SEC delays "stock token" innovation exemption—who is fiercely opposing it?

- Core Viewpoint: The U.S. SEC originally planned to introduce an "innovation exemption" for the tokenization of US stocks. However, due to strong opposition from traditional Wall Street forces and internal SEC factions citing concerns over liquidity fragmentation, compliance risks, and legal loopholes, the plan has been delayed, causing a sharp short-term decline in the cryptocurrency market.

- Key Elements:

- The SEC postponed the "innovation exemption" plan, which was intended to allow the provision of on-chain trading services for US stocks under more relaxed conditions, viewed as a significant signal supporting tokenized securities.

- Affected by this negative news, BTC fell below 76,000 USDT, and ETH dropped below 2,100 USDT; the related concept token ONDO erased its gains, falling 6.4% in 24 hours to 0.382 USDT.

- The opposition camp is primarily composed of traditional Wall Street powers such as Citadel Securities and SIFMA, who worry about market liquidity fragmentation, lack of AML/KYC compliance, and legal and technical loopholes in the execution of token equity rights.

- SEC Commissioner Hester Peirce, known as the "Crypto Mom," also tends to limit the scope of the exemption, supporting tokenization led only by the issuers themselves, rather than third-party issuance of synthetic assets.

- Despite the regulatory slowdown, crypto-native forces (such as Ondo and Hyperliquid) and Wall Street institutions (such as DTCC, Nasdaq, and ICE) are accelerating their respective deployments in tokenized assets and blockchain frameworks.

Original | Odaily Planet Daily (@OdailyChina)

By Azuma (@azuma_eth)

In the early hours of May 23, Beijing time, Bloomberg reported, citing sources, that the U.S. Securities and Exchange Commission (SEC) has delayed the originally planned introduction of the "Innovation Exemption" program. This program was intended to greenlight products related to "tokenized U.S. stocks," but the SEC decided to put it on hold due to numerous concerns raised by market participants.

Following this bearish news, the cryptocurrency market saw a sharp short-term decline, with BTC falling below 76,000 USDT and ETH dipping below 2,100 USDT. Concepts related to "tokenized U.S. stocks" were hit even harder; ONDO gave back all the short-term gains it made yesterday, indirectly spurred by the "CSRC penalties on brokerages like Tiger Brokers, Futu, and Changqiao," and as of press time, it was trading at 0.382 USDT, down 6.4% in 24 hours.

Innovation Exemption Halted at the Last Moment

Since Chairman Paul Atkins took office, the SEC has shifted away from its previous tough stance of "enforcement as regulation," tending to provide a compliance sandbox for the crypto industry.

Earlier this week, market rumors emerged that the SEC would announce an exemption proposal as early as this week, allowing trading platforms to offer on-chain token trading services for listed securities (such as NVDA, AAPL, TSLA, etc.) under more relaxed regulatory conditions. Driven by SEC Chairman Paul Atkins and Commissioner Hester Peirce, the exemption aims to create a legal testing ground for tokenized securities. The market interpreted this as a significant signal that U.S. regulators are further shifting towards supporting tokenized securities.

However, this innovation exemption, originally set to be unveiled to the public as early as this week, was abruptly halted just before the finish line. Sources reveal that the SEC has now returned the draft and has begun intensively consulting again with stock exchanges and other market participants.

From a "full green light" to "emergency brakes," what kind of resistance did the SEC face? In this epic battle over "putting U.S. stocks on the chain," who is fiercely opposing it?

The Main Opposition: Wall Street Again

Similar to the CLARITY Act, which also faces resistance (see CLARITY Review Delayed: Why is there such deep division in the industry?), at the forefront of the camp fiercely opposing this exemption proposal are traditional Wall Street powers represented by Citadel Securities and the Securities Industry and Financial Markets Association (SIFMA).

Months ago, when the policy was still in the trial balloon stage, these traditional financial giants had already submitted strongly worded opposition letters to the SEC. Overall, Wall Street's core arguments against the proposal focus on the following three aspects.

First, concerns about potential liquidity fragmentation in the market. Institutions like Citadel Securities warned that allowing various third parties to bypass issuers and issue "synthetic U.S. stocks" indiscriminately would lead to U.S. stock assets being fragmented and scattered across countless DeFi platforms lacking interconnection, depth, and price transparency. This would not bring efficiency but would instead leave investors unable to determine the real value of their tokenized stocks at any given moment.

Second, concerns that tokenized U.S. stocks could threaten traditional compliance defenses. On anonymous or pseudonymous public blockchain networks, how to ensure that transactions of these third-party tokens do not become a breeding ground for money laundering? Wall Street giants believe that the current technical capabilities of decentralized platforms are simply insufficient to strictly enforce core investor protection mechanisms like AML and KYC.

Third, technical and legal gaps still exist. Citing opinions from legal experts, institutions pointed out that allowing an unauthorized third-party crypto platform (without authorization from companies like Apple or Microsoft) to "grant token holders voting rights and dividend distribution" on-chain remains uncertain under the current legal framework and technical pathways.

Reservations Exist Within the SEC Itself

It's worth noting that this wave of opposition comes not only from Wall Street's "vested interests" but also includes prudent reservations within the SEC itself.

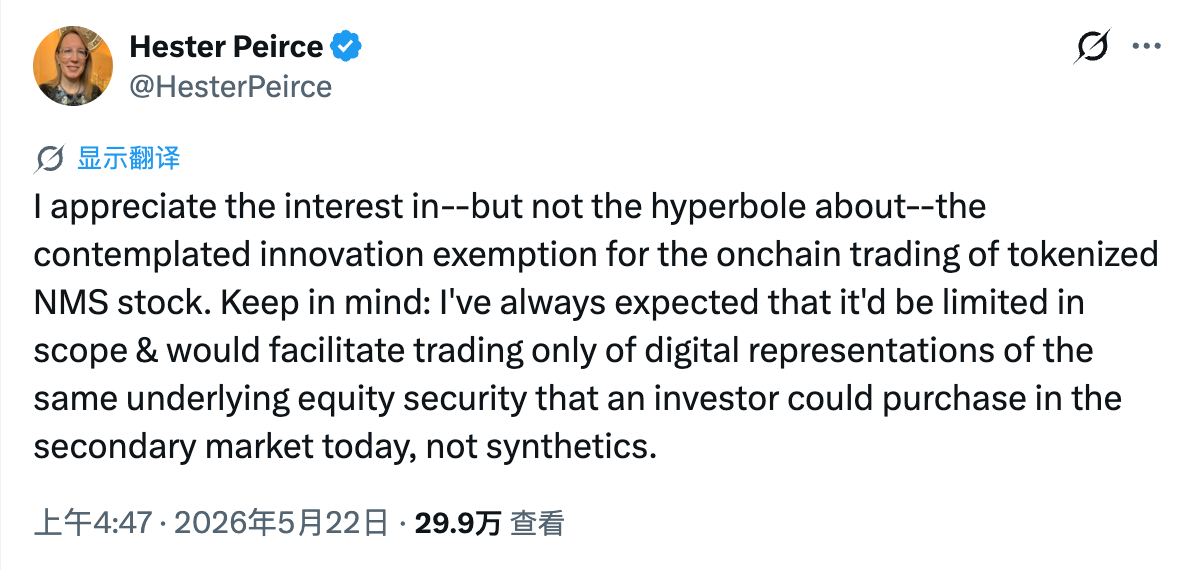

Hester Peirce, an old ally of the crypto community affectionately known as "Crypto Mom," publicly stated on X yesterday that she "shifted sides," indicating that the scope of this exemption should be strictly limited.

Peirce stated that what the SEC should allow are attempts by "the issuer itself or its affiliates" to digitize or tokenize their own stocks on the chain; it should not allow a proliferation of third-party synthetic assets outside regulatory control. In other words, the "U.S. stock tokens" that Peirce wants to see should be led, authorized, or endorsed by the specific listed company itself (the issuer), and must guarantee investors enjoy equal rights (such as dividends, voting rights, etc.) as ordinary shareholders, rather than the more mainstream derivative synthetic tokens issued by third parties that track the price performance of the underlying stock.

Even Peirce, a staunch advocate for crypto innovation, chose to side with "limiting the scope of the exemption," highlighting the significant legal and compliance hurdles the proposal faces.

What Does the Future Hold for Tokenized Stocks?

This week's "suspension" is undoubtedly a blow to the RWA (Real World Assets) sector, which was on the verge of exploding. The sharp short-term decline in related tokens like ONDO reflects that the market's previous expectations for "full on-chain compliance of U.S. stocks" were overly optimistic. However, it is undeniable that regardless of the regulatory stance's vacillation, the trend of combining U.S. stock assets with blockchain technology is already an irreversible torrent. In the shadow of this regulatory game, both crypto-native forces and orthodox Wall Street institutions are racing madly on their respective tracks.

- On one hand, crypto-native forces are breaking in from the bottom up. Crypto-native projects like Ondo, xStocks, and MSX are actively bringing U.S. stock assets onto the chain, while platforms like Hyperliquid, Trade.xyz, and major CEXs are using perpetual contracts to indirectly provide global crypto users with windows to invest in U.S. stocks. This grassroots innovation demand is constantly forcing regulators to provide clear answers.

- On the other hand, Wall Street itself is also accelerating its layout of related businesses. The Depository Trust & Clearing Corporation (DTCC) plans to officially launch limited production trading of tokenized assets this July, with a broader expansion in October; Nasdaq is also rapidly developing a blockchain-based stock issuance framework; Intercontinental Exchange (ICE) has chosen to collaborate with leading crypto exchange OKX to jointly advance the development of tokenized stocks and crypto-related products.

In essence, this delay of the exemption is a fierce collision between the innovative attempts of emerging forces and the defensive mechanisms of traditional powers. Based on the current progress of events, the SEC has not made a final decision on the revised draft, meaning the "Innovation Exemption" is not completely dead. However, it is foreseeable that amidst the fierce backlash from Wall Street giants and internal revisions of opinion within the SEC, even if this exemption is eventually reintroduced, its aggressiveness and scope of application will likely be subject to a certain "discount."

The dream of fully liberalizing "tokenized stock" trading may still have a long way to go amidst regulatory tug-of-war, but the door to asset tokenization has been kicked open and is destined never to close again.