A glance at the current crypto claims market structure: GTX, Xclaim, Claims-Market

Recently, according to a financing document circulated in the market, Su Zhu and Kyle Davies, founders of the original Three Arrows Capital, are preparing to build a new centralized encryption trading platform "GTX". Bit joint creation Sudhu Arumugam and Mark Lamb sparked widespread heated discussions in the industry.

Some people think that the debt trading market formed for encrypted assets is indeed a neglected blue ocean market at present, and it is also a good business to make money. However, there are other different views on this: Based on the previous bankruptcy experience and credit depreciation of Su Zhu and several other GTX joint ventures in the encryption circle, the newly created GTX will eventually be used by no one.

first level title

The Influence and Origin of Debt Transactions

First, let's look at what problems are solved by debt transactions, and where it can be traced back to.

Corporate bankruptcy is one of the most misunderstood topics in the business world. For many people, the first word that comes to mind when hearing a company that has filed for Chapter 11 bankruptcy is usually "failure" or "loss," and bankruptcy is rarely associated with words like "opportunity."

This is often because Chapter 11 bankruptcy is a complex court process for both debtors and creditors, with many intricacies and unpredictability going on in the legal process, and because Chapter 11 is not always the right solution for all parties involved. side to bring favorable recovery.

Fortunately, though, for creditors caught in the chain reaction of endless bankruptcy cases, there is another, more convenient recovery option, and it's one of the lesser-known areas of corporate bankruptcy: a process called"Bankruptcy Claims Trading" or "Debt Trading"common practice.

During the normal course of bankruptcy proceedings, creditors assert their right to repayment by submitting a "proof of claim" to the debtor, which clearly states the amount owed to the creditor according to the accounting records, to which the debtor is obliged to pay. Also, creditors will typically provide supporting documentation (i.e., contracts, invoices, lease agreements, etc.) along with the submitted Proof of Claim form as evidence of the creditor's bankruptcy claim.

But after all of that, creditors still have to wait for the debtor's bankruptcy case to go through the court process before their claims are approved and payments issued, a process that can take years for creditors to receive any amount owed to them.

In addition, for creditors seeking recovery guarantees and financial certainty, their bankruptcy outcome adds some uncertainty due to 4 factors:

1) Claim Verification

A valid creditor's claim is considered allowed if the creditor has submitted proof of claim or if the debtor does not object to the claim. At the same time, the debtor can also raise an objection to the claim to make the claim invalid or rejected, thereby reducing its own responsibility to facilitate reorganization.

If the debtor's objection is successful, the court will dismiss the claim and the creditor will not be able to share in the repayment distribution from the debtor's bankruptcy estate. For creditors, objections from debtors and rejection of their claims by courts may lead to increased uncertainty about eventual recovery.

2) Priority of creditors

Another factor that creates uncertainty for creditors is the priority of bankruptcy claims. This is the result of the Chapter 11 claims classification process, which determines the creditor's priority in receiving payment.

Higher-priority claims or secured claims will be paid in full from the debtor's estate before lower-priority claims are paid. Unsecured claims and equity holders, which are lower-tier bankruptcy claims, are often only paid a percentage of the amount of their claims, or offered alternative payment methods, or may not receive payment at all.

3) Debtor's reorganization plan

Within 120 days of the date of the bankruptcy filing, debtors must file a reorganization plan outlining how they plan to reorganize and return to being a healthier business, though they also reserve the right to request an extension if needed.

In this process, not only is it time-consuming for the debtor to formulate and submit a reorganization plan, but it is also time-consuming for creditors to review, vote and approve the terms of the reorganization plan, and the two parties often have certain differences on the future reorganization plan.

4) Claims procedure

After receiving confirmation of the reorganization plan from the court, the claims process began. Finally, the debtor can begin implementing the approved plan and begin making payments to creditors in the order defined by their rank and seniority levels. Even at this point, if the funds in the bankruptcy estate are exhausted, creditors with unsecured claims may not receive payment, or be offered alternative forms of redress.

Given the above uncertainties, this is why debt transactions offer creditors a unique opportunity to recover their losses and minimize uncertainty.

With debt transactions, creditors can monetize their claims in exchange for instant cash, in addition to bypassing the lengthy bankruptcy claim process and potentially protracted court proceedings. Thus, a claim transaction describes a financial and legal transaction in which a creditor sells and transfers its title in a bankruptcy claim to another entity for immediate monetary payment of the claim from the buyer.

In short, creditors are selling their receivables in exchange for instant cash from interested buyers. As a result of this transaction, a formal claim for this debt was recorded in bankruptcy court and legally transferred to the buyer, who then assumed the risk of recovering payment from the debtor.

first level title

Current status and opportunities of encrypted debt trading market

In the traditional debt transaction process, each of the above steps is largely handled manually and carried out through paper documents, fax transmissions or telephone/mail correspondence. It is the creditor's and buyer's responsibility to cooperate with each other to make the debt transaction successful. Similar to buying a home, the process can be complex and each manual step has the potential for mistakes to jeopardize the deal.

At the same time, before there was a centralized debt trading market, there were mainly some OTC markets. Buyers and sellers negotiated and settled in QQ groups through simple communication tools and even some domestic transactions. Credit transactions are either directly from the seller to the buyer, or from the seller to the buyer indirectly through a broker. The market is very unbalanced. There may be tens of thousands of creditors in a bankruptcy case, but the order of magnitude of buyers is much smaller.

As the market evolves, the process today is not only inefficient and inconvenient for both parties, but also risky and lacks transparency, making currency recovery more difficult to achieve. The bankruptcy claims market therefore urgently needs a centralized platform that digitally connects creditors with verified buyers and provides a safe and secure online environment to trade claims efficiently and recover cash quickly.

In the field of encryption, with the serial thunderstorms of encryption companies in 2022, and the bankruptcy of FTX alone, millions of encryption account holders have become creditors of the exchange. Su Zhu mentioned in GTX's financing documents that this will be an emerging market with a scale of 20 billion U.S. dollars, so more tailored solutions are needed in this segment to help unlock frozen accounts.

At present, more and more encrypted claims platforms have introduced technology and automation into this debt trading market plagued by inefficiency and information asymmetry. It aims to help users solve 3 core problems:Help creditors obtain the highest price, provide transparent settlement documentation, and build a predictable settlement process.

In terms of mechanism design, in order to allow each creditor to claim as much as possible to recover as much as possible, most platforms charge zero fees for creditors to register, list, sell or transfer the creditor's rights of bankruptcy institutions, and a small amount of transactions paid to the platform Fees are often provided by the buyer.

On the other hand, bids from buyers are generally non-binding and subject to a 48-hour due diligence period and standard contractual clauses. Once the buyer agrees to proceed to claim the purchase and provide any proposed contract modifications, the platform will notify creditors of the proposed transaction terms. If the creditor accepts the proposed terms, a binding confirmation of the transaction is created and the parties proceed to complete the transaction.

first level title

secondary title

GTX

With the disclosure of GTX's financing documents, Su Zhu began to officially enter the debt trading market, focusing first on the debt trading after FTX's bankruptcy. He believes that creditors of FTX are currently unable to withdraw assets from the platform, but the current creditor’s rights market is very unfriendly to the experience of small creditors with cumbersome procedures and high handling fees, and GTX will build an order book like BTC. The traditional and in-depth creditor's rights trading market, and creditor's rights can be used as transaction collateral to increase more financial liquidity.

Previously, BlockBeats had writtenWhat exactly does Three Arrows Su Zhu's new trading platform GTX do? "An introduction to GTX is given, and the reader is referred back to it.

In the earlier period, the largest bankrupt companies in the encryption field mainly included Mt Gox in 2014 and the collapse of QuadrigaCX, Canada's largest cryptocurrency exchange in 2020, but the market capacity was still very limited at that time.

With Luna, Three Arrows Capital, FTX, Celsius, Voyager and many other crypto institutions going bankrupt and thundering in 2022, an encrypted debt trading market formed around this can no longer be ignored.

secondary title

Xclaim

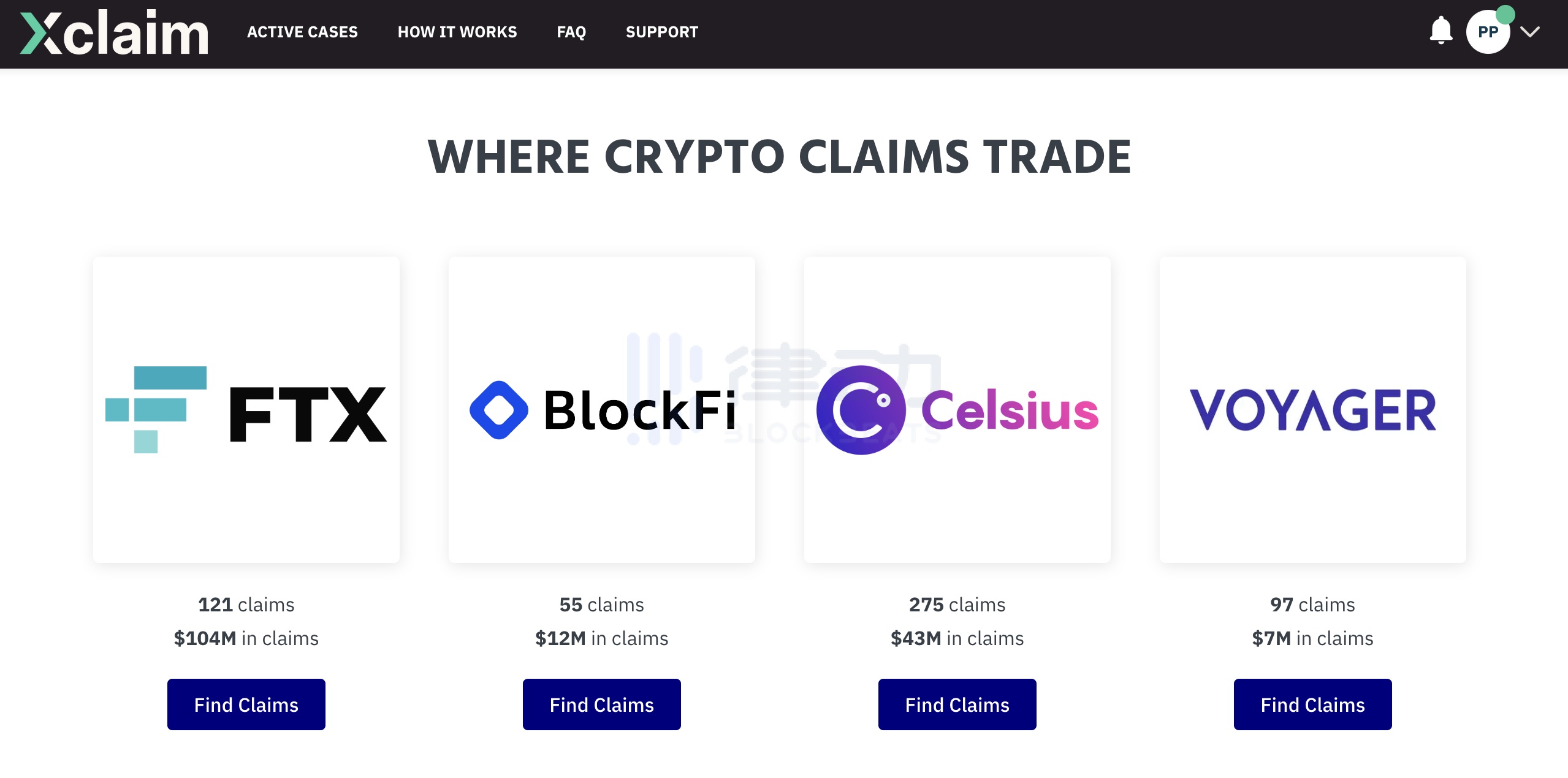

XclaimFounded in 2018, it aims to provide transparent pricing and fast execution for each crypto claimant. It has a diverse team of engineers, data scientists, financial, legal experts, etc. The founder and CEO Matthew Sedigh has worked in 15 years of experience in the corporate restructuring industry.

Currently, Xclaim can provide creditor's rights transactions on four bankruptcy platforms: FTX, BlockFi, Celsius, and Voyager. There are more than 500 people who have listed tradable claims on this market, with total assets reaching 166 million US dollars.

On the other hand, the level of interest claimed by users may vary depending on the nature of the assets claimed and the status and timeline of the bankruptcy case. Platform data shows that the current transaction value of FTX claims is only 15.5% of the total value, while the transaction prices of BlockFi, Celsius and Voyager's claims are 30.5%, 19.5% and 38% of the total account value respectively.

The specific operation steps of the platform are mainly divided into the following 4 steps: (The specific transaction steps can also be viewedHow FTX Creditors Sell Claims on Xclaim? "One article for experience)

1) Register an encrypted account and provide basic information to share with other users who are interested in purchasing bankruptcy claims;

2) Get great deals and ensure fair market value by comparing multiple offers from the largest network of online buyers;

3) The platform will only trade at the price approved by the creditor, and support and handle all legal affairs along the way. Before the creditor signs, everything is not the final decision;

4) Final payment to the creditor's bank account.

In terms of platform advantages, although Xclaim Marketplace does not include secured claims, the platform has more than one million priorities, administrative 503(b)( 9) (the Bankruptcy Code stipulates that creditors can target claims received by debtors within 20 days. Commodity filing administrative fee claims) and general unsecured claims are available for trading.

secondary title

Claims-Market

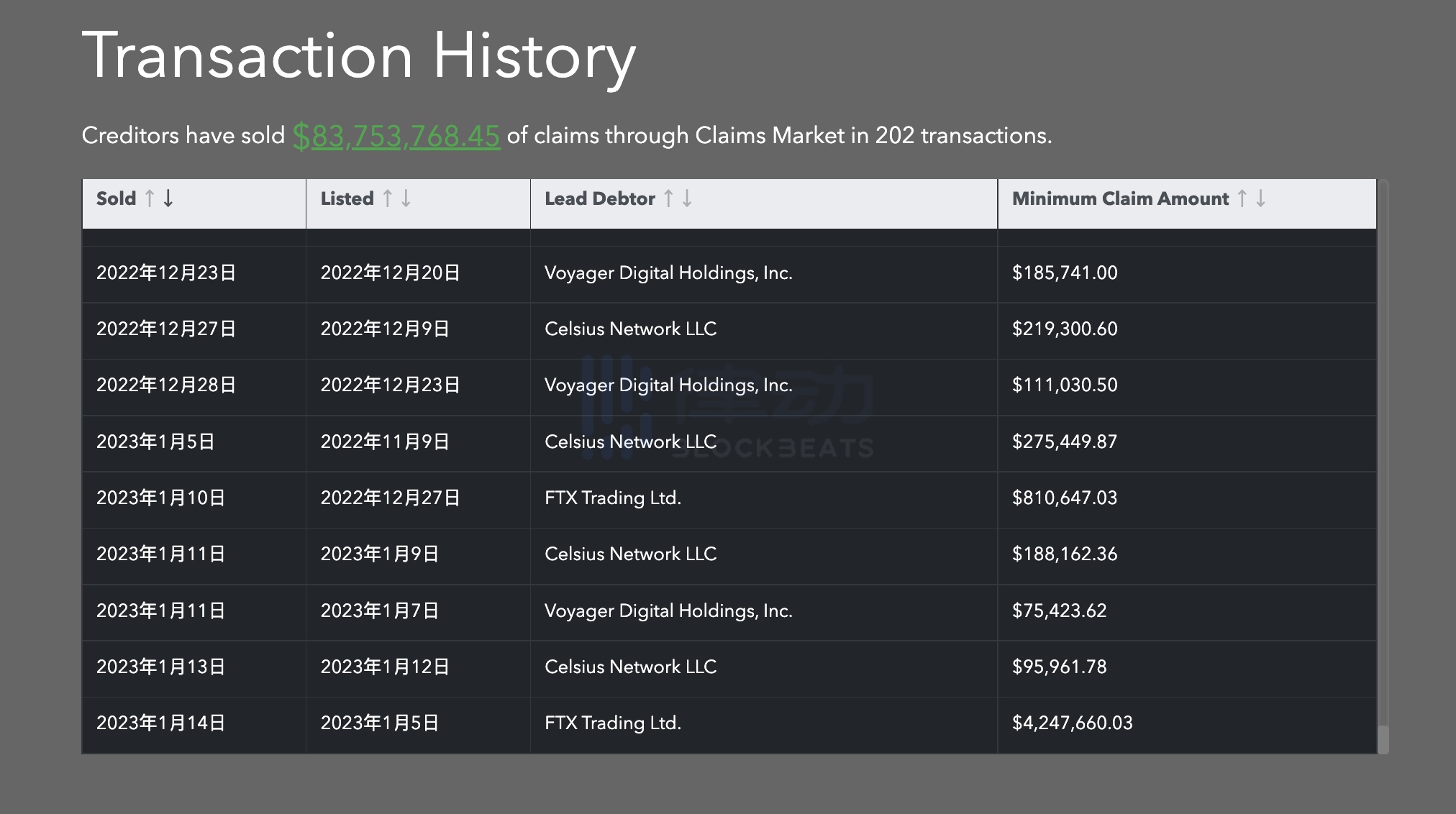

Claims-Marketis an investment bankCherokee AcquisitionThe market structure of its claim settlement products is also designed for creditors. After the seller's price is accepted by the buyer and the transaction is confirmed, the buyer and seller are introduced to each other, and the transaction takes place directly between the buyer and the seller. And also by the buyer to pay the management fee, the seller does not pay any fees.

Vladimir Jelisavcic, manager and founder of Cherokee Acquisition, has said that customers with about $1 billion in credit claims are interested in selling their claims through Cherokee, which matches creditors with debt buyers, mainly hedge funds, Sometimes they also hold part of the debt.

At the same time, he was also shocked by the bankruptcy of crypto institutions such as FTX, Voyager and Celsius, and many customers will only be able to recover a small part of their total assets from these platforms. Still, many people don't want to wait for the lengthy bankruptcy process to end, opting instead to get some money now.

Another frustrating aspect of the bond transaction is not knowing when the buyer will pay. There can be many reasons for this uncertainty: complex, unsubstantiated claims requiring extensive due diligence, legal counsel's inexperience in selling debt transactions, and delays by buyers in preparing closing documents, among others.

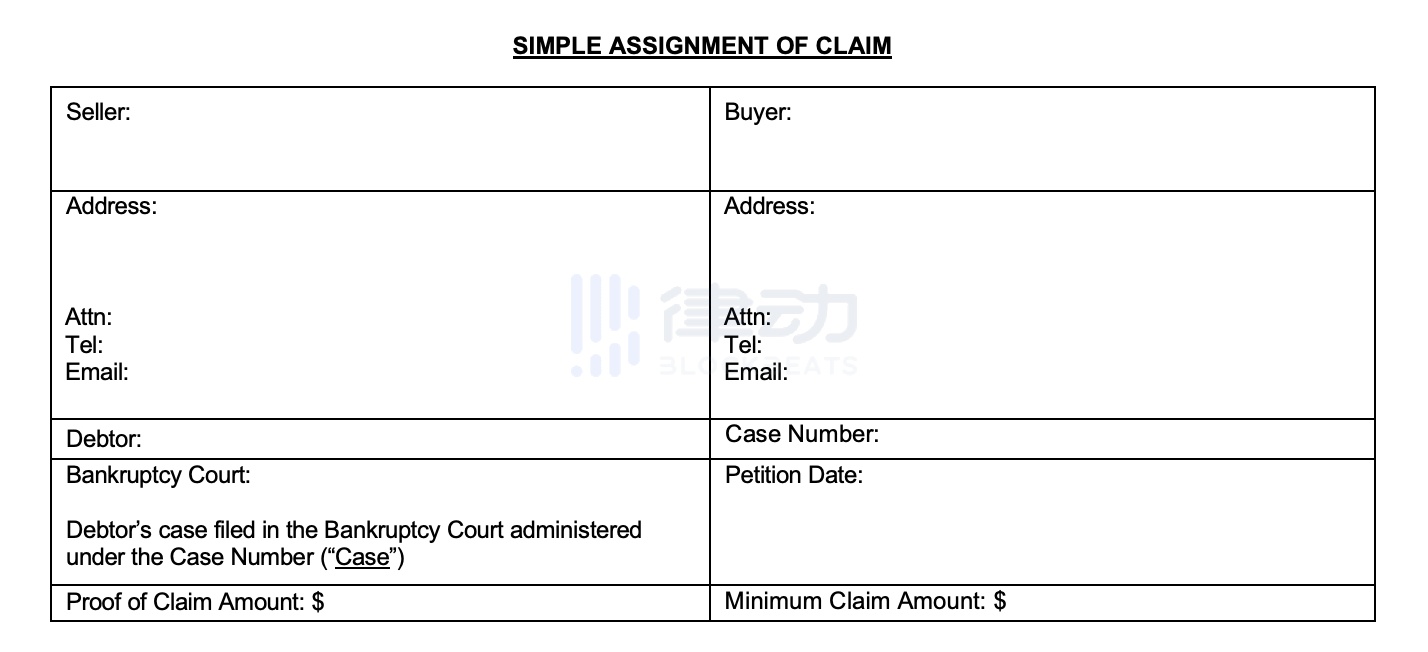

image description

SAC Claim Assignment Agreement

Among other things, claims made on Claims-Market using SAC will be signed before the seller is listed, providing the buyer with a guaranteed delivery. Since all buyers agree to use SAC, transaction costs and delays are minimized if sellers also agree to use SAC.

Negotiating time and money friction is also minimized if a specific change to the SAC is chosen, as the buyer only needs to focus on the seller's specific redline changes to the SAC.

In addition, Claims-Market has developed the Simple Pass Allocation Agreement "SPTA" to facilitate the secondary trading of claims. In some cases, the intermediary will act as a risk-free principal to satisfy the buyer's requirements against the intermediary. In other cases, where an investor may wish to sell a claim to a buyer without having to make the representations and warranties customary to the original creditor, the SPTA allows intermediaries to make representations and warranties that relate only to their own conduct.

first level title

Can GTX be made

Finally, let's briefly summarize and analyze whether GTX can be made, and what advantages and disadvantages exist.

1) With Luna, Three Arrows Capital, FTX and many CeFi institutions going bankrupt and thundering in 2022, the debt trading market for encrypted assets has gradually grown, and may reach a scale of 100 billion US dollars, but it has not yet been affected Pay more attention.

At the same time, the debt transaction on the bankruptcy platform is a very unequal market between buyers and sellers. There are much fewer buyers than sellers. In terms of matching transactions, the platform often charges higher transaction fees than ordinary spot trading platforms. Therefore, this track is indeed a Good business to make money.

2) At present, there are not many players in this field and it is still a blue ocean market, mainly including Xclaim and Claims-Market. Although these two institutions are platforms that have been established for four or five years, according to their official data on the transaction volume of encrypted asset claims, they are 166 million U.S. dollars and nearly 33 million U.S. dollars respectively, each accounting for 1/1000 of the total market size. For a while, late-entry projects such as GTX still have great opportunities to catch up from behind.

3) The core team members of GTX include Su Zhu, Kyle Davies from Three Arrows Capital, Sudhu Arumugam and Mark Lamb from CoinFLEX, and executives from many former encrypted financial institutions. Certain advantages. Coupled with the new narrative of encrypted debt trading, GTX can still gain the preference of some investors.

4) However, based on the previous bankruptcy experience of Su Zhu and several other joint ventures of GTX, as well as the current reputation in the industry, it is not easy for GTX to gain the recognition of investors and the trust of users. For example, the founder of Wintermute posted an article with GTX drew a line and said it would not participate in its investment.

5) After several years of development, Xclaim and Claims-Market currently have their own characteristics in providing creditor's rights trading products, and have also captured a large number of users, and are more comfortable in handling administrative work related to courts in various countries.

The specific product of GTX is planned to be officially launched in 2-3 months. Therefore, the success of the GTX project in the future depends on the user experience after the product release and long-term operation. observation.