Grayscale Decryption 2026: Ten Trends Reshaping the Industry Ecosystem

- 核心观点:加密市场主导力量转向机构资本。

- 关键要素:

- 宏观不确定性推升替代性价值储存需求。

- 监管清晰化推动机构资金通过ETP等合规渠道入场。

- 比特币预计2026年上半年创历史新高。

- 市场影响:推动市场估值整体走高,弱化散户驱动的四年周期叙事。

- 时效性标注:中期影响

Original title: 2026 Digital Asset Outlook: Dawn of the Institutional Era

Original author: Grayscale research team

Original translation by Peggy, BlockBeats

Editor's Note: After years of high volatility and narrative-driven cycles, crypto assets are entering a distinctly different phase. Rising uncertainty in the fiat currency system, the gradual formation of regulatory frameworks, and the advancement of legislation and institutional allocation for spot ETPs and stablecoins are reshaping how funds enter the crypto market.

Grayscale's core assessment in its "2026 Digital Asset Outlook" is that the dominant force in the crypto market is shifting from retail cycles to institutional capital. Prices are no longer primarily driven by emotional, explosive price increases, but rather by compliant channels, long-term funds, and sustainable fundamentals, and the "four-year cycle" narrative is weakening.

This article systematically outlines the top ten investment themes that may shape the market in 2026, ranging from value stores, stablecoins, and asset tokenization to DeFi, AI, and privacy infrastructure, painting a picture of a crypto ecosystem gradually embedding itself into the mainstream financial system. At the same time, the report also clearly points out which hot topics are more like "noise" than decisive variables in the short term.

The following is the original text:

Key Takeaways

We anticipate a structural shift in digital asset investment will accelerate in 2026, driven primarily by two themes: rising macroeconomic demand for alternative stores of value and significantly improved regulatory clarity. These factors combined are expected to attract new funding sources, expand the adoption of digital assets (particularly among wealth management advisors and institutional investors), and drive the more comprehensive integration of public blockchains into mainstream financial infrastructure.

Based on the above trends, we predict that digital asset valuations will generally rise in 2026, while the so-called "four-year cycle" (the theory that the crypto market follows a fixed four-year rhythm) will come to an end. In our view, Bitcoin prices are likely to reach new all-time highs in the first half of the year.

Grayscale anticipates that bipartisan structural legislation for the crypto market will become U.S. law in 2026. This will further deepen the integration of public blockchains with traditional finance, promote compliant trading of digital asset securities, and potentially allow startups and established companies to conduct on-chain issuances.

The future of the fiat currency system is becoming increasingly uncertain; in contrast, we are almost certain that the 20 millionth Bitcoin will be mined in March 2026. Against the backdrop of rising risks to fiat currencies, digital currency systems like Bitcoin and Ethereum, with their transparent, programmable, and ultimately scarce supply characteristics, are expected to see stronger demand.

We anticipate that more crypto assets will become available to investors through exchange-traded products (ETPs) in 2026. These products have had a good start, but many platforms are still conducting due diligence and pushing forward with the integration of crypto assets into their asset allocation processes. As this process matures, substantial but slower-moving institutional funds are expected to continue entering the market throughout 2026.

We have also compiled a list of the top ten crypto investment themes for 2026 to reflect the wide range of emerging applications of public blockchain technology. Each theme corresponds to a specific crypto asset:

1. The risk of dollar depreciation is driving demand for currency alternatives.

2. Increased regulatory clarity supports the adoption of digital assets.

3. Since the implementation of the GENIUS Act, the influence of stablecoins has continued to expand.

4. Asset tokenization reaches a critical inflection point.

5. Blockchain is becoming mainstream, increasing demand for privacy solutions.

6. The centralization of AI calls for blockchain-based solutions.

7. DeFi is accelerating its development, with lending as its leading sector.

8. Mainstream adoption is forcing the construction of next-generation infrastructure.

9. Greater focus on sustainable revenue models

10. Investors will "default" to seeking collateralized returns.

Finally, we also pointed out two issues that are not expected to have a substantial impact on the crypto market in 2026:

Quantum computing: We believe that research and preparation for post-quantum cryptography will continue to advance, but it is unlikely to have an impact on market valuations in the next year.

Digital Asset Vaults (DATs): Despite receiving considerable media attention, we believe they will not be a key variable influencing the digital asset market in 2026.

2026 Digital Asset Outlook: The Dawn of the Institutional Era

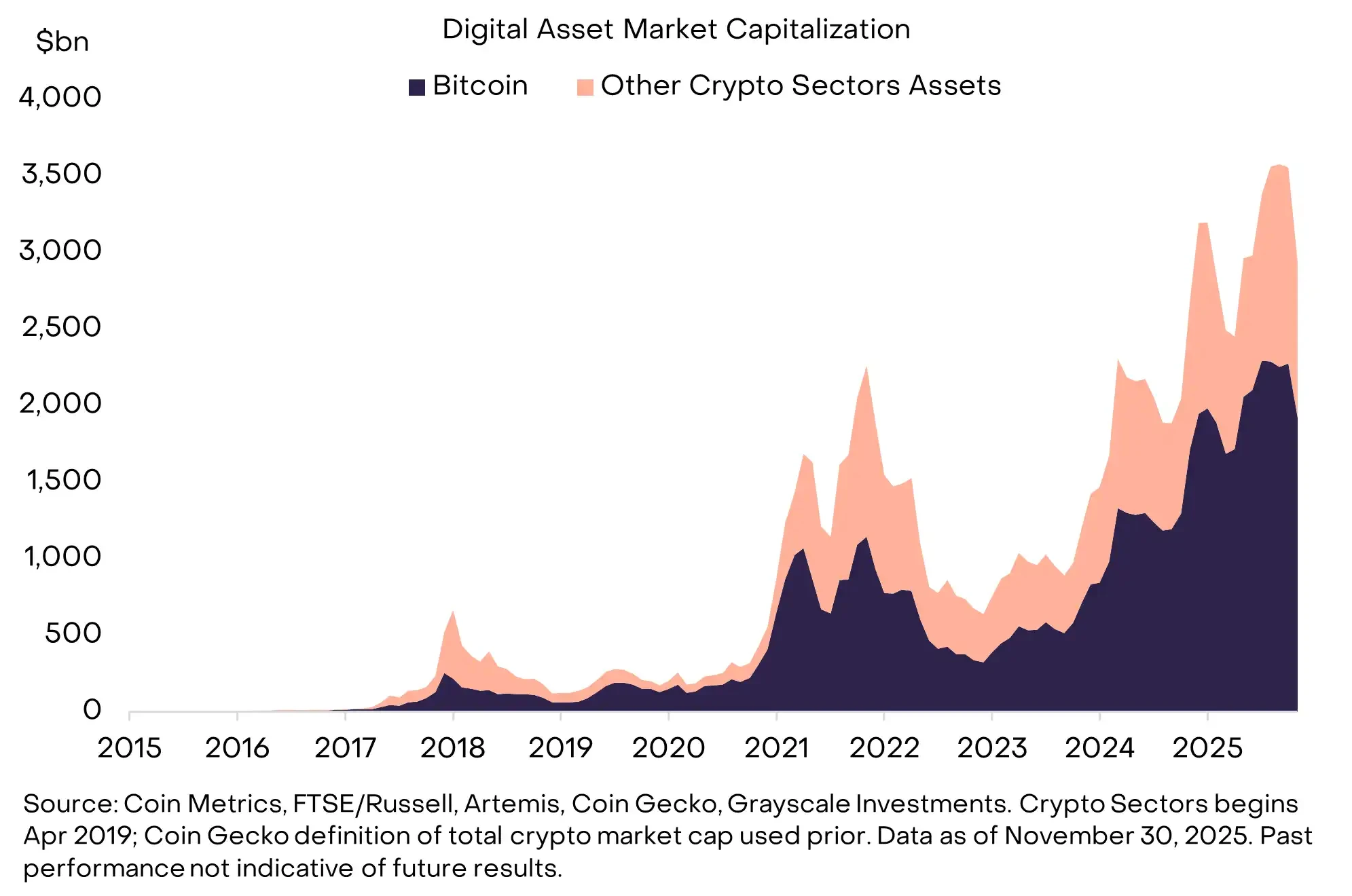

Fifteen years ago, cryptocurrency was still an experimental experiment: there was only one asset on the market, Bitcoin, with a market capitalization of about $1 million. Today, cryptocurrency has evolved into an emerging industry and grown into a mid-sized alternative asset class, consisting of millions of tokens with a total market capitalization of about $3 trillion (see Chart 1).

As major economies gradually establish more comprehensive regulatory frameworks, the integration of public blockchains with the traditional financial system is deepening, continuously attracting capital inflows for long-term allocation into this market.

Chart 1: Crypto assets have grown into a mid-sized alternative asset class.

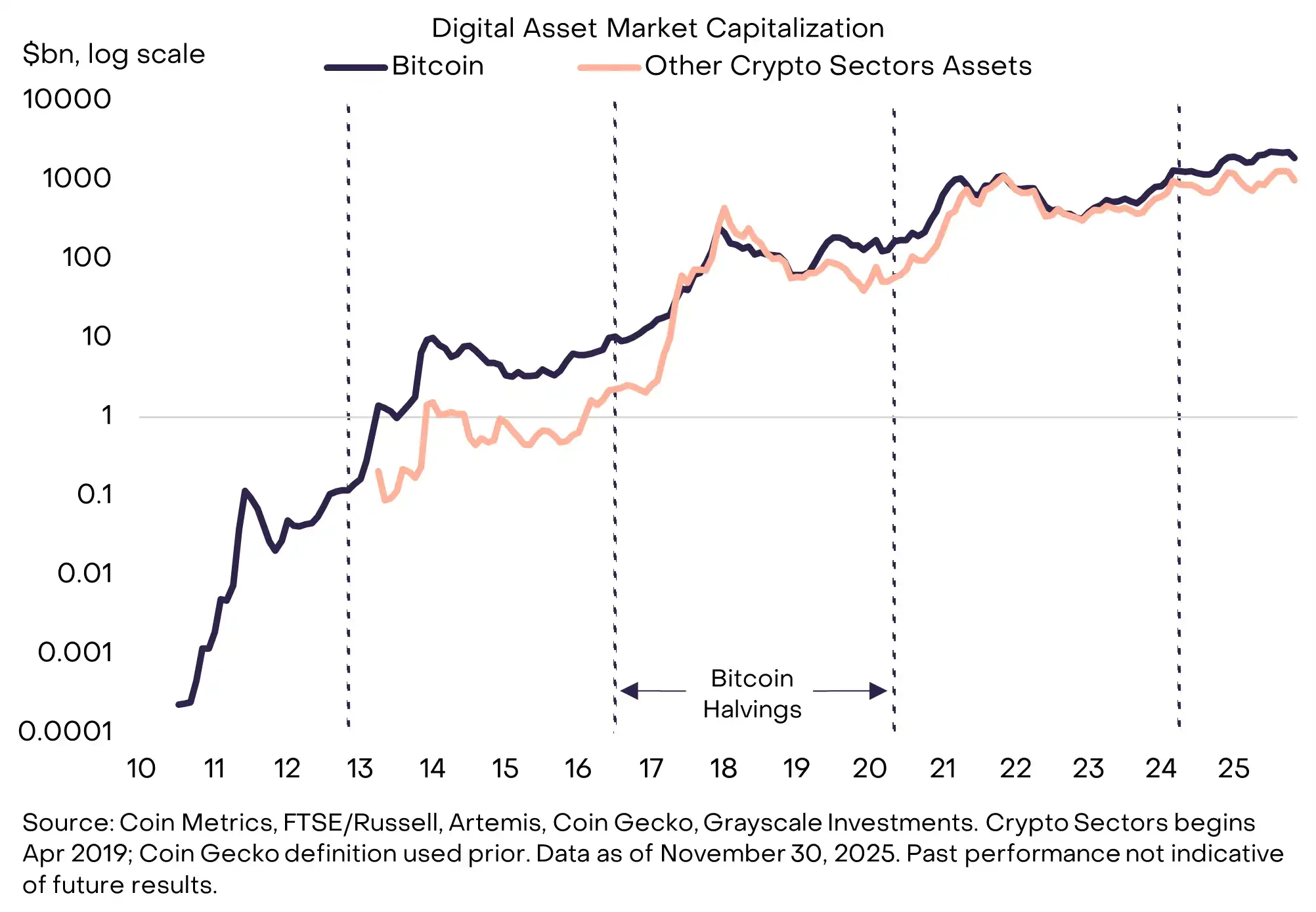

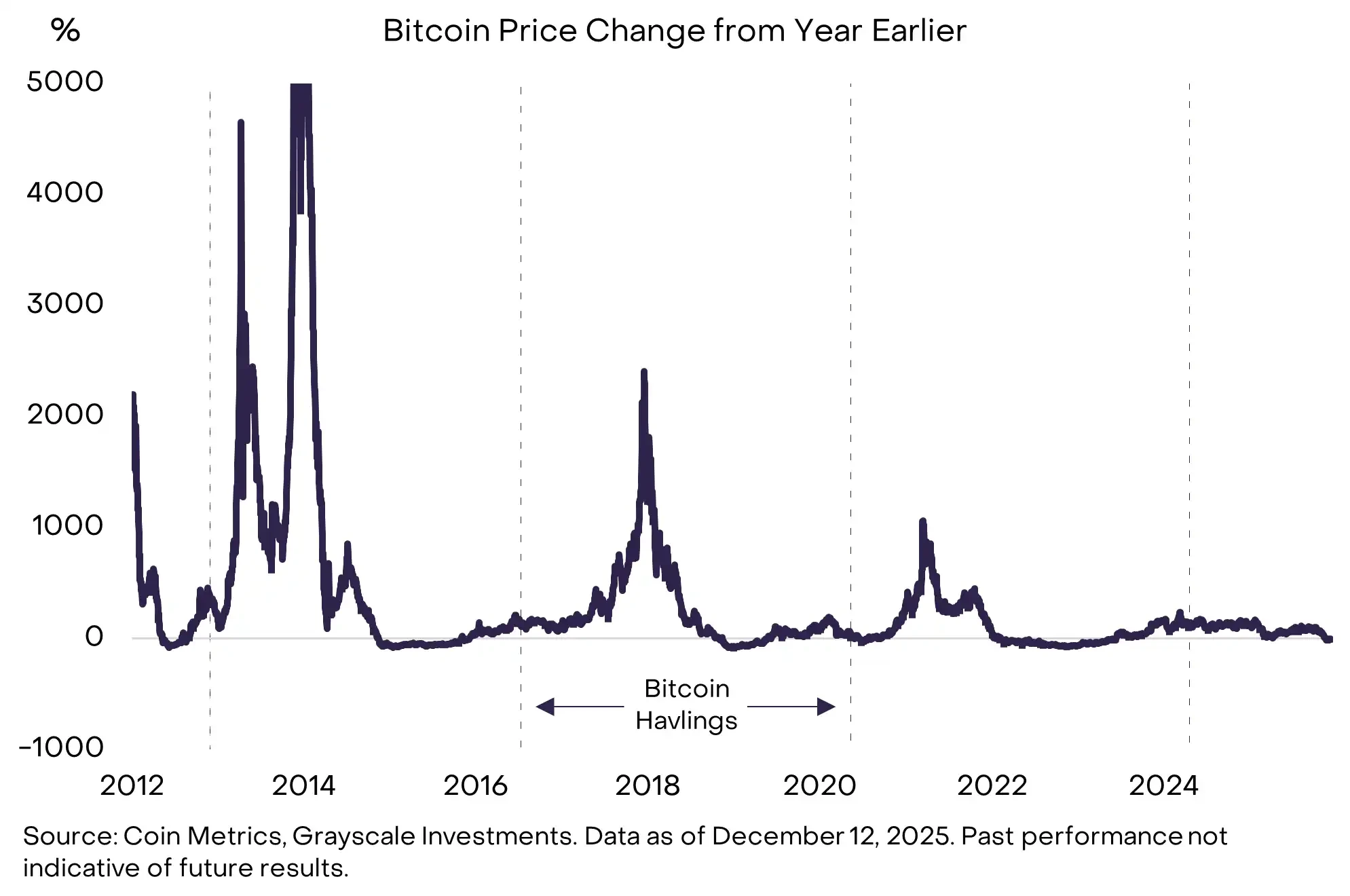

Throughout the development of crypto assets, token valuations have experienced four major cyclical pullbacks, roughly occurring every four years (see Chart 2). In three of these cases, the cyclical peaks in valuations occurred approximately 1 to 1.5 years after a Bitcoin halving event; and Bitcoin halvings themselves also occur on a four-year cycle.

This bull market has lasted for over three years, and the last Bitcoin halving occurred in April 2024, more than 1.5 years ago. Therefore, some market participants, based on traditional experience, believe that the price of Bitcoin may have peaked in October, and that 2026 will be a challenging year for returns on crypto assets.

Chart 2: The valuation upturn in 2026 will mark the end of the "four-year cycle" theory.

Grayscale believes the crypto asset class is in a sustained bull market, and 2026 will be a key turning point as the so-called "four-year cycle" comes to an end. We expect valuations across all six crypto asset sectors to rise in 2026, and predict that Bitcoin's price is likely to break its previous all-time high in the first half of the year.

Our optimism is based primarily on two core pillars:

First, at the macro level, the demand for alternative value storage tools will continue.

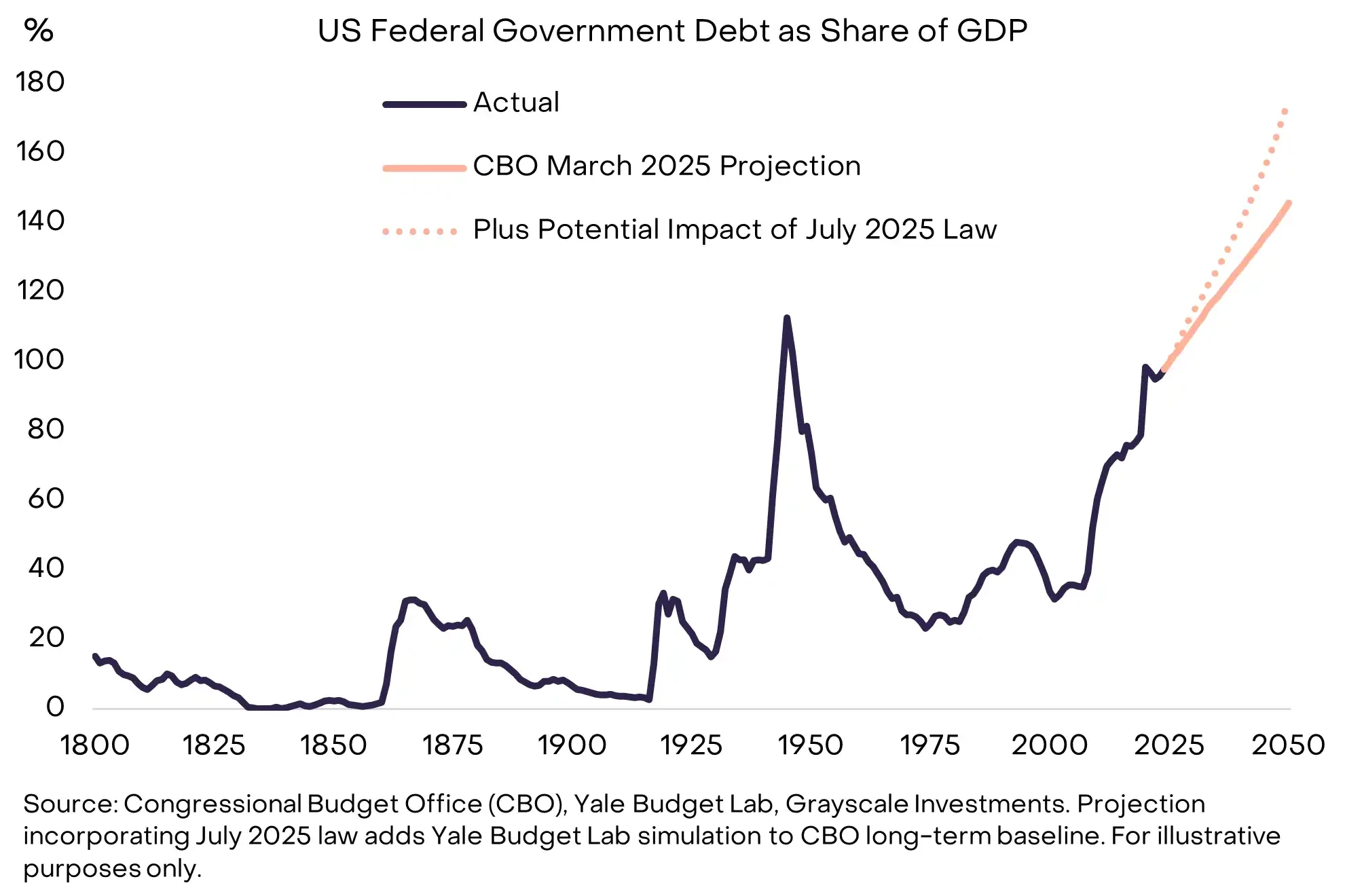

Bitcoin and Ethereum are currently the two largest crypto assets by market capitalization and can be considered scarce digital commodities and alternative monetary assets. Meanwhile, the fiat currency system (and assets denominated in fiat currency) faces additional risks, with high and rising public sector debt potentially putting pressure on inflation in the medium to long term (see Chart 3).

In this context, scarce commodities, whether physical gold and silver or digital Bitcoin and Ethereum, can serve as a "ballast" to hedge against fiat currency risk in investment portfolios. In our view, as long as the risk of fiat currency devaluation continues to rise, the demand for Bitcoin and Ethereum in investment portfolios is likely to increase accordingly.

Chart 3: The US debt problem undermines the credibility of low inflation expectations.

Second, greater regulatory clarity is driving institutional funding into the public blockchain space.

This point is easily overlooked, but until this year, the US government was still investigating and/or suing several leading crypto institutions, including Coinbase, Ripple, Binance, Robinhood, Consensys, Uniswap, and OpenSea. Even today, exchanges and other crypto intermediaries still lack clear and unified regulatory guidelines at the spot market level.

However, the situation is slowly but clearly shifting.

In 2023, Grayscale won a lawsuit against the U.S. Securities and Exchange Commission (SEC), paving the way for cryptocurrency spot exchange-traded products (ETPs).

In 2024, Bitcoin and Ethereum spot ETPs officially entered the market;

In 2025, the U.S. Congress passed the GENIUS Act, which targets stablecoins. Regulators also began to adjust their attitude towards the crypto industry, continuing to emphasize consumer protection and financial stability while collaborating with the industry to provide clearer regulatory guidance.

In 2026, Grayscale expects Congress to pass legislation on a crypto market structure with bipartisan consensus, which is expected to solidify the position of blockchain finance in the US capital market at the institutional level and further drive the continued inflow of institutional investment (see Chart 4).

Chart 4: Rising financing levels may reflect increasing institutional confidence.

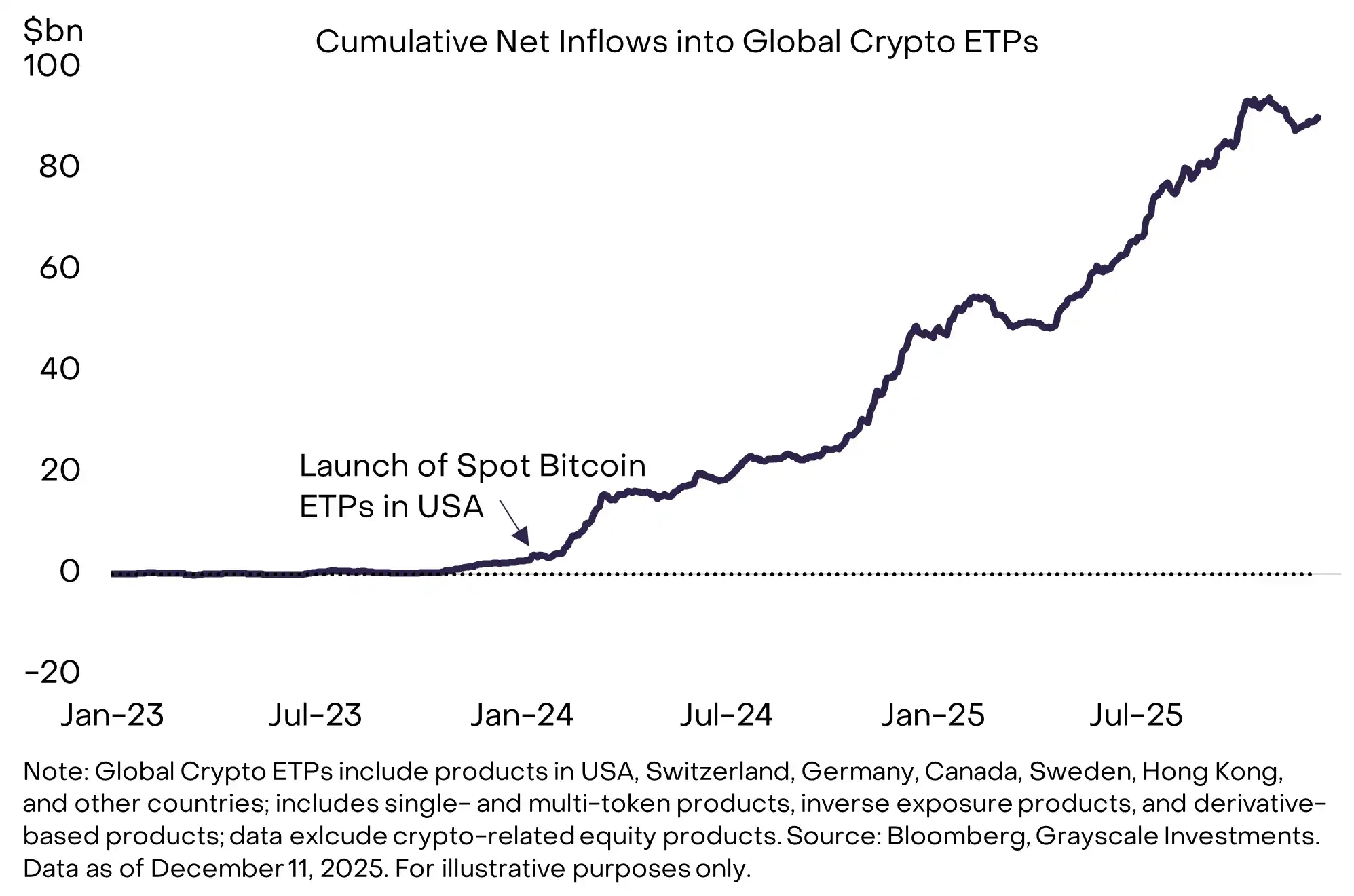

In our view, new funds entering the crypto ecosystem will primarily flow in through spot ETPs. Since the listing of Bitcoin spot ETPs in the US in January 2024, global crypto ETPs have recorded a cumulative net inflow of approximately $87 billion (see Chart 5).

Despite the significant success these products achieved upon their initial launch, the process of integrating crypto assets into mainstream investment portfolios is still in its early stages. Grayscale estimates that currently, less than 0.5% of wealth managed by trustees/advisors in the United States is allocated to crypto assets. This percentage is expected to continue to rise as more investment platforms complete due diligence, establish corresponding capital market assumptions, and incorporate crypto assets into their model portfolios.

Beyond wealth management channels, some pioneering institutions have already allocated crypto ETPs to their institutional portfolios, including Harvard Management Company and Mubadala (one of Abu Dhabi's sovereign wealth funds). We expect this list to expand significantly by 2026.

Chart 5: Crypto spot ETPs continue to attract net inflows of funds.

As the crypto market becomes increasingly driven by institutional inflows, price performance is changing. In every previous bull market, Bitcoin's price has risen by at least 1000% within a year (see Chart 6). In this cycle, the highest year-over-year increase is approximately 240% (annual range up to March 2024).

We believe this difference reflects more robust and sustained institutional buying recently, rather than the retail-driven, sentiment-driven rally of the past. While crypto asset investing still carries significant risks, at the time of writing this report, we judge the probability of a deep and prolonged cyclical pullback to be relatively low. Instead, driven by continued institutional inflows, prices are more likely to exhibit a more stable and gradual upward trend, potentially becoming the dominant trend next year.

Chart 6: Bitcoin prices did not experience a sharp surge during this cycle.

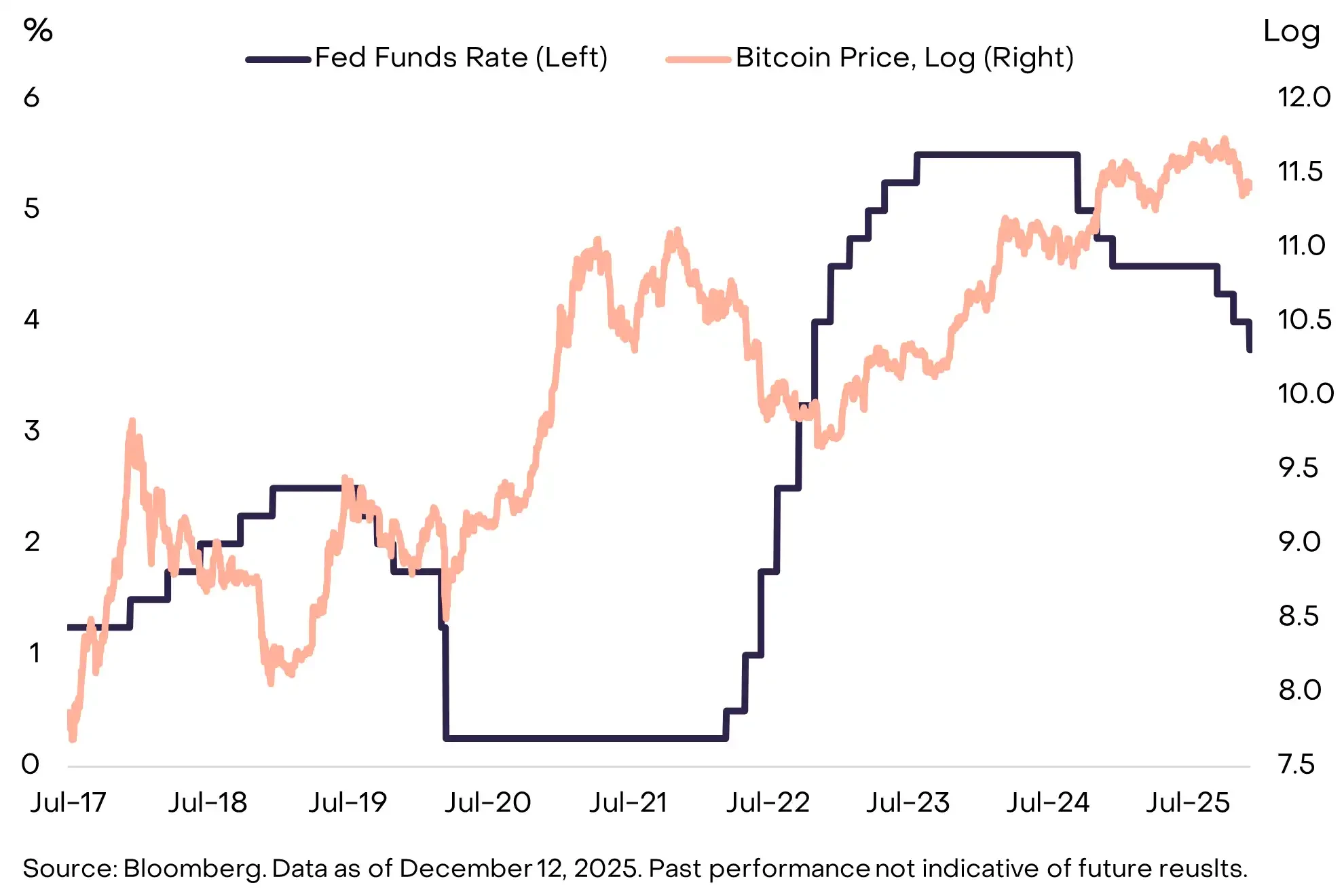

A relatively favorable macroeconomic environment may also provide some buffer against the downside risks to token prices in 2026.

Historically, the previous two cyclical peaks both occurred during periods of Federal Reserve interest rate hikes (see Chart 7). In contrast, the Fed has already cut rates three times by 2025 and is expected to continue lowering rates next year.

Kevin Hassett, who is considered a potential successor to Jerome Powell as Federal Reserve Chairman, recently stated on the show "Face the Nation": "The American people can expect President Trump to choose someone who can help them get cheaper car loans and more easily obtain mortgages at lower interest rates."

Overall, economic growth coupled with a relatively loose Federal Reserve policy environment typically helps to boost investors' risk appetite and creates potential upside for risk assets, including crypto assets.

Chart 7: Historically, cyclical peaks have often been accompanied by Federal Reserve interest rate hikes.

Like other asset classes, the price of crypto assets is driven by both fundamentals and capital flows. Commodity markets are cyclical, and crypto assets may also experience prolonged cyclical pullbacks in the future. However, we believe that such conditions will not be present in 2026.

From a fundamental perspective, supporting factors remain solid: the continued demand for alternative stores of value at the macro level, and the entry of institutional funds due to increased regulatory clarity, are laying a long-term foundation for public blockchain technology. Meanwhile, new funds continue to flow into the market. By the end of next year, crypto ETPs are likely to appear in more investment portfolios. This cycle has not seen a single, concentrated wave of retail investor funds; instead, there is a continuous and stable demand for crypto ETPs from various investment portfolios. In this generally favorable macroeconomic environment, we believe this is a key condition for the crypto asset class to reach new highs in 2026.

Top 10 Crypto Investment Themes for 2026

Crypto assets are a highly diversified asset class, reflecting the diverse application scenarios covered by public blockchain technology. The following section outlines Grayscale's assessment of the top ten most important crypto investment themes for 2026, with two additional "red herrings." Under each theme, we have listed the tokens that are most relevant from our perspective. For a classification of investable digital assets, please refer to our Crypto Sectors framework.

Theme 1: The risk of dollar depreciation drives demand for currency alternatives

Related crypto assets: BTC, ETH, ZEC

The US economy is facing structural debt problems (see Chart 3), which could put pressure on the dollar's status as a store of value in the medium to long term. Other countries face similar challenges, but because the dollar remains the most important international currency, the credibility of US policy is particularly crucial to potential cross-border capital flows.

In our view, only a small subset of digital assets are viable as stores of value, requiring a sufficiently broad adoption base, a highly decentralized network structure, and limited supply growth. The most typical examples are the two largest crypto assets by market capitalization—Bitcoin and Ethereum. Similar to physical gold, their value stems in part from their scarcity and autonomy.

The total supply of Bitcoin is permanently capped at 21 million, entirely determined by procedural rules. For example, we can be highly certain that the 20 millionth Bitcoin will be mined in March 2026. This transparent, predictable, and ultimately scarce digital currency system, while not inherently complex in concept, is gaining increasing appeal in the current environment of tail risks in the fiat currency system. As long as macroeconomic imbalances causing fiat currency risks continue to worsen, portfolio demand for alternative stores of value is likely to continue to rise (see Chart 8).

In addition, Zcash, as a smaller, more privacy-focused decentralized digital currency, may also be suitable for portfolio allocation to hedge against the risk of dollar depreciation (see Theme 5 for details).

Chart 8: Macroeconomic imbalances may drive up demand for alternative stores of value.

Theme 2: Increased Regulatory Clarity Supports Widespread Adoption of Digital Assets

Related crypto assets: almost all

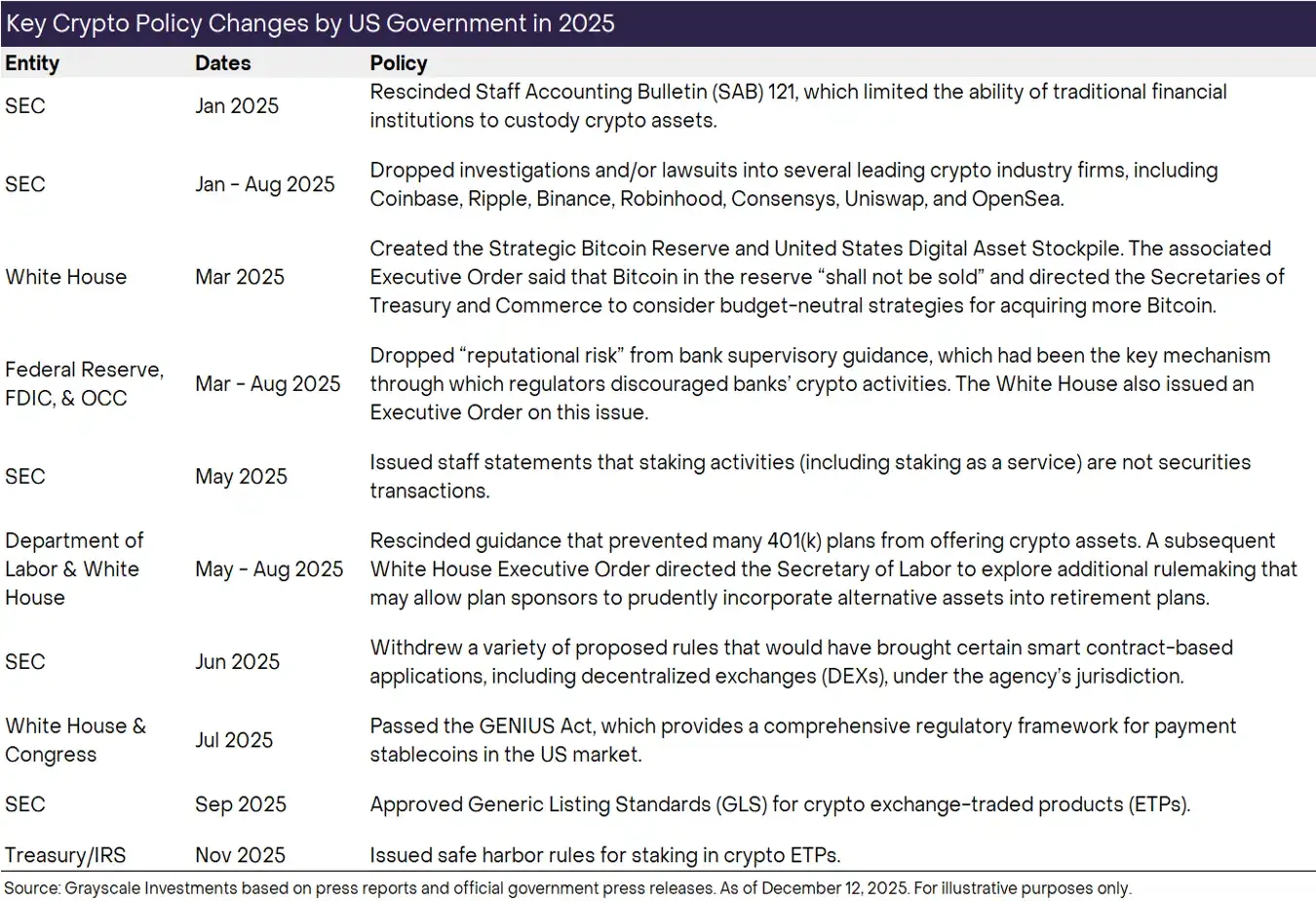

The United States took a key step toward clearer regulation of crypto in 2025, including: passing the GENIUS Act for stablecoins, rescinding the SEC’s 121 Employee Accounting Notice (SAB 121, which involves custody accounting), introducing a common listing standard applicable to crypto ETPs, and addressing access issues for the crypto industry within the traditional banking system (see Chart 9).

Looking ahead to 2026, we anticipate an even more decisive step – the passage of bipartisan legislation to structure the crypto market. The U.S. House of Representatives passed its version of the bill, the Clarity Act, in July, and the Senate subsequently initiated its own legislative process. While specific provisions still require further negotiation, the overall framework of this legislation will provide the crypto capital market with a set of rules benchmarked against traditional finance, covering registration and disclosure requirements, classification standards for crypto assets, and codes of conduct for insiders.

On a practical level, a more comprehensive regulatory framework gradually taking shape in the US and other major economies means that regulated financial service institutions may formally include digital assets on their balance sheets and begin trading on the blockchain. Simultaneously, this is expected to drive on-chain capital formation—both startups and established companies may issue compliant on-chain tokens. By further unleashing the potential of blockchain technology, regulatory clarity is expected to comprehensively raise the value center of the crypto asset class.

Given the potential importance of regulatory clarity in driving the development of crypto assets in 2026, we believe that significant disagreements or breakdowns between the two parties in Congress during the relevant legislative process should be considered a major downside risk.

Chart 9: The United States made significant progress in clarifying crypto regulations by 2025.

Theme 3: The Influence of Stablecoins Continues to Expand After the GENIUS Act Was Enacted

Related crypto assets: ETH, TRX, BNB, SOL, XPL, LINK

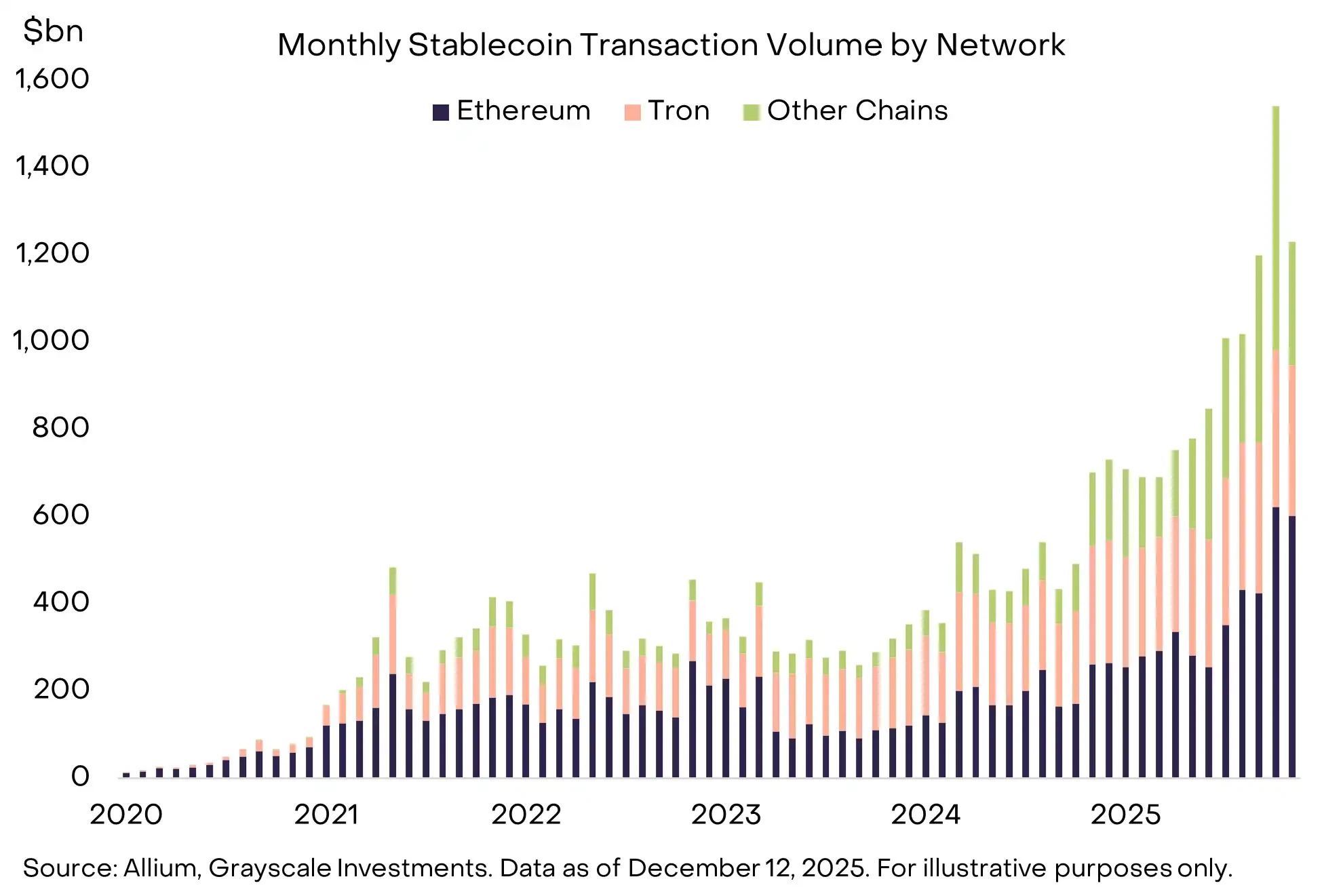

Stablecoins truly broke out of their niche in 2025: their circulating supply rose to approximately $300 billion, with an average monthly trading volume of approximately $1.1 trillion in the six months ending in November; at the same time, the U.S. Congress passed the GENIUS Act, and a large amount of institutional capital began to flow into this sector at an accelerated pace (see Chart 10).

Looking ahead to 2026, we anticipate these changes will translate into practical applications: stablecoins will be more widely embedded in cross-border payment services; used as collateral assets in derivatives exchanges; appear on corporate balance sheets; and become an alternative to credit cards in online consumer payments. Meanwhile, the continued growth of the prediction market may further fuel new demand for stablecoins.

The continued growth in stablecoin trading volume will directly benefit the blockchain networks that support these transactions (such as ETH, TRX, BNB, SOL, etc.), and will also drive the development of a series of supporting infrastructure (such as LINK) and decentralized finance (DeFi) applications (see Theme 7 for details).

Chart 10: Stablecoins are entering a critical period of explosive growth.

Theme 4: Asset Tokenization Reaches a Critical Turning Point

Related crypto assets: LINK, ETH, SOL, AVAX, BNB, CC

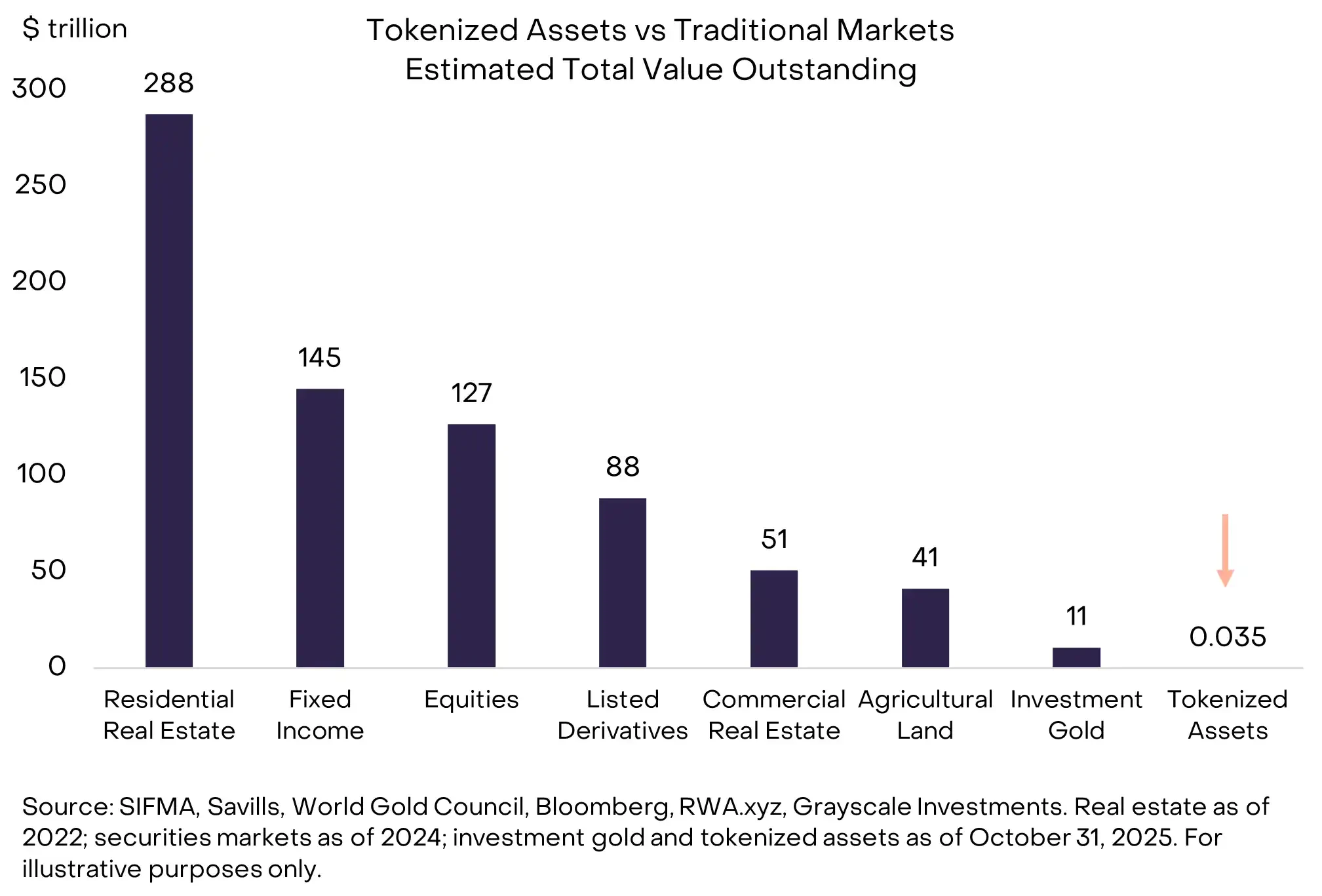

At present, tokenized assets remain negligible: they account for only about 0.01% of the total market capitalization of global stocks and bonds (see Chart 11). Grayscale expects asset tokenization to accelerate in the coming years as blockchain technology matures and regulatory clarity continues to improve.

In our view, it is not inconceivable that the scale of tokenized assets will grow by approximately 1,000 times by 2030. This expansion is likely to create significant value for blockchain networks that process tokenized asset transactions and various supporting applications.

Currently, the leading public blockchains in the tokenized asset field include Ethereum (ETH), BNB Chain (BNB), and Solana (SOL), but this landscape may change in the future. In terms of supporting applications, Chainlink (LINK) is considered to have a particularly strong competitive advantage due to its unique and comprehensive software technology portfolio.

Chart 11: Tokenized assets have huge growth potential.

Theme 5: Blockchain Goes Mainstream, Demand for Privacy Solutions Rises

Related crypto assets: ZEC, AZTEC, RAIL

Privacy is a fundamental component of the financial system. Most people assume that their salary, tax information, asset size, and spending habits should not be publicly displayed on public ledgers. However, most current blockchains are designed with high transparency by default. If public blockchains are to integrate more deeply into the financial system, they must be accompanied by more mature and robust privacy infrastructure—and this is becoming increasingly apparent as regulators push for the integration of blockchain with traditional finance.

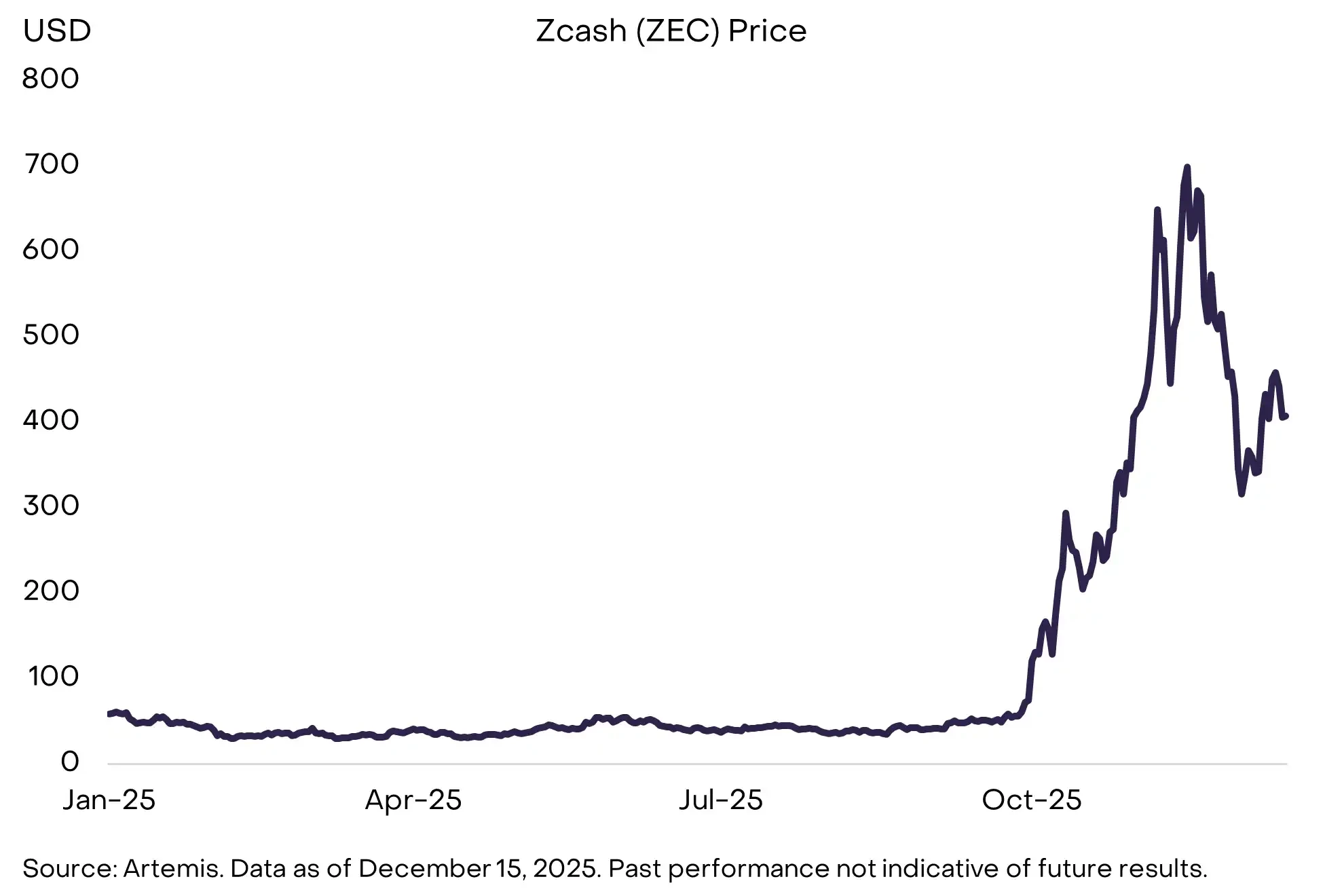

Amidst increased investor focus on privacy, one potential beneficiary is Zcash (ZEC): a decentralized cryptocurrency structurally similar to Bitcoin but with built-in privacy protections. Zcash saw a significant surge in Q4 2025 (see Chart 12). Other notable projects include Aztec (a privacy-focused Ethereum Layer 2 network) and Railgun (a privacy middleware for DeFi).

Furthermore, we may see mainstream smart contract platforms adopting "confidential transactions" mechanisms more widely, such as Ethereum's ERC-7984 standard and Solana's Confidential Transfers token extension. At the same time, the improvement of privacy tools may also force the DeFi sector to upgrade its identity verification and compliance infrastructure in tandem.

Chart 12: Crypto investors are increasingly focused on privacy features.

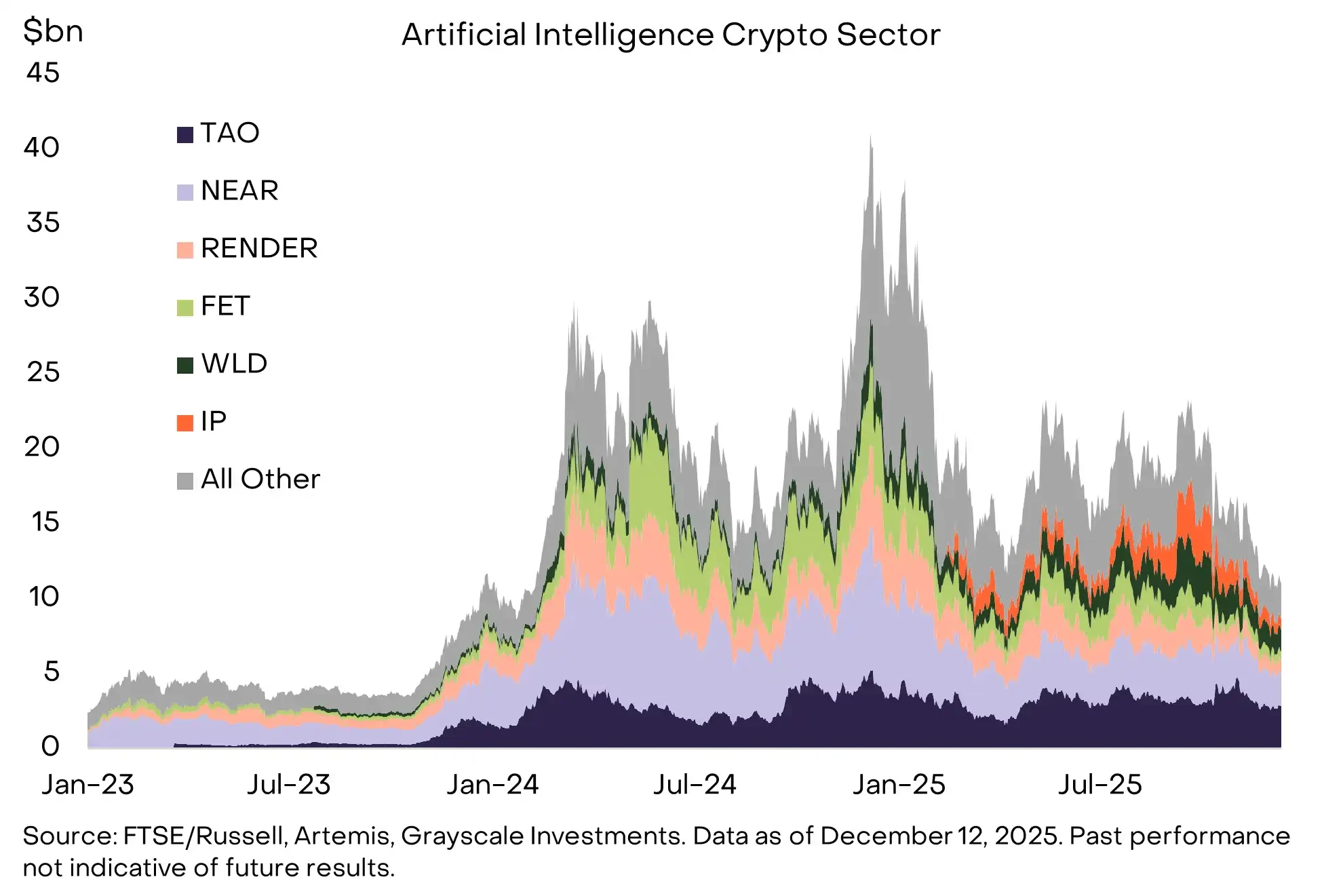

Theme Six: AI Moving Towards Centralization, Calling for Blockchain-Style Solutions

Related crypto assets: TAO, IP, NEAR, WORLD

The fundamental compatibility between encryption technology and artificial intelligence has never been clearer and stronger. Currently, AI systems are gradually concentrating in the hands of a few leading companies, raising a series of concerns about trust, bias, and ownership; encryption technology, on the other hand, provides a set of primitives that can directly address these risks.

For example, decentralized AI development platforms like Bittensor aim to reduce reliance on centralized AI technologies; World provides verifiable "Proof of Personhood" to distinguish real humans from intelligent agents in an environment rife with synthetic activity; and networks like Story Protocol offer transparent, traceable on-chain representations of intellectual property in an era where the sources of digital content are increasingly difficult to identify. Meanwhile, tools like X402, a zero-fee stablecoin payment open layer running on Base and Solana, provide the necessary low-cost, instant micropayment capabilities for economic interactions between intelligent agents or between machines and humans.

These elements collectively constitute the early infrastructure of the so-called "agent economy": in which identity, computing power, data, and payments must all be verifiable, programmable, and censorship-resistant. Although this ecosystem is still in its early stages and development is uneven, the intersection of cryptography and AI remains one of the most promising application areas in the industry in the long term. As AI becomes more decentralized, autonomous, and capable of economic behavior, protocols building real-world infrastructure are expected to be potential beneficiaries (see Chart 13).

Chart 13: Solutions to Some Key Risks Brought by AI by Blockchain

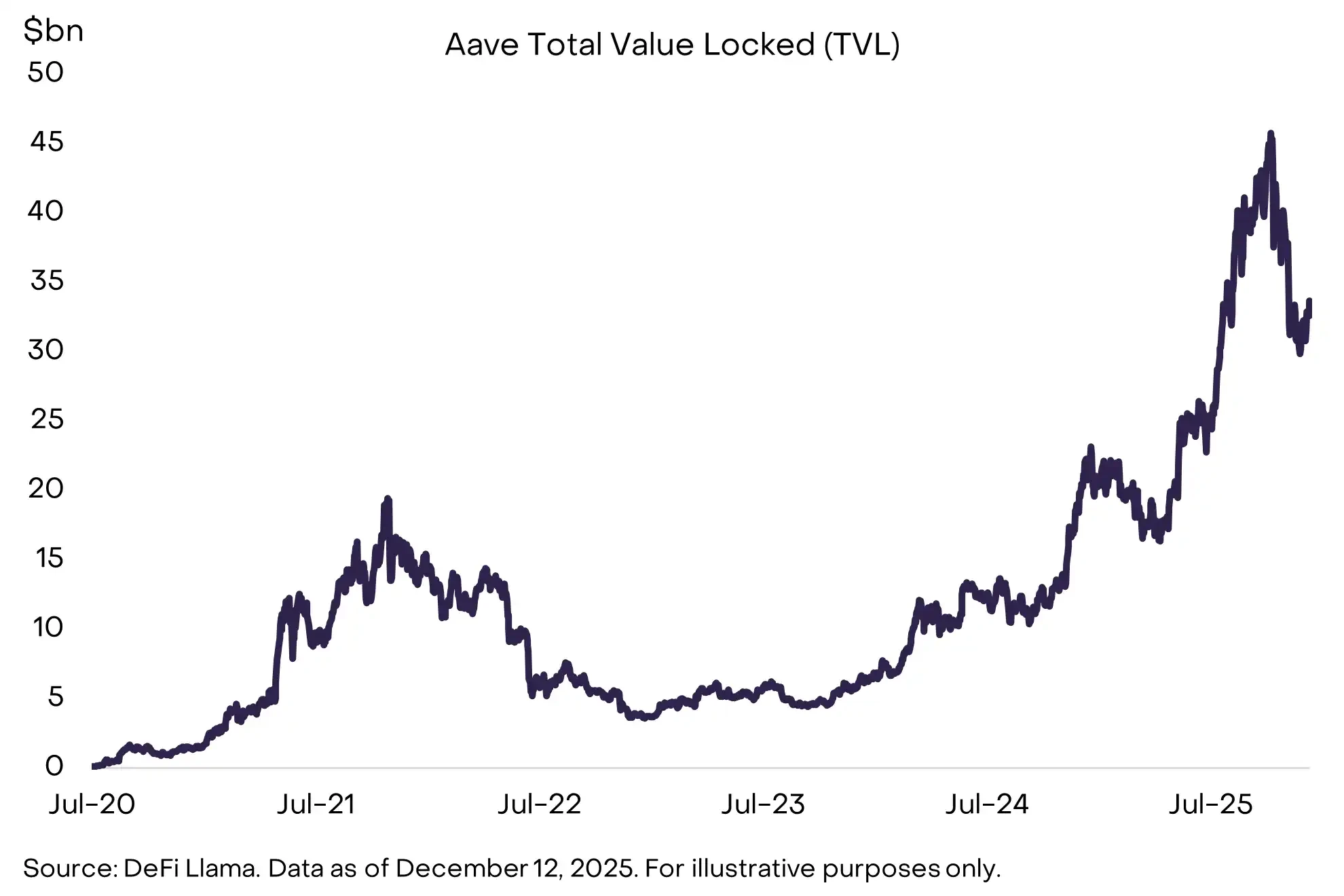

Theme 7: DeFi is accelerating its development, led by the lending sector.

Related crypto assets: AAVE, MORPHO, MAPLE, KMNO, UNI, AERO, RAY, JUP, HYPE, LINK

Driven by both increased technological maturity and a more favorable regulatory environment, DeFi applications accelerated significantly in 2025. The growth of stablecoins and tokenized assets was the most prominent success story, but at the same time, the DeFi lending sector also experienced substantial expansion, led by protocols such as Aave, Morpho, and Maple Finance (see Chart 14).

Meanwhile, decentralized perpetual contract exchanges (such as Hyperliquid) have been steadily approaching, and even rivaling, some large centralized derivatives exchanges in terms of metrics such as open interest and daily trading volume. Looking ahead, with improved liquidity, enhanced cross-protocol interoperability, and closer integration with the real-world price system, DeFi is gradually becoming a trusted alternative for users who wish to conduct financial activities directly on-chain.

We anticipate that more DeFi protocols will partner with traditional fintech companies to leverage their mature infrastructure and existing user base. In this process, core DeFi protocols are expected to continue to benefit—including lending platforms (such as AAVE), decentralized exchanges (such as UNI and HYPE), and related infrastructure protocols (such as LINK); simultaneously, public blockchains that host the majority of DeFi activity (such as ETH, SOL, and BASE) will also benefit.

Chart 14: DeFi continues to expand in scale and form, and its ecosystem is becoming increasingly diverse.

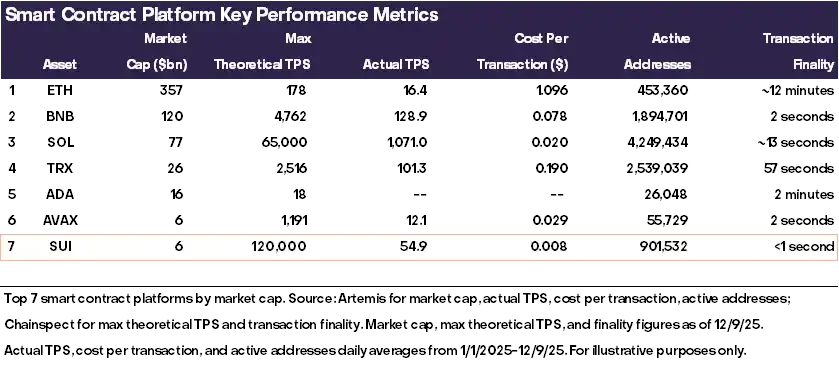

Theme 8: Mainstream Adoption Drives Upgrades to Next-Generation Infrastructure

Related crypto assets: SUI, MON, NEAR, MEGA

The next generation of blockchains is constantly pushing the boundaries of technology. However, some investors believe that more block space is not needed at present because the demand of existing public chains has not yet been fully met. Solana was once a typical example of this skepticism: as a public chain with extremely fast performance but limited usage, it was once regarded as having "excess block space" until the subsequent wave of applications arrived, and it grew into one of the most successful examples in the industry.

Not all current high-performance public blockchains will replicate Solana's path, but we believe a few projects are poised for breakthroughs. Superior technology doesn't necessarily guarantee adoption, but the architecture of these next-generation networks gives them a unique advantage in emerging application scenarios such as AI micropayments, real-time game loops, high-frequency on-chain transactions, and intent-based systems.

Within this tier, we expect Sui to stand out, with its strengths stemming from its clear technological leadership and highly integrated development strategy (see Chart 15). Other projects to watch include Monad (parallelized EVM architecture), MegaETH (ultra-fast Ethereum Layer 2 network), and Near (an AI-focused blockchain that has made progress on its Intents product).

Chart 15: Next-generation blockchains such as Sui enable faster and lower-cost transaction experiences.

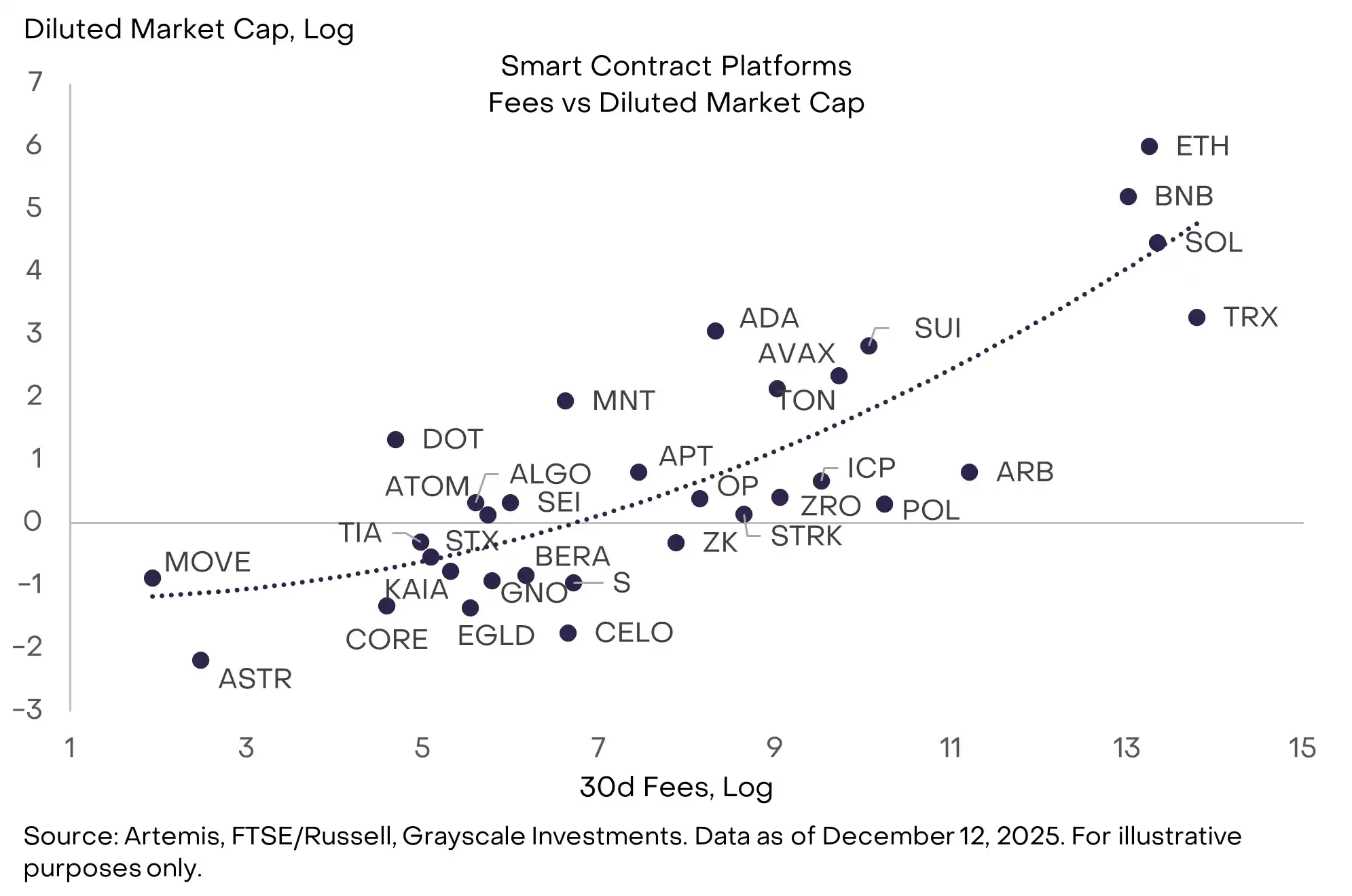

Theme Nine: A Greater Focus on Sustainable Income Capacity

Related crypto assets: SOL, ETH, BNB, HYPE, PUMP, TRX

Blockchain companies are not traditional businesses, but they do possess quantifiable fundamental metrics, including: number of users, number of transactions, transaction fees, locked-in capital (capital/TVL), developer scale, and application ecosystem. Among these metrics, Grayscale considers transaction fees to be the most valuable single fundamental metric because it is the most difficult to manipulate and has higher comparability across different blockchains (while also exhibiting the best empirical fit).

From the perspective of traditional corporate finance, transaction fees can be likened to "revenue." For blockchain applications, it's necessary to further distinguish between protocol-level fees/revenue and "supply-side" fees/revenue. As institutional investors begin systematically allocating to crypto assets, we expect them to pay more attention to blockchains and applications with higher or clearly defined fee revenue levels (excluding Bitcoin).

Currently, among smart contract platforms, those with relatively high transaction fee revenue include TRX, SOL, ETH, and BNB (see Chart 16); while among application layer assets, projects with high revenue performance include HYPE and PUMP.

Chart 16: Institutional investors may scrutinize the fundamental performance of blockchain more rigorously.

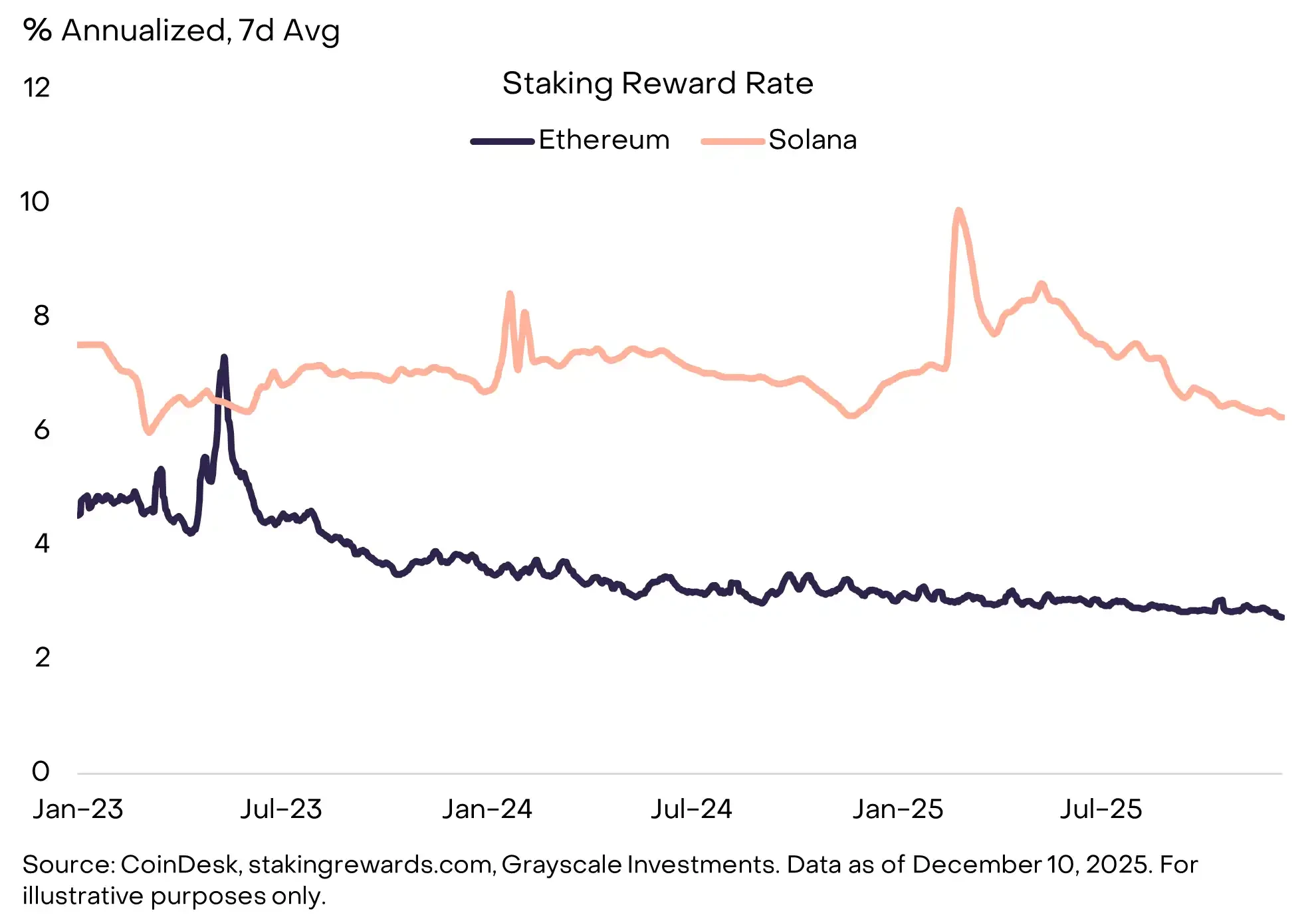

Topic 10: Investors will "default" to staking.

Related crypto assets: LDO, JTO

In 2025, US policymakers made two key adjustments to the staking mechanism, paving the way for more token holders to participate in staking activities:

(1) The U.S. Securities and Exchange Commission (SEC) has explicitly stated that liquidity staking does not constitute a securities transaction;

(2) The Internal Revenue Service (IRS) and the Treasury Department have confirmed that investment trusts and exchange-traded products (ETPs) can be used to pledge digital assets.

Regulatory guidelines surrounding liquidity staking services are expected to directly benefit Lido and Jito—the two leading liquidity staking protocols in the Ethereum and Solana ecosystems, respectively, based on TVL (Total Value Locked). From a broader perspective, the ability of crypto ETPs to participate in staking is likely to make "staking as the default holding method" the standard structure for Proof-of-Stake (PoS) token investment, thereby increasing the overall staking ratio and putting downward pressure on staking returns (see Chart 17).

In an environment where staking is more widely adopted, custodial staking via ETPs will provide investors with a convenient way to obtain staking rewards; while on-chain, non-custodial liquidity staking has unique advantages in terms of composability within the DeFi ecosystem. We expect this dual-track structure to persist for quite some time.

Chart 17: Proof-of-Stake (PoS) tokens inherently possess a staking reward mechanism

"Distractors" for 2026 (Red Herrings)

We anticipate that all of the aforementioned investment themes will have a real impact on the development of the crypto market in 2026. However, there are two topics that, despite much discussion, we do not believe will substantially influence the crypto market's trajectory next year: the potential threat of quantum computing to cryptography, and the evolution of digital asset vault companies (DATs). The market will devote considerable attention to these two issues, but in our view, they are not the core variables determining the market's outlook.

On quantum computing

If advancements in quantum computing continue, most blockchains will eventually need to upgrade their cryptographic systems. Theoretically, a sufficiently powerful quantum computer could deduce private keys from public keys, thereby generating valid digital signatures and transferring user assets. Therefore, Bitcoin, and the vast majority of blockchains, and indeed the entire cryptographic-dependent modern economic system, will need to transition to post-quantum cryptographic tools in the long term. However, experts generally believe that a quantum computer capable of breaking Bitcoin's cryptography is unlikely to emerge until at least 2030. We anticipate an acceleration in research and community preparations surrounding quantum risks in 2026, but this topic is unlikely to have a substantial impact on prices in the short term.

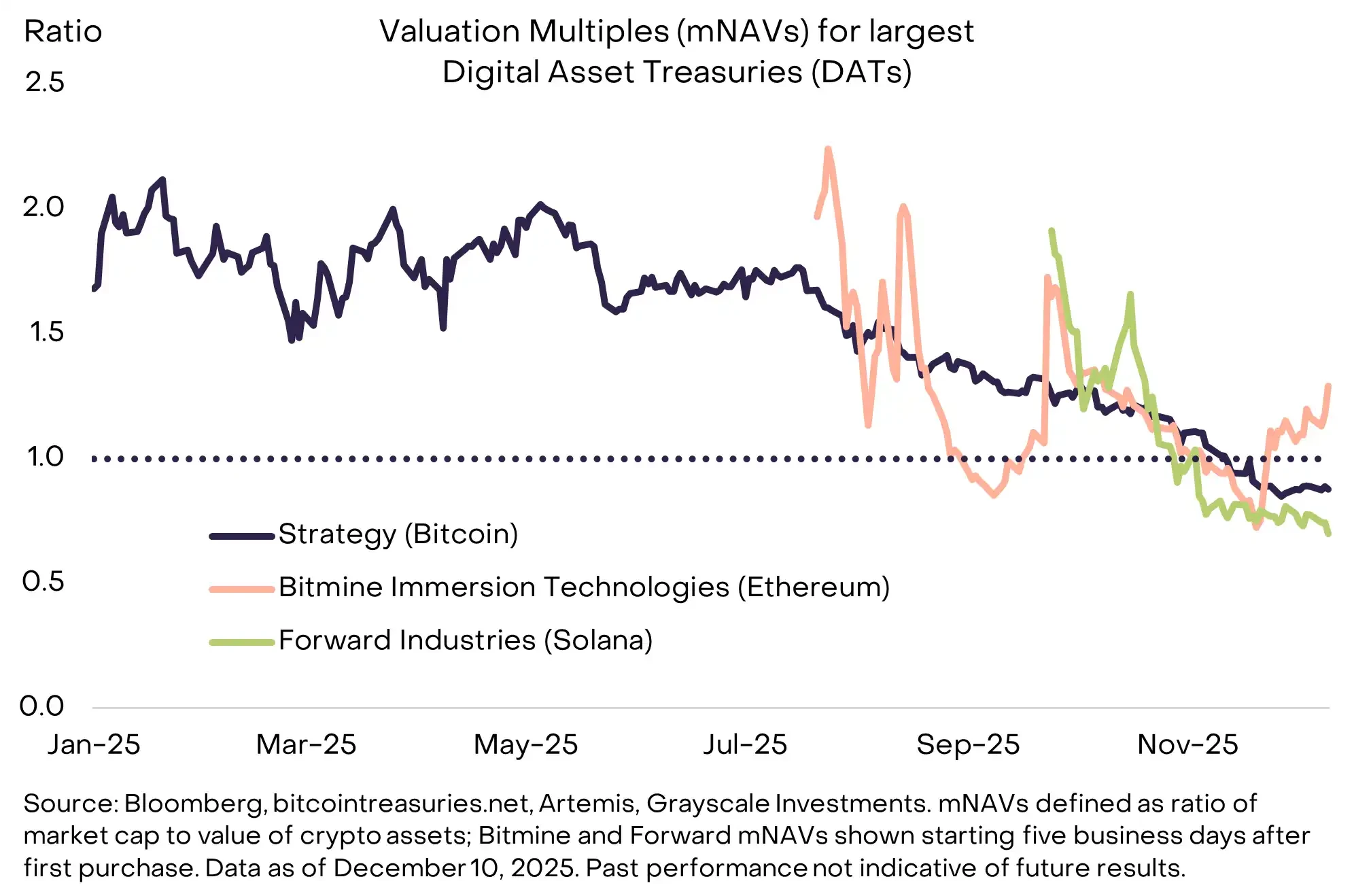

About Digital Asset Vaults (DATs)

The strategy of "incorporating digital assets into corporate balance sheets," pioneered by Michael Saylor, spawned dozens of imitators in 2025. According to our estimates, DATs currently hold 3.7% of Bitcoin's total supply, 4.6% of Ethereum's, and 2.5% of Solana's. However, since its peak in mid-2025, market demand for these instruments has cooled: the largest DATs currently have a mNAV (market capitalization/net asset value) that has fallen back to near 1.0 (see Chart 18).

It's worth noting that most DATs do not employ excessive leverage (or even any leverage at all), making them unlikely to be forced to sell assets during market downturns. Strategy, the largest DAT by market capitalization, recently established a dollar reserve fund to ensure continued payments of its preferred stock dividends even if Bitcoin prices fall. We expect most DATs to behave more like closed-end funds: trading within a range of net asset value fluctuations, occasionally experiencing premiums or discounts, but rarely actively liquidating assets.

Overall, these tools are likely to become a long-term component of the crypto investment landscape, but in our view, they are unlikely to be a major source of new token demand in 2026, nor are they likely to constitute a significant source of selling pressure.

Chart 18: The DAT premium has converged significantly, but the likelihood of a large-scale asset sale is low.

in conclusion

We hold a positive outlook for digital assets in 2026, supported by two key forces: continued macroeconomic demand for alternative stores of value and increasing regulatory clarity. A key theme for next year is likely to be the deepening connection between blockchain finance and traditional finance, and the continued inflow of institutional capital. Tokens adopted by institutions often possess clear application scenarios, sustainable revenue models, and access to compliant exchanges and application systems. Investors can also expect to see a continued expansion of the range of crypto assets available for investment through ETPs, with staking mechanisms enabled by default where conditions permit.

At the same time, the process of regulatory clarification and institutionalization will raise the bar for mainstream success. For example, crypto projects seeking listing on regulated exchanges may need to meet new registration and disclosure requirements. Institutional investors are also more likely to overlook crypto assets lacking clear use cases—even if these assets currently have relatively high market capitalizations. The GENIUS Act legally distinguishes between regulated payment stablecoins (which enjoy corresponding rights and obligations under US law) and other stablecoins (which do not have equal rights). Similarly, we expect that the institutional era for crypto assets will further widen the gap between assets that can access compliant channels and institutional capital and those that cannot obtain equal access.

The crypto industry is entering a new phase, and not every token can successfully transition from the old era to the new.