Độ "vàng" của hợp đồng dài hạn Micron: Khách hàng đặt cọc trước 22 tỷ USD, hợp đồng không thể hủy bỏ, còn khóa chặt biên lợi nhuận gộp "cao nhất trong lịch sử"

- 核心观点:美光与客户签署的长期战略协议(SCA)通过客户预付220亿美元押金、锁定最低价格与量,将美光从周期性存储供应商转变为拥有高利润下限的长期供应商,此举被三大投行视为“改变游戏规则”,并一致上调目标价。

- 关键要素:

- SCA覆盖约20%的DRAM和三分之一NAND出货量,已签14份协议的最低承诺收入约1000亿美元,预计最终收入将“远高于”此底线。

- 客户需支付合计220亿美元押金(180亿现金+40亿信用证),合同不可取消,押金提高了客户违约成本,为美光需求提供保证金。

- 合同定价框架中的价格下限对应的毛利率“远高于历史峰值”(62%),当前美光毛利率已达84.9%,即使触发底价,盈利水平仍远超历史最好时期。

- 为履行合同,美光将FY26净资本开支指引提高至约270亿美元,长期协议为扩产提供了确定性依据,但产能投放仍是周期变量。

- SCA协议预计将使超过50%的公司收入来自此类合同,其中固定价格或价格区间协议将占约40%的收入,显著提升盈利稳定性。

Original author: Long Yue

Original source: Wall Street News

Customers first pay $22 billion in deposits, sign non-cancelable long-term contracts, and accept a pricing framework far more favorable to Micron than any period in history—these are the core terms of Micron's latest batch of long-term Strategic Customer Agreements (SCAs).

According to information from the Zhui Feng trading desk, on June 25, Barclays, Morgan Stanley, and JPMorgan collectively viewed these as "game-changing" agreements. JPMorgan semiconductor analyst Harlan Sur characterized these SCAs in a research report as a "fundamental transformation" of Micron's business model—from a cyclical commodity supplier to a long-term supplier with multi-year contract protection and significant downside hedging for both revenue and profit.

The value of these contracts lies in: First, the substantial coverage, with signed agreements corresponding to approximately 20% of DRAM volume and about one-third of NAND volume; second, price-volume binding, with 14 agreements, based on minimum commitment volumes and minimum prices, translating to approximately $100 billion in cumulative minimum revenue; third, customers must provide a total of $22 billion in deposits and financial commitments. Fourth, the gross margin corresponding to the contract price floor is "far higher than historical peaks" (the historical peak is approximately 62%), essentially locking in a higher profitability baseline for Micron.

16 Contracts, Covering 20% of DRAM and One-Third of NAND

Micron disclosed that it has signed 16 SCAs, with customers spanning the three major markets of data centers, consumer electronics, and automotive.

Customer distribution includes 4 large customers (market speculation suggests including hyperscale cloud providers and major consumer electronics OEMs), 3 medium-sized customers, and the remaining 9 are smaller customers in the automotive industry.

Contract terms: Data center and consumer electronics contracts are for 5 years, covering 2026 to 2030; automotive contracts are for 3 years.

Coverage scale: These 16 agreements collectively cover approximately 20% of Micron's DRAM shipments and about one-third of its NAND shipments.

According to a Barclays research report, management indicated that once all planned SCAs are fully signed, over 50% of the company's revenue is expected to come from these agreements. Among these, agreements with fixed prices or price ranges are expected to account for approximately 40% of the company's revenue.

$22 Billion Deposits Raise Breach Costs: Customers Pay First, Micron Holds Temporarily, Refunds at Maturity

Under the 16 signed agreements, Micron will receive a total of approximately $22 billion in cash deposits and other financial commitments—$18 billion in unrestricted cash and $4 billion in letters of credit.

These funds are held by Micron, remain on the balance sheet during the contract term, and are returned to customers upon maturity, with a "back-end weighted" return schedule, meaning substantial return occurs only in the latter half of the agreement period.

This money cannot simply be viewed as deferred revenue. Its real function is to increase the cost of customer backtracking.

Regarding the binding force of the contracts, a Morgan Stanley research report directly quoted management's statement from the conference call: "These contracts are non-cancelable." If a customer fails to take delivery according to the agreed volume and price, Micron can take action against the deposit. For Micron, this is equivalent to adding a margin to a portion of future demand for the next few years; for customers, it is the cost of commitment paid for supply certainty.

This also explains why customers are willing to accept price ranges and deposit arrangements. Driven by demand from AI servers, data center SSDs, HBM, and high-end terminal devices, when memory supply is tight, locking in volume itself holds value.

Pricing Structure: Has a Ceiling, but the Gross Margin Locked by the Floor is "Far Higher Than Historical Peaks"

The pricing framework of SCAs falls into three categories: fixed prices, price ranges with upper and lower limits, or floating within a similar range referencing market prices.

Regarding the price ceiling: For existing products, the price ceiling references the market price of the second quarter of 2026. This clause was interpreted by some market participants as Micron "actively capping the upside potential," which has sparked some divergence of opinion.

But the price floor part is the real highlight: The gross margin corresponding to the floor is "far higher than the peak profitability of any historical cycle." Micron's past peak gross margin was approximately 62%, while the current gross margin has reached 84.9%—meaning even if the floor price clause is triggered, Micron's profitability level remains far higher than its best historical period.

However, SCA is not a "prices always go up" contract. Some existing products have set price ceilings, with the ceiling anchored to the market price of the second quarter of 2026. In other words, Micron has traded off part of its future pricing flexibility for higher revenue certainty and a gross margin floor.

Analyst Joseph Moore commented on this, stating that while "the contract price ceiling being flat with the Q2 price" indeed raises concerns about "the company capping its ceiling," he also pointed out that gross margins are approaching 90% and are expected to remain in that range for a considerable period—it is reasonable for counterparties to seek some protection in negotiations, and the duration of the contract is the core dimension for assessing its value.

$100 Billion Revenue Floor, and It's Just the "Minimum"

Of the 16 agreements, 14 have clearly defined price terms.

According to Barclays and JPMorgan research reports, the total minimum committed revenue (Remaining Performance Obligations, RPO, calculated based on minimum committed volume and price) for these 14 agreements is approximately $100 billion.

Management explicitly stated that actual revenue is expected to be "far higher" than this floor—because this $100 billion is only the guaranteed value calculated at the floor price. If market prices exceed the floor price, revenue will naturally increase accordingly.

For new products, the agreements also retain additional pricing upside.

Expansion Still Needed Behind the Long-Term Contracts, CapEx Hasn't Disappeared

Locking in demand does not mean automatic delivery.

Micron has raised its FY26 net capital expenditure guidance to approximately $27 billion, up from around $25 billion earlier. FY27 quarterly capital expenditure is expected to be higher than the FQ4 level, with over half of the year-over-year increase coming from construction-related CapEx for early investment in cleanroom capacity.

This indicates that SCAs do not lead to an asset-light model, but rather provide a more certain rationale for expansion.

Customers are willing to put up deposits, and Micron also needs to invest capital. Long-term contracts provide a stronger basis for expansion. However, if future demand or prices deviate, capacity deployment can still become a cyclical variable.

Behind the Three Major Institutions' Consensus Upgrade of Target Prices, the Market is Re-evaluating "How Long Peak Profits Can Last"

All three institutions raised their target prices for Micron, but the core logic extends beyond the Q3 May quarter earnings beat.

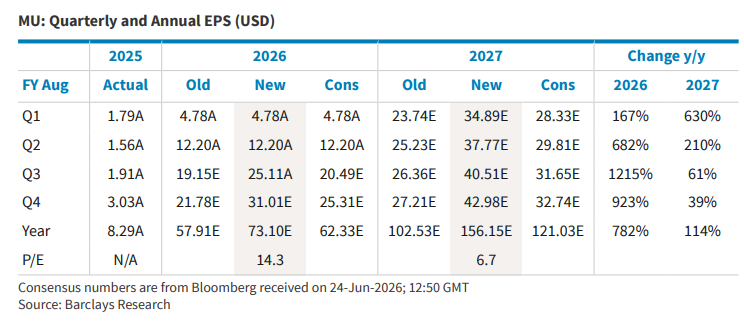

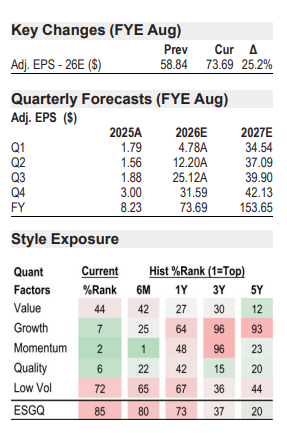

Barclays (Analyst Tom O'Malley): Target price raised from $1,175 to $2,000, based on 12x CY27 EPS of $166.74. The report states that SCA details are "better than expected," viewing these agreements as "materially positive for downside protection," while supply-demand imbalances are unlikely to fade in the short term, leaving room for upside.

Morgan Stanley (Analyst Joseph Moore): Target price raised from $1,050 to $1,200, based on 30x through-cycle earnings power ($40 per share). The report raised the through-cycle earnings estimate from $35 to $40 per share, citing the earnings run rate approaching $200/share.

JPMorgan (Analyst Harlan Sur): Target price significantly raised from $550 (Dec 2026 target) to $1,540 (Dec 2027 target), based on 10x (median P/E over 10 years) FY28 EPS of $154. The report characterized the SCA expansion as a "step-function change," fundamentally altering the nature of Micron's business model.

Behind these model changes, the key variable is profit sustainability.

Micron's Q3 May quarter revenue reached $41.456 billion, up 73.7% quarter-over-quarter; the midpoint of the Q4 August quarter revenue guidance is $50 billion, and the midpoint of non-GAAP EPS guidance is $31. Quarterly figures are already very high, but the SCAs pose another question for the market: If prices stop rising rapidly, can Micron still maintain high gross margins and high free cash flow?

The current framework suggests: A portion of revenue has stronger protection, but not all revenue. Price ceilings, future expansion plans, and the sustainability of AI demand remain boundary conditions.

Deposits and Cash Flow Open Up Capital Return Possibilities, But Timing is Restricted

The SCAs also bring a change to the balance sheet: Deposits will flow into Micron's hands. Although these must eventually be returned to customers, they will increase the cash scale in the short term.

As of the Q3 May quarter, Micron held approximately $26 billion in cash and investments; operating cash flow for the quarter was $25.4 billion, and adjusted free cash flow was $18.3 billion. The Q4 August quarter is also expected to receive approximately $10 billion in customer cash deposits.

The path for capital returns is also becoming clearer. Restrictions related to the U.S. CHIPS Act currently limit Micron's short-term buyback capacity; after December 9, 2026, as these restrictions expire, the company's stated direction is to gradually return 100% of excess cash to shareholders, with buybacks being the primary method.

This part is not a direct revenue contribution from the SCAs, but it is another aspect of how SCAs change the market narrative: If high profits are sustained and cash accumulates rapidly, Micron may no longer just be "earning cyclical money" but could enter a more stable cash return framework.

The Earnings Report Itself: Record High Gross Margin, Next Quarter Guidance Beats Expectations Again

Beyond the SCAs, Micron's Q3 FY3Q26 (May quarter) earnings data was equally strong:

- Revenue of $41.456 billion, up 73.7% quarter-over-quarter, significantly beating market expectations of $35.6 billion

- DRAM revenue of $31.3 billion (up 67% QoQ), NAND revenue of $9.9 billion (up 99% QoQ)

- Average DRAM selling prices rose approximately in the low 60% range quarter-over-quarter, average NAND selling prices rose approximately in the mid-80% range quarter-over-quarter

- Gross margin of 84.9%, a record high, exceeding market expectations of approximately 81.8%-81.9%

- Earnings per share of $25.11-$25.12, significantly beating market expectations of approximately $20.49

Q4 FY4Q26 (August quarter) guidance:

- Revenue guidance midpoint of $50 billion, higher than market expectations of approximately $43.1-$43.6 billion

- Gross margin guidance of approximately 86%, continuing to exceed market expectations

- Earnings per share guidance midpoint of $31.00, higher than market expectations of approximately $25.31-$25.72