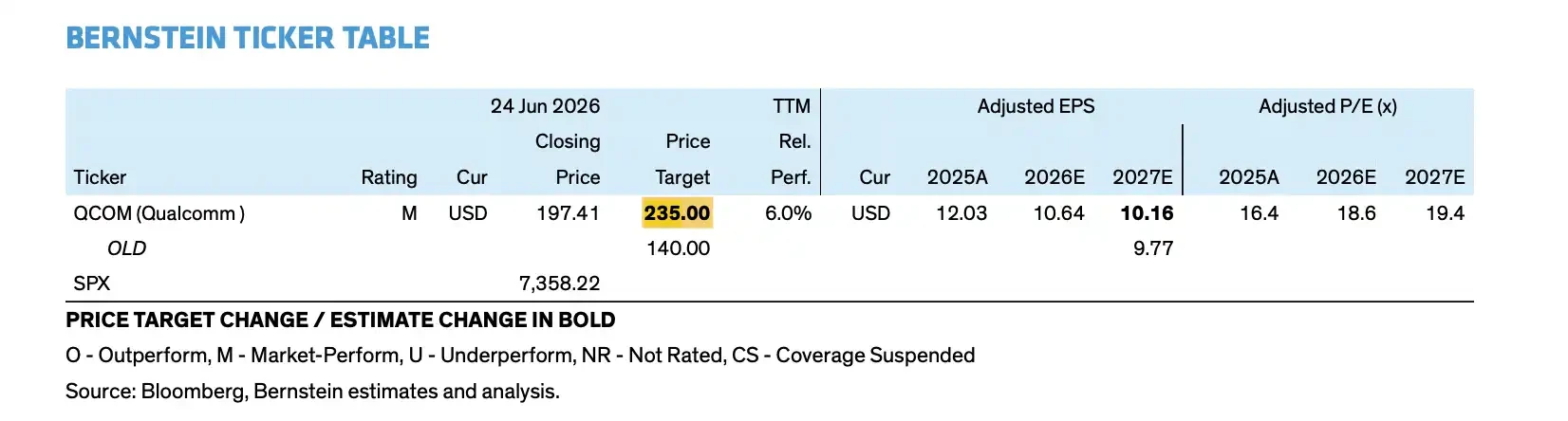

Bernstein raises Qualcomm price target to $235, but why does the rating remain unchanged?

- Core View: Bernstein raised its price target for Qualcomm from $140 to $235, but maintained a "Market Perform" rating. The core rationale lies in recognizing long-term growth targets such as AI data centers (around $400 billion in non-handset revenue for FY2029). However, near-term headwinds including a decline in the handset business, rising operating expenses, and uncertainty over data center gross margins act as constraints, with the risk/reward not clearly skewed towards a buy.

- Key Elements:

- The price target increase stems from incorporating larger data center revenue (over $15 billion by FY2029) and a more diversified structure into the valuation model, with the P/E multiple expanding from 14x to 20x, rather than a significant upward revision in near-term earnings.

- The data center roadmap includes custom ASICs and the Dragonfly C1000 CPU. Two unnamed cloud clients are expected to each contribute over $1 billion in custom silicon revenue by FY2027. The Meta collaboration confirms a non-exclusive, multi-generational CPU partnership.

- Automotive and IoT form the second growth curve, with the automotive design pipeline expanding from $45 billion to $65 billion. FY2029 targets are set at over $10 billion and over $14 billion, respectively.

- The handset business faces pressure: Android revenue for FY2027 is expected to be flat or slightly down. The exit of Apple revenue could reduce handset revenue by $5-6 billion. The compound annual growth rate for Android handset revenue from FY2026 to FY2029 is only around 5%.

- Cost pressures are emerging early: Operating expenses will see double-digit growth in FY2027, while data center revenue recognition lags behind investment. This could lead to downward risk for earnings per share around FY2027.

- Data center gross margins of approximately 40% are below the company average. Overall gross margins could decline from 55.2% in FY2026 to 51.6% in FY2029, impacting earnings quality.

- In a downside scenario, even if data center revenue falls significantly short of the $15 billion target, FY2029 EPS would still be around $15, demonstrating a solid base. However, achieving the target of over $18 EPS depends on client volume ramp-up, stable gross margins, and a smooth transition in the handset business.

TL;DR

- Bernstein raised Qualcomm's price target from $140 to $235, but maintained a Market Perform rating.

- Qualcomm's FY2029 target focuses on data centers, automotive, and IoT, with non-handset revenue targeting approximately $40 billion.

- The decline in the handset business, rising OPEX, and uncertainty around data center gross margins remain the core constraints preventing a rating upgrade.

Price Target Soars, But Rating Doesn't Follow

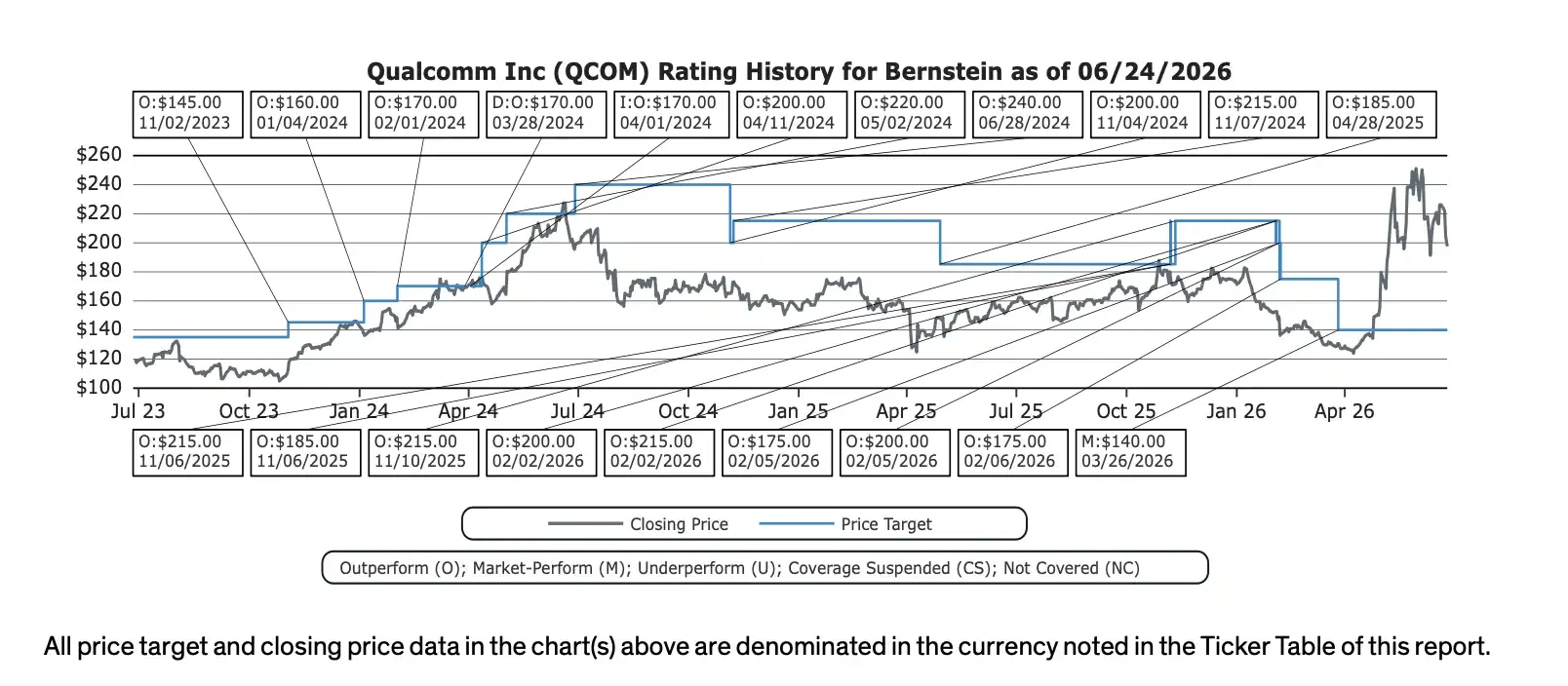

Following Qualcomm's Investor Day in New York, the company presented a larger long-term growth target to the market. Bernstein subsequently raised Qualcomm's price target from $140 to $235, yet maintained a Market Perform rating.

The price target hike indicates Bernstein acknowledges Qualcomm's long-term narrative is expanding. The company is no longer positioning itself solely as a mobile chip supplier but is attempting to enter broader computing markets, including AI data centers, automotive, IoT, and personal AI devices. According to Qualcomm's official targets, by FY2029, the company's non-handset revenue will reach approximately $40 billion, data center revenue will exceed $15 billion, and Non-GAAP EPS will surpass $18.

However, the unchanged rating suggests the sell-side does not believe this narrative is sufficiently certain yet. The real constraint lies in the timing gap: the realization of data center and automotive businesses is further out, while the decline in the handset business, the loss of Apple revenue, increasing OPEX, and gross margin pressure will impact earnings sooner.

This explains why a $235 price target does not equate to a "buy" signal. Bernstein acknowledges the ceiling for Qualcomm's long-term valuation has been raised, but with current stock prices already reflecting some optimistic expectations, the risk-reward ratio has not yet clearly tilted towards buying.

New Narrative: Shifting from Mobile Cycles to AI Data Centers

Qualcomm's most important new story this time is the data center.

The company's official targets show data center revenue exceeding $15 billion by FY2029. Compared to the current data center revenue base of approximately $30 million, this means Qualcomm must genuinely enter cloud vendors' AI infrastructure budgets in the coming years, rather than just staying in the mobile chip and edge computing market.

Qualcomm's disclosed data center roadmap includes custom ASICs, AI inference accelerators, the Dragonfly C1000 CPU, connectivity products, and related software layers. The company also mentioned two unnamed Hyperscaler customers, each expected to contribute over $1 billion in custom silicon revenue by FY2027.

The partnership with Meta is another important validation point. Qualcomm and Meta announced a multi-generational data center CPU collaboration, with the Dragonfly C1000 CPU planned for production in the second half of 2028. However, caution is warranted here: the official statement is that Qualcomm will be one of the suppliers, with the specific amounts, production capacity, and exclusivity not disclosed.

Automotive and IoT form the second growth curve. Qualcomm's official targets show FY2029 automotive revenue reaching $10 billion and IoT revenue exceeding $14 billion. The automotive design-win pipeline has grown from $45 billion 18 months ago to $65 billion, with the company continuing to bet on digital cockpits, assisted driving, and in-vehicle connectivity.

$235 Price Target Bets on 2029, Not Next Year

The core reason for Bernstein's price target increase is not a sudden improvement in Qualcomm's short-term performance, but the valuation model beginning to incorporate larger data center revenue and a more balanced business structure.

According to Bernstein's model, Qualcomm's FY2029 revenue is approximately $64.8 billion, with EPS around $18.12, closely aligning with the company's long-term target of "Non-GAAP EPS exceeding $18." Compared to the past, when the market mainly priced Qualcomm based on mobile cycles, data centers, automotive, and IoT give the company an opportunity to achieve a higher valuation multiple.

The $235 price target corresponds to a higher valuation framework. Bernstein uses an average EPS of approximately $11.75 for FY2027/FY2028 and a 20x P/E valuation; the previous $140 price target corresponded to a multiple of about 14x. In other words, the key to the price target increase is not a significant upward revision in next year's earnings, but the market's willingness to pay a higher multiple for Qualcomm's AI data center and diversified revenue story.

However, this is where divergence lies. Bernstein's model assumes a gross margin of about 40% for the data center business, lower than Qualcomm's current company average. Even if data center revenue scales up, it may not elevate overall profitability in the early stages. The report estimates that due to the changing business mix, Qualcomm's overall gross margin could decline from 55.2% in FY2026 to 51.6% in FY2029.

Handset Pressure Comes First, Data Center Realization Awaits

Qualcomm wants to prove its revenue structure will change with data centers, automotive, and IoT, but pressure on the handset business hasn't disappeared.

According to the sell-side report and management Q&A, FY2027 Android handset revenue is expected to be flat or slightly lower. Coupled with the loss of Apple revenue, total handset revenue could decrease by $5 billion to $6 billion year-over-year. The handset business remains Qualcomm's largest current revenue source, and this decline will directly impact the profit base over the next two years.

The company's long-term assumptions for Android handsets are also more cautious. From FY2026 to FY2029, the compound annual growth rate for Android handset revenue is expected to be about 5%, significantly lower than the high-growth phases in previous cycles. Qualcomm may still maintain advantages in high-end Android phones, AI phones, and RF front-end, but this can hardly fully offset the pressure from Apple's exit and the slowdown in the smartphone industry.

The expense side will also face pressure ahead of time. Qualcomm explicitly stated that FY2027 OPEX will see double-digit growth. To advance data center CPUs, AI accelerators, custom silicon, and the software ecosystem, the company needs to invest early in R&D, sales, and customer support. Revenue recognition typically lags behind investment, meaning that EPS forecasts around FY2027 may actually face downward revision risks.

This is the key reason for the price target increase but unchanged rating: Qualcomm's long-term story is bigger, but the earnings trajectory for the next two to three years may not be smoother. Investors need to accept two judgments simultaneously: FY2029 EPS could be boosted by AI data centers, but earnings pressure around FY2027 is also likely to be more pronounced.

The Disagreement Lies in Whether $15 Billion in Data Center Revenue Can Become Real Profit

Bernstein's report is not simply bearish on Qualcomm; rather, while repricing Qualcomm, it reminds the market not to treat long-term targets as already realized performance.

In a downside scenario, if data center revenue significantly falls short of the $15 billion target and growth in personal AI and computing businesses is also limited, Qualcomm's FY2029 EPS could still reach approximately $15. This shows Qualcomm's fundamentals are not fragile; automotive, IoT, licensing business, and cost control can still support a certain level of profitability.

But the gap between $15 and over $18 in EPS has a significant impact on valuation. If the market has already priced Qualcomm based on more optimistic data center revenue and higher valuation multiples, the company must prove three things: cloud vendor customers can scale as planned; data center gross margins won't persistently drag down overall profitability; and the decline in the handset business won't excessively depress EPS before new businesses materialize.

Therefore, the $235 price target is not a conclusion that "Qualcomm's AI transformation is already successful," but a new price point after incorporating long-term diversification prospects into the valuation. Qualcomm's story is indeed bigger than before, and it looks more like a chip platform company spanning handsets, automotive, IoT, and AI data centers.

However, the Market Perform rating reminds us that until the headwinds in the handset business ease, data center revenue materializes, and gross margins are verified, the market still has reason not to rush into treating Qualcomm as a definitive AI winner. What truly needs verification next is not whether Qualcomm can articulate a $15 billion data center target, but whether this target can translate into revenue on time and ultimately into sufficiently good profits.