Hyperliquid at a crossroads: Follow Robinhood or continue the Nasdaq economic paradigm?

- 核心观点:Hyperliquid交易量大但费率低,盈利模式面临挑战。

- 关键要素:

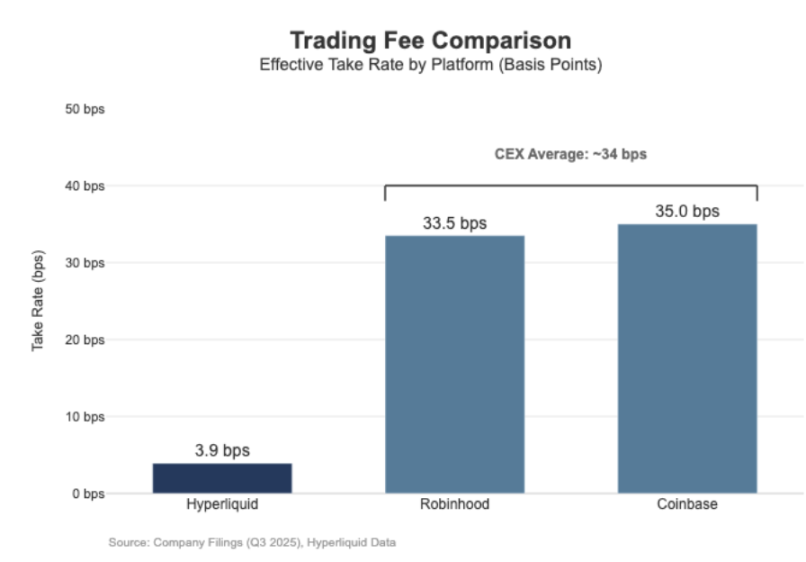

- 30天清算额2056亿美元,费率仅3.9基点。

- Coinbase等零售平台费率超35基点,盈利渠道多元。

- Hyperliquid定位为“市场层”交易所,利润空间受结构性压缩。

- 市场影响:凸显去中心化交易平台盈利模式转型压力。

- 时效性标注:中期影响。

Original author: shaunda devens

Original translation by: Saoirse, Foresight News

Hyperliquid's perpetual contract liquidation volume has reached Nasdaq levels, but its economic benefits have not matched this. In the past 30 days, the platform liquidated perpetual contracts with a notional value of $205.6 billion (an annualized value of $617 billion on a quarterly basis), but its fee revenue was only $80.3 million, with a fee rate of approximately 3.9 basis points.

Its profit model is similar to that of a "wholesale trading venue".

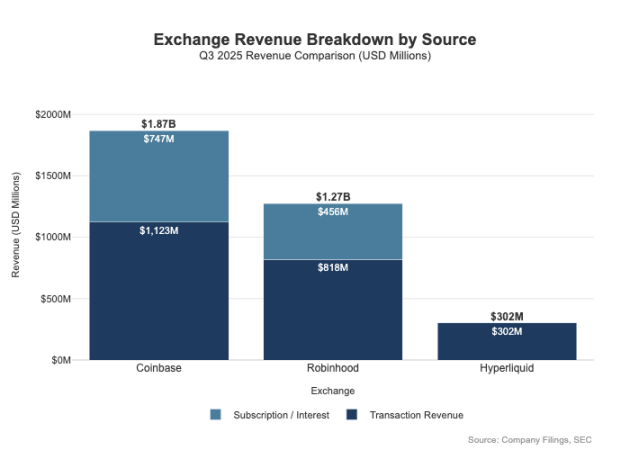

In comparison, Coinbase reported a trading volume of $295 billion and trading revenue of $1.046 billion in Q3 2025, with an implied fee rate of 35.5 basis points. Robinhood exhibits a similar "retail-style profit model" in its cryptocurrency business: $80 billion in nominal cryptocurrency trading volume generated $268 million in cryptocurrency trading revenue, with an implied fee rate of 33.5 basis points; meanwhile, the platform's nominal stock trading volume in Q3 2025 was $647 billion.

The difference between the two lies not only in fee rates—retail platforms have more diversified revenue streams. In the third quarter of 2025, Robinhood's transaction-related revenue was $730 million, in addition to $456 million in net interest income and $88 million in other revenue (primarily from its Gold subscription service). In contrast, Hyperliquid still relies heavily on transaction fees, and at the protocol level, its fee rates have consistently remained at single-digit basis points.

This difference essentially stems from their different positioning: Coinbase and Robinhood are "brokerage/distributor companies," generating profits through their balance sheets and subscription services; while Hyperliquid is closer to the "exchange level." In traditional market structures, profit pools are distributed at these two levels.

The Difference Between Brokerage and Exchange Models

The core difference in traditional finance (TradFi) lies in the separation of the "distribution layer" and the "market layer." Retail platforms such as Robinhood and Coinbase occupy the "distribution layer," which occupies the high-margin area; while exchanges such as Nasdaq occupy the "market layer"—at this level, pricing power is structurally limited, and competition in the transaction execution process is gradually trending towards a "commoditized economic model" (i.e., profit margins are significantly compressed).

1. Brokerage firm = Distribution + Client balance sheet

Brokerage firms control client relationships. Most users don't directly access NASDAQ but instead enter the market through a broker: the broker handles account opening, asset custody, margin/risk management, client support, and tax documentation, before routing orders to the specific trading venue. This "client relationship ownership" creates profit opportunities beyond trading itself.

- Related to cash balance: cash collection interest rate spread, margin trading interest, securities lending income;

- Service packages: subscription services, bundled products, bank card services/consulting services;

- Order routing economics: Brokers control transaction flow and can embed payment sharing or revenue-sharing mechanisms in the routing chain.

This is the core reason why brokers can profit more than trading venues: the profit pool is concentrated on the "distribution end" and the "fund balance end".

2. An exchange consists of order matching, a rules system, and infrastructure; its transaction fee rate is subject to a cap.

Exchanges operate trading venues, and their core functions include order matching, setting market rules, ensuring deterministic execution, and providing trading connectivity. Their revenue sources include:

- Transaction fees (in highly liquid products, fees are continuously driven down due to competition).

- Rebate/Liquidity Incentive Programs (to attract liquidity, a large portion of the public transaction fees are often returned to market makers);

- Market data services, transaction connectivity/server hosting services;

- Listing services and index licensing fees.

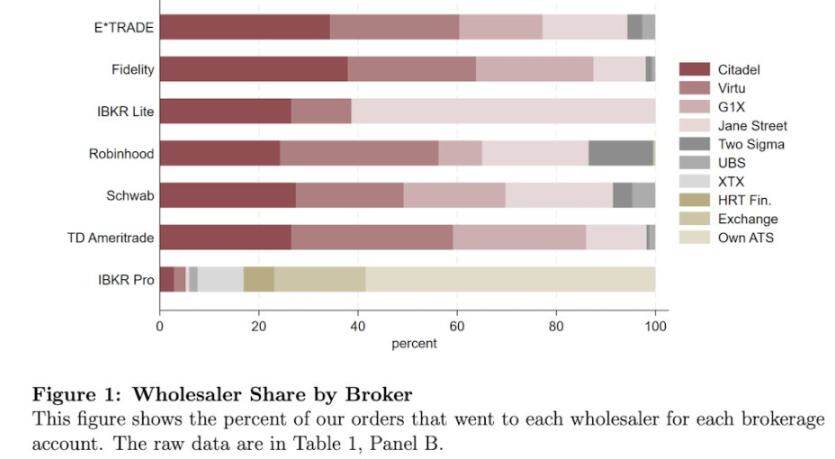

Robinhood's order routing model clearly illustrates this architecture: the broker (Robinhood Securities) controls users and routes orders to third-party marketplace centers, with revenue from the routing process shared throughout the chain. The "distribution layer" is the high-margin segment—it controls user acquisition and develops diverse revenue streams around trade execution (such as order flow fees, financing, securities lending, and subscription services).

Nasdaq belongs to the "low-margin tier": its core products are "commoditized trade execution" and "order queue access rights". Its pricing power is subject to three constraints in terms of mechanism - it needs to return commissions to market makers in order to attract liquidity, regulators set a cap on access fees, and order routing is highly flexible (users can easily switch to other platforms).

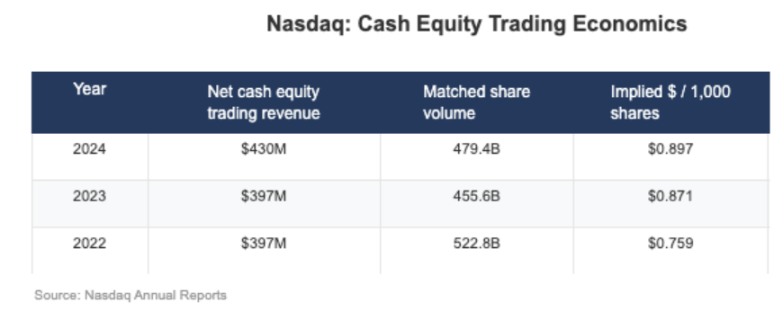

Data disclosed by Nasdaq shows that its stock business has an "implied net cash gain" of only $0.001 per share (i.e., one-thousandth of a dollar per share).

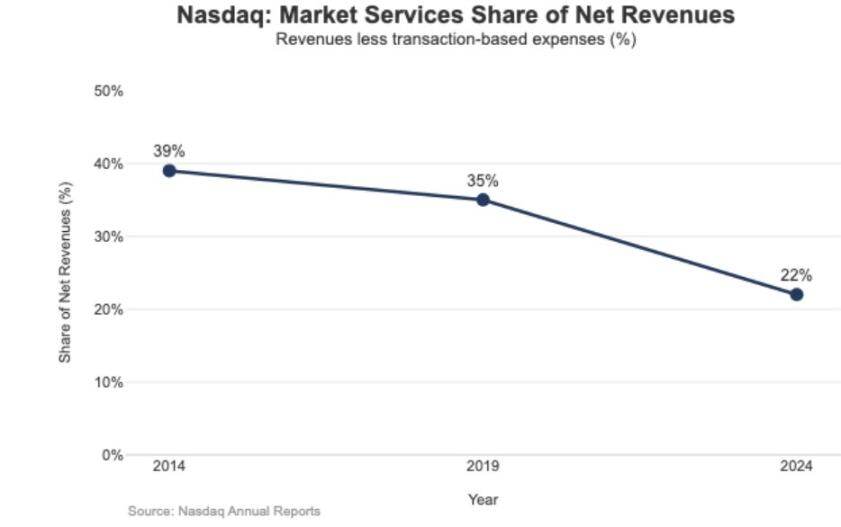

The strategic impact of low profit margins is also reflected in Nasdaq's revenue structure: In 2024, "market services" revenue was $1.02 billion, accounting for only 22% of total revenue of $4.649 billion; while this proportion was 39.4% in 2014 and 35% in 2019 - this trend indicates that Nasdaq is gradually shifting from "execution business that relies on market transactions" to "more sustainable software/data business".

Hyperliquid, positioned at the "market level"

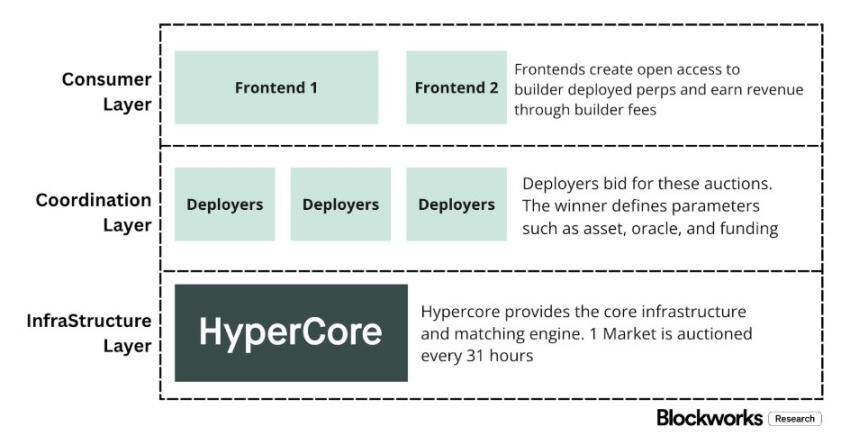

Hyperliquid's actual fee rate of 4 basis points aligns with its strategy of "proactively choosing its market layer positioning." The platform is building an "on-chain Nasdaq": through a high-throughput order matching, margin calculation, and clearing technology stack (HyperCore), it adopts a "market maker/taker" pricing model and provides market maker rebates—its core optimization direction is "trade execution quality" and "liquidity sharing," rather than "retail user profitability."

This positioning is reflected in the separation of two "traditional financial" aspects, a design that most cryptocurrency trading platforms do not adopt:

1. Unlicensed Brokers/Distributors (Builder Codes)

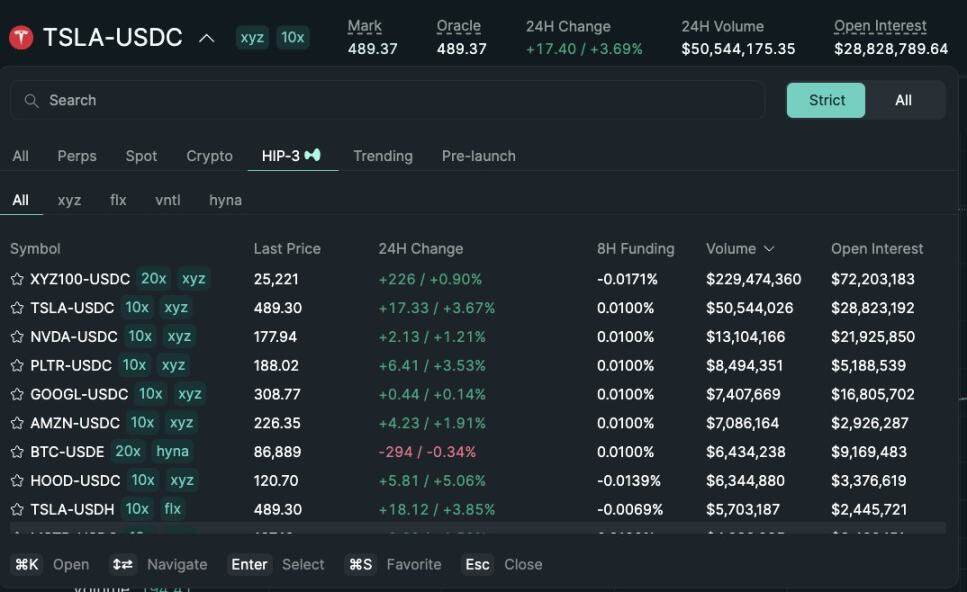

"Builder Codes" allows third-party interfaces to connect to core trading venues and set their own fee structures. The third-party transaction fee cap for perpetual contracts is 0.1% (10 basis points), while the fee for spot trading is 1%, and fees can be set individually for each order—this design creates a "competitive distribution market" rather than a "monopoly by a single app."

2. Unlicensed Market Launch/Product Tier (HIP-3)

In traditional finance, exchanges control listing authority and product creation rights; HIP-3 externalizes this function: developers can deploy perpetual contracts based on the HyperCore technology stack and APIs, and independently define and operate trading markets. From an economic perspective, HIP-3 formally establishes a "revenue-sharing mechanism between trading venues and product providers"—the deployers of spot and HIP-3 perpetual contracts can receive 50% of the transaction fees for the deployed assets.

"Builder Codes" has already proven effective in distribution: as of mid-December, about one-third of users were transacting through third-party front-ends rather than the official interface.

However, this structure also puts predictable pressure on the transaction fee revenue of trading venues:

- Pricing compression: Multiple front-ends share the same back-end liquidity, and competition forces the "overall cost" to be reduced to the lowest level; moreover, transaction fees can be adjusted according to orders, further pushing pricing closer to the bottom line;

- Loss of profit channels: The front end controls the user account opening, service packaging, subscription and trading process, occupying the high gross profit margin of the "broker layer", while Hyperliquid only retains the low gross profit of the "trading venue layer";

- Strategic routing risk: If the front end develops into a "cross-platform order routing provider", Hyperliquid will be forced into "wholesale execution competition" - and will need to reduce fees or increase rebates to maintain transaction traffic.

Hyperliquid has proactively chosen a "low-margin market tier" positioning through HIP-3 and Builder Codes, while allowing a "high-margin broker tier" to form above it. If the front end continues to expand, these brokers will gradually control "user-side pricing," "user retention channels," and "routing power," which will put structural pressure on Hyperliquid's commission rates in the long run.

Defend distribution rights and expand non-exchange profit pool

Hyperliquid's core risk is the "commoditization trap": if third-party front-ends can continue to attract users at prices lower than the official interface and eventually achieve "cross-platform routing", the platform will be forced to shift to a "wholesale execution economy model" (i.e., continuously narrowing profit margins).

Judging from recent design adjustments, Hyperliquid is trying to avoid this outcome while broadening its revenue streams beyond transaction fees.

1. Distribution Defense: Maintaining the economic competitiveness of the official interface.

Previously, Hyperliquid proposed a "up to 40% discount on transaction fees for staking HYPE tokens"—a design that would have structurally made it feasible for third-party front-ends to offer "lower prices than the official interface." With the cancellation of this proposal, external distribution channels lost the direct subsidy of "pricing lower than the official interface." Meanwhile, the HIP-3 marketplace, initially only distributed through "developer distribution" and not displayed on the official front-end, has now been included in the official front-end's "strict list." This series of actions sends a clear signal: Hyperliquid retains permissionless characteristics at the "developer level" but is unwilling to compromise on "core distribution rights."

2. Stablecoin USDH: Shifting from "Trading Profits" to "Liquidity Pool Profits"

The core purpose of launching USDH is to reclaim the "stablecoin reserve revenue" that was originally flowing out. According to the public mechanism, 50% of the reserve revenue is allocated to Hyperliquid, and 50% is used for the development of the USDH ecosystem. In addition, the design of "USDH trading market enjoying transaction fee discounts" further strengthens this logic: Hyperliquid is willing to exchange "compressed profit per transaction" for "larger and more stable liquidity pool profits" - essentially adding a "similar annuity income stream", the growth of which can rely on the "currency base" (rather than solely on trading volume).

3. Portfolio Margin: Introducing "Institutional Brokerage Financing Economy"

The "combined margin" mechanism unifies the margin calculation for spot and perpetual contracts, allowing for risk exposure hedging while introducing a "native lending cycle." Hyperliquid charges "10% of the borrower's interest"—this design gradually links the protocol's economic model to "leverage utilization" and "interest rates," making it closer to the profit logic of "brokers/institutional brokers" rather than a pure exchange model.

Hyperliquid's Path Towards a Brokerage Economy Model

Hyperliquid's trading volume has reached the level of "mainstream exchanges," but its profit model remains at the "market level": nominal trading volume is huge, but the actual transaction fee rate is only a single-digit basis point. The gap with Coinbase and Robinhood is structural: retail platforms are at the "broker level," controlling user relationships and fund balances, and achieving high gross margins through diversified profit pools such as "financing, idle funds, and subscriptions"; pure exchanges, on the other hand, take "trade execution as their core product," and due to liquidity competition and routing flexibility, "trade execution" will inevitably become commoditized, and profit margins will be continuously squeezed—Nasdaq is a typical example of this constraint in traditional finance.

Hyperliquid initially aligned deeply with the "exchange marketplace prototype": by separating "distribution (Builder Codes)" from "product creation (HIP-3)," it rapidly drove ecosystem expansion and market coverage. However, this architecture came at the cost of "economic spillover": if third-party front-ends controlled "overall pricing" and "cross-platform routing rights," Hyperliquid would face the risk of "becoming a wholesale channel, clearing transaction traffic with low profit margins."

However, recent actions indicate that the platform is consciously shifting towards "defending distribution rights" and "broadening its revenue structure" (no longer relying on transaction fees). For example, it has stopped subsidizing "external front-end price competition," incorporated the HIP-3 market into its official front-end, and added a "balance sheet-style profit pool." The launch of USDH is a typical example of incorporating "reserve returns" into the ecosystem (including a 50% commission and fee discounts); the portfolio margin introduces a "financing economy" by "charging 10% interest to borrowers."

Currently, Hyperliquid is gradually moving towards a "hybrid model": based on a "trade execution channel," it is combined with "distribution defense" and a "profit pool driven by a liquidity pool." This transformation reduces the risk of "falling into the wholesale low-margin trap" while moving closer to a "brokerage-style revenue structure" without abandoning its core advantages of "unified execution and clearing."

Looking ahead to 2026, Hyperliquid's core challenge is how to move towards a "brokerage-style economy" without disrupting its "outsourcing-friendly model." USDH serves as the most direct test case—its current supply is approximately $100 million, demonstrating that without platform control over distribution, the expansion of "outsourced issuance" will be extremely slow. A more obvious alternative would be a "default setting on the official interface," such as automatically converting the approximately $4 billion USDC base into a native stablecoin (similar to Binance's automatic conversion of USDC to BUSD).

If Hyperliquid wants to acquire a "broker-grade profit pool," it must take "broker-style actions": strengthen control, deepen the integration of its own products and official interfaces, and clarify the boundaries with the ecosystem team (to avoid internal friction over "distribution rights" and "fund balances").