Profit traps faced by crypto internet banks

- 核心观点:加密银行正重蹈传统互联网银行覆辙。

- 关键要素:

- 收入过度依赖微薄交换费。

- 缺乏核心借贷业务致资本闲置。

- 高昂获客成本挤压利润空间。

- 市场影响:推动行业向嵌入式DeFi转型。

- 时效性标注:中期影响

Original title: Replaying the Neobank Mistake in Crypto or Rebuilding It Right?

Original author: @0xcoconutt

Original translation: SpecialistXBT, BlockBeats

Editor's Note: This article serves as a sobering reminder of the current booming "crypto banking" sector. The author astutely points out that the vast majority of "traditional internet banks" have failed to achieve profitability because they rely excessively on meager exchange fees and lack core lending businesses, ultimately becoming expensive "deposit warehouses." Now, most new crypto banks seem to be blindly repeating this mistake, using high incentives to acquire unprofitable deposits.

Did you know that less than 5% of internet banks (Neobank) are profitable?

Internet banks make enticing claims: fully digital banking services, lower fees, and a better user experience. However, it turns out that these digital banks have fundamental flaws in their economic model.

This article will delve into why many traditional internet banks struggle to turn a profit, and why encrypted internet banks are following suit.

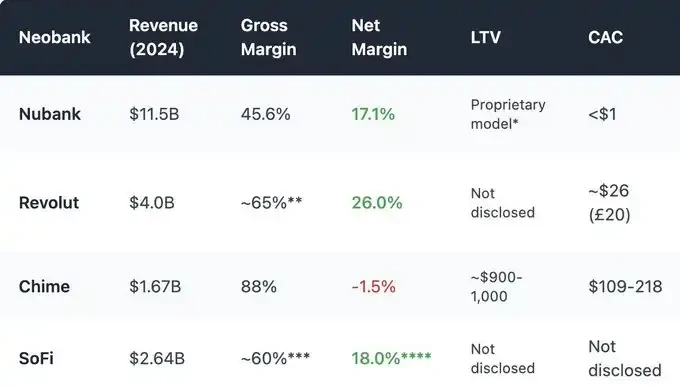

Image source: @ashwathbk (https://x.com/ashwathbk/status/1975899128745054710)

Image source: @ashwathbk (https://x.com/ashwathbk/status/1975899128745054710)

Business models over-rely on exchange fees

The vast majority of internet banks' revenue relies on "exchange fees," which are the small percentage that banks earn each time a user swipes their debit card.

This model is only effective under economies of scale, and only if profit margins are maintained and total consumption is high enough. However, in practice, this economic model often results in meager profits and is extremely fragile.

Take Chime, the US-based internet bank, as an example. It doesn't have its own banking license and relies on partner banks to hold deposits and issue cards—a mechanism very similar to that of crypto internet banks. Its business model is highly focused on bank card transactions. In 2024, approximately 80% of its total revenue came from exchange fees.

However, regulators in many regions have already capped exchange rates:

EU: 0.2% per transaction

United States (Durbin Amendment): Approximately $0.21 + 0.05% per transaction.

Chime utilizes small partner banks to charge up to approximately $0.44 per transaction.

However, this kind of "regulatory arbitrage" is facing increasing pressure, and for internet banks, the profit margin from exchange fees alone is already meager, making it difficult to support a sustainable business model.

Furthermore, exchange fee revenue is highly sensitive to consumer spending cycles. During economic downturns, if people reduce credit card spending, internet banks' revenue will decline accordingly.

Capital idle: No borrowing, no interest income

The core revenue of banking operations comes from loan interest, not payments.

Traditional banks convert deposits into loans, earning interest through mortgages, lines of credit, and business financing.

Even those internet banks that possess banking licenses have largely failed to establish this core function.

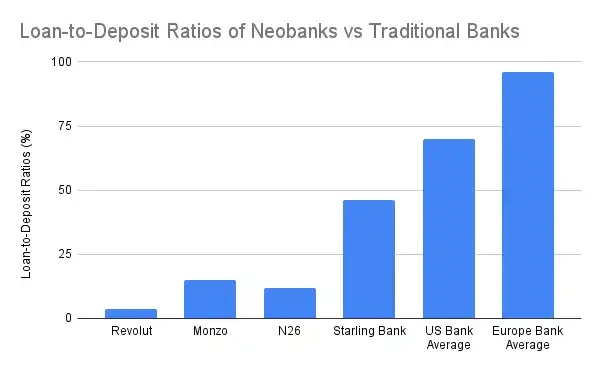

Traditional banks derive 60-65% of their revenue from net interest income, with loan-to-deposit ratios reaching 55-65%, and even higher on average globally. However, most internet banks lag far behind in this primary revenue stream, with the sole exception of Starling Bank, which acquired a mortgage portfolio.

Crypto internet banks operating under a self-custodial model lack the ability to earn interest income from deposits. They cannot use users' funds to generate returns. At best, they merely "direct" deposits to DeFi protocols like Aave or Lido, taking a small cut of the returns as commission. However, this integration offers neither risk underwriting nor genuine control over funds, and it introduces its own unique risks, such as protocol hacking and stablecoin de-pegging.

Whether in traditional fintech or cryptocurrency-based models, the same paradox is repeating itself: deposits pile up, yet they cannot be monetized.

Essentially, many internet banks (including crypto internet banks) are just expensive "deposit warehouses".

High customer acquisition and maintenance costs

Traditional banks have historically achieved organic growth through their branch networks, while internet banks must compete for each customer in a crowded digital market through marketing and referrals. This results in extremely high customer acquisition costs, severely squeezing their profit margins.

Due to higher barriers to entry and the required user education costs, customer acquisition costs for crypto internet banks are only going to be higher. Not to mention, most of them also use high annualized returns and token incentives to attract user deposits. This constitutes a "deferred liability" that the company needs to repay, significantly increasing customer acquisition costs.

Crypto internet banks have an even worse cost-to-income ratio than traditional internet banks:

Stablecoin-based payments have squeezed profit margins in foreign exchange and exchange fees, leading to a "race to the bottom" in increasingly fierce competition.

Regulatory obligations (even with a self-custodial model) require KYC, deposit and withdrawal controls, and bank card compliance. If fraudulent transactions are detected, the crypto internet bank will be responsible for cancellations and penalties. They may even face the risk of having their services suspended by centralized card issuers.

Most users are retail investors with low balances (deposits < $1,000), while the costs of customer support, anti-fraud, and infrastructure are fixed.

Rebuilding Business Models: Winning Through Embedded DeFi

Given their self-custodial nature, crypto internet banks operate on entirely different business foundations and cannot succeed by simply imitating Chime or Monzo. I don't believe crypto internet banks have any advantage over traditional internet banks, but I do think crypto technology can help internet banks improve profitability through "embedded DeFi."

Trading is the main source of income

Transaction revenue has become a proven way for traditional internet banks and crypto wallets to drive high-profit income.

Revolut Wealth (including crypto business, 2024): Revenue of £506 million (16.3% of total revenue), a year-on-year increase of 298%, primarily driven by customers’ cryptocurrency speculation rather than traditional banking business.

Phantom Wallet (projected for 2025): $79 million in profits from in-wallet token trading.

Embedded trading functionality has become an industry standard. To stand out and ensure the best trading experience for users, applications need to offer a wide range of asset classes, trading pairs, MEV (Maximum Extractable Value) protection, fast execution, and other features.

Structured returns and on-chain financial products

Internet banks don't need to lend money directly; instead, they can package complex DeFi products into financial products that are easy for retail investors to understand and invest in.

They issue their own stablecoin and earn yields on the underlying U.S. Treasury bonds (T-bills) by encouraging users to redeem it.

A well-planned profit-sharing vault and savings agreements for retail investors

On-chain ETFs / Real-world Assets (RWA)

Insurance

I haven't seen many Western internet banks replicate the success of Alipay's wealth management product suite.

Screenshot of Alipay wealth management product interface

Screenshot of Alipay wealth management product interface

Crypto internet banks have an advantage in offering a wide range of wealth management products; they can simplify DeFi and make high-yield financial products more accessible to a broader audience.

Embedded DeFi can greatly enrich the wealth management product lines of internet banks.

Building a DeFi "track," not recreating banks.

Internet banks have always had thin profit margins. Crypto internet banks, despite having native DeFi tools, face even greater challenges: lower fees from stablecoin payments, higher compliance costs, more difficult onboarding, and fierce competition once traditional internet banks also "embrace crypto."

As Revolut and Nubank begin offering stablecoin and cryptocurrency trading and on-chain yields on top of their existing infrastructure, "crypto-first" internet banks will find it difficult to compete with them in terms of user mindshare.

The real key to success lies not in reinventing an internet bank, but in providing the "track": developing yield routers, stablecoin FX layers, DeFi wrappers, or curated protocols that can be plugged into existing bank distribution channels. We may struggle to compete with internet banks that have already amassed massive user bases, but we should strive to leverage cryptography to complement and enhance their profitability.