想買的人已經買完了:SpaceX 散戶狂歡退潮,真正的拋壓還在8月

- 核心觀點:SpaceX(SPCX)上市後經歷散戶狂熱推動的短暫暴漲,但動能迅速消退,在拋壓擔憂和內部股份解禁預期下,股價連跌三天,回吐全部漲幅至開盤價附近,市場認為「想買的人已買完」。

- 關鍵要素:

- SpaceX上市首日開盤價150美元,隨後六天內漲至225美元歷史高點,市值一度超過微軟,但散戶日度資金流在6月16日見頂後崩潰。

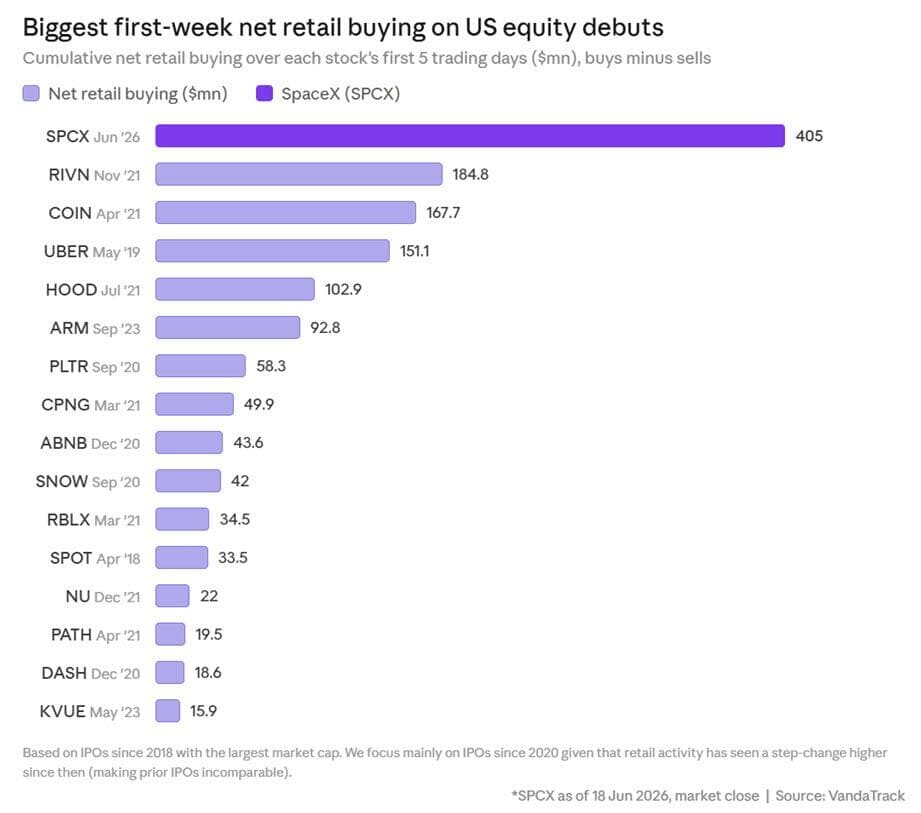

- 上市首週散戶淨買入4.05億美元SPCX,超過同期所有Mag 7個股(合計2.78億美元)及SPY和QQQ ETF的散戶買盤總和。

- 當前僅5%流通盤可交易,但內部人股份將在8-9月逐步解禁,首次20%於財報後釋放,截至9月初最多可出售44%股權,擴大流通盤約900%。

- 散戶資金迅速湧向槓桿產品,如2倍做多SPCX ETF在頭數日吸引6580萬美元,但後續需求遠低於典型狂熱水平。

- 6月16日見頂後,股價連跌三日,週一單日暴跌16.4%,抹去6000億美元市值,盤後觸及150美元上市開盤價,威脅所有二級市場買入者。

- 分析師警告,美股市場(尤其是科技股)當前上漲依賴散戶狂熱和動能,一旦散戶退縮,拋盤壓力可能擴散至儲存和半導體板塊。

Original Author: Tyler Durden (ZeroHedge pseudonym)

Original Compilation: Source: ZeroHedge

Introduction: SpaceX has fallen for three consecutive days, plunging 16.4% on Monday alone, erasing $600 billion in market capitalization and falling back to its opening price of $150. This analysis argues bluntly that everyone who wanted to buy has already bought, and more importantly, the selling pressure hasn't truly arrived yet. This pump-and-dump move utilized only 5% of the circulating shares, while insiders could offload up to 44% of shares by early September.

It started with a bang. SpaceX went public on June 12 with an opening price of $150, well above its IPO price of $135. Within two days, aggressive traders began frantically buying $380 call options expiring in two days, attempting to send the stock price into orbit and trigger a gamma squeeze (forcing market makers to buy the stock to hedge their positions, pushing the price higher).

@zerohedge tweeted: They're really going for it

Canaccord, in a report this morning, described the "wave of renewed optimism" accompanying the SpaceX IPO as follows:

"SPCX's order book shows the market has entered a new level of frenzy. Before this historic IPO, we thought AI optimism was already strong, sometimes excessive, but buying was largely from rational (if euphoric) institutions – large, well-capitalized public companies and PE investors. In our view, SPCX has opened a new chapter, with retail participation surging, pushing the stock into the global top six by market cap and adding the equivalent of half a META in its first week of trading. Its market cap now far exceeds that of sister company TSLA, despite having only about 20% of its revenue. Despite the company name SpaceX, revenue is actually skewed towards connectivity – Starlink contributed $11.39 billion, launch services only $4.1 billion, and AI compute $3.2 billion in 2025."

VandaTrack put it even more dramatically. In a review earlier Monday, it wrote: "SpaceX's first week of trading set a record. Retail investors net bought $405 million of SPCX in the first five trading days, the strongest retail participation in an IPO in recent years. Buying was extremely intense in the first few days, cooling somewhat later in the week. The flow increasingly looks like long-term position building rather than chasing a short-term meme stock."

Figure Note: Retail flows for SPCX in the first five trading days

Source: VandaTrack

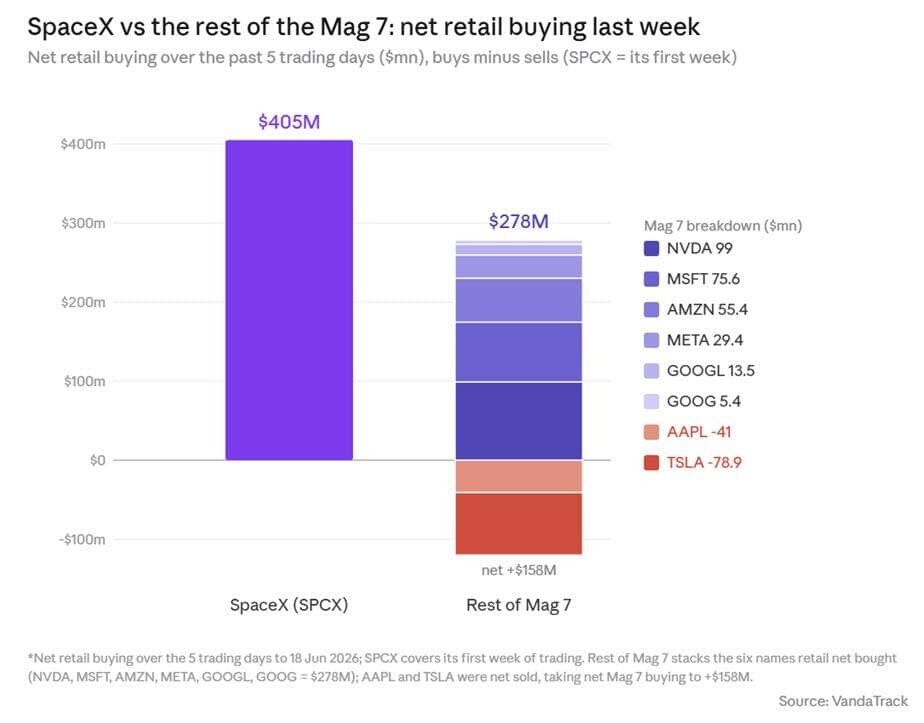

The scale of retail buying of SPCX becomes even more astounding in context. Last week, retail purchases of SPCX exceeded their combined purchases of all other Mag 7 stocks – NVDA, MSFT, AMZN, META, GOOGL, and GOOG – which totaled only $278 million over the five days. Retail buying of SPCX also surpassed the combined retail inflows into the SPY and QQQ ETFs over the same period ($352 million). A stock that only began trading last week is already competing with the market's largest individual stocks and ETFs for retail money.

Figure Note: SPCX retail buying vs. Mag 7 individual stock retail buying comparison

Source: VandaTrack

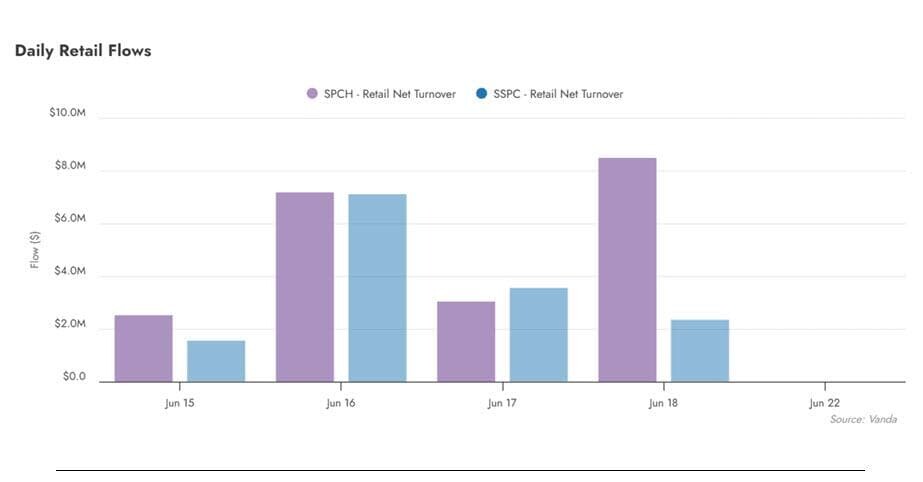

The old playbook was in effect again. As individual stock buying exploded, retail investors swiftly piled into various SpaceX leveraged products, with equally strong demand. In the first few trading days, retail bought $65.8 million of Leverage Shares 2x Long SPCX Daily ETF – a significant amount, but still far below typical levels for retail speculative frenzy. Even so, it dwarfed recent thematic new products: Roundhill's storage ETF (ticker DRAM) attracted only $5.6 million in its first four trading days, and it took DRAM 22 trading days for cumulative retail buying to surpass what the SpaceX leveraged ETF absorbed.

Figure Note: Retail flows comparison between SPCX leveraged ETF and contemporaneous thematic ETFs

Source: VandaTrack

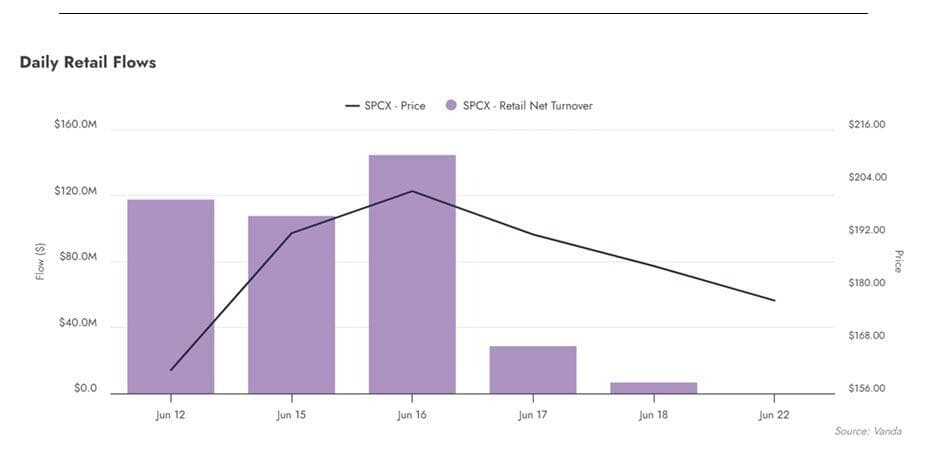

After the initial burst, momentum quickly fizzled, and the fantasy of "riding a reusable rocket into orbit via gamma squeeze" dissipated. June 16 was the peak, with SPCX hitting an all-time high of $225, briefly surpassing Microsoft's market cap. Since then, daily retail flows collapsed, and retail turnover nearly vanished.

Figure Note: SPCX daily retail flows – cliff-like decline after peaking on June 16

Source: VandaTrack

This brings us back to Canaccord's statement. Based on SpaceX's early trajectory, the investment bank judged that "tech stocks can probably maintain momentum in the short term," but it also warned: "There is a more dangerous vacuum beneath these stocks now."

Sure enough, once momentum faded, combined with the market's realization that trillions of shares were about to unlock, the stock fell for three consecutive days, culminating in a crash on Monday. That day, as SpaceX attempted to issue over $20 billion in investment-grade bonds – its first such offering – to replace a much higher-interest bridge loan before the debt market window closed, SPCX plummeted 16.4%, wiping out a record $600 billion in market cap in a single day. Adding in Wednesday's 5% drop and Thursday's 3.5% decline, the stock is now only slightly above its $150 opening price from two weeks ago.

Figure Note: SPCX price action since listing – falling from the $225 high back to near $150

Source: ZeroHedge

Worse still, in after-hours trading, SPCX briefly touched its listing opening price of $150. If it breaks below this level tomorrow, everyone who bought and held on the secondary market will be underwater.

Figure Note: SPCX fell to near its $150 listing opening price in after-hours trading

Source: ZeroHedge

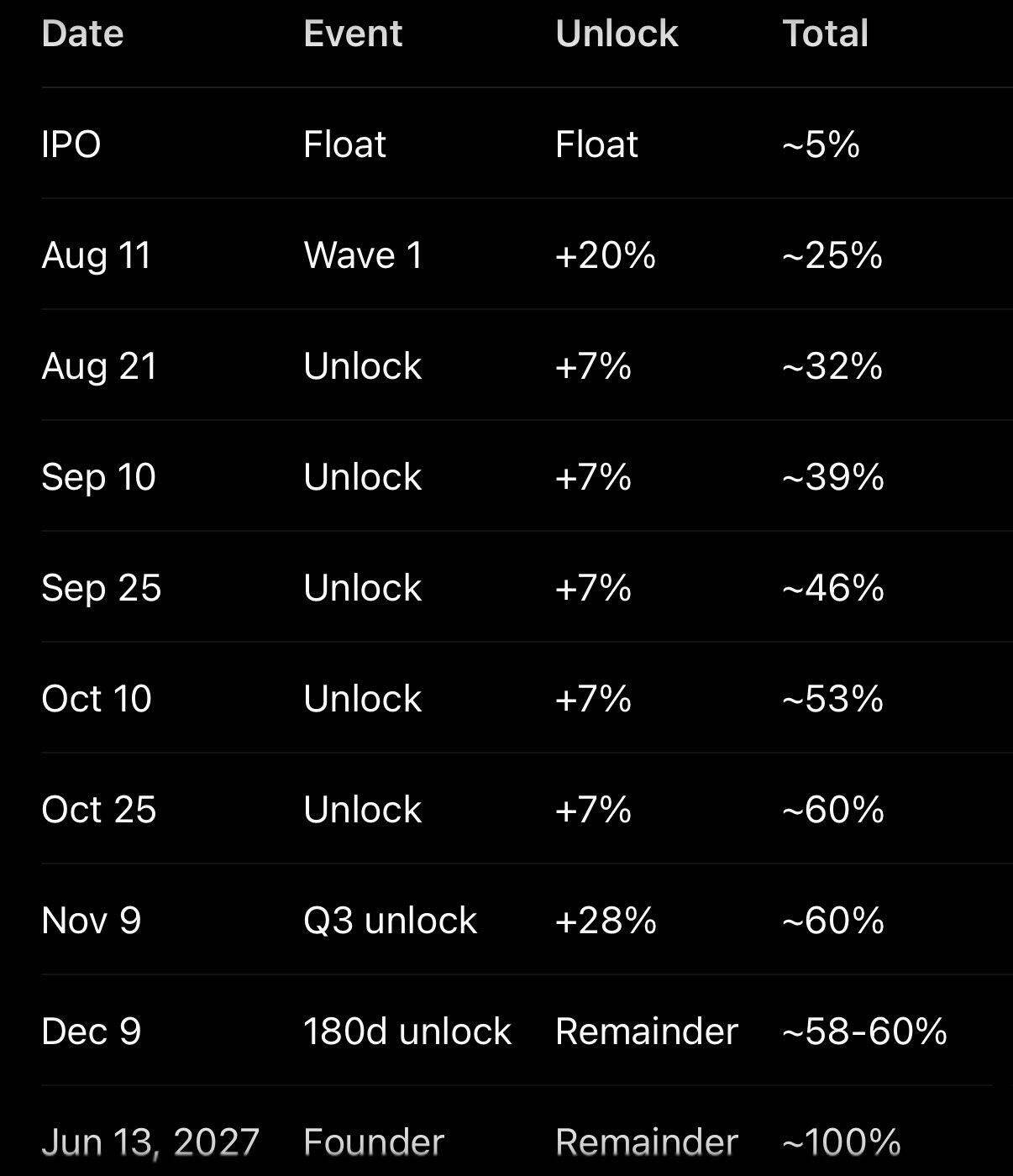

It's particularly worth noting that this pump-and-dump occurred with only 5% of the float available for trading – 95% of the stock remains locked up. But that will soon change.

Figure Note: SPCX unlock structure – currently only 5% float, 95% locked

Source: ZeroHedge

Jeff Jacobson, a strategist at 22V Research, said that after SpaceX reports earnings from early to mid-August, 20% of insider shares will be unlocked. Additionally, if the stock price is 30% above the IPO price, another 10% unlock is triggered; there are also 7% unlocks around August 21 and September 10.

Figure Note: SPCX lockup expiration schedule

Source: 22V Research

Jacobson said insiders could sell up to 44% of their SpaceX shares by early September, expanding the current float by approximately 900%.

In other words, it will only get harder to push the stock price higher. Meanwhile, Michael O'Rourke, Chief Market Strategist at JonesTrading, stated that "the sellers have regained control," adding: "Everyone in the world who wants to buy has already bought."

Bloomberg, commenting on today's decline, wrote that SpaceX's drop "dragged down a large part of the market."

Whether that's truly the case remains to be seen. But in this market – which has been propped up almost entirely by retail frenzy and momentum chasing since the March lows – if retail investors truly become timid, first SpaceX, then the storage bubble, and finally the semiconductor stocks that have fully capitalized on the AI trade...

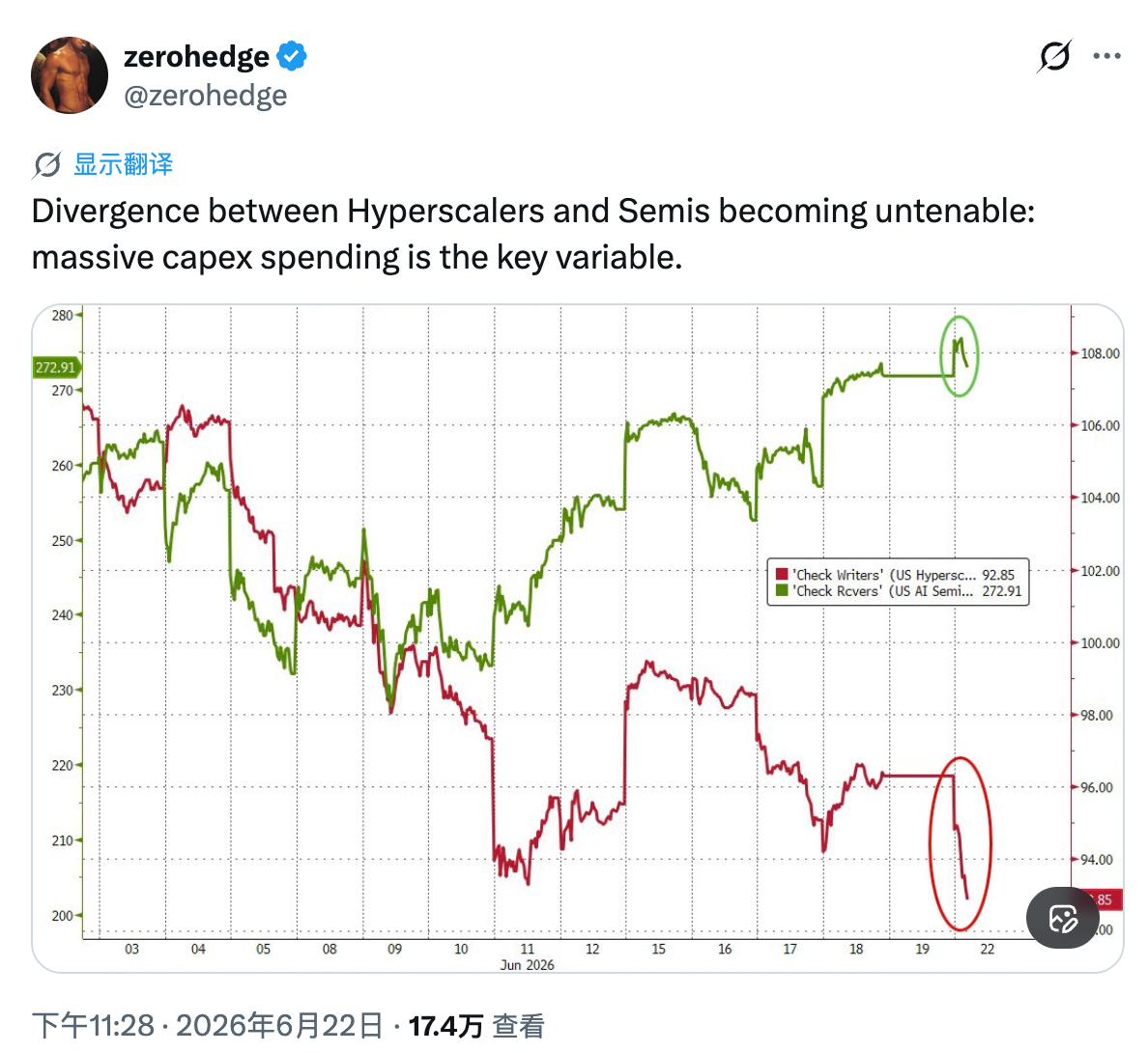

@zerohedge tweeted: The divergence between hyperscalers and semiconductors is unsustainable: massive capital expenditures are the key variable.

...then it's time to invert T.S. Eliot's line: This is how the selling ends, not with a whimper but with a bang.