Nasdaq Enters Tokenized Stocks: Wall Street's On-Chain Revolution

- 核心观点:代币化证券市场正爆炸式增长。

- 关键要素:

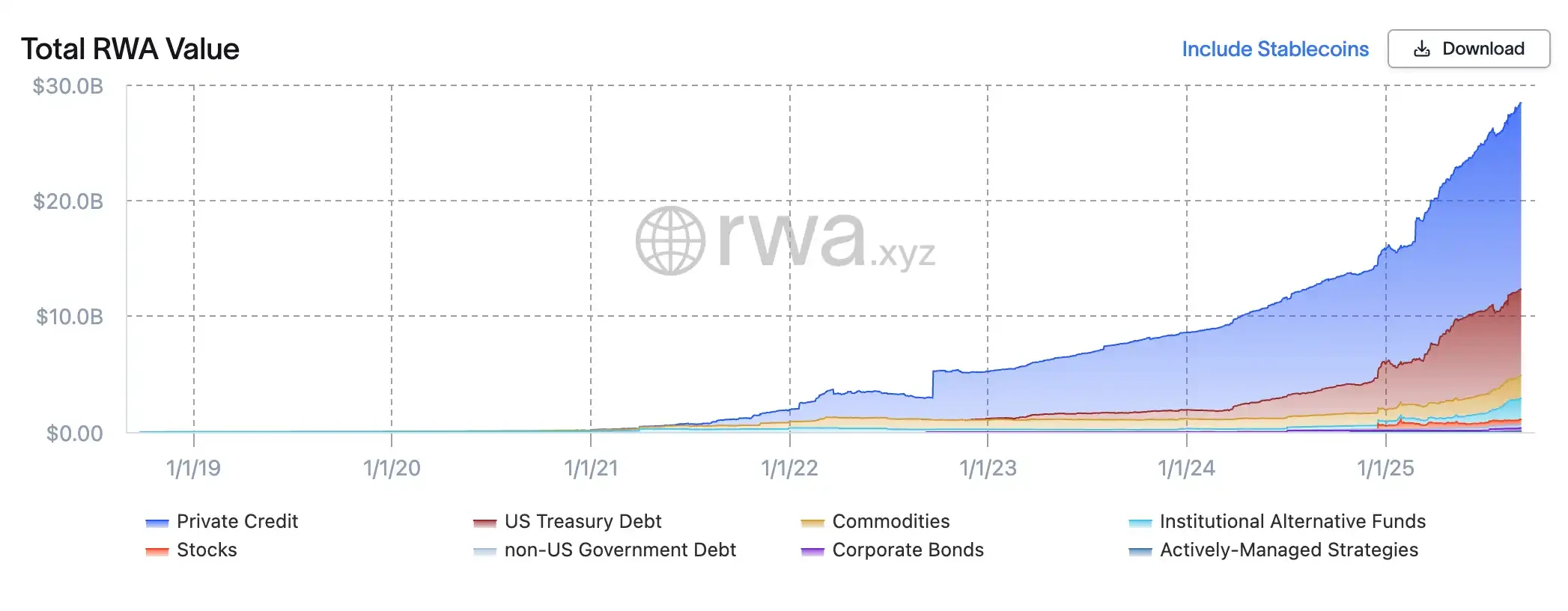

- RWA总市值突破28亿美元。

- 链上股票规模两年暴涨80倍。

- 纳斯达克申请代币化股票交易。

- 市场影响:推动传统金融与区块链融合。

- 时效性标注:中期影响。

In less than two years, the tokenized securities market has experienced near-explosive growth. According to RWA.xyz , the total market capitalization of tokenized real-world assets (RWAs) has surpassed $2.8 billion, with on-chain equities accounting for $420 million. This represents an over 80-fold increase from less than $5 million at the beginning of 2024.

Driving this wave is the collective entry and accelerated deployment of companies: Robinhood launched a tokenized private equity product, covering popular targets like SpaceX and OpenAI; Kraken's XStocks has listed tokenized versions of over 50 US stocks and ETFs; Ondo's Wall Street 2.0 has listed over 100 US stocks and ETFs on Ethereum; Galaxy Digital was the first to move its Nasdaq-listed shares onto a public blockchain; and SBI Holdings partnered with Startale to establish an on-chain trading platform in Japan. Both crypto-native companies and traditional financial giants are vying for first-mover advantage in the emerging market of tokenized equities.

This isn't just a race between crypto and traditional finance; it's also seen as a potential revolution in the traditional exchange model. On September 8th, Nasdaq, the world's second-largest exchange, proactively embraced the challenge by submitting an application to the U.S. Securities and Exchange Commission (SEC) to formally embrace tokenized stocks, attempting to elevate this transformation from a "fringe experiment" to the heart of Wall Street.

New packaging for an old system: The operating logic of tokenized stocks

Tokenized stocks aren't a new asset class that appears out of thin air; rather, they're a new "package" for traditional equity. The key lies in integrating blockchain's accounting and settlement capabilities with existing financial infrastructure. This logic is clearly articulated in Nasdaq's proposed rule submission to the SEC : In the future, investors will be able to select "tokenized settlement" when placing orders. Trades will still be matched within the same order book, with no additional priority granted due to tokenization. The real change occurs after the trade—Nasdaq will transmit settlement instructions to the Depository Trust Company (DTC), which will transfer the traditional stocks into a dedicated account, mint equivalent tokens on-chain, and distribute them to brokers' wallets. This way, the trading process for tokenized stocks remains identical to that of traditional stocks, with only on-chain mapping introduced at the settlement level.

This design means that tokenized stocks are not isolated from the National Market System (NMS), but rather integrated into the existing regulatory and transparency framework: transactions are still factored into the National Best Bid and Offer (NBBO), ownership and voting rights are identical to those of traditional stocks, and trading monitoring is jointly conducted by Nasdaq and FINRA. In other words, tokenization isn't a "new beginning" here, but rather an upgrade to the underlying infrastructure. "We're not replacing the existing system, but rather providing the market with a more efficient and transparent technological alternative," Chuck Mack, Nasdaq's Senior Vice President of North American Markets, said in an interview. "Tokenized securities are simply the same asset, expressed in a new form on the blockchain." This approach leverages existing market structures and clearing systems while making blockchain a next-generation custody and settlement tool.

From a broader perspective, the appeal of tokenization lies in its ability to address several core pain points in the capital markets. First, settlement efficiency. In the existing system, stock trades typically require T+1 or even longer to settle. On-chain settlement, however, allows for near-instant settlement, reducing counterparty risk. Second, trading time and accessibility. Traditional exchanges operate on an open-and-closed trading system, requiring cross-border investment to go through layers of intermediaries. Tokenized stocks, on the other hand, can theoretically be traded 24/7 and more easily reach overseas investors through blockchain wallets. Finally, asset programmability means that proxy voting, dividend distribution, and even corporate governance can be automated and transparent with the support of smart contracts.

In the long term, Nasdaq has positioned tokenization as the next iteration of capital markets infrastructure. With the completion of the Direct Trading (DTC) upgrade, on-chain settlement functionality is planned for implementation as early as the third quarter of 2026, enabling tokenized stocks to operate alongside traditional stocks within the regulated US market. Nasdaq has explicitly refused to pursue these initiatives through exemptions or circumventions, which not only upholds investor protection principles but also mitigates the risk of liquidity fragmentation.

Different paths for different players

xStocks: Compliant Custody + DeFi Composability

xStocks, driven by Backed Finance, leverages the distributed ledger (DLT) laws of Switzerland and Liechtenstein to establish a special purpose vehicle (SPV) to hold real shares, which are then minted on a public blockchain at a 1:1 ratio. Legally, these tokens are asset-backed senior debt certificates, backed by a custodian and real-time proof of reserves. By separating issuance from trading, the tokens can be traded on centralized exchanges like Kraken and Bybit, as well as integrated into DeFi protocols like Solana's Jupiter and Kamino. While this model offers openness and transparency, and true cross-market and cross-protocol compatibility, its drawbacks are limited liquidity and a market size not yet comparable to that of off-chain platforms.

Robinhood: A Closed-Loop On-Chain Experiment for a Licensed Brokerage Firm

Robinhood takes a completely different approach. Leveraging its Lithuanian subsidiary's MiFID II license, it sources and custody US stocks, ETFs, and private equity within a compliant framework, then mints corresponding tokens on the Arbitrum blockchain. All token transactions are completed within the Robinhood app, with tokens mapped to actual shares in real time to ensure that "on-chain quantity = custody position." This model offers advantages such as manageable regulation, a consistent user experience, and even the ability to implement fractional share dividends and on-chain liquidations. However, the tokens are virtually impossible to transfer freely, lacking open liquidity. Robinhood views tokenization as a tool to expand its financial reach, rather than simply as a market innovation.

Galaxy: A listed company’s self-hosted “native token”

Unlike the previous two, Galaxy Digital chose to move its Nasdaq-listed shares directly onto the blockchain. Working with SEC-registered transfer agent Superstate, it allows shareholders to convert their GLXY common stock into tokenized shares on Solana at a 1:1 ratio through a compliant process. Unlike "mirror tokens" or "synthetic contracts," these tokens are legally real shares, with full voting and dividend rights. Galaxy's initiative is the first to achieve "equal rights for tokens and shares," laying the foundation for a true on-chain equity market. However, its liquidity is still in its infancy, currently supporting only peer-to-peer transactions between registered users, and further regulatory relaxation is needed before a full secondary market can be established.

Ondo: Building Wall Street 2.0

Founded by former Goldman Sachs executives, Ondo Finance pursues a strategy of "institutional-grade packaging + open distribution." Its newly launched Ondo Global Markets platform tokenizes over 100 US stocks and ETFs onto Ethereum, providing non-US investors with a legitimate on-chain investment portal. Its model involves Ondo purchasing and custodial real stocks through licensed brokers, then minting tokens on-chain at a 1:1 ratio, ensuring that each token carries full economic rights, including dividends and corporate actions. Ondo's strengths lie in its scalability and openness—it not only offers daily proof of reserves, bankruptcy remoteness, and third-party custody, but also supports cross-chain interoperability and DeFi integration. Users can invest in high-profile stocks like Apple and Tesla, as well as use tokens as collateral for lending and automated strategies. Ondo has transformed tokenization into a "global financial supermarket," attempting to combine the liquidity of Wall Street with the transparency of blockchain to create a true Wall Street 2.0.

Related reading: From Robinhood to xStocks, how is US stock tokenization achieved?

Embrace or Risk? Wall Street Faces the Challenge of On-chain Transformation

Nasdaq has officially submitted its application to the SEC for tokenized stock trading, a move seen as a "core experiment" in Wall Street's digitization journey. The core of this proposal is that tokenized stocks should enjoy all the same rights and protections as their underlying securities. Trading matching will continue within the existing order book, while clearing will be handled by the DTC, which mints equivalent tokens on-chain. This means that tokenization is no longer a marginal experiment but could become a part of the institutional infrastructure of the US capital market. Compared to Robinhood or xStocks, which remain stuck in price mapping and contract voucher models, Nasdaq's approach is more radical—it is the first tokenization solution to fully migrate all shareholder rights (voting, dividend, and governance rights) onto the chain. This means that investors no longer receive a "shadow" of a stock but rather a digital share with full rights.

Nasdaq CEO Tal Cohen stated, "Blockchain technology offers unprecedented possibilities for shortening settlement cycles, modernizing proxy voting, and automating corporate actions." In other words, Nasdaq isn't looking to overturn the old order; rather, it aims to upgrade the underlying market structure with minimal institutional friction, ensuring the core principles of investor protection and market transparency remain intact. For regulators, this gesture sends a positive signal—rather than allowing tokenization to flourish unchecked overseas or in gray areas, it's better to directly incorporate it into a regulated framework.

However, there are also negative voices. JPMorgan Chase stated in a research report that the tokenization of bonds and stocks "has yet to achieve significant adoption outside of crypto-native companies," cautioning the market against overestimating short-term prospects. Citadel Securities warned that if regulators rush forward without establishing clear rules, this could lead to market risks. Globally, the World Federation of Exchanges (WFE) also sent a letter to regulators expressing concern that tokenized stocks "mimic" real equity but may lack shareholder rights and safeguards, and calling for strengthened legal and custodial frameworks. These concerns suggest that while tokenization has enormous potential, the implementation of the system still requires a long period of adjustment.

Summarize

Nasdaq's proposal isn't just a technical adjustment; it's an institutional "test of the waters." If the SEC ultimately approves it, it would mark the first time blockchain technology has taken a central role in the mainstream US stock market, potentially laying the foundation for future 24/7 trading, instant settlement, and smart contract governance. However, before this actually happens, the market remains to be seen: whether regulators can provide a clear framework, whether investors can trust this new model, and whether tokenization can truly deliver value beyond traditional markets.