The Curve team is starting a new business. Will Yield Basis become the next phenomenal DeFi application?

- 核心观点:YieldBasis通过杠杆和再平衡消除无常损失。

- 关键要素:

- 使用闪电贷构建2倍杠杆头寸。

- 自动再平衡维持50%债务比率。

- 费用分配激励用户和治理参与。

- 市场影响:提升流动性提供者收益,推动DeFi创新。

- 时效性标注:中期影响

Original author: Saint

Original translation: AididiaoJP, Foresight News

Every once in a while, a DeFi hit product appears in the crypto market.

Pumpfun makes token issuance easy, while Kaito revolutionizes content distribution.

Now, YieldBasis will redefine how liquidity providers profit: by converting volatility into yield and eliminating impermanent loss.

In this article, we’ll explore the basics, explain how YieldBasis works, and highlight related investment opportunities.

Overview

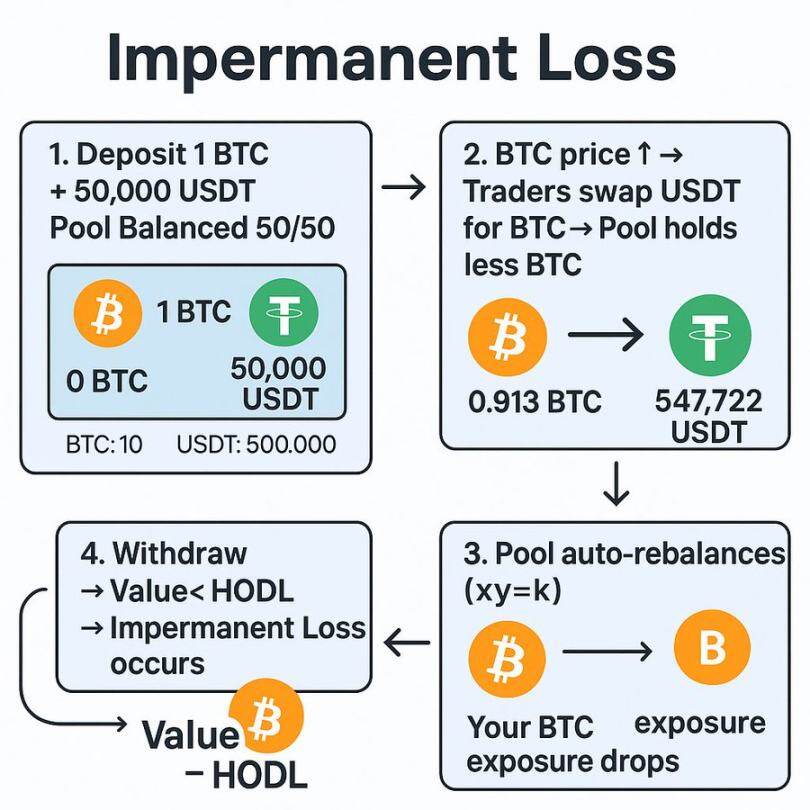

If you’ve ever provided liquidity to a dual-asset pool, you’ve likely experienced impermanent loss firsthand.

But for those of you who are not familiar with the concept, a quick recap:

Impermanent loss is a temporary loss of value that occurs when liquidity is provided to a pool of two assets.

As users trade between these assets, the pool automatically rebalances, which typically results in liquidity providers holding more of the asset being sold.

For example, in a BTC/USDT pool, if the price of BTC rises, traders will sell BTC to the pool for profit, and liquidity providers will end up holding more USDT and less BTC.

When withdrawing funds, the total value of the position is usually lower than if you simply held BTC.

As early as 2021, high annualized percentage yields and liquidity incentives were more than enough to offset this.

But as DeFi matures, impermanent loss becomes a real flaw.

Various protocols have introduced fixes such as pooled liquidity, delta-neutral liquidity providers, and unilateral pools, but each approach has its own trade-offs.

YieldBasis takes a new approach that aims to make liquidity provision profitable again by capturing yield from volatility while completely eliminating impermanent loss.

What is YieldBasis?

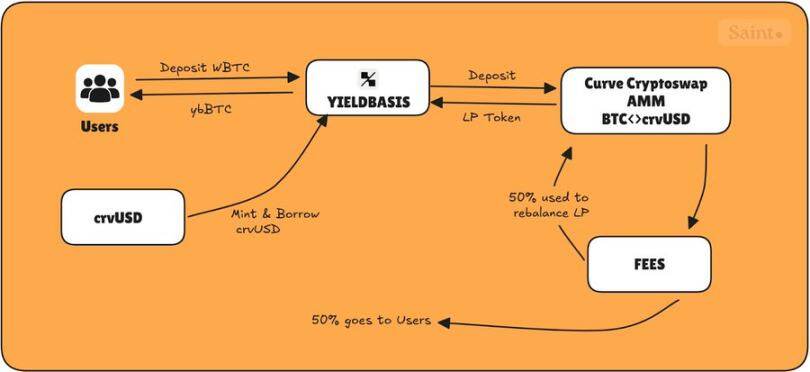

Simply put, YieldBasis is a platform built on Curve that uses Curve pools to generate yield from price fluctuations while protecting liquidity provider positions from impermanent loss.

At launch, Bitcoin was the primary asset. Users deposited BTC into YieldBasis, which allocated it to Curve’s BTC pool and applied leverage using a unique on-chain structure, thereby mitigating impermanent loss.

Founded by the same team behind Curve, including @newmichwill.

YieldBasis has achieved significant milestones:

• Raised over $50 million from top founders and investors

• Recorded over $150 million in commitments in the Legion sale

• Filled its BTC pool within minutes of launch

So, how does this mechanism actually work?

Understanding the YieldBasis Workflow

YieldBasis operates through a three-step process designed to maintain a 2x leveraged position while protecting liquidity providers from downside risk.

Deposit

The first step for users is to deposit BTC into YieldBasis to mint ybBTC, a receipt token representing their share of the pool. Currently supported assets include cbBTC, tBTC, and WBTC.

Flash Loans and Leverage Settings

The protocol flash loans crvUSD equal to the USD value of the deposited BTC.

BTC and borrowed crvUSD are paired and provided as liquidity to the BTC/crvUSD Curve pool.

The resulting LP tokens are deposited as collateral into a Curve CDP (collateralized debt position) to obtain another crvUSD loan, which is used to repay the flash loan, making the position fully leveraged.

This creates a 2x leveraged position with a constant 50% debt ratio.

Leverage Rebalancing

As the BTC price fluctuates, the system automatically rebalances to maintain a 50% debt-to-equity ratio:

- If BTC rises: LP value increases → protocol borrows more crvUSD → exposure reset to 2x

- If BTC falls: LP value drops → Redeem some LP → Repay debt → Ratio returns to 50%

This keeps your BTC exposure constant, so you won’t lose BTC even if the price fluctuates.

Rebalancing is handled by two key components: the rebalancing automated market maker and the virtual liquidity pool.

The rebalancing automated market maker tracks LP tokens and crvUSD debt, adjusting prices to encourage arbitrageurs to restore equilibrium.

At the same time, the virtual funding pool packages all steps of flash loan, LP token minting/destruction and CDP repayment into a single atomic transaction.

This mechanism prevents liquidation events by keeping leverage stable while giving arbitrageurs a small profit incentive to maintain equilibrium.

The result is a self-balancing system that continuously hedges against impermanent loss.

Fees and Token Distribution

YieldBasis has four main tokens that define its incentive system:

- ybBTC: Claim rights on 2x leveraged BTC/crvUSD LP

- Staked ybBTC: A staking version that earns token emissions

- YB: Native protocol token

- veYB: YB locked by voting, granting governance rights and enhancement rewards

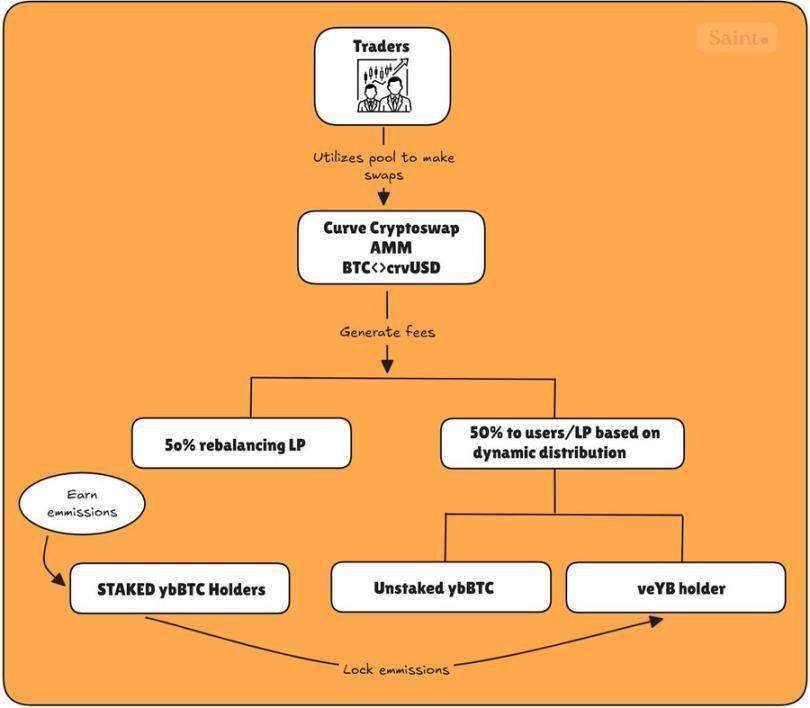

All transaction fees generated from the BTC/crvUSD pool are divided equally:

- 50% goes to users (shared between unstaked ybBTC and veYB holders)

- 50% returns to the protocol to fund the rebalancing mechanism

Returning 50% of the rebalancing pool ensures that no liquidation calls occur due to a lack of arbitrageurs to balance the pool; thus the protocol does this itself using 50% of the protocol fees.

The remaining 50% allocated to users is shared between unstaked ybBTC and veYB governance, following a dynamic allocation.

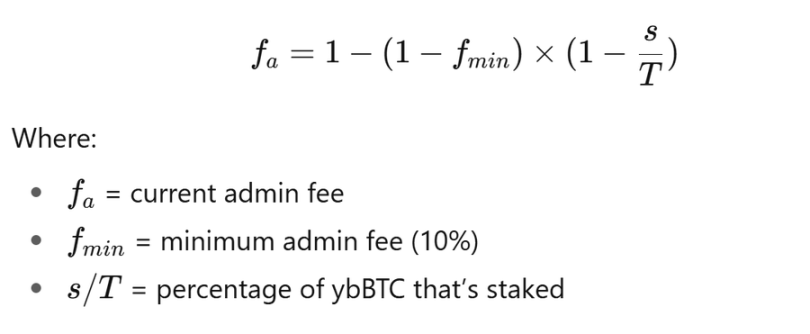

In short, the protocol tracks the amount of staked ybBTC and adjusts the fees each holder (of both unstaked ybBTC and veYB) can potentially earn using the following formula:

When no one stakes (s = 0)

Therefore, 𝑓ₐ = 𝑓𝑚𝑖𝑛 = 10%, veYB holders only receive a small portion (10%), and unstaked ybBTC holders receive the rest (90%).

When everyone stakes (s = T)

Therefore, 𝑓ₐ = 100%, and veYB holders receive all user-side fees because no one is left to earn transaction fees.

When half of the supply is staked (s = 0.5 T), the management fee rises (≈ 36.4%), veYB receives 36.4%, and unstaked holders share 63.6%.

For ybBTC holders who stake, they receive YB emissions which can be locked as veYB for a minimum of 1 week and a maximum of 4 years.

Staked ybBTC holders can lock in the emissions they receive to simultaneously enjoy both fees and emissions as a veYB holder, creating a flywheel effect that enables them to earn maximum fees from the protocol, as shown in the figure below.

Since launching, yieldbasis has had some interesting statistics:

- Total transaction volume reached US$28.9 million

- Over $6 million spent on rebalancing

- Incurred expenses exceeding $200,000.

Personal Thoughts

YieldBasis represents one of the most innovative designs in liquidity provision since Curve’s original stable swap model.

It combines proven mechanisms; voting custody token economics, automatic rebalancing, and leveraged liquidity provision, into a new framework that may set the next standard for capital-efficient income strategies.

Given that it was built by the same folks behind Curve, the market’s optimism is unsurprising. With over $50 million raised and the funding pool filling up instantly, investors are clearly betting on its future token launch.

Still, the product is in its early stages. While Bitcoin’s relatively stable nature makes it an ideal testing asset, introducing high-volatility trading pairs too early could challenge the rebalancing mechanism.

That being said, the foundations appear solid, and if the model can be scaled safely, it could open up a whole new frontier of returns for DeFi liquidity providers.