瑞银中国AI产业链调研:光互连和SiC升温,胜宏押注Rubin PCB

- Quan điểm chính: Nhu cầu về cơ sở hạ tầng AI đang lan tỏa từ GPU sang nhiều thành phần phần cứng khác như PCB, kết nối quang, làm mát bằng chất lỏng, đế SiC. Các công ty liên quan tại Trung Quốc đã đưa ra lộ trình và mục tiêu sản lượng đầy tích cực, nhưng phần lớn là định hướng từ ban lãnh đạo. Việc thực hiện vẫn phụ thuộc vào sản xuất hàng loạt, chứng nhận và các hạn chế bên ngoài.

- Các yếu tố chính:

- Biren Technology lên kế hoạch ra mắt GPU BR20X vào nửa cuối năm 2026, BR30X/BR31X dự kiến thương mại hóa vào năm 2028, nhưng quy trình tiên tiến và khả năng tương thích hệ sinh thái là những nút thắt trong triển khai.

- Shenghong Technology dự kiến đầu tư tài sản cố định năm 2026 không quá 18 tỷ CNY; nền tảng Rubin của NVIDIA là động lực tăng trưởng PCB chính của họ, với mục tiêu thị phần khách hàng khoảng 50%.

- Ban lãnh đạo TY Tech cho biết đơn đặt hàng SiC đã đầy; họ đang chọn lọc tăng giá với các đơn hàng gấp từ khách hàng nhỏ và đặt mục tiêu tỷ lệ xuất xưởng đế 8 inch lên 50% vào năm 2026.

- Xizhi Technology nắm giữ khoảng 88% thị phần trong các giải pháp kết nối quang độc lập, tập trung vào các giải pháp LPO/NPO để giảm bớt nút thắt kết nối trong các cụm AI quy mô lớn.

- Lens Technology thâm nhập lĩnh vực cáp quang lõi rỗng thông qua mua lại; ban lãnh đạo mảng làm mát bằng chất lỏng đặt mục tiêu doanh thu tài khóa 2026 đạt hàng tỷ CNY, nhưng thiếu các công bố công khai để xác nhận.

- Các hạn chế xuất khẩu từ bên ngoài vẫn ảnh hưởng đến nhịp độ của chuỗi cung ứng phần cứng AI nội địa. Phần lớn thông tin là từ trao đổi với ban lãnh đạo và khảo sát của bên bán, không đồng nghĩa với kết quả kinh doanh đã được thực hiện.

TL;DR

- After UBS surveyed five Chinese tech hardware companies, AI infrastructure demand remains a common theme.

- Victory Giant Technology plans to cap fixed asset investment in 2026 at no more than 18 billion yuan, with the Rubin platform being the focal point for PCB growth.

- Several key figures came from management discussions; realization depends on mass production, certification, and external constraints.

In a research note published on June 26, UBS detailed the expanding demand diffusion across China's AI hardware chain: AI infrastructure demand remains strong, with the pull extending beyond just GPUs to include PCBs, optical interconnects, liquid cooling, SiC substrates, and optical communication materials.

The news value of this material lies not in order changes from a single chip company, but in several segments simultaneously providing more ambitious timelines and capacity targets. Biren Technology has laid out its GPU roadmap through 2028. Victory Giant Technology plans fixed asset investment of no more than 18 billion yuan in 2026. Management at SICC stated that SiC orders are saturated and that they are selectively raising prices for urgent small-customer orders.

This content primarily stems from management communications and company guidance during UBS's research, not formal earnings forecasts. They are more like a thermometer for AI hardware chain demand, reflecting industry heat but not directly equating to realized revenue and profits.

Domestic GPU Roadmap Reaches 2028, Victory Giant Bets on Rubin PCBs

The timeline provided by Biren Technology is one of the most direct signals for domestic AI computing power in the research material.

The company told Caijing that the BR20X is expected to commercialize in 2026, with the BR30X/BR31X expected in 2028. Management communications within the UBS material further indicated that the BR20X series GPUs are planned for launch in the second half of 2026, featuring upgrades in computing power, memory capacity, and interconnect bandwidth compared to the previous generation.

Catching up in domestic GPUs depends not only on single-chip computing power but also on whether memory, interconnects, packaging, and the software ecosystem can keep pace. For AI training and inference clusters, bottlenecks often occur at the inter-chip, inter-server, and system scheduling levels, not just theoretical computing power.

The limitations are also clear. Advanced process nodes, advanced packaging, customer volume production timelines, and software ecosystem adaptation will all impact the subsequent rollout of the BR20X and BR30X. The external export control environment will continue to influence the pace of the domestic AI hardware supply chain.

Closer to near-term orders and capital expenditure is the PCB guidance from Victory Giant Technology.

Management stated that overall raw material costs for AI PCBs are stable, cost pass-through for new generation products is relatively smooth, and they expect gross margins for the FY2026 to be roughly flat compared to FY2025. The proportion of AI-related revenue is expected to rise from below 50% to 60%-70%.

The Rubin platform is the most watched growth driver. The research material stated that Victory Giant maintains a majority share in NVIDIA's Rubin compute tray HDI, consistent with the situation for the GB300 platform, with an overall customer share target of approximately 50%. As this claim hasn't been verified by public announcements, it is better understood as a management target and sell-side research information. If realized, NVIDIA's new platform iterations will continue to drive China's high-end PCB supply chain.

The expansion figures also require precise interpretation. Public information shows Victory Giant's total investment for 2026 will not exceed 20 billion yuan, with fixed asset investment capped at 18 billion yuan, primarily allocated to Huizhou Factories 10-13. This scale indicates that AI server PCBs have been placed by management as a core capacity direction for the coming years.

The material solution for the orthogonal backplane required by Rubin Ultra is not yet fully finalized. The company stated there are no delays related to this, but they are still evaluating multiple material and supplier combinations, including Q-glass and PTFE. While the order direction is relatively clear, the process and material routes are still under selection.

Optical Interconnects and Liquid Cooling Emerge as Supporting Demands for AI Clusters

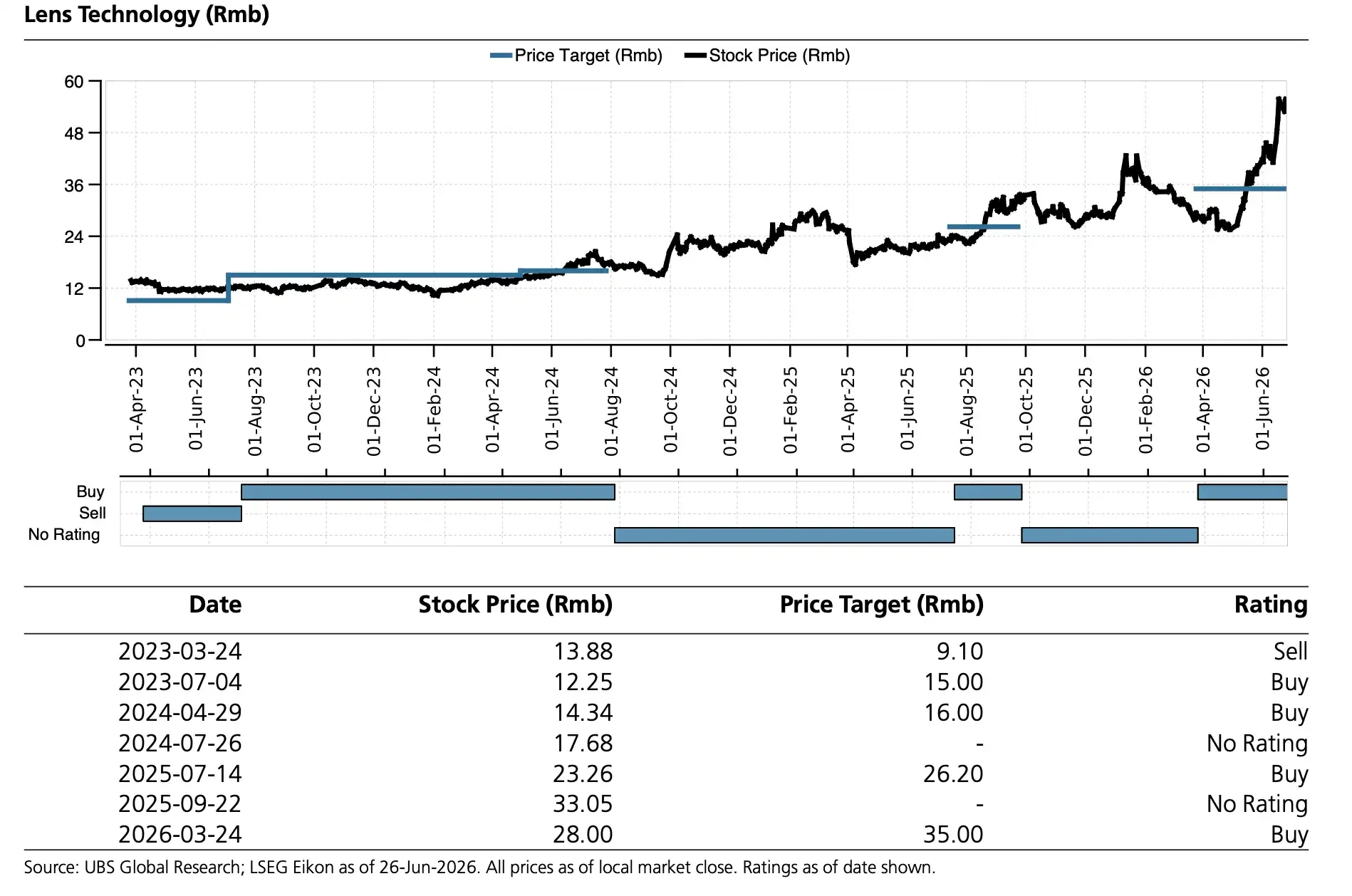

As AI clusters continue to scale up, the importance of interconnects and thermal management rises. Lightmatter and Lens Technology provide two pieces of supporting evidence.

UBS research materials state that Lightmatter holds approximately an 88% market share in standalone scale-up optical interconnect solutions, focusing on LPO, NPO, and similar approaches serving large-scale GPU and ASIC clusters. Their optical computing processors use a method of vertically stacking electronic ICs and silicon photonics via 3D TSV to offload certain computing tasks to the silicon photonics layer, thereby reducing latency and decreasing reliance on advanced process nodes.

The key point of such solutions isn't "optical computing replacing GPUs," but rather that the larger the AI cluster, the more prominent the interconnect bottleneck becomes. If LPO, NPO, and silicon photonics packaging can achieve stable mass production, they could provide incremental benefits in bandwidth, power consumption, and latency for large-scale clusters.

Lens Technology's AI infrastructure layout stems from optical communications and liquid cooling. Public reports indicate that Lens Optical Electronics strategically acquired a controlling stake in Shenzhen Tongsheng Optoelectronics Co., Ltd. in June 2026, entering the field of hollow-core fiber optic cables. Management targets in the UBS research show that the optical communication business is expected to make a more meaningful contribution to the profit and loss statement from 2027 onwards, with a revenue potential of approximately 10 billion yuan.

On the liquid cooling front, the management target is to become the largest shareholder of Yuans Tech, with liquid cooling business revenue potentially reaching a scale of several billion yuan in FY2026. The unit value for cold plates, manifolds, and UOD is estimated at $40,000-$50,000. These figures lack verification from public announcements and should still be understood within the context of targets and guidance.

Chart showing Lens Technology's stock price vs. target price historical trends along with historical rating and target price adjustments.

SiC Orders Saturated, 8-Inch Shipment Target Raised to 50%

On the power device chain, SICC provided signals closer to "supply-demand tightness is already impacting certain prices."

A company press release cited Fuji Keizai data stating that in 2025, it held the global number one market share for SiC substrates, including 6-inch and 8-inch, with an 8-inch share of 51.3%. Further management communications in the UBS research material indicated strong current demand and saturated orders. Overall prices remained stable in Q1 2026, but selective price increases were implemented for urgent small-customer orders.

Management's target for 2026 is for 50% of shipments to come from higher-margin 8-inch SiC substrates to drive gross margin expansion. If achieved, this target would directly impact the company's product mix and profitability.

Historically, SiC demand was primarily driven by electric vehicles, photovoltaics, and energy storage. Now, high-power AI servers and data center power systems are also becoming sources of new demand. HVDC, SST, AI glasses, and advanced packaging are also listed as potential drivers.

The key takeaway here is not that SiC demand has suddenly shifted from automotive to AI, but that AI data centers continue to expand the demand boundary for power semiconductors. Saturated orders and selective price increases indicate that supply tightness is already affecting prices in certain customer and urgent-order scenarios.

Whether prices can continue to rise depends on the ramp-up of 8-inch capacity, customer qualification, and the pace of downstream demand. If capacity release outpaces order growth, the potential for price increases may be weakened. If data center demand materializes faster than expected, the scope for gross margin improvement at SICC will become clearer.

Order Direction is Clear; Challenges Remain in Mass Production and Constraints

This set of research information collectively points to one change: AI hardware demand is spreading outwards along GPU, PCB, optical interconnects, liquid cooling, and SiC, with the Chinese supply chain providing more proactive capacity and product roadmaps across multiple segments.

However, it is not suitable to be framed as "a comprehensive breakthrough in domestic AI hardware." Biren Technology's GPU roadmap remains constrained by process nodes and ecosystem limitations. Victory Giant's Rubin-related market share awaits platform mass production and material solution finalization. Lightmatter's optical interconnects and optical computing require large-scale customer validation. Lens Technology's contributions from optical communications and liquid cooling are primarily expected in 2026-2027. Whether SICC's selective price increases can be sustained depends on 8-inch capacity and data center demand realization.

The broader external constraints remain in areas related to advanced process nodes, advanced packaging, high-end GPUs, and cloud provider capital expenditure. The closer the AI hardware chain gets to these positions, the more susceptible it becomes to policy and supply chain constraints.

The most valuable aspect of these figures is that they show AI infrastructure orders are diffusing to more hardware segments. The boundaries that need to be maintained are equally clear: most figures are still management targets and research information; actual realization awaits customer mass production, material finalization, and the external environment.