In-depth analysis of what expectations the Ethereum Shapella upgrade can bring us

Original title: What can we expect from Shapella?

Authors: Henry Ang, Mustafa Yilham, Allen Zhao, Jermaine Wong & Jin Hao

first level title

Where are we now on the Ethereum roadmap?

Ethereum mergers throughout 2022. Ethereum passed the Paris upgrade, transitioning from Proof of Work (PoW) to Proof of Stake (PoS). On April 12th, Ethereum will undergo Shanghai and Shapella upgrades, pledged Ethereum can be withdrawn, and Ethereum will completely transform into a blockchain with a proof-of-stake mechanism.

first level title

Background to the Shapella upgrade

Although Shapella appears to be a single change to Ethereum, it is actually the amalgamation of two names that were upgraded at the same time -andandCapella. Ethereum’s execution layer will undergo a Shanghai upgrade, while its consensus layer will undergo a Shapella upgrade.

While the Shanghai upgrade consists of five EIPs, the most important of these is EIP-4895, which makes all Ether staked and locked by validators in Ethereum's consensus layer (the Beacon Chain) since its launch in December 2020. Cash can be withdrawn. Shapella is the third major upgrade to the consensus layer designed to facilitate this process, not only allowing blocks to process withdrawal requests, but also implementing account cleanup, which we will detail later.

secondary title

partial withdrawal

Partial withdrawals only involve the amount above the 32 ETH required to run validators. This account cleanup (or "scraping") happens automatically and periodically to any active validators who have updated to new withdrawal credentials.

This feature is extremely useful for two main reasons:

Since validator rewards are not automatically reinvested, this mechanism improves the capital efficiency of staker funds. Stakers will be allowed to reallocate their excess ETH for other benefits without having to pay any gas fees.

Additionally, partial withdrawals prevent long exit queues and excessive validator rotations that would otherwise be required to fully exit the beacon chain to access their rewards, potentially destabilizing the network.

secondary title

full withdrawal

If a validator chooses to completely "exit" as an active validator of the network, it will receive back 32 ETH and all rewards accumulated since its creation, which will occur in full withdrawal.

Similar to other PoS blockchains, validators will have a release period during which they will wait until they have received their full stake and reward balance. The length of this release period is determined by the sum of two variable times, the time it takes for a validator to exit the Ethereum consensus layer and the time it takes for the entire withdrawal process. Therefore, validators seeking to make a full withdrawal should expect at least 261 epochs or 28 hours.

articlearticlefirst level title

What does this mean for the price of $ETH?

secondary title

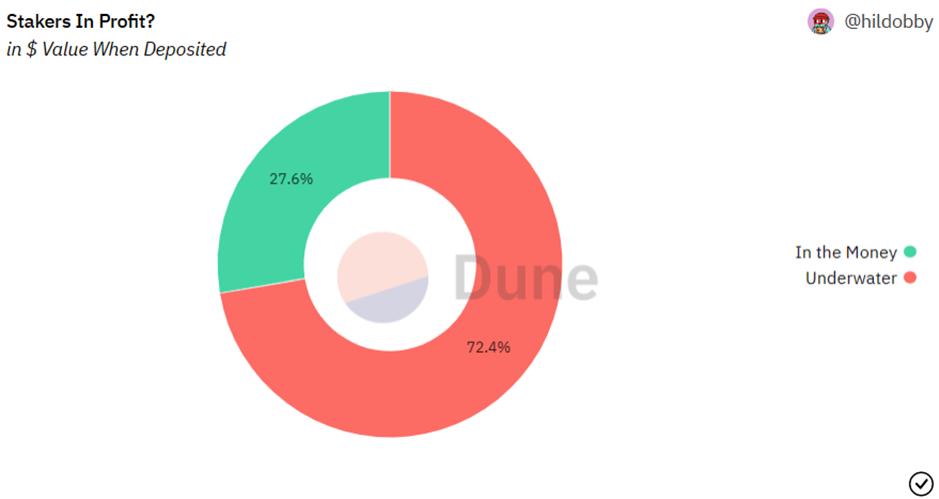

The Situation for Existing ETH Stakers

In order to estimate the potential price impact, we need to first assess the state of existing stakers and the decisions they might make. We believe that these decisions are largely driven by the financial situation of the stakers. In other words, are ETH stakers making a profit or a loss?

by hildobbyData Kanbansecondary title

The pledge amount of the liquidity pledge agreement

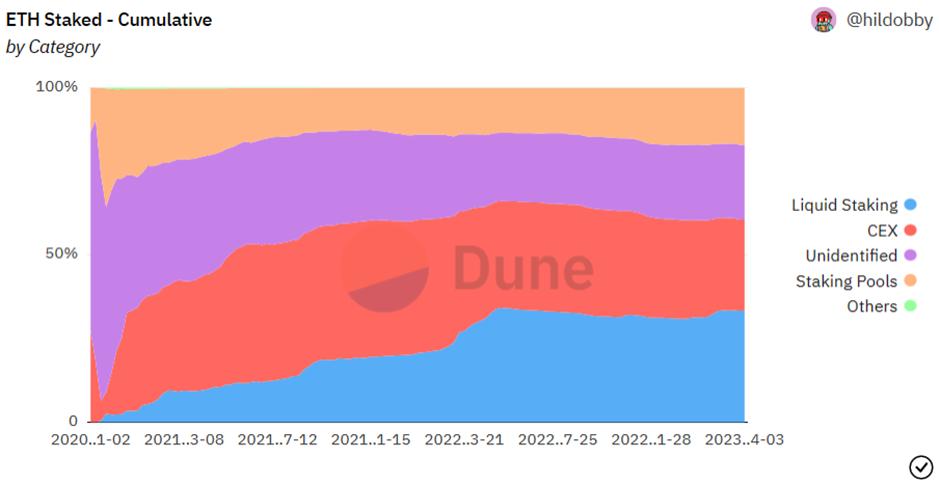

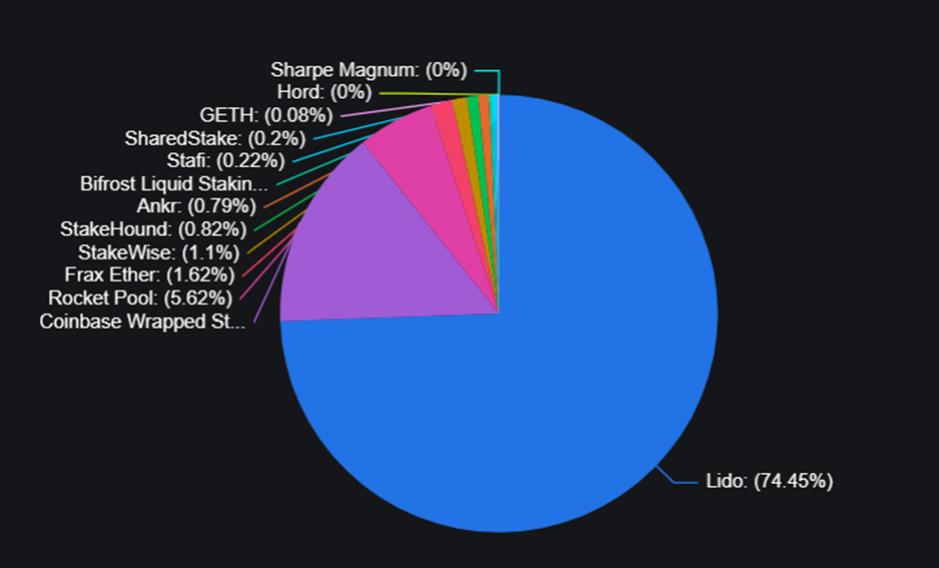

Another factor is to consider how much ETH is already staked via Liquidity Staking Protocols (LSPs). At the time of writing, according to DefiLlama, that number is over 30% (closer to 45% when including stakes on Coinbase), with the majority of ETH staked on Lido.

In the case of Lido, stETH is automatically rescaled to account for the accumulated rewards earned by staking liquidity. This means that users who choose to stake on Lido can “catch” ETH rewards by selling them on the secondary market. Therefore, for the validators behind Lido, there is relatively less pressure to withdraw directly and more flexibility to deal with excess rewards.

secondary title

Price of $ETH

Now that we've considered the key factors that determine the potential for a possible sale of ETH rewards, what does this mean for the $ETH price?

“If we assume that validators will sell 50% of their staked ETH rewards (instead of their main staked ETH), we expect 553,650 ETH to be sold. On a 7-day amortized basis, this equates to a daily sale of About 1% of daily ETH trading volume (including spot and perpetual futures trading volume).

Based on the overall risk environment and the overall liquidity situation for ETH during the expected Shanghai upgrade in early April, we think the impact of this volume will gradually spread to a slight decline in ETHUSD. Another view is that the smooth progress of the Shanghai upgrade is an overall bullish factor for Ethereum as a technology, so ETHUSD will rise. "—Galaxy

articlearticle, which we highly recommend reading.

first level title

secondary title

Liquidity Pledge Agreement

The Shapella upgrade could be a bullish catalyst for Liquidity Staking Protocols (LSPs) from multiple perspectives.

With ETH available for withdrawal, it should be easier and more economical for LSPs to maintain a price peg between their respective Liquid Staking Derivatives (LSDs) and ETH. This allows LSD to better borrow against collateral, as the tighter peg helps limit price volatility, reducing liquidation risk. Coupled with the growing adoption trend of LSD in the Ethereum DeFi ecosystem, this will become an opportunity for investors to pursue higher capital efficient returns.

The tighter peg also facilitates liquid staking of ETH, which is more of a “risk-free” or benchmark rate for investors. They used to be cautious about the long-term peg, because the peg largely depends on the supply and demand balance of various liquidity pools. And in the recent case of failure (stETH devaluation due to massive sell-off on the curve), it is impressive.

For the reasons above, we expect most of the withdrawn and idle ETH to flow into LSPs and their adoption to increase further. But which LSPs are better prepared than others? We'll go over some of the different LSPs below, what they do, their flywheel effects and feedback paths, and how these LSPs give users more control over their extraction keys, NFT utilization, and more through MEV strategy for additional benefits.

Lido Finance (LDO, stETH)

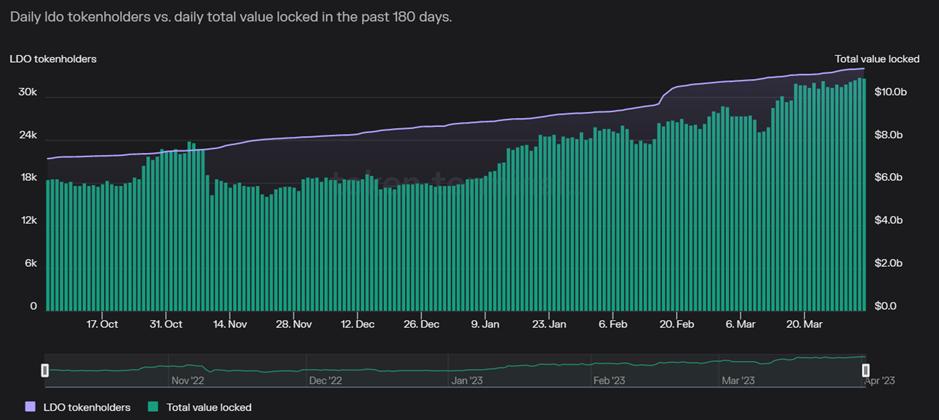

After the upgrade, it is clear that Lido's TVL will increase significantly, making it the leader in the LSP space. With a strong reputation, deeper liquidity, and a plethora of DeFi integrations, those looking for a liquid staking project have good reason to choose Lido. Since November, Lido has seen an upward trend in token holder count and TVL, accounting for nearly 75% of total ETH staked to date.

With the centralization issue caused by Lido's increasingly strong position in the LSP circuit, coupled with the increased governance scrutiny after the Arbitrum incident, the governance system will be more important than before. Although they have taken steps tostETH holdersBeing included as part of the governance of LDO holders is commendable, but users who want to help decentralize the ETH token may also consider the other alternatives we list below. Lido also recently announced that its upcoming v2 will take a step towards further decentralization and revolve around two major upgrades, withdrawal and staking routing.

Swell Network

Swell Network is also an upcoming LSP that aims to provide users with higher staking returns. Currently, their latest version, Seawolf, is already running on the Goerli testnet, and Swell is preparing to launch on the Ethereum mainnet in late April after the Shapella upgrade. While initially working with a set of licensed professional node operators will still be required to deliver large-scale, reliable benefits to users in a competitive environment, subsequent iterations will see the set of operators expand and eventually become unnecessary. Authorized, with sufficient liquidity, stability and risk mitigation technologies, such as DVT, these are consistent with the value orientation of the agreement.

Swell’s liquid staking token, swETH, will be a yield-bearing token whose value increases as on-chain rewards accumulate. Users can be rewarded through consensus layer rewards (such as staking rewards) and execution layer rewards (such as priority fees and MEV). Users who stake in the Swell Network also have access to vaults that run yield-enhancing strategies, all within their dApp. Swell will be the lowest-cost staking project on the market, with no protocol staking fees.

Rocket Pool (RPL, rETH)

Rocket Pool appears to have some advantages over more dominant players like LDO, such as a more decentralized network of node operators and lower capital requirements for node operations (only 16 ETH). However, it also has its own disadvantages. These disadvantages include higher performance fees compared to competitors, and the fact that node operators must lock a percentage of the value of their staked ETH in RPL as collateral for protocol insurance.

While this higher friction exists for users looking to operate a node from Rocket Pool, the benefits of the upcoming Atlas upgrade may more than offset it. The Atlas upgrade, scheduled for release on April 18, brings several improvements, including improved protocol efficiency, increased node operator rewards, and greatly increased rETH capacity, while maintaining the completely permissionless nature of the protocol. One of the most important features is the introduction of 8 ETH mini pools, which will further reduce the minimum capital requirement. At the same time, this feature can lead to higher returns for node operators and rETH stakers, providing up to 18% additional returns when users run two 8-ETH mini-pools instead of one 16-ETH mini-pool . While this is good for Rocket Pool going forward, we still need to see if the watcher has been updated to actually effectively attract TVL and market share from its competitors.

Frax Finance (FXS, frxETH/sfrxETH)

Frax has grown rapidly in market share this year and has become a serious contender with a promising future ahead. This growth can easily be tied to the highest staking annualized yield of around 5.6% that Frax offers, as well as its dual-token model. In this context, frxETH acts as a stablecoin loosely pegged to ETH, and sfrxETH is a staking version of frxETH that earns staking rewards. Through this design, Frax enables frxETH holders to earn in multiple ways, namely staking for sfrxETH and validator rewards, or providing frxETH-ETH liquidity on Curve. Together, these two options not only create deeper liquidity in frxETH, but also increase the annualized rate of return in the sfrxETH and Curve liquidity pools.

Like Rocket Pool, Frax is also planning an upgrade after Shapella, which could be a strong catalyst for its adoption. The frxETH v2 upgrade is planned to increase decentralization by enabling no need to be restricted to validators (run by the protocol itself). In addition to this, a proposal was recently passed to use FXS bribes and incentives to initiate future liquidity of frxETH trading pairs, creating a powerful flywheel that would theoretically eventually lead to an increase in the value of FXS and frxETH, as well as more High yield and attract more liquidity for LSD. ZhouYeMen from DWF Labs explains this topic in great detail here.

Ether.fi (eETH)

Ether.fi is another decentralized LSP entering the market, but it has some important distinguishing characteristics. Ether.fi uses a non-custodial delegated stake protocol where users generate and hold their own ETH keys. Another feature is that it utilizes NFTs, minted for each validator initiated through the protocol. These NFTs control the stake of 32 ETH and store validator-related metadata such as client, geographic location, node operator, and any node services. Ether.fi’s eETH is then minted from the liquidity pool of these NFTs.

The combination of these two mechanisms allows users to submit exit commands themselves, rather than the usual node operators. The recovered collateralized ETH will be deposited into a withdrawal safe, where users will be able to net their ETH back by burning their NFTs. This successfully reduces the significant and opaque counterparty risk that users have in other LSPs, while ensuring that there will always be sufficient ETH liquidity for eETH holders to redeem. Therefore, we expect Ether.fi to be one of the LSPs to see a surge in users and TVL post-Shapella.

In the future, Ether.fi plans to use EigenLayer to create a node service market where users and node operators can register their minted NFTs, provide node infrastructure services, and share the revenue of these services with users and node operators. At present, Ether.fi has provided institutional equity entrustment services, customized investment structure services, and developed an early user program for retail liquidity equity. With ETH withdrawals enabled, institutions may also view ETH stake delegation as a viable investment, with Ether.fi positioned as one of many beneficiaries.

Manifold Finance (FOLD, mevETH)

Manifold is also a new player in the LSP space, having launched its MEV-optimized, multi-chain LSP less than a week ago. mevETH is implemented as a chain-wide utility token (OFT) that can be directly bridged between chains without wrappers, making it the most composable LSD to date. At the same time, mevETH is designed around MEV capture, adopting Manifold LSP's unique and novel MEV method to provide users with additional benefits in addition to staking benefits. One of these ways is by arbitrage the peg between ETH and mevETH, not only providing a means of additional yield, but also helping to strengthen the peg.

secondary title

Perspectives on LSD

secondary title

DeFi

Pendle Finance (PENDLE)

Pendle is a yield trading protocol that allows users to execute various yield management strategies by encapsulating yield tokens and splitting them into two tokens—PT representing principal and YT representing yield. Both can transact through their custom AMM. 1 PT gives the user the right to redeem the underlying asset at maturity, with the expiration date being determined by the initial token holder, while 1 YT gives the user the right to receive the proceeds on the underlying asset before the expiration date. This allows Pendle to essentially create an income market, enabling users to adopt a variety of strategies, including long-term holding assets at discounts, targeting annualized returns, and even obtaining low-risk and stable-growing fixed income.

Likewise, locked ETH users can use Pendle to split their stETH into 1 PT stETH and 1 YT stETH, then use Pendle's custom AMM to trade any token and place targeted bets on the proceeds. With the upcoming Shapella upgrade and expected staking yields decreasing over time, one possible trade stETH holders can take is to sell YT stETH at the current price to earn a differential based on their existing yield.

Since December, Pendle's TVL has seen a seven-fold spike, with more and more users discovering its potential. According to DefiLlama's breakdown of token TVL, more than a third of this can be attributed to LSD, including stETH and frxETH. With Pendle's latest integration of sfrxETH, we may see LSD increase as a percentage of Pendle's TVL.

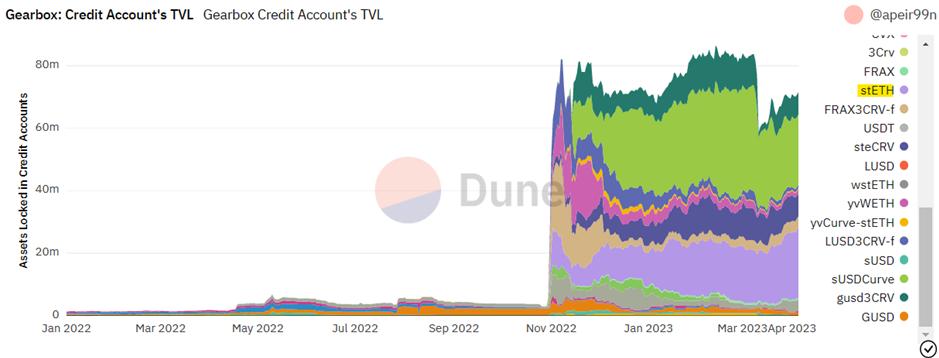

Gearbox (GEAR)

On the topic of leverage, the closer connection between LSD and ETH after the aforementioned Shapella upgrade reduces liquidity risk and unlocks the feasibility of leveraged ETH staking. Gearbox is a two-way lending marketplace that connects users looking to offer their assets passively and securely via APY with leverage enthusiasts looking for additional capital. The protocol introduces Leveraged Liquid Staking Derivatives, or LLSD, as a one-click strategy that enables users to locally stake up to 10 times the value of their ETH collateral for higher staking yields, up to 12 % more, compared to the 4.3% APR currently offered by Lido.

The strategy has so far been enabled for Lido’s stETH and Coinbase’s cbETH (waiting for DAO vote), with plans to integrate Frax’s and Rocket Pool’s frxETH and rETH once they have mainnet Chainlink oracles respectively. As a base layer of leverage, Gearbox is positioned to benefit indirectly from the projected increase in the number of ETH staked and the growth and adoption of LSPs and LSDs, as more ETH stakers are looking for relatively low-risk ways to increase their staking returns . Over the past few months, stETH has accounted for more than one-third of Gearbox’s total credit account TVL, which stands at approximately $22 million.

With the launch of Gearbox v3 just around the corner, one can expect new features like automated portfolio management and health factor maintenance to further incentivize LSD token holders to leverage Gearbox’s leverage capabilities, pushing it to the forefront of DeFi.

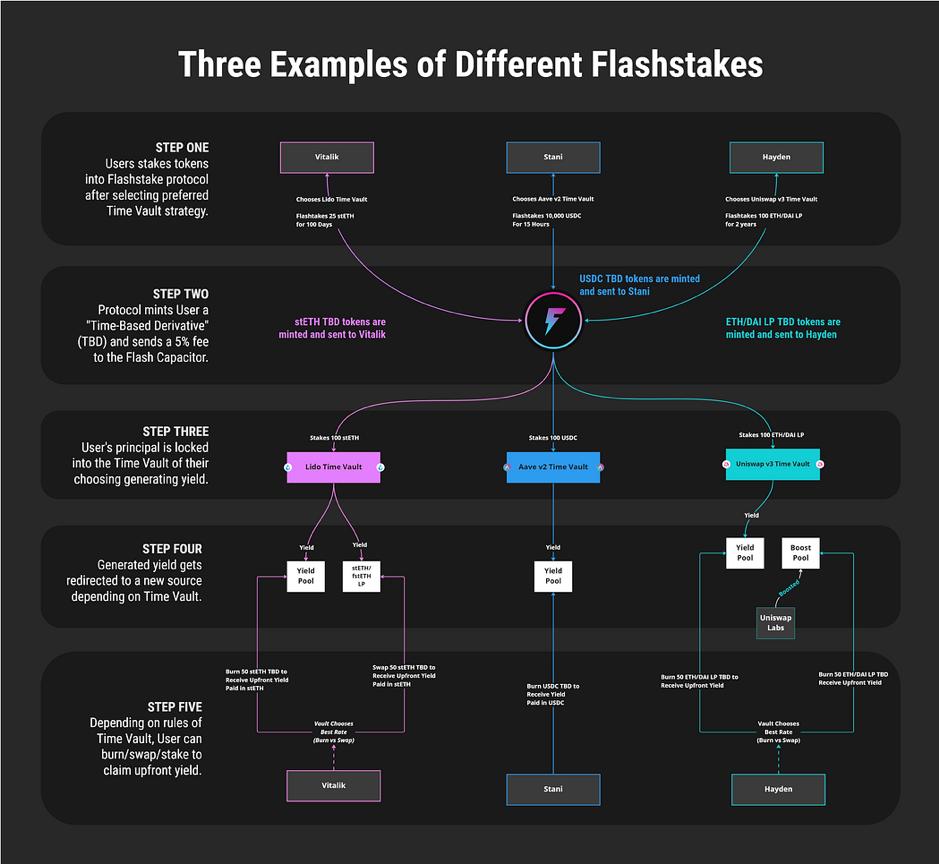

Flashstake (FLASH)

Flashstake is another novel protocol that introduces a unique mechanism to increase the capital efficiency of user assets. Users deposit and mortgage their assets, lock in the current annual interest rate, and mint time-based derivatives (TBDs) corresponding to their positions. Users can then burn or swap these TBDs for an upfront yield on their assets, getting their principal deposit back after a chosen lockup period. This is especially interesting considering ETH’s collateralized yield is expected to decrease over time. Flashstake enables early adopters to not only secure and anchor current (supposedly highest) ETH staking returns for a period of up to 1 year, but also continue to generate returns elsewhere.

Understandably, this may cause some concern. Where do these prepaid proceeds come from? To provide this yield to users, Flashstake employs a three-pool approach consisting of a yield pool, a liquidity pool, and an acceleration pool.

secondary title

re-pledge

EigenLayer

With the upgrade of Shapella to extract Ethereum, the ETH locked using the EigenLayer contract can be withdrawn and reduced if malicious intent is detected. This paves the way for EigenLayer to become a decentralized trust layer for applications where existing ETH holders can choose to use their stake to secure new applications on EigenLayer. EigenLayer's rehypothecation mechanism offers users an opportunity for incremental returns beyond what they would have earned by simply staking ETH and earning MEV-related rewards, while fulfilling its primary purpose of modularizing and enabling Ethereum's trust layer Broad design space for new middleware and adjacent chains.

secondary title

new innovation

Ion Protocol

Despite some success in increasing LSD adoption in DeFi, there is still significant friction today. Since there are multiple different LSD and liquidity staking designs, DeFi protocols that want to integrate each of them will require multiple custom and novel solutions. For example, Uniswap cannot accept rebase LSD like stETH from Lido, while blue-chip protocols like Aave and Maker require separate vaults and pools for different LSD tokens. This results in decentralized and shallow liquidity for LSDs, leading to increased slippage and inefficient price discovery, defeating their original purpose of representing staking ETH and distributing staking rewards.

Among its many goals, Ion Protocol aims to provide a solution to the aforementioned problems by utilizing a dual-token model to aggregate deposits of various existing LSD tokens into a common unit of account. This universal unit of account will allow for better frictionless integration into DeFi, harnessing the full potential of LSD, using it as low-risk, yield-generating collateral, and even increasing capital efficiency through leverage.

UnshETH (USH)

UnshETH promotes the decentralization of validators through incentives, directing more revenue to LSPs with lower dominance. This is done with new classes of primitives called LSDfi, including validator decentralized mining (vdMining) and validator dominance options (VDO).

vdMining is a token distribution mechanism that rewards users for investing more in LSPs that meet a predefined optimal decentralization ratio, while VDO is a mechanism that allows the holding of dominant LSD Validators sell "puts" on their validator dominance percentage, with strike prices set at percentages below their current dominance. If the dominance is lower than the strike price at maturity, the VDO holder will lose a portion of the proceeds, which will be distributed to holders of other LSDs. These two mechanisms combine to incentivize new stakeholders to do so with less dominant LSPs and incentivize more existing dominant LSD holders to spread their capital across various LSPs.

New features are planned for the Shapella upgrade, including a router for staking ETH liquidity and others that will help improve the utility of UnshETH's native token, USH. Next, we can see how much UnshETH's TVL will eventually capture and whether it can become a de facto income solution for ETH holders.

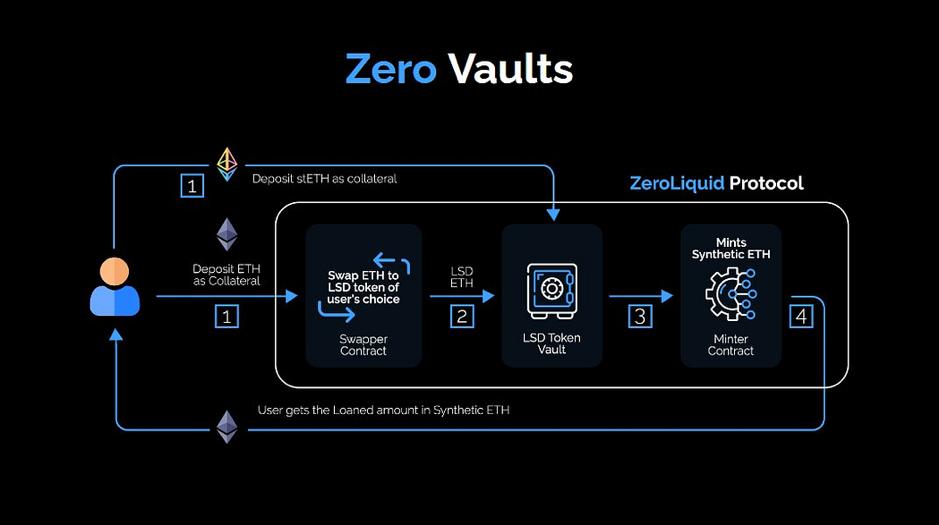

Zero Liquid (ZERO)

Zero Liquid is another new protocol that may belong to LSDfi's new track, issuing self-repaying loans for users' LSD. Similar to more traditional money market protocols like Aave, Euler, etc., users first deposit assets as collateral and are then able to take out loans for a portion of their collateral value.

In the case of Zero Liquid, users are able to deposit LSD and native chain tokens (ETH, MATIC, etc.) as collateral and receive a synthetic version of the asset as a loan. However, these loans are characterized by their 0% interest and self-repaying nature which, combined with the use of synthetic assets, allows the protocol to offer a zero-liquidation model. Zero Liquid achieves this goal by automatically repaying debt using the proceeds generated by users depositing collateral.

While the protocol has yet to officially launch its product, one can already foresee many unique use cases beyond maximizing user assets, where it comes in very handy. With zero liquidity, users can basically invest and buy without requiring any upfront capital. With some resemblance to the real-world "buy now, pay later" model, paying through Zero Liquid's products will allow users to buy or "spend" immediately and only use the future rate of return (or time, depends on how you look at it) to pay.

first level title

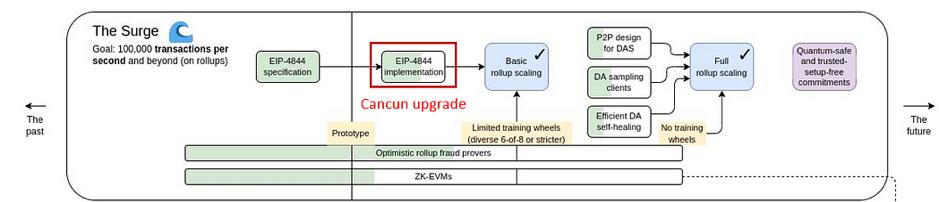

What happens after Shapella?

After Shapella, the next anticipated Ethereum upgrade will be the Cancun upgrade, which is part of the scaling roadmap. While second-layer scaling solutions like Optimism and Arbitrum have reduced costs by more than 8x, data storage fees are still high, accounting for more than 90% of transaction costs.

EIP-4844 aims to reduce the cost of L2 rollup by 10-100 times and usher in a new era of low-cost on-chain activities by introducing proto-danksharding into Ethereum. It provides support for implementing Danksharding schemes (e.g. transaction formats, validation rules). EIP-4844 introduces temporary "blob" storage that can be removed from Ethereum when not needed. Ethereum is expected to provide more than 100x throughput and reduce transaction costs below $0.001.

Other possible improvements in the Cancun upgrade include six EIPs accumulated over the years in the EVM Object Format (EOF) group, which aim to better structure bytecode, or computer object code, so that the interpreter converts it to binary Machine code for computer hardware processors to read, making systems faster, more efficient, cheaper and more secure. One of these has been included in the previous London update, some may be in the upcoming Shanghai update, and the rest may arrive with the Cancun update. These EIPs will support the implementation of EOF 2, a new extension to EOF that revolutionizes the control flow.

The immediate beneficiaries of the Cancun upgrade will be those rollups and users that can be deployed directly for Dapps. Thanks to the sharp drop in transaction costs, new applications will also be able to benefit from this upgrade. For example, the cost of order books on the chain will be lower, and the decentralized physical infrastructure network will also be able to take advantage of faster L2 conducts transactions while settling to the trusted Ethereum base layer. We'll dive into these opportunities further as the Cancun upgrade rolls around.

Disclaimer: Bixin Ventures is an investor in the three projects mentioned in the article, EigenLayer, Pendle Finance and Swell Network.