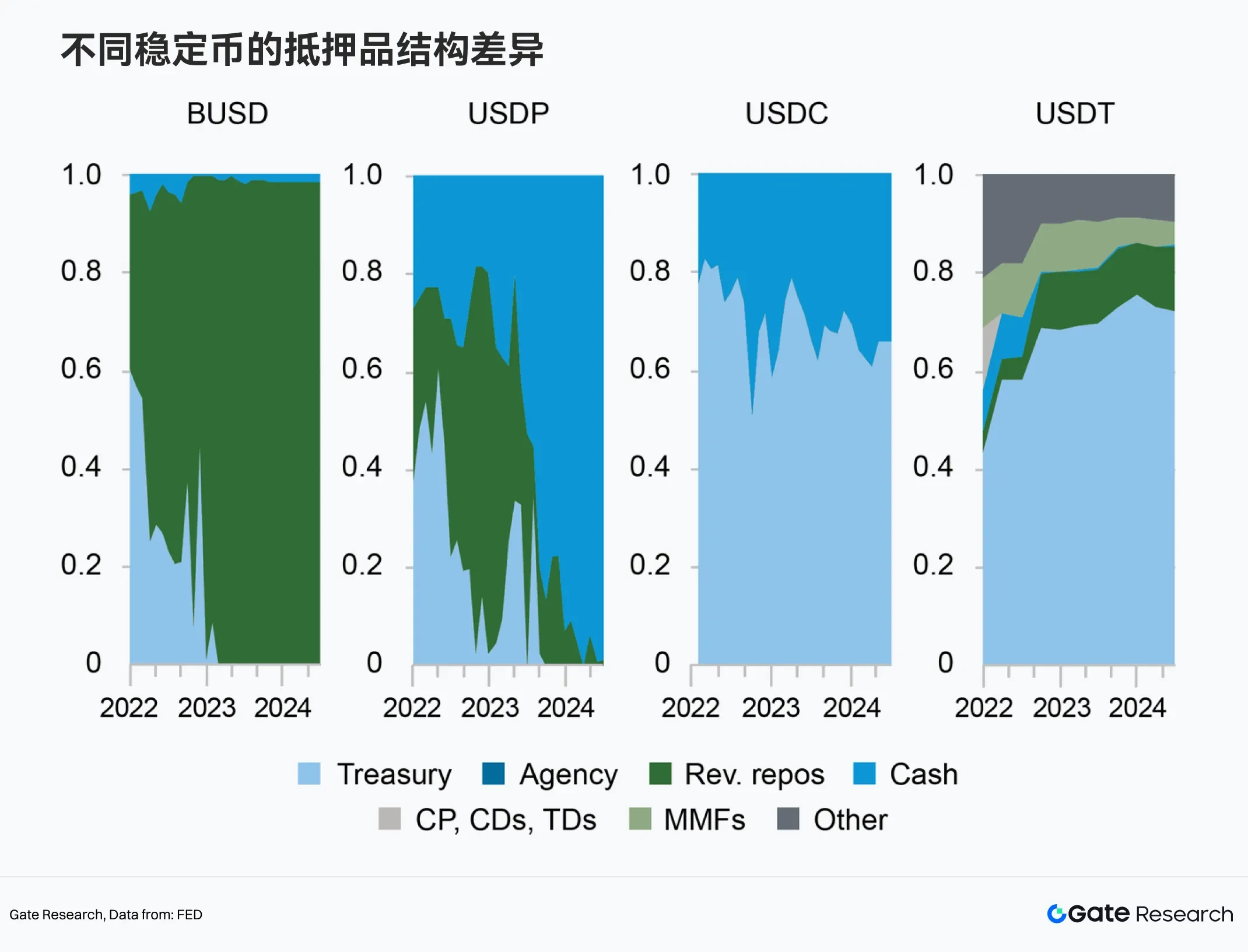

2.2.1 Differences in Collateral Structures Among Stablecoins Due to Regulatory and Business Positioning Variations

On the surface, there are significant differences in the choices of "where assets are placed" among different stablecoins: some are almost entirely composed of cash and short-term Treasuries, while others still include loans, crypto assets, and other non-standard assets. In fact, these differences are the result of the long-term interplay of the regulatory environment, business objectives, and risk preferences of the issuers.

Differences in regulatory constraints are the most核心的分水岭. Stablecoins like USDC, BUSD, and USDP have issuing entities primarily located in heavily regulated jurisdictions. This means issuers have extremely limited freedom in asset allocation,几乎只能选择 the "cleanest," most监管接受的 asset types.

Specifically, cash, reverse repos collateralized by US Treasuries, and ultra-short-term Treasuries have become the main components of these stablecoins' reserves. These assets are not necessarily the highest-yielding, but they are structurally clear, risk-explainable, and highly liquid, making it easier to demonstrate solvency to regulators and the market under any stress scenario.

In contrast, USDT operates in a more offshore regulatory environment. Its historical information disclosure transparency has been lower, and it faces relatively looser direct regulatory constraints. This gives USDT greater leeway in asset allocation. Furthermore, USDT has long played a market-oriented role rather than being a strictly compliant financial product. Therefore, its reserves have historically included commercial paper, loans, and even non-stablecoin crypto assets.

Differences in business positioning further amplify this structural divergence. The core objectives of USDC and USDP are very clear: avoid de-pegging at all costs. To achieve this, they are willing to forgo some yield to prioritize liquidity and transparency. In this model, stablecoins更像是一种被动的货币工具. USDT's goals, however, lean more towards scale, usability, and global coverage. At certain stages, USDT's reserves were not only used to passively support stablecoin redemptions but also for lending, supporting exchange and market maker operations, and even allocating to non-stablecoin crypto assets. This makes USDT functionally closer to a shadow bank with financial intermediary attributes, rather than just a simple payment medium.

2.2.2 Stablecoins Are Not Homogeneous; "Safety Tiers" Are Beginning to Dominate Pricing

In the early stages of the crypto market, stablecoins were更多被视为一种功能性工具—as long as they were pegged to the dollar and priced close to $1, they were默认是等价的. This "homogeneity assumption" was rarely challenged during平稳时期, but past rounds of systemic冲击 have gradually broken this perception.

The Terra event was the first real watershed. The collapse of UST in 2022 was not due to an external financial shock but rather its own structure rapidly failing under a reversal of confidence. This event made the market clearly realize for the first time: even if nominally stable, if缺乏真实资产支撑, a stablecoin is almost inevitably prone to de-pegging or even归零 under pressure. From that moment, "whether it has real, liquidatable dollar asset backing" became the first threshold for distinguishing stablecoin safety.

The FTX collapse, also in 2022, further reinforced the second layer of judgment: having assets alone is not enough; transparency and issuer credit are equally important. Although FTX itself was not a stablecoin issuer, its commingling of funds and lack of transparency quickly evolved into a liquidity crisis, severely impacting market trust in centralized financial intermediaries. This event indirectly changed the risk pricing logic for stablecoins, pointing to the fact that stablecoins are no longer just about "whether there are assets" but about "whether the assets are credible."

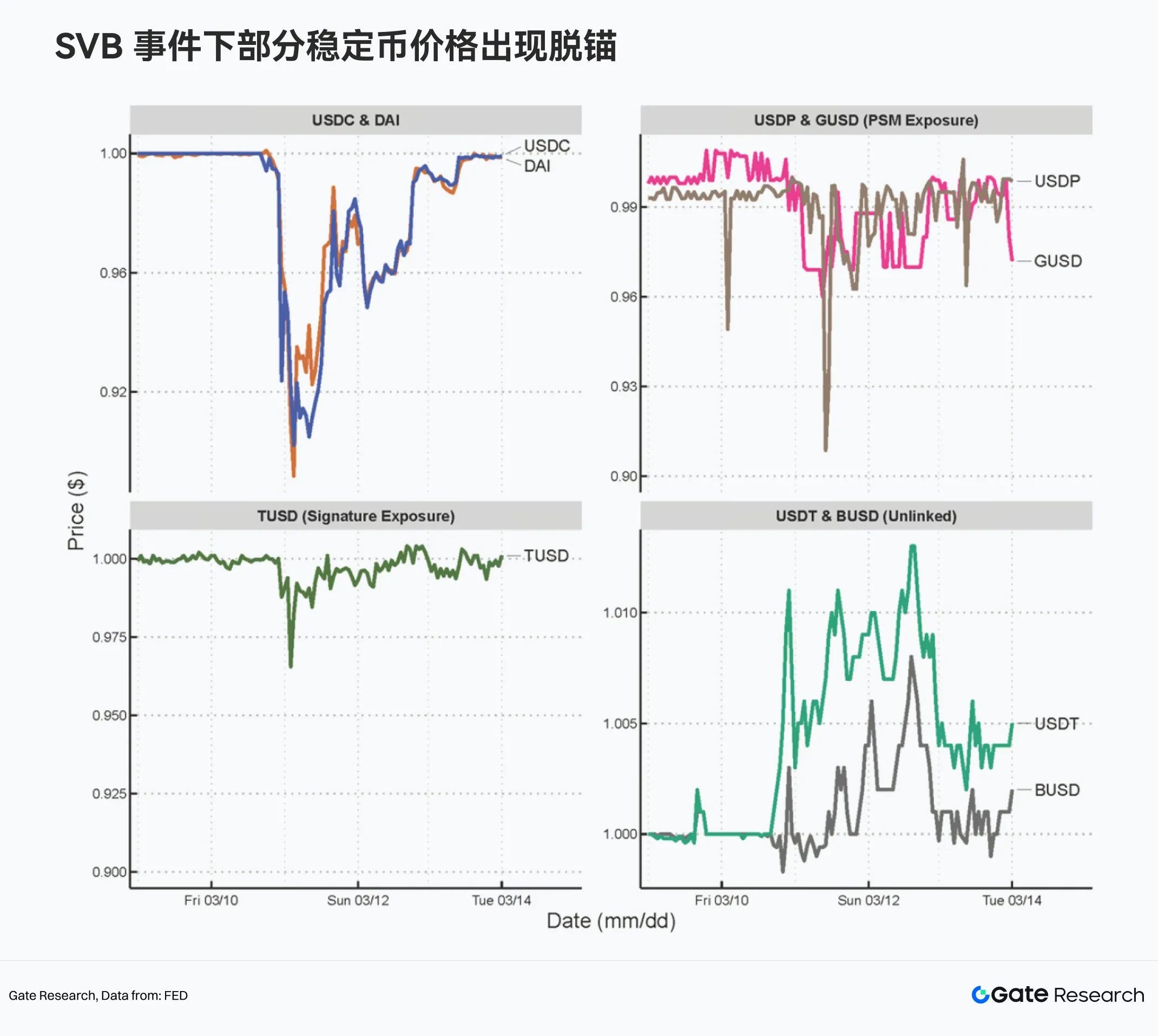

What truly brought safety tiers明确推到台前的 was the Silicon Valley Bank (SVB) incident in 2023. During this shock, USDC briefly lost its peg as part of its reserves were held at SVB, with its secondary market price一度跌至约 $0.86. Meanwhile, USDT, which the market perceived as having no direct risk exposure to the event, showed a premium in some trading scenarios. This contrast was highly symbolic: for the first time, within the same time window, the market clearly differentiated stablecoins into "relatively safe" and "relatively unsafe" dollars, expressing this directly through price.

Simultaneously, this tiering did not only occur in centralized trading markets. In DeFi systems, automated mechanisms反而放大 risk transmission. Taking MakerDAO's Peg Stability Module (PSM) as an example, other stablecoins like DAI maintain a 1:1 exchange with USDC through the PSM. When USDC de-pegged, arbitrage行为迅速抽干 PSM liquidity, causing stablecoins not directly exposed to SVB risk (e.g., DAI, USDP) to also experience price波动. A technical module originally designed as a connector反而成为风险的加速器 under stress scenarios.

This series of events collectively points to one conclusion: the market no longer views stablecoins as a single, homogeneous dollar substitute. Instead, an implicit credit hierarchy has formed internally. Furthermore, collateral quality,