Gate Research Institute: Diverging Paths in Traditional Asset Trading on Exchanges, Gate Builds a Full-Category Orderbook Perpetual System

- Core Viewpoint: Gate Exchange's core advantage in the traditional finance (TradFi) derivatives arena is not the number of assets, but its unique unified orderbook perpetual contract architecture. This positions it as a builder of multi-asset trading infrastructure, rather than a mere product expander.

- Key Elements:

- Gate is the only exchange to achieve full-category orderbook perpetual contract coverage for stocks, metals, indices, forex, and commodities, providing professional users with a transparent, order-placable, API-friendly trading experience.

- Unlike most competitors that use quote-based (CFD) models, Gate integrates TradFi assets into the crypto-native perpetual contract framework, emphasizing public order matching and market-driven price discovery, creating a differentiated moat at the mechanism level.

- This unified orderbook architecture positions the platform as a neutral matching entity, avoiding directional risk, which is more conducive to supporting future expansion into standardized trading scenarios for multiple assets (including RWA).

- In terms of fee structure, Gate employs fixed per-lot fees for assets like metals, offering greater cost certainty and competitiveness in small-to-medium position and high-frequency trading scenarios compared to percentage-based fee models.

- Gate concentrates its investment in marketing and user education, reinforcing the perception of TradFi as a core business module through high-frequency operational activities and systematic content, thereby reducing user understanding and conversion costs.

Summary

• Gate is the only exchange that achieves full-category coverage (stocks, metals, indices, forex, commodities) in perpetual contracts (Orderbook mode). For professional users who prefer order book matching, transparent depth, and API trading, Gate provides the most comprehensive and crypto-native-like TradFi trading experience.

• Most competitors focus on independent TradFi CFD modules, attracting cross-border users with a wide range of underlying assets and low barriers. In contrast, Gate's differentiated advantage lies in integrating traditional assets into a unified order book perpetual framework, treating it as reusable derivative infrastructure, thereby creating a significant mechanism gap with competitors at the order book perpetual level.

• As the industry shifts from product stacking to competition in trading infrastructure, the order book model emphasizes public matching, transparent liquidity structure, and reusable trading paradigms, aligning more closely with the long-term direction of RWA towards standardized trading scenarios. Gate's unified order book architecture covering multiple asset classes provides stronger scalability for future expansion into more complex real-world asset trading forms.

1. Market Product Form Definition

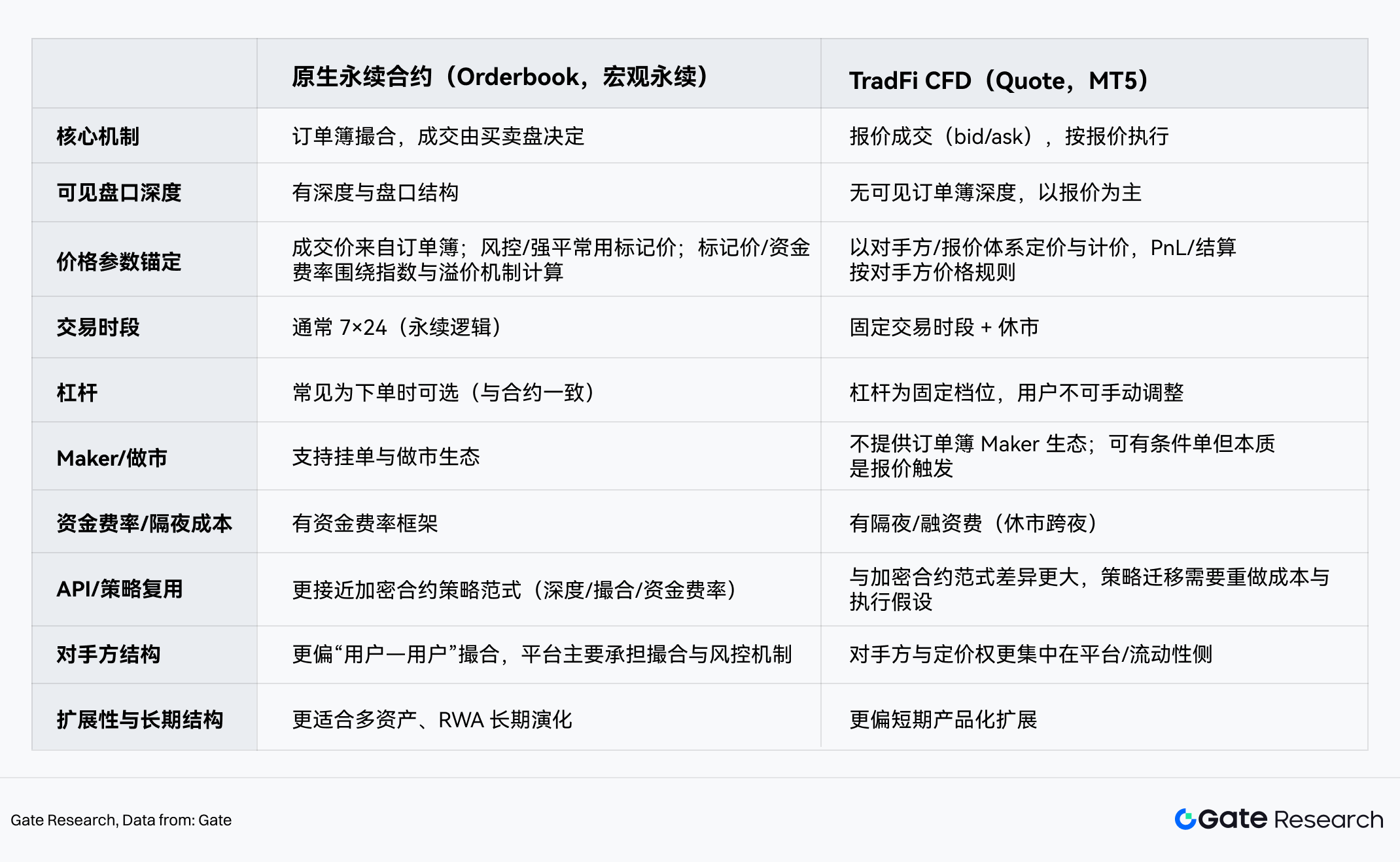

In the TradFi layouts of mainstream crypto exchanges, the key difference between platforms lies not only in how many traditional assets are listed but also in the trading form through which these assets are introduced to the market. Different product forms determine how trades are matched, how key price parameters (e.g., index price/mark price) and risk control mechanisms are anchored, and whether the trading experience and strategies can be reused within the crypto derivatives framework.

Based on differences in trading mechanisms, current CEX TradFi derivatives implementations can be categorized into two mainstream forms:

• One is the native perpetual contract (Orderbook) model, which integrates stocks, indices, forex, or commodities into the order book matching system. Trades are completed by matching buy and sell orders and follow the funding rate framework of crypto perpetual contracts. Meanwhile, the mark price and funding rate are typically calculated based on external indices or reference prices and premium indices, making TradFi assets closer to the crypto-native contract experience in terms of visible depth, order placement/market making, and API consistency, naturally suitable for quantitative institutions and API users.

• The other is the TradFi CFD (Quote) model, centered on bilateral quotes from the platform or liquidity providers. Trading is more about matching based on bid/ask quotes, lacking visible order book depth and a Maker ecosystem. The advantages lie in a rich variety of assets and low entry barriers. However, key elements such as price formation, spreads/commissions, overnight fees, and liquidation paths rely more on platform-side mechanisms, offering relatively limited strategy reusability, leaning more towards medium-low frequency and directional trading.

I. Perpetual Contracts vs. CFD

Regarding differences in product form and trading mechanisms, the product roadmaps and long-term strategies of various platforms have shown significant divergence.

2. Core Data Matrix Analysis

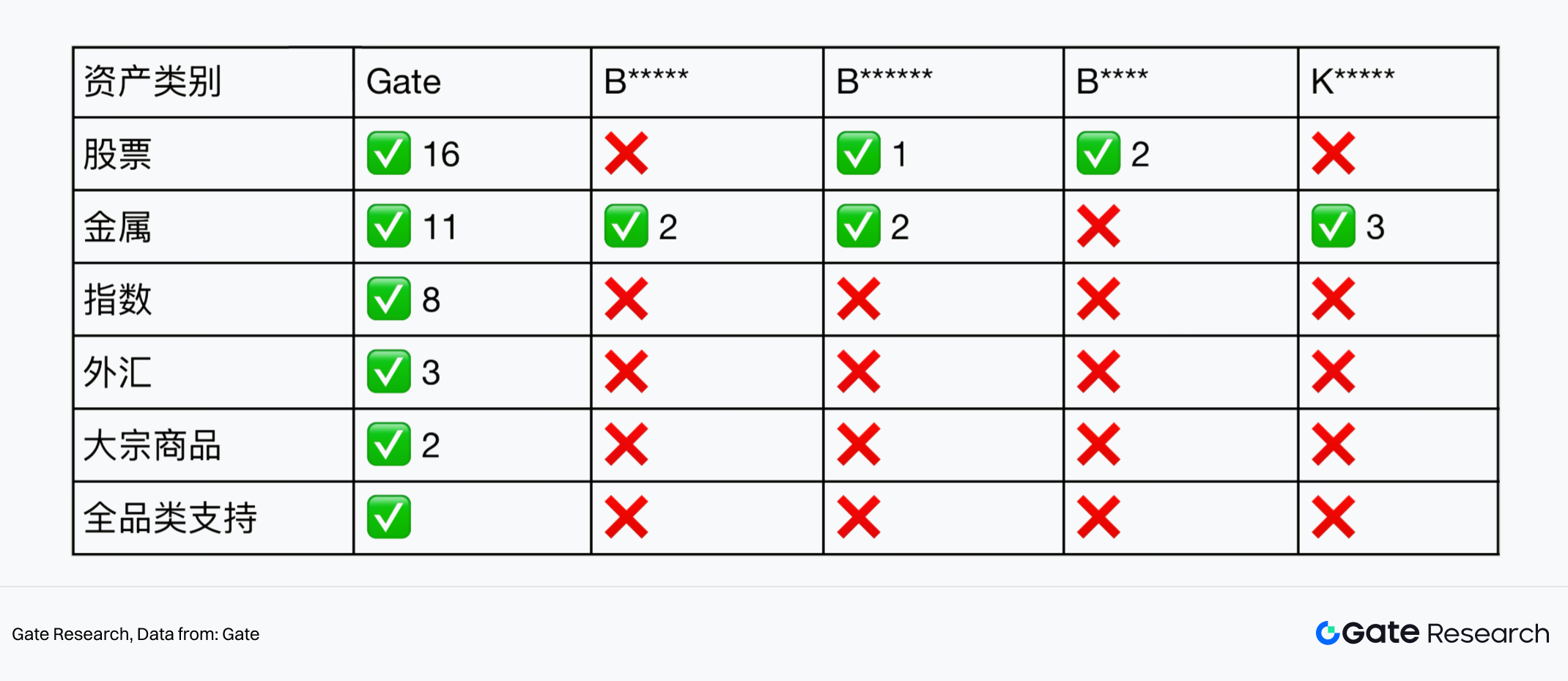

2.1 Perpetual Contract (Orderbook) Coverage Matrix — Gate's Absolute Moat

From the coverage matrix perspective, Gate has established a very clear leading position in traditional asset Orderbooks. Currently, Gate is the only platform achieving full-category Orderbook coverage; stocks, metals, indices, forex, and commodities can all be traded within the same Orderbook system. Simultaneously, Gate is also the only exchange that has truly placed indices and commodities into the Orderbook. Placing TradFi assets directly into the Orderbook, rather than relying on quote-based CFDs, essentially chooses a method closer to real trading. In other words, this means prices are formed through market matching, with real order books, depth, and the ability to place orders and make markets. Consequently, TradFi assets can be directly used by quantitative strategies and APIs, just like BTC and ETH.

II. TradFi Orderbook Coverage of Mainstream Crypto Exchanges

Statistical Scope Note: Only perpetual contract products supporting the Orderbook mechanism are counted; quote-based (CFD / Quote) modules are excluded.

Regarding stocks, Gate has listed 16 assets supporting Orderbook matching, placing it at the forefront among similar platforms. It currently covers core tech stocks represented by AAPL, NVDA, and TSLA, includes high-beta assets highly correlated with crypto like COIN and MSTR, and extends to indices and leveraged ETFs such as QQQ and TQQQ. This combination enables professional traders to participate in stock core assets, crypto-linked assets, and macro index-level opportunities within the same Orderbook perpetual system, forming a more complete cross-market trading and hedging structure.

Regarding metals, Gate's perpetual contracts not only cover core safe-haven assets like gold and silver but also extend to platinum, palladium, and industrial metals like copper, aluminum, and nickel, forming a complete precious and industrial metals trading structure. Against the backdrop of overall metal strength and significantly amplified volatility in 2026, this multi-layered coverage allows metal assets to simultaneously carry safe-haven, macro, and industrial cycle trading logics within the Orderbook perpetual system, significantly enhancing tradability and strategy space.

Furthermore, Gate has established a substantial first-mover advantage in index perpetual contracts, currently listing 8 indices such as NAS100, UK100, SPX500, US30, HK50, and JPN225, all operating on the Orderbook system, constituting a difficult-to-replicate product barrier.

Additionally, forex and commodity perpetuals have also been practically implemented. Although the number is still expanding, the technology, risk control, and liquidity models have been validated. Among them, Gate has formed a completely independent differentiated segment in TradFi commodity perpetual contracts, having already launched live trading for XTI (WTI crude oil) and XBR (Brent crude oil) perpetual contracts. In the context of escalating geopolitical tensions and significantly amplified energy price volatility in 2026, integrating crude oil, a core commodity, into the Orderbook perpetual system enables related risk hedging, directional trading, and cross-asset allocation to be efficiently completed for the first time within a crypto-native derivatives framework, further amplifying Gate's first-mover advantage in the TradFi perpetual track.

2.2 TradFi CFD Module Comparison — The Main Battlefield for Competitors

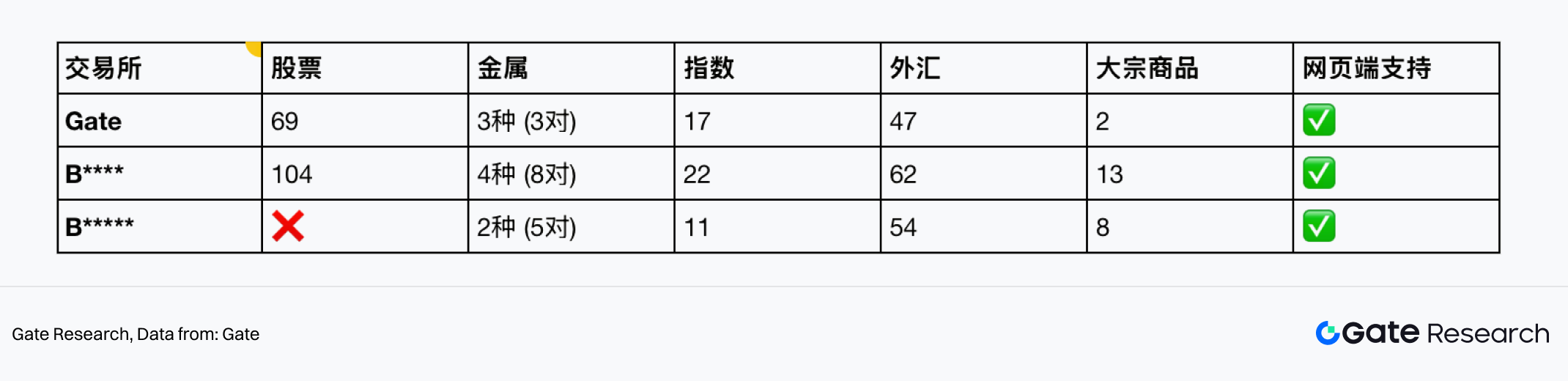

In the TradFi CFD module, the market presents a completely different competitive landscape from Orderbook perpetuals. This track emphasizes "more assets," with the core goal of lowering barriers and quickly meeting the trading needs of cross-border users. The product form is primarily quote-based, with shallow or no order books. The trading experience is closer to traditional forex or CFD platforms, suitable for directional speculation but not emphasizing deep participation or high-frequency trading.

III. TradFi CFD Module Comparison of Mainstream Crypto Exchanges

Statistical Scope Note: Only independently existing TradFi / CFD quote-based modules within exchanges are counted; perpetual contract products are excluded.

Within this framework, other mainstream CEXs cover a broader user base with a large number of stock, forex, and index assets. In comparison, although Gate also provides a certain scale of stock CFD products, its resource investment is relatively restrained. In terms of quantity, Gate's CFD module covers 69 stocks, 17 indices, 47 forex pairs, supplemented by a small number of metal and commodity varieties, possessing basic completeness overall but serving more as a supplementary role rather than the platform's core focus.

Overall, for Gate, the advantage does not lie in how many TradFi assets are listed, but in whether these assets can truly be traded like crypto assets—for example, having real order books, continuous price discovery, the ability to place orders, make markets, and be directly used by quantitative strategies and APIs. It is precisely this approach of treating TradFi assets as crypto-native derivatives that creates the gap between Gate and other platforms at the perpetual contract level.

3. Objective Facts and User Experience Differences (Qualitative Analysis)

Beyond quantitative statistics, product operations, user experience, and fee structures also influence user choices.

3.1 Asset Visibility and Compliance Thresholds

Regarding asset visibility and compliance strategies, different platforms have adopted clearly divergent paths. Gate adopts a relatively conservative strategy; TradFi stock trading pairs are only open to logged-in users, and visitors cannot directly view the order book, which to some extent limits search engine indexing and organic traffic acquisition. Simultaneously, Gate clearly segregates related assets in naming, using prefixes like 'X' or suffixes like 'ONDO' (e.g., TESLAX, APPLON) to emphasize their synthetic asset or tokenized nature. This approach helps reduce compliance risks but can also reinforce the cognitive boundary of "not being real stocks" in users' minds.

In contrast, M*** and B***** adopt more aggressive customer acquisition strategies. Their related TradFi stock products are open to visitors across the entire network, directly displayed using native stock tickers like AAPL and TSLA. This facilitates organic traffic acquisition, with almost zero user understanding cost, significantly improving initial reach and conversion efficiency. Similarly, B******'s order book information is also externally visible. Such strategies hold more advantages in user growth and cognitive migration but may also face higher securities attribute and regulatory compliance pressures.

3.2 Fee Structures and Product Operations

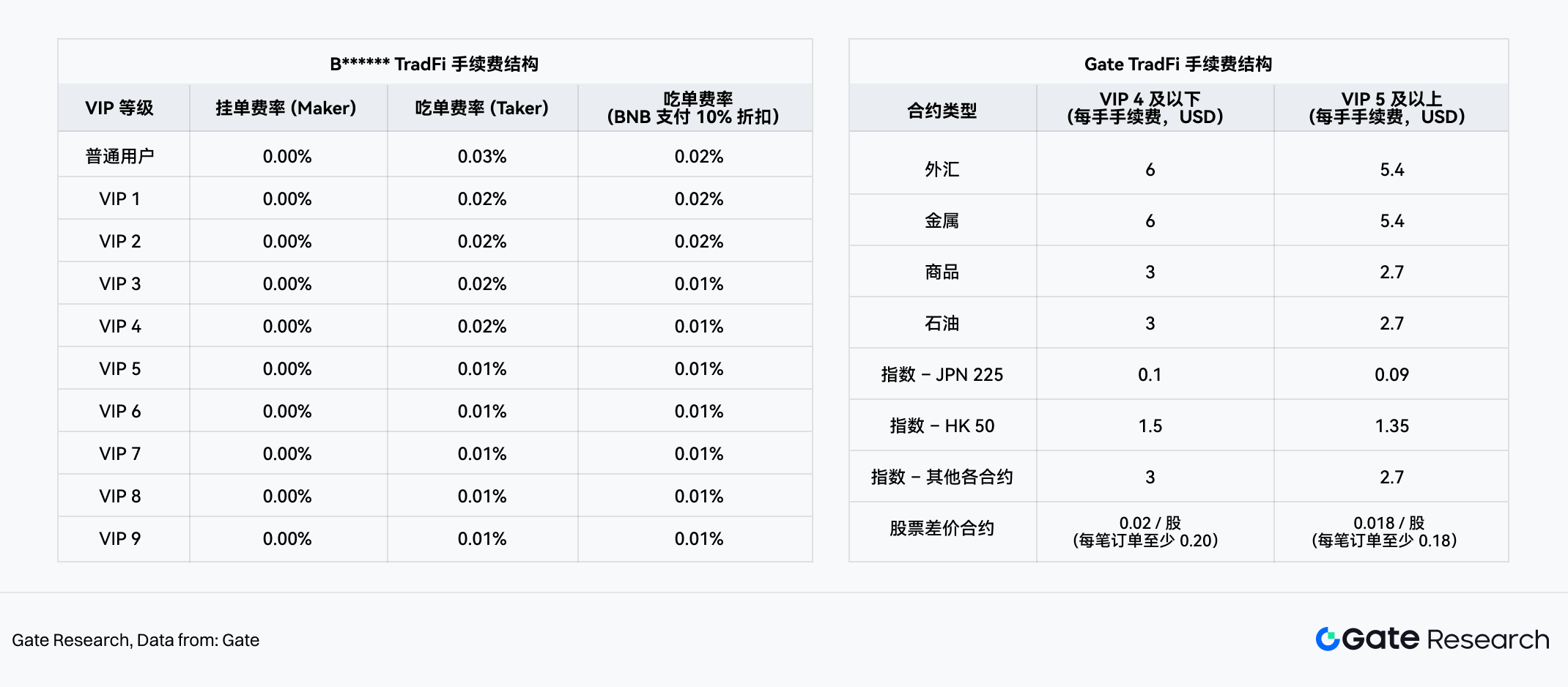

In TradFi-related products, Gate and B****** have adopted截然不同的 pricing models in fee design. Gate continues with the fixed per-lot charging model common in traditional CFD markets, while B****** TradFi Perps沿用 the percentage fee structure based on notional trading volume used in perpetual contracts.

IV. B****** TradFi Fee Structure / Gate TradFi Fee Structure

Taking gold (XAUUSD) as an example, with a contract specification of 1 lot = 100 oz, Gate's metal TradFi contracts adopt a fixed per-lot fee: approximately $6 per lot for regular users (VIP4 and below), which can be reduced to $5.4 for high-level users (VIP5 and above). This fee is independent of the gold price and notional trading volume, with costs clearly known before order placement, offering high predictability.

In contrast, B******* TradFi Perps沿用 the percentage fee model of U-based perpetual contracts. Under the original price system without considering any phased discounts, the taker fee for regular users is 0.05% (0.045% when paying with BNB), while for the highest-level users (VIP9), the taker fee is 0.017% (0.0153% with BNB). In this model, fees change linearly with the gold price.

Comparing under the premise of 1 lot = 100 oz, the gold price range where Gate and B******* fees break even is approximately, with B******'s fees typically being lower under normal circumstances:

• Regular users: $120–133/oz

• Highest-level users: $318–353/oz

Considering real gold prices have long been far above this threshold, in the current market environment, Gate's fees are overall more competitive for small to medium-sized position trades. This is mainly reflected in the following trading scenarios:

• Trades primarily involving 1 lot or a small number of lots, avoiding fee amplification as prices rise.

• High-frequency or strategic trading, where stability and predictability of single-trade costs are more critical.

• TradFi / CFD user migration scenarios, where users are more familiar with per-lot pricing.

Regarding marketing packaging and content provision, Gate's investment in TradFi is more concentrated and sustained. Based on current visible pages on the App and Web, Gate has launched 10+ ongoing or recent operational activities around TradFi, covering various forms such as trading rewards, physical gold incentives, exclusive tasks for beginners, trial funds, and point incentives, maintaining a high update frequency. Simultaneously, Gate provides 10+ announcements, tutorials, and explanatory materials around TradFi, covering product launch notes, contract rules, leverage and risk control adjustments, research interpretations, and beginner guides, forming a relatively complete activity and educational content system.

In product presentation, Gate highlights the TradFi module prominently on the App and Web homepage, continuously exposing it as a core business module to reduce user discovery and understanding costs. In contrast, B******'s TradFi-related entry points are relatively deeper in the hierarchy, leaning more towards functional contract supplements, with relatively limited related marketing activities and systematic tutorials. Overall, through higher-frequency activity operations and denser explanatory content, Gate holds more obvious advantages in user reach, initial conversion, and TradFi user education.

V. Gate TradFi Entry Point

3.3 Strategic Divergence in Trading Models

3.3.1 Model Selection by Each Platform

In the TradFi track, each platform's choice of trading model for traditional assets directly reflects its strategic positioning and product architecture differences:

• B****'s Pure CFD Strategy: B**** does not support classic TradFi assets in its perpetual contract products. All traditional asset trading occurs within an independent TradFi CFD module. This effectively separates crypto users and traditional trading users into two different systems, with trading logic and matching mechanisms not interfering with each other.

• B*****'s Hybrid Model Strategy: B***** supports stock and metal assets in its perpetual contract products, but other asset classes (indices, forex, commodities, etc.) still need to be traded through its TradFi CFD module. Users need to re-login or re-authenticate when jumping from the main site to the TradFi interface, implying interface and session state switching costs.

• Gate's Multi-Asset Orderbook Perpetual Contract Strategy: For the five categories of traditional assets—stocks, metals, indices, forex, and commodities—Gate employs the Orderbook mode perpetual contract matching mechanism, rather than relying on independent CFD quote products to carry trading. This means related TradFi assets enter the matching market on Gate in the form of standardized derivatives, with prices determined by the supply and demand of buy and sell orders in the order book. Users face market liquidity rather than platform counterparty quotes. Although different asset classes are located in their respective trading sections, their underlying matching framework, order book logic, and trading rules remain consistent, giving multi-asset trading a unified market structure and strategy reusability at the mechanism level.

3.3.2 Strategic Implications Behind Model Selection

These three designs represent different strategic approaches. B**** and B***** have taken a more "pragmatic" path, optimizing for different user groups and market demands by isolating the trading systems for crypto assets and TradFi assets. This architecture allows for rapid product launch and market demand coverage in a relatively short time.

On the other hand, Gate chooses to cover all asset classes based on a unified Orderbook architecture. This not only unifies trading logic but also positions the platform as a neutral matching entity. In the Orderbook mode, the platform does not directly act as a counterparty; its revenue comes from trading fees and is not directly linked to user profits or losses. In contrast, in CFD mode, the platform typically acts as the counterparty, and its revenue may be correlated with user trading outcomes. Gate's insistence on the Orderbook mode for TradFi conveys a philosophy: TradFi assets should be treated with the same matching approach as crypto assets.

For users pursuing trading transparency, clear liquidity structure, and controllable counterparty risk, this consistent trading experience holds significant appeal.

3.3.3 Long-Term Strategic Intent

From the perspective of trading structure and risk-bearing mechanisms, different trading models have inherent differences in long-term scalability. Under the Orderbook architecture, the platform only undertakes matching functions; users are counterparties to each other, and the platform itself does not need to intervene in price formation or bear directional risk. This design allows the platform to continuously focus on liquidity building, matching efficiency, and trading depth optimization without being constrained by the structural burden brought by asset class expansion, making it more suitable for supporting a multi-asset, long-term evolving trading system.

From the long-term perspective of the RWA track, truly mature RWA trading forms should possess clear price discovery mechanisms, transparent liquidity structures, and reusable trading infrastructure, rather than relying on a single product form or closed pricing model. The public matching and market-based pricing emphasized by the Orderbook mode naturally align more closely with this goal. Gate's current use of a unified Orderbook architecture for TradFi assets essentially builds scalable technology and trading paradigms in advance for future more complex and standardized real-world asset trading scenarios.

4. Conclusion: Gate is Transitioning from Multi-Asset Expansion to Trading Infrastructure Upgrade

Synthesizing the systematic analysis of product forms, data matrices, and platform paths above leads to a clear conclusion: Gate's true differentiation in the TradFi track is not reflected in "whether it provides stocks, indices, or forex," but in "what trading structure is used to carry these assets." While most platforms in the industry are still in the TradFi product expansion stage, Gate has already entered the competition stage at the trading mechanism level.

The mainstream approach in the current market is to incorporate traditional assets into independent CFD quote systems, with asset coverage quantity and low-barrier experience as core competitive points. Gate has chosen a path leaning more towards underlying architecture evolution—directly integrating TradFi assets into a unified Orderbook perpetual matching system, making them consistent with crypto-native contracts in price formation, order book structure, matching logic, and API rules.