预测市場概念第一股出現了!

- 核心觀點:Robinhood 透過自建預測市場交易所 Rothera,逐步將原先流向合作夥伴 Kalshi 的訂單轉移至內部體系,並以世界盃為起點,體現了「流量即控制權」的行業邏輯。預測市場的未來競爭,將從牌照之爭轉向渠道之爭。

- 關鍵要素:

- Robinhood 與 Kalshi 曾於 2025 年 3 月合作,Robinhood 提供用戶入口,Kalshi 提供底層市場與清算。Robinhood Q1 預測市場相關收入達 1.47 億美元。

- 2026 年 1 月,Robinhood 與 Susquehanna 收購受 CFTC 監管的衍生品交易所 MIAXdx 90% 控制權,並將其重組為 Rothera Exchange,取得獨立營運預測市場的牌照與清算資格。

- 2026 年 6 月世界盃期間,Robinhood 首次將部分賽事合約(包括單場勝負、冠軍歸屬、總進球數等)訂單導向 Rothera 撮合,標誌著訂單轉移正式啟動。

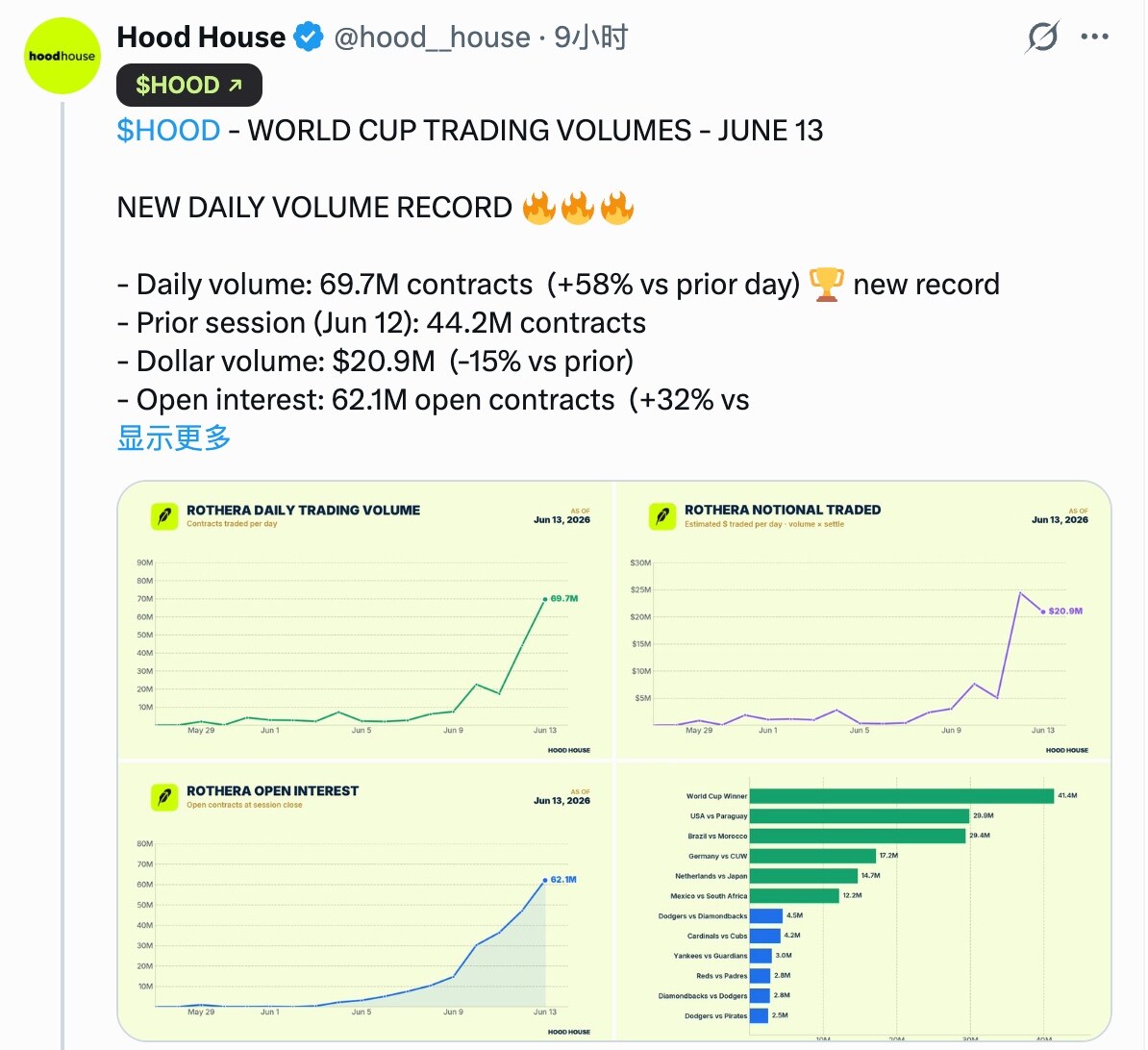

- Rothera 上線初期表現強勁,6 月 12 日完成 4420 萬份合約交易(約當 2440 萬美元),6 月 13 日完成 6970 萬份合約(約 2090 萬美元)。

- Robinhood 掌握數千萬零售用戶入口,用戶不關心訂單最終成交場所,只需體驗一致,這使得渠道方的整合能力成為核心稀缺資源。

- Piper Sandler 分析師估算,透過 Robinhood 渠道完成的交易量曾占 Kalshi 總交易量的 25%-35%,世界盃後此比例將快速下降。

Original | Odaily Planet Daily (@OdailyChina)

Author|Azuma (@Azuma_eth)

The World Cup has kicked off, and the total trading volume across prediction markets is hitting new highs. However, Kalshi, the industry leader, is probably not feeling too great right now.

The reason isn't fluctuations in Kalshi's own business data, but rather the "sudden" emergence of another formidable rival following Polymarket, and this opponent was once its most important ally.

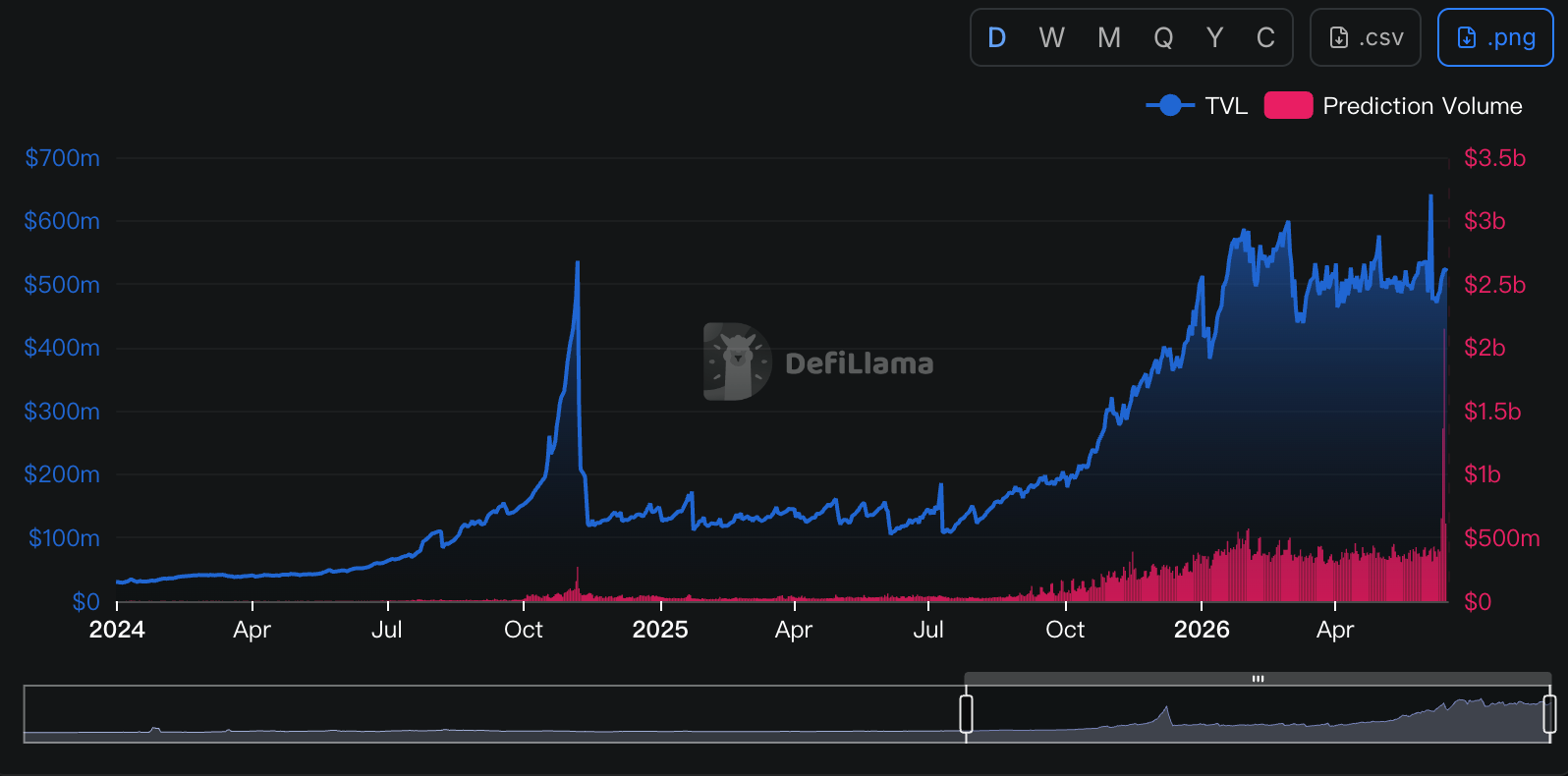

- Odaily Note: Data sourced from Defillama.

Kalshi's Most Important Traffic Channel – Robinhood

Let's rewind to March 2025. At that time, Kalshi announced a partnership with the US online brokerage Robinhood. The latter would leverage the former to offer prediction market trading services to its users, allowing them to place bets on events such as politics, economics, and sports.

From a business model perspective, this was a classic "win-win" – Robinhood, responsible for user access and trade distribution, could directly use Kalshi's mature products; Kalshi, responsible for the underlying market, matching, clearing, and regulatory compliance, could tap into the massive retail user base that Robinhood commanded.

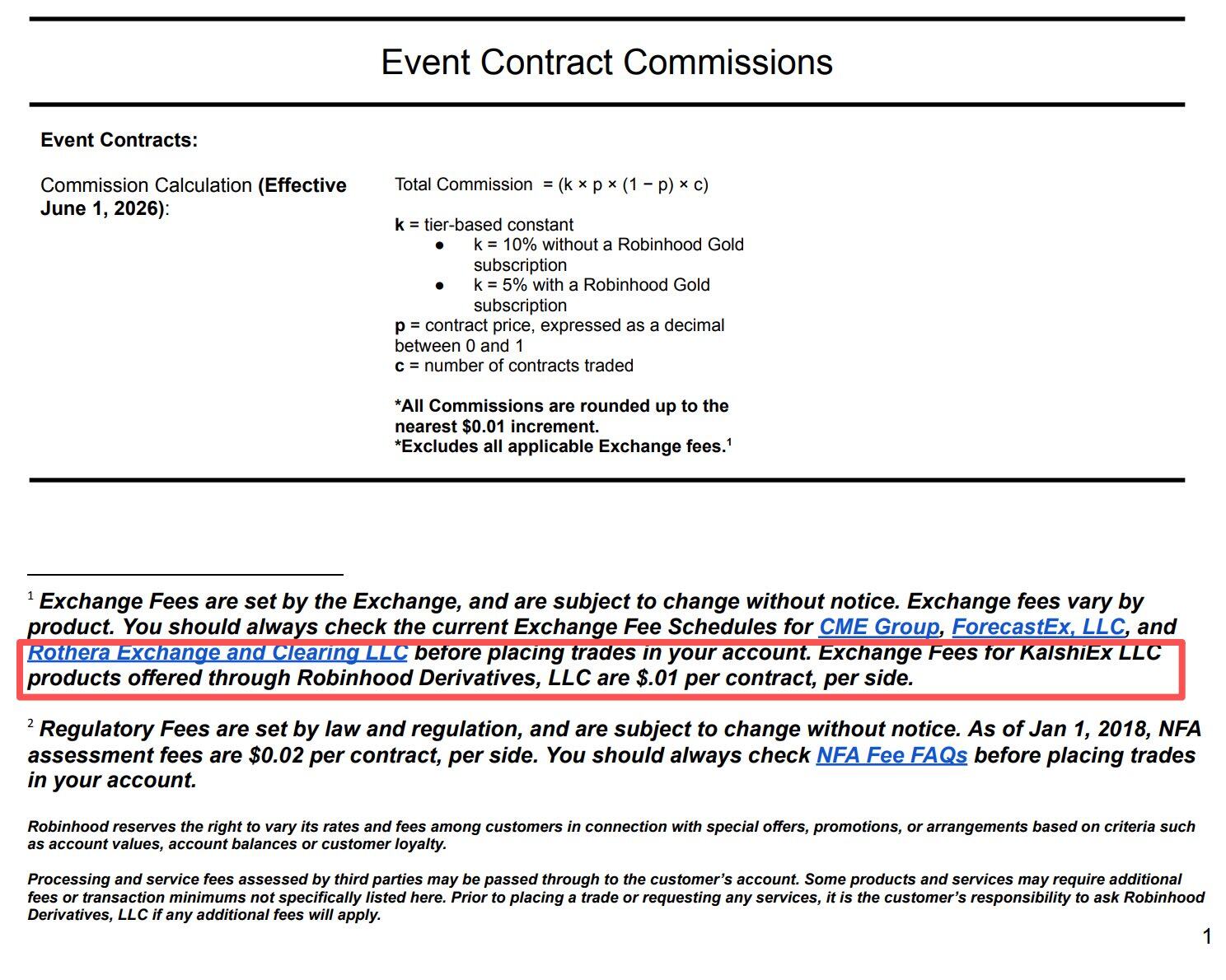

The subsequent story proved the "win-win" outcome of this partnership. Through Robinhood's distribution channels, Kalshi indirectly gained a huge influx of users and trading volume. Piper Sandler analysts estimated that "trading volume completed through the Robinhood channel accounted for approximately 25%-35% of Kalshi's total volume." These orders ultimately translated into revenue for both parties – Robinhood charges a separate fee for all Kalshi event contracts traded through its channel, $0.01 per contract per side, and then splits the fee with Kalshi (the specific ratio was not disclosed).

The Q1 earnings report disclosed at the end of April this year showed that Robinhood executed 8.8 billion event contracts in Q1, driving "Other Transaction Revenue" up 320% year-over-year to $147 million. Prediction markets have become the brightest new engine in Robinhood's product line in terms of growth rate.

But recently, this relationship has seen some subtle shifts.

Robinhood's Ambition: Reclaiming the Pie Shared with Kalshi

As internet history has proven countless times, when a channel gains enough influence, it will no longer be satisfied with just being a channel. Robinhood is no exception.

Although the partnership with Kalshi has brought considerable revenue to Robinhood, with prediction markets becoming one of the fastest-growing new businesses on its platform, Robinhood is no longer content with the current profit-sharing arrangement.

In their cooperation model, Kalshi was responsible for providing the market and infrastructure, while Robinhood was responsible for providing users and order flow. However, as the partnership deepened, Robinhood gradually realized that what was truly scarce might not be the market itself, but the user gateway it firmly controlled. After all, for most Robinhood users, they don't care whether their orders are ultimately executed on Kalshi or another platform – users only see a trading entry point within the Robinhood App, not the underlying infrastructure provider.

In other words, Robinhood always held one of the most important resources in the prediction market – distribution capability. Since users belong to Robinhood, why should orders flow to others?

In fact, while Robinhood was quickly validating prediction market demand using Kalshi, a parallel Plan B was also being initiated shortly thereafter.

In November 2025, Robinhood announced a joint venture with Wall Street quantitative trading giant Susquehanna and planned to acquire the CFTC-regulated derivatives exchange MIAXdx. According to official statements, the joint venture would operate an independent futures and derivatives exchange and clearinghouse in the future, with the prediction market being one of its key strategic areas. At the time, many outsiders viewed it more as an infrastructure investment, but as more information was disclosed, people gradually realized that Robinhood's goal went far beyond just finding a new partner for prediction markets.

In January 2026, the transaction was officially completed. Robinhood and Susquehanna obtained a 90% controlling stake in MIAXdx, along with a complete CFTC regulatory framework, including Designated Contract Market (DCM) and Derivatives Clearing Organization (DCO) qualifications. Subsequently, MIAXdx was renamed Rothera Exchange, and its clearinghouse was renamed Rothera Clearing.

At this point, Robinhood already possessed the core elements needed to independently operate a prediction market. The only missing piece was a mature product comparable to Kalshi, but for Robinhood, which has rich experience in developing internet products, this was clearly not a difficult task.

Rothera's Opportunity: The World Cup

In June 2026, after about six months of accelerated development, the Rothera product gradually took shape, and Robinhood finally made the move that seemed almost inevitable – to gradually redirect the orders that once went to Kalshi into its own controlled system.

Robinhood deliberately chose an excellent debut battleground for Rothera – the World Cup. For prediction markets, the World Cup is undoubtedly one of the most traffic-generating trading themes. Whether it's match outcomes, progression results, or the championship winner, related markets can attract a large number of new users to participate in trading within a short period. For a newly launched platform like Rothera, there is no better scenario for a cold start than the World Cup.

According to Robinhood's official disclosure, during this World Cup featuring a total of 104 matches, some event contracts will be routed to Rothera for matching and clearing, including markets for individual World Cup match results, the final World Cup champion, and total goals scored in individual matches. Compared to the previous model of relying entirely on Kalshi, this marks the first time Robinhood has redirected a significant volume of prediction market orders into its own trading system.

Looking at the results, Rothera clearly seized this opportunity. According to data disclosed by Hood House, an investment research self-media organization tracking Robinhood's developments, on June 12, Rothera completed 44.2 million contracts, corresponding to a trading volume of approximately $24.4 million; on June 13, Rothera completed 69.7 million contracts, corresponding to a trading volume of about $20.9 million. Although these numbers still lag behind Kalshi's popular markets, which often see hundreds of millions of dollars in volume, considering that Rothera had only been live for a few days, this performance is already quite successful.

For Robinhood and Kalshi, this means the balance of their partnership has begun to tilt. On Robinhood's side, the transaction fees that previously had to be shared with Kalshi can now be retained more within its own ecosystem. On Kalshi's side, this signals that one of its most important growth engines has started to show signs of weakening.

And the World Cup is clearly just the beginning of Rothera's encroachment on Kalshi. Looking further ahead, Robinhood will inevitably expand Rothera's coverage to more sporting events, as well as topics like economics and politics, and those orders that once flowed to Kalshi will be sequentially intercepted by Rothera.

Since Robinhood and Kalshi have never publicly disclosed the profit-sharing ratio between them, we cannot know the exact dollar value of this interception. However, considering that Robinhood achieved $147 million in prediction market-related revenue in just Q1 alone, and that the Q2 World Cup and the longer-term midterm elections can undoubtedly generate even larger trading activity, on an annual basis, the value of this interception could potentially reach several hundred million dollars.

Who Controls Distribution, Controls Everything

The narrative of Robinhood and Kalshi transitioning from allies to rivals once again illustrates a logic repeatedly validated in the internet market – Products are easy to build, traffic is hard to find; whoever controls distribution, controls everything.

In the past few years, the market generally believed that Kalshi's core moat came from its regulatory licenses, exchange qualifications, and clearing capabilities. Therefore, brokerages like Robinhood, as well as various media, communities, and traffic platforms, were essentially just channel partners and traffic gateways for Kalshi. However, the emergence of Rothera has proven one thing: in an era of severe product homogenization, the product itself may not be the most important factor. What is truly scarce are the users.

Where users are, liquidity follows; where liquidity is, the market exists. When Robinhood controls the gateway for tens of millions of retail users, it is fully capable of directing these users to any trading venue. For users, they don't care whether their orders are ultimately executed on Kalshi or Rothera; as long as the experience is not significantly different, it doesn't matter who is matching and clearing behind the scenes.

If the theme of the prediction market industry over the past few years was the market competition between Polymarket and Kalshi, then the theme for the next few years might become a battle of channels. Robinhood incubating Rothera is, in essence, a reverse integration initiated by the channel side against the market side. And as more platforms with traffic gateways begin to realize the strategic value of prediction markets, similar stories are likely to continue happening. Whether it's exchanges, brokerages, social platforms, or media platforms, they all have the potential to become new prediction market gateways.

When gateways begin to control the market and channels start to have pricing power, the ultimate winner in the prediction market industry might no longer be the platform responsible for matching orders, but the entity that is closest to the user and best able to control distribution.

This was the case in the internet era, and it was the case in the mobile internet era. This time, it's no different.