Ethereum's identity dilemma: Is it cryptocurrency, or a shadow of Bitcoin?

- 核心观点:以太坊货币化进程依附于比特币。

- 关键要素:

- ETF资金流入强劲,按市值计需求超比特币。

- 财库公司兴起,创造持续结构性买盘。

- 与比特币高相关性,贝塔系数高,属杠杆表达。

- 市场影响:强化其作为比特币高贝塔资产的地位。

- 时效性标注:中期影响。

Original author: AJC

Original translation by Luffy, Foresight News

Among all mainstream cryptocurrency assets, Ethereum has sparked the most intense debate. While Bitcoin's status as a mainstream cryptocurrency is widely recognized, Ethereum's position remains unresolved. Some argue that Ethereum is the only non-sovereign currency asset besides Bitcoin with credibility; others believe that Ethereum is essentially a business, facing declining revenue, shrinking profit margins, and fierce competition from numerous public chains offering faster and lower-cost transactions.

This controversy seemed to reach its peak in the first half of the year. In March, Ripple's (XRP) fully diluted valuation briefly surpassed Ethereum's (it's worth noting that all of Ethereum's tokens are in circulation, while Ripple's circulating supply is only about 60% of its total supply).

On March 16th, Ethereum's fully diluted valuation was $227.65 billion, while Ripple's corresponding valuation reached $239.23 billion. This outcome was almost unpredictable a year prior. Then, on April 8th, 2025, the Ethereum-to-Bitcoin exchange rate (ETH/BTC) fell below 0.02, hitting its lowest level since February 2020. In other words, all of Ethereum's gains relative to Bitcoin during the previous bull market had been completely wiped out. At that time, market sentiment towards Ethereum plummeted to its lowest point in years.

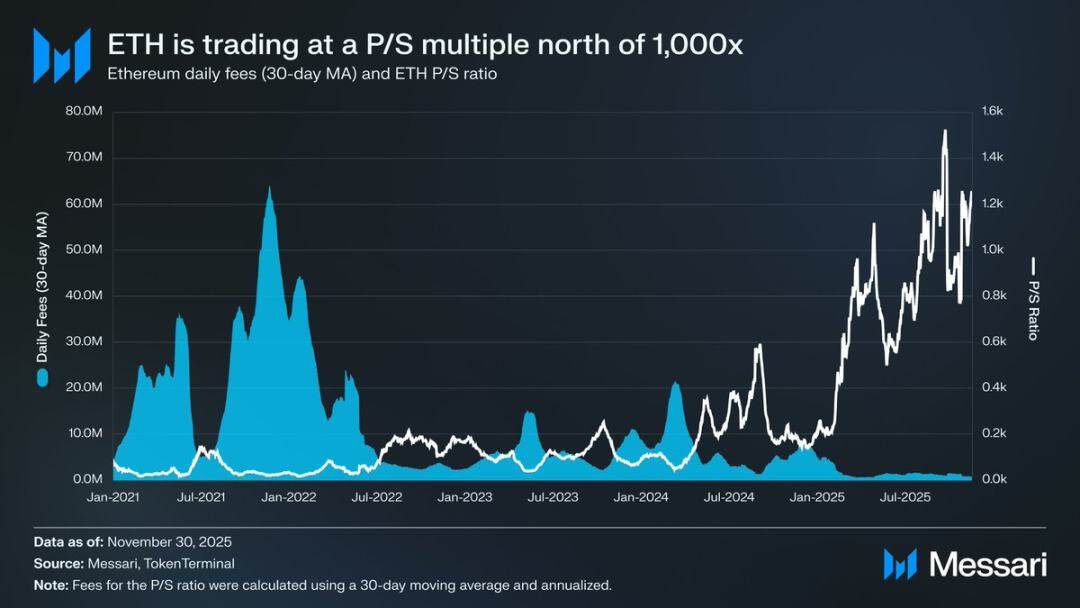

To make matters worse, the price slump is just the tip of the iceberg. With the rise of competing ecosystems, Ethereum's share of the public blockchain transaction fee market continues to shrink. In 2024, Solana made a comeback; in 2025, Hyperliquid emerged as a dark horse. Together, they reduced Ethereum's transaction fee market share to 17%, ranking fourth among public blockchains—a precipitous drop from its top position a year earlier. While transaction fees don't tell the whole story, they are a clear signal reflecting the flow of economic activity. Today, Ethereum faces the most severe competitive landscape in its history.

However, historical experience shows that major reversals in the cryptocurrency market often begin at the moment when market sentiment is at its most pessimistic. When Ethereum was declared a "failure asset" by the outside world, most of its apparent decline had already been priced in by the market.

In May 2025, signs of excessive bearishness on Ethereum began to emerge. Around this time, both the Ethereum-to-Bitcoin exchange rate and its price in US dollars experienced a strong rebound. The Ethereum-to-Bitcoin exchange rate climbed from a low of 0.017 in April to 0.042 in August, a gain of 139%; during the same period, the price of Ethereum in US dollars surged from $1646 to $4793, a gain of 191%. This rally peaked on August 24th, with the price of Ethereum reaching $4946, a new all-time high. After this revaluation, Ethereum's overall trend has clearly returned to an upward trajectory. The leadership change at the Ethereum Foundation and the emergence of a number of treasury companies focused on Ethereum have injected confidence into the market.

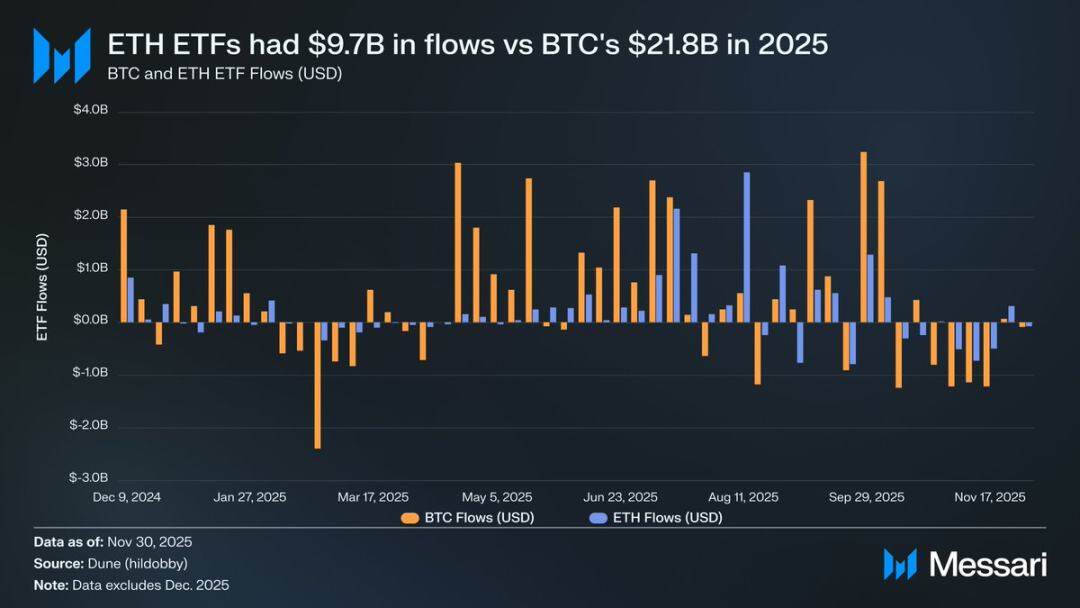

Prior to this surge, the stark contrast between Ethereum and Bitcoin's fortunes was clearly reflected in their respective exchange-traded fund (ETF) markets. In July 2024, an Ethereum spot ETF was launched, but inflows were extremely low. In the first six months after its launch, net inflows totaled only $2.41 billion, a stark contrast to the record-breaking performance of Bitcoin ETFs.

However, with Ethereum's strong recovery, market concerns about its ETF inflows have dissipated. For the year, Ethereum spot ETFs saw net inflows of $9.72 billion, while Bitcoin ETFs saw $21.78 billion. Considering Bitcoin's market capitalization is nearly five times that of Ethereum, the difference in inflows between the two ETFs is only 2.2 times, a gap far lower than market expectations. In other words, adjusted for market capitalization, the market demand for Ethereum ETFs actually exceeded that for Bitcoin. This result completely reversed the argument that "institutions lack genuine interest in Ethereum." Moreover, during certain periods, Ethereum ETF inflows even directly outpaced Bitcoin. From May 26th to August 25th, Ethereum ETFs saw net inflows of $10.2 billion, exceeding the $9.79 billion of Bitcoin ETFs during the same period, marking the first time institutional demand clearly shifted towards Ethereum.

Looking at the performance of ETF issuers, BlackRock continues to lead the market. As of the end of 2025, BlackRock's Ethereum ETF held 3.7 million Ethereum tokens, accounting for 60% of the Ethereum spot ETF market. Compared to 1.1 million tokens held at the end of 2024, this represents a staggering 241% increase, far exceeding the annual growth rate of other issuers. Overall, Ethereum spot ETFs held 6.2 million Ethereum tokens at the end of 2025, representing approximately 5% of its total token supply.

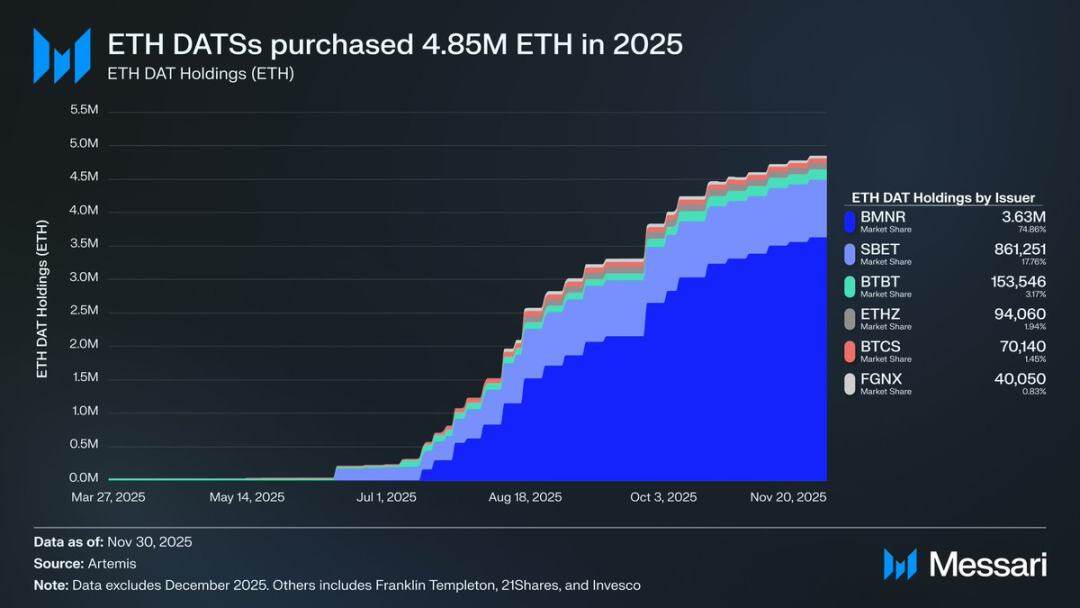

Behind Ethereum's strong rebound, the most crucial driver is the rise of treasury companies focused on Ethereum. These reserves have created unprecedented, stable, and continuous demand for Ethereum, providing support for the asset that narrative hype or speculative funds cannot match. If Ethereum's price movement marked a clear turning point, then the continued accumulation by treasury companies represents the deep structural change that facilitated this inflection.

In 2025, Ethereum treasury companies accumulated 4.8 million Ethereum, representing 4% of its total supply, significantly impacting the price of Ethereum. The most prominent among them was Bitmine (stock code BMNR), led by Tom Lee. This company, originally focused on Bitcoin mining, began gradually converting its reserves and capital into Ethereum in July 2025. Between July and November, Bitmine purchased a total of 3.63 million Ethereum, maintaining its leading position in the Ethereum treasury market with a 75% holding.

Despite Ethereum's strong rebound, the rally has eventually cooled. As of November 30th, the price of Ethereum had fallen from its August high to $2991, even below the all-time high of $4878 during the previous bull run. Compared to the trough in April, Ethereum's situation has improved significantly, but this rebound has not completely eliminated the structural concerns that initially triggered the market's bearish sentiment. On the contrary, the debate surrounding Ethereum's positioning is returning to the public eye with even greater intensity.

On the one hand, Ethereum is exhibiting many characteristics similar to Bitcoin; and these characteristics are precisely what enabled Bitcoin to rise to the status of a monetary asset. Currently, inflows into Ethereum ETFs are no longer weak, and Ethereum Treasury has become a source of sustained demand. Perhaps most importantly, a growing number of market participants are beginning to differentiate Ethereum from other public blockchain tokens, incorporating it into the same monetary framework as Bitcoin.

On the other hand, the core issues that dragged Ethereum down in the first half of this year remain unresolved. Ethereum's core fundamentals have not fully recovered: its public chain transaction fee market share continues to be squeezed by strong competitors such as Solana and Hyperliquid; the transaction activity of the Ethereum underlying network is still far below the peak levels of the last bull market; despite the significant price rebound, Bitcoin has easily broken through its all-time high, while Ethereum is still hovering below its all-time high. Even during Ethereum's strongest months, many holders still viewed this rally as an opportunity to cash out rather than an endorsement of its long-term value.

The core issue in this controversy is not whether Ethereum has value, but rather how ETH, as an asset, can accumulate value through the development of the Ethereum network.

During the last bull market, the market generally believed that ETH's value would directly benefit from the success of the Ethereum network. This is precisely the core logic of the "Ultrasonic Currency Theory": the practicality of the Ethereum network will generate a large demand for token burning, thereby building a clear and institutionalized value support for Ethereum assets.

Today, we can be almost certain that this logic no longer holds true. Ethereum's transaction fee revenue has plummeted and shows no sign of recovery; meanwhile, the two core areas driving Ethereum network growth—real-world assets (RWAs) and institutional markets—both use the US dollar as their core settlement currency, not Ethereum.

Ethereum's future value will depend on how it indirectly benefits from the development of the Ethereum network. However, this indirect value accumulation is highly uncertain. It presupposes that as the systemic importance of the Ethereum network continues to increase, more and more users and capital are willing to view Ethereum as a cryptocurrency and a store of value.

Unlike direct, institutionalized value accumulation, this indirect path offers no certainty whatsoever. It relies entirely on market preferences and collective consensus. This isn't inherently a flaw; however, it means that Ethereum's value growth will no longer have a necessary causal link to the economic activities of the Ethereum network.

All of this brings the controversy surrounding Ethereum back to its core point of contention: while Ethereum may indeed be gradually accumulating a monetary premium, this premium consistently lags behind Bitcoin. The market is once again viewing Ethereum as a "leveraged expression" of Bitcoin's monetary attributes, rather than an independent monetary asset. Throughout 2025, the 90-day rolling correlation coefficient between Ethereum and Bitcoin remained between 0.7 and 0.9, while the rolling beta coefficient soared to a multi-year high, briefly exceeding 1.8. This means that Ethereum's price volatility far exceeds that of Bitcoin, but it also consistently follows Bitcoin's price movements.

This is a subtle but crucial difference. Ethereum's current monetary attributes are rooted in the market's continued acceptance of Bitcoin's monetary narrative. As long as the market firmly believes in Bitcoin's non-sovereign store-of-value nature, some peripheral market participants will be willing to extend this trust to Ethereum. Therefore, if Bitcoin continues its upward trend in 2026, Ethereum will also be able to recover more lost ground.

Currently, Ethereum Treasury is still in its early stages, and its funds for increasing its Ethereum holdings primarily come from common stock issuance. However, if the cryptocurrency market experiences a new bull market, such institutions may explore more diversified financing strategies, such as adopting Strategy's model for expanding its Bitcoin holdings by issuing convertible bonds and preferred stock.

For example, Ethereum treasury companies like BitMine can raise funds by issuing low-interest convertible bonds and high-yield preferred stock, directly using the raised funds to increase their Ethereum holdings while simultaneously staking these Ethereum to generate continuous returns. Under reasonable assumptions, staking returns can partially offset bond interest and preferred stock dividends. This model allows the treasury to leverage financial resources to continuously increase its Ethereum holdings when market conditions are favorable. Assuming a full-blown bull market for Bitcoin in 2026, this "second growth curve" for Ethereum treasury companies will further reinforce Ethereum's high beta relative to Bitcoin.

Ultimately, the market's current pricing of Ethereum's premium is still predicated on Bitcoin's price movement. Ethereum has not yet become a self-sufficient monetary asset with independent macroeconomic fundamentals; rather, it is merely a secondary beneficiary of Bitcoin's monetary consensus, and this beneficiary group is gradually expanding. Ethereum's recent strong rebound reflects that some market participants are willing to view it as a peer of Bitcoin, rather than an ordinary public chain token. However, even in relatively strong phases, market confidence in Ethereum remains inextricably linked to the continued strengthening of the Bitcoin narrative.

In short, while Ethereum's monetization narrative has emerged from its shattered state, it is far from settled. Under the current market structure, coupled with Ethereum's high beta relative to Bitcoin, as long as Bitcoin's monetary narrative continues to materialize, Ethereum's price is expected to see substantial increases; and the structural demand from Ethereum Treasury companies and corporate funds will provide real upward momentum. However, ultimately, in the foreseeable future, Ethereum's monetization process will remain dependent on Bitcoin. Unless Ethereum can achieve low correlation and a low beta coefficient with Bitcoin over a longer period—a goal it has never achieved—Ethereum's premium will always be overshadowed by Bitcoin's luster.